AI: The Divergence

AI's productivity dividend is real. The argument is no longer whether it exists — but who is allowed to keep it.

For two years the debate about artificial intelligence and work was a debate about magnitude. Would it add a percentage point to productivity, or ten? Would it erase a few million jobs, or reorganize a few hundred million? In mid-2026 the magnitude question is quietly being settled — the gains are real, modest in aggregate, and accelerating — and a harder question is moving to the center of the table. Not how big the dividend is. Who gets to keep it.

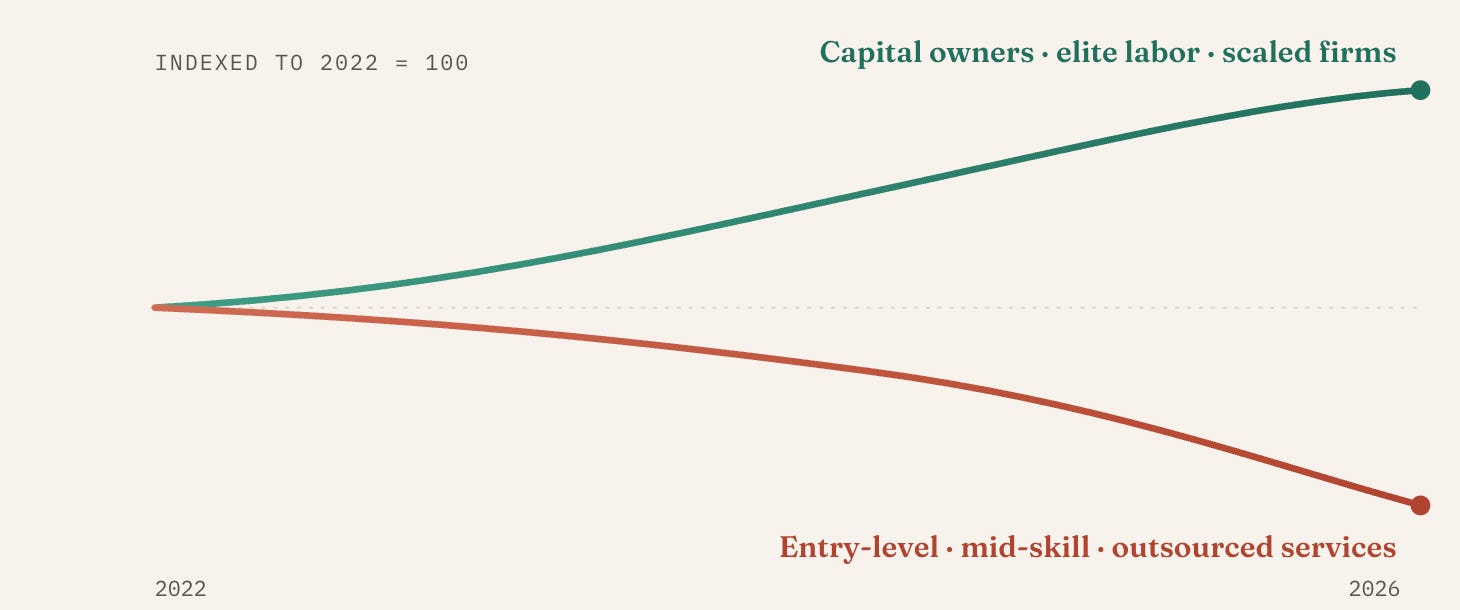

Same shock, opposite vectors. A stylized rendering of the central claim: a single technology pulling two cohorts apart. The numbers behind each line follow below.Illustrative. Underlying figures sourced throughout this note.

The honest answer, on today’s evidence, is that the dividend is not being shared evenly — and that the unevenness has a recognizable shape. The same tool that lifts one worker’s wage erodes another’s bargaining power. The same automation that fattens a software firm’s margin hollows out a call-center contract. To a first approximation, AI is behaving less like a rising tide and more like a sorting machine: it routes surplus toward whoever already owns scale, judgment, or capital, and away from whoever sold standardized effort by the hour.

That is the thesis of this note. But we want to be careful, because the data does not march in one direction — and the most interesting evidence actively cuts against the two-tier story. We’ll give that counter-evidence its full weight before arriving, deliberately, at a conclusion that stays a question. This is not a polemic. It is a ledger — and ledgers require both columns.

