Home Depot's Quiet Resilience: Reading the Q1 FY2026 Signal

Revenue beats, margin compression, and an SRS-powered Pro pivot — what the numbers tell investors about America's largest home improvement retailer in a frozen housing market.

01 / Executive Summary

A Company Navigating Two Cycles at Once

Earnings Beat Guidance Reaffirmed Margin Pressure

Home Depot entered fiscal 2026 carrying the weight of the most consequential acquisition in its history — the $18.25 billion purchase of SRS Distribution — and a housing market that remains structurally impaired by the mortgage rate lock-in effect. Its Q1 FY2026 results, reported on May 19, 2026, tell the story of a company that is executing well on its strategic pivot toward professional contractors while waiting, patiently, for the residential housing cycle to turn.

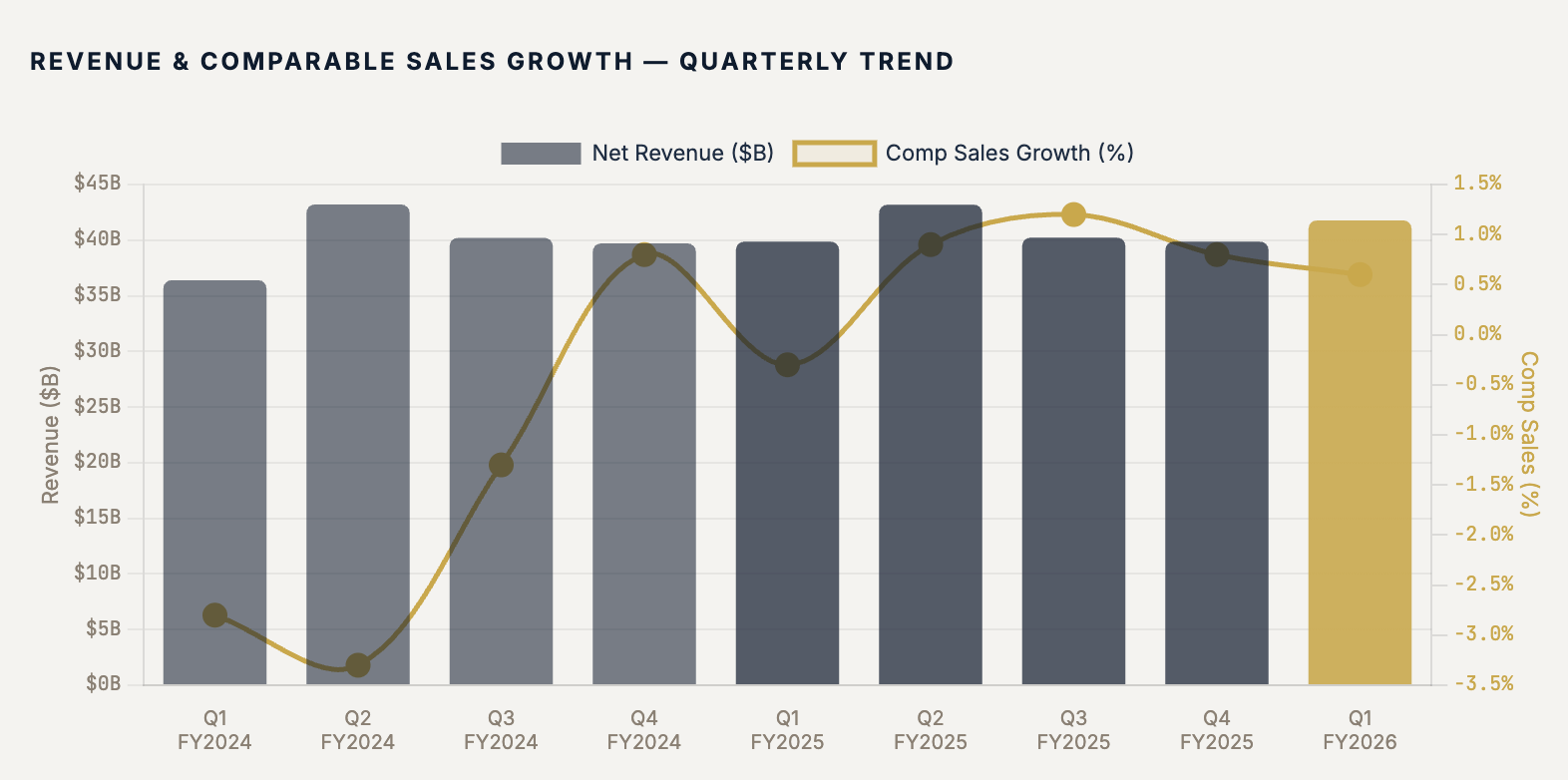

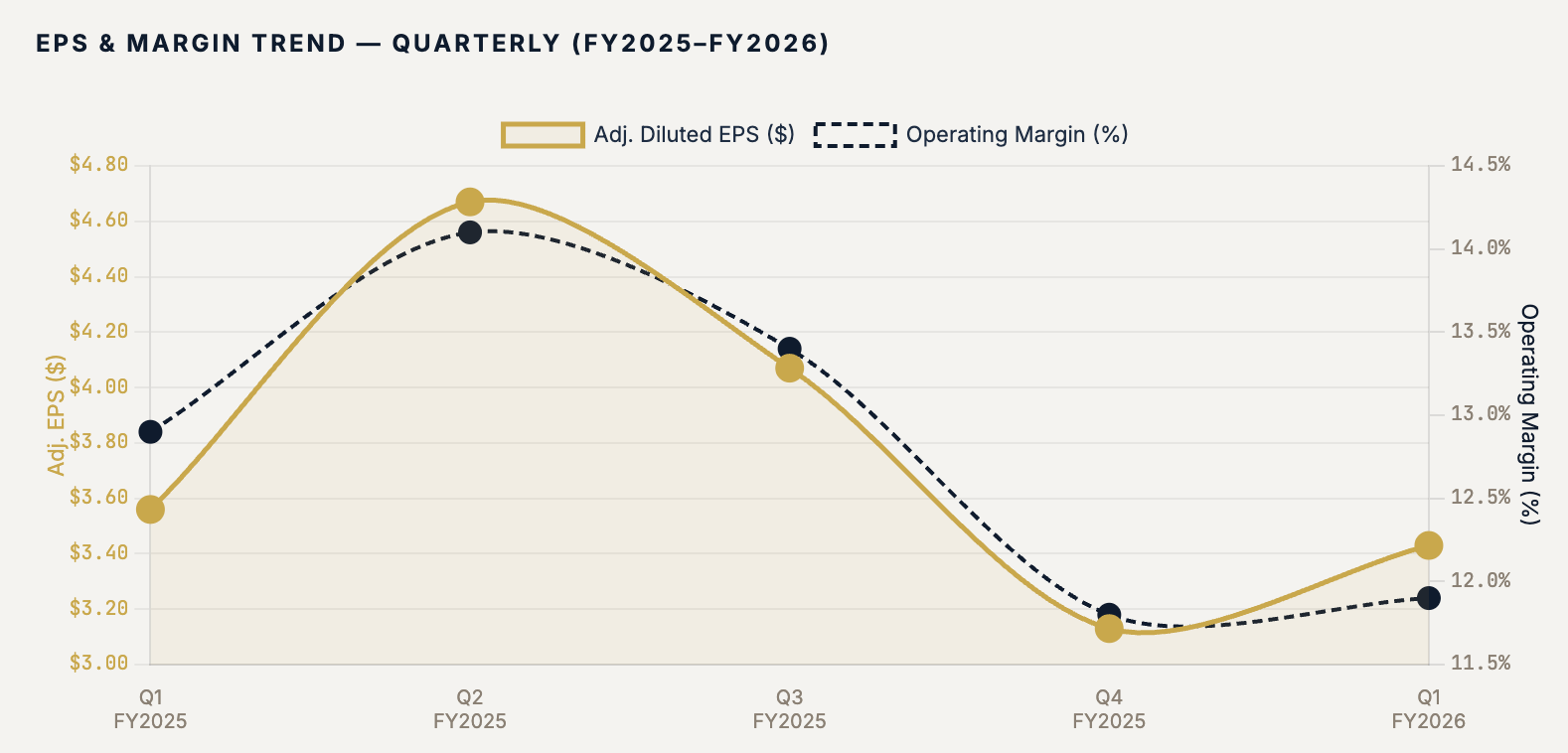

The headline numbers cleared Wall Street’s bar: net sales of $41.77 billion beat the $41.52 billion consensus estimate, rising 4.8% year over year. Adjusted diluted EPS came in at $3.43, a cent above the $3.41 consensus, even as GAAP diluted EPS fell to $3.30 from $3.47 in the prior-year quarter. Comparable sales grew 0.6%, turning positive after a decline of 0.3% in Q1 FY2025, though the result fell short of the 0.9% comp growth analysts had projected — a soft spot that weighed on the stock’s initial reaction. Management reaffirmed full-year FY2026 guidance, calling for total sales growth of 2.5%–4.5% and comp growth in the range of flat to +2%.