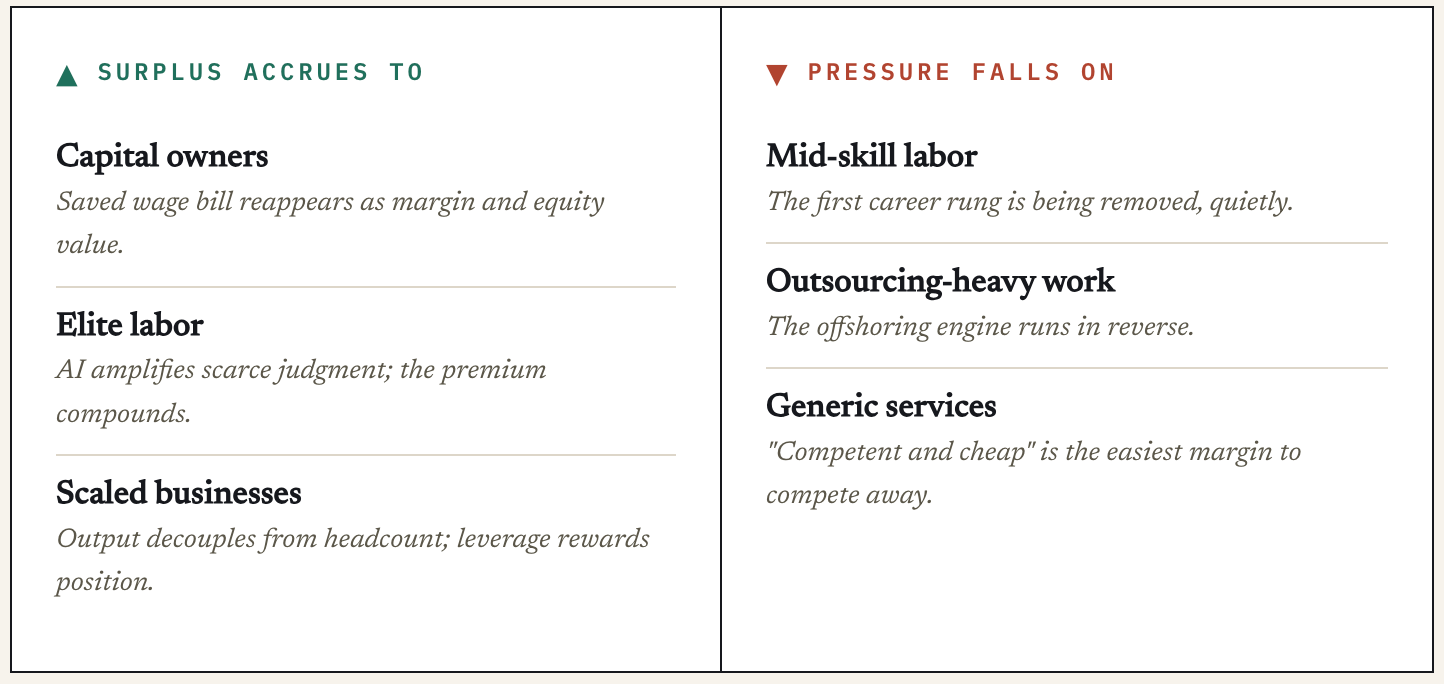

§ 01 — The Winners

Where the surplus is pooling

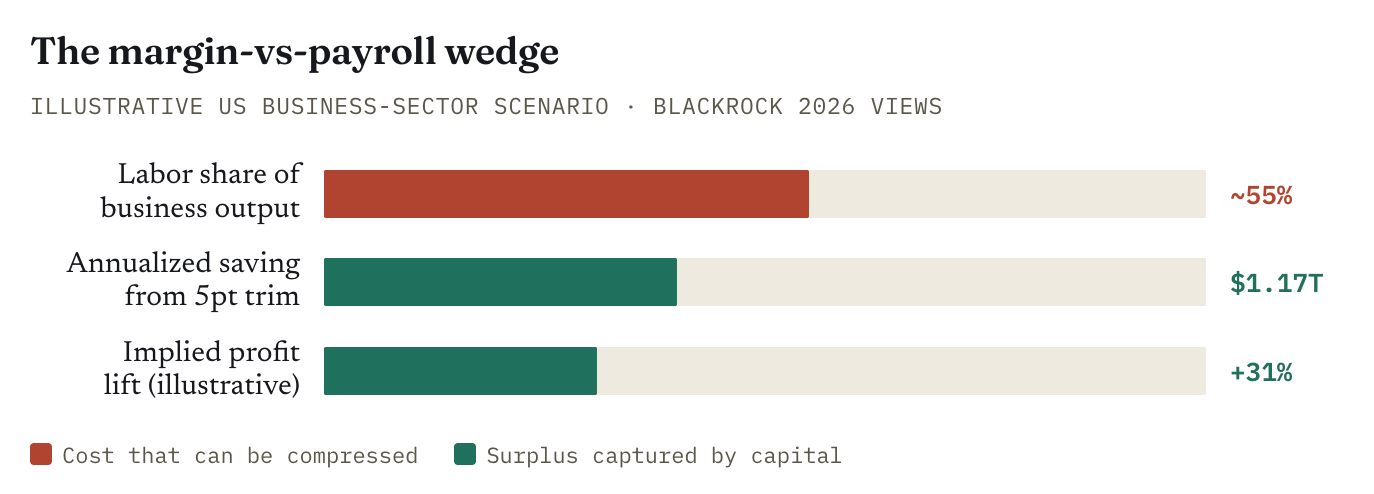

Start with the cleanest signal, because it is an accounting identity before it is an argument. When a firm produces the same output with less labor, the saved wage bill does not evaporate — it reappears as margin. BlackRock’s 2026 investment outlook spells out the arithmetic with unusual bluntness: labor costs run roughly 55% of US business-sector output, so an illustrative 5% trim to labor’s share of costs would free on the order of $1.17 trillion annually — flowing, the bank notes, straight into corporate profitability. Against a US corporate profit base now above $3.5 trillion annually (Bureau of Economic Analysis, full-year 2025), that kind of margin expansion represents a structural shift in who receives the output of American enterprise. BlackRock observes that 2025 already showed output growing faster than hiring, “an early signal that productivity is doing more of the work.” That is the winners’ column in one sentence: output is decoupling from headcount, and the gap is being booked as profit. Profit accrues to capital. Capital is the first tier.

This is not a hypothetical. The S&P 500’s blended net profit margin hit 13.2% in Q4 2025 — the seventh consecutive quarter above 12% — even as aggregate employment growth decelerated. The index itself has become a concentration instrument: the ten largest constituents, all AI-linked, now represent roughly 37% of S&P 500 market capitalization, the highest concentration in the postwar era. The equity market is effectively an AI-leverage instrument for whoever owns it — and in the United States, the top 10% of households own approximately 93% of directly held equities. The productivity surplus is, in its first distribution, almost entirely a windfall for that cohort.

The academic literature has caught up to the identity. A strand of recent work characterizes generative AI as a capital-biased innovation — one that allocates a growing share of technological gains to capital rather than labor. A CEPR analysis across 238 regions in 21 European countries finds intensifying AI innovation correlated with declining labor-income shares, most sharply in industrial areas. The important caveat: this data covers the period 2000–2017, predating the generative AI era. It measures the distributional effects of the earlier wave of automation and narrow AI. If capital-bias held for that technology, there is little in the structure of large language models to suggest it reverses for this one — and everything in the current earnings data to suggest it is intensifying. The International AI Safety Report’s 2026 edition reaches the same destination from the top down: AI adoption “may shift earnings from labour to capital owners, such as shareholders of firms that develop or use AI.”

The second tier of winners: elite labor