Beneath the headline, the story is richer. SRS Distribution contributed approximately $2.6 billion in revenue in the quarter, acting as both a structural volume driver and a margin headwind — gross margin compressed 75 basis points to 33.0%, largely reflecting the lower-margin distribution model that SRS operates. Operating income fell 3% to approximately $4.98 billion, and operating margin contracted from 12.9% to 11.9%. The message from CFO Richard McPhail was unambiguous: the margin compression is understood, expected, and a deliberate trade-off for long-term Pro penetration. CEO Ted Decker, for his part, described demand conditions as “relatively similar to what we saw throughout fiscal 2025” — not inspiring, but stable.

The real story of Q1 FY2026 is one of two timelines. On the short timeline, Home Depot is navigating a housing market in suspended animation, where 30-year mortgage rates hovering near 6.4% have frozen homeowner mobility and crimped enthusiasm for large discretionary renovation projects. On the long timeline, the company is methodically assembling the most comprehensive professional contractor ecosystem in North American retail history — a “supply house” model that could prove enormously valuable when housing turnover eventually recovers. Investors who can hold both timelines in mind simultaneously will find this quarter genuinely informative.

02 / Q1 FY2026 Financial Results

Revenue Beats Expectations; Margins Tell a More Complex Story

First-quarter fiscal 2026 net sales of $41.77 billion represent a 4.8% increase over the $39.86 billion recorded in Q1 FY2025. Strip out SRS Distribution’s approximate $2.6 billion contribution and underlying organic growth runs closer to flat — a sober reminder of how much of the revenue expansion is acquisition-driven rather than same-store demand improvement.

Comp Sales: Positive, but Softer Than Expected

Comparable store sales rose 0.6% globally and 0.4% in the United States — turning positive for the first time after two consecutive negative comp quarters. However, the result missed the 0.9% consensus estimate. Foreign exchange translation added approximately 55 basis points to the total comp figure, meaning domestic organic comp performance was essentially flat. Northern and Western divisions drove most of the positive momentum as favorable spring weather encouraged outdoor project activity. The Southern divisions lagged, reflecting ongoing housing affordability constraints.

Customer transactions at retail locations reached 391.1 million, with comparable transactions down 1.3% — meaning fewer customers visited stores. The offset came from average ticket growth of 2.3%, lifting per-transaction spend to $92.76. Transactions above $1,000 grew 0.8%, signaling that high-value Pro and semi-Pro customers are engaged even if the casual DIY shopper remains cautious. Larger discretionary projects — kitchen and bath remodels, deck replacements, whole-home painting — remain under pressure as homeowners defer commitments pending rate clarity.

Earnings Per Share: Beat on Adjusted, Decline on GAAP

Adjusted diluted EPS of $3.43 cleared the $3.41 consensus by $0.02, but represents a 3.7% decline from $3.56 in Q1 FY2025. GAAP diluted EPS fell to $3.30 from $3.45. The divergence between reported and adjusted figures reflects integration-related expenses tied to the SRS/GMS acquisitions. The full-year adjusted EPS guidance range of flat to +4% versus FY2025’s $14.69 implies a full-year target band of approximately $14.69–$15.28.

“The underlying demand in our business was relatively similar to what we saw throughout fiscal 2025, despite greater consumer uncertainty and housing affordability pressure.”

— Ted Decker, CEO, Home Depot Q1 FY2026 Earnings Call

Gross Margin Compression: The SRS Toll

Gross margin contracted 75 basis points to 33.0% from 33.75% in Q1 FY2025. Management explicitly attributed the majority of this decline to mix shift — specifically the inclusion of SRS and the recently completed $5.5 billion GMS acquisition (completed September 4, 2025), both of which carry structurally lower gross margins than Home Depot’s core retail operation. Shrink improvements and supply chain productivity provided partial offsets. For the full year, management guided gross margin to approximately 33.1%, broadly consistent with original guidance.

03 / The SRS Effect

A $18 Billion Bet on the Professional Contractor Economy

No analysis of Home Depot’s current financials is complete without understanding the SRS Distribution acquisition — arguably the most transformative deal in the company’s 47-year history. Home Depot closed the $18.25 billion purchase of SRS Distribution in June 2024, adding a national distributor that serves roofing, landscaping, and pool professionals across more than 760 branch locations in North America. In Q1 FY2026, SRS contributed approximately $2.6 billion to total revenue, making it the single largest driver of the company’s year-over-year sales growth.

SRS Distribution — At a Glance

Purchase price: $18.25 billion (June 2024) · Branches: 760+ · Verticals: Roofing, Landscaping, Pool · Q1 FY2026 Revenue: ~$2.6B · FY2026 Organic Growth Target: Mid-single digits · Cross-sell run-rate target: ~$400M in FY2026. SRS also completed the acquisition of Mingledorff’s in early 2026, adding HVAC distribution capabilities.

The strategic logic is straightforward: professional contractors — roofers, landscapers, pool builders, general contractors — represent a fundamentally different and more valuable customer than the weekend DIY enthusiast. Pros spend roughly three times more per trip, visit stores far more frequently, and are far less sensitive to housing market cycles because they work on both new construction and the replacement/repair segment. SRS gives Home Depot a direct supply relationship with these customers outside of the traditional retail store model — a “supply house” model that resembles wholesale distribution more than big-box retail.

The GMS Addition Deepens the Moat

Just months after closing SRS, Home Depot announced and subsequently completed (September 4, 2025) the $5.5 billion acquisition of GMS Inc. through SRS Distribution — adding a leading distributor of wallboard, ceilings, steel framing, and complementary building materials operating over 300 distribution centers and nearly 100 tool sales and rental centers across the US and Canada. GMS fills a critical gap: the interior commercial and residential construction supply segment, where contractors need consistent, large-format access to commodity building materials. Together, SRS + GMS gives Home Depot a multi-category distribution platform covering the exterior envelope (roofing), hardscape and softscape (landscaping, pool), HVAC (via Mingledorff’s), and interior structure (GMS) — essentially the full Pro construction supply stack.

Cross-Sell Runway Is the Long Game

Management guided to approximately $400 million in cross-sell run-rate revenue for FY2026, leveraging the combined Home Depot / SRS / GMS customer relationships. This figure, while modest relative to total revenue, is expected to compound significantly as the integrations mature. The thesis: a roofing contractor who buys shingles through SRS can be introduced to Home Depot’s Pro Xtra loyalty program, its B2B purchasing platform, and its tool and equipment rental offering — deepening wallet share across all of a contractor’s project needs. Management described SRS as “an engine for growth” across all three business verticals, and expressed confidence in the mid-single-digit organic growth trajectory for the SRS segment in FY2026. New store openings of approximately 15 traditional Home Depot locations and 40–50 new SRS branch locations are planned for the year.

04 / Housing Market Headwinds

The Mortgage Lock-In Effect: Why 6.4% Rates Freeze Home Improvement

To understand Home Depot’s current performance — and its near-term ceiling — you need to understand the single most important macro variable for the home improvement sector: housing turnover. When Americans move, they buy new furniture, upgrade fixtures, repaint rooms, replace flooring, and renovate kitchens. Home Depot estimates that a home purchase triggers roughly $8,000–$10,000 in incremental home improvement spend in the first two years. In a market where existing home sales are suppressed, that spending simply does not materialize at scale.

The Lock-In Trap

As of mid-May 2026, the 30-year fixed-rate mortgage averaged 6.36%, according to Freddie Mac data — down from 6.81% a year ago, but still far above the 2.5%–3.5% rates that characterized the pandemic-era refinancing wave. Fannie Mae forecasts that rates will hover around 6.2%–6.3% through the end of 2026 and into 2027, never reaching the psychological 6.0% threshold. The result is a phenomenon economists call the “rate lock-in effect”: homeowners who refinanced at sub-3% rates in 2020–2021 face an enormous financial penalty — often hundreds of dollars per month — if they sell their homes and take on a new mortgage at prevailing rates. An estimated 60%+ of outstanding US mortgages carry rates below 4%, creating a powerful disincentive to move.

The Consequence for Home Depot

The housing turnover constraint manifests most directly in large discretionary project categories: kitchen remodels, bathroom renovations, whole-home flooring replacements, deck construction. These projects — which carry average tickets in the thousands of dollars — are most commonly triggered by either a home purchase (the “I’m making this place my own” impulse) or a sale preparation (”I need to improve curb appeal before listing”). With both motivators dampened, these high-margin categories remain sluggish. CFO Richard McPhail acknowledged as much on the earnings call: “They continue to tell us that they are going to defer their spend on larger projects.” The “they” in that sentence — homeowners surveyed by management — are waiting for rate relief that Fannie Mae suggests may not arrive in a meaningful way in 2026.

Yet the picture is not uniformly bleak. Repair and maintenance spending — the unglamorous but resilient category of leaky roofs, broken HVAC systems, and worn-out appliances — does not require a trigger event. It is need-driven, not want-driven. Home Depot’s exposure to this category, amplified by SRS’s roofing distribution business and GMS’s wallboard and framing supply, provides a meaningful structural floor for demand even in low-turnover environments. The spring seasonal uplift was also visible in Q1, with Northern and Western divisions reporting positive comps as homeowners tackled outdoor projects. The underlying demand story is one of bifurcation: essential repairs holding, discretionary renovations deferring.

“They continue to tell us that they are going to defer their spend on larger projects.”

— Richard McPhail, CFO, Home Depot Q1 FY2026 Earnings Call

05 / Pro vs. DIY: The Split