Not every winner owns equity. The NBER’s 2026 survey of nearly 750 corporate executives finds labor-productivity gains that are positive, sector-dependent, and concentrated in high-skill services and finance — and, tellingly, “not primarily driven by capital deepening.” Translation: the gains accrue to the people whose judgment AI amplifies rather than replaces. The signal in compensation data is becoming readable: median total compensation for AI and ML engineers at large US technology firms crossed $450,000 in 2025, up from roughly $260,000 in 2022, a 73% increase over three years while inflation ran at an annualized 3–4%. The premium sits on top of an existing skill, which is precisely why it widens the gap rather than closing it. AI is not creating a new middle class of AI workers — it is making the existing top of the skills distribution disproportionately more valuable, at an accelerating rate.

The effect extends beyond technology workers. A senior partner at a law firm who can now run the analysis that previously required four associates is worth more to the firm. A managing director at a bank whose AI stack produces equity research at twice the speed is more valuable than her predecessor. A physician who can see 30% more patients without administrative burnout, because AI handles documentation, is more productive. In each case, the AI premium accrues to the person who already had the most valuable skill. The Matthew effect — to him that hath, more shall be given — has a technological engine now.

The third tier: scaled and scalable businesses

The most novel winner is structural. When execution gets cheap, the binding constraint on a business shifts from headcount to judgment — and a small number of operators can suddenly run what used to require a department. The solopreneur economy is the visible edge of this: solo-founded firms rose from roughly 24% of US startups in 2019 to over 36% by mid-2025, according to Carta data. AI adoption among solo founders has reached an estimated 74% according to industry surveys — though that figure should be treated as directionally reliable rather than precisely measured, absent a single definitive primary survey.

It would be a mistake to romanticize this. The same reporting that celebrates the “one-person company” concedes that a tiny fraction of solopreneurs currently clear $1M in revenue — AI “changes the productivity ceiling, not the market dynamics.” The honest reading is narrower and more important: AI lowers the floor for experimentation and lets whoever finds product-market fit scale without bleeding margin into payroll. That advantage compounds for firms that are already scaled. The one-person company that clears $1M is exceptional; the 500-person company that grows to $1B without adding 200 more employees is the more consequential story. Which is the point — leverage rewards those already positioned to use it.

When execution becomes cheap, the prize migrates to whoever owns the scarce input: capital, distribution, or judgment.

§ 02 — The Losers

Where the floor is dropping out

If the winners’ story is about capture, the losers’ story is about position — specifically, the structural position of selling standardized cognitive effort. Three cohorts sit directly in the blast radius, and the damage is concentrated enough in each to be measured but diffuse enough in aggregate to be invisible in headline unemployment figures.

Mid-skill and the vanishing first rung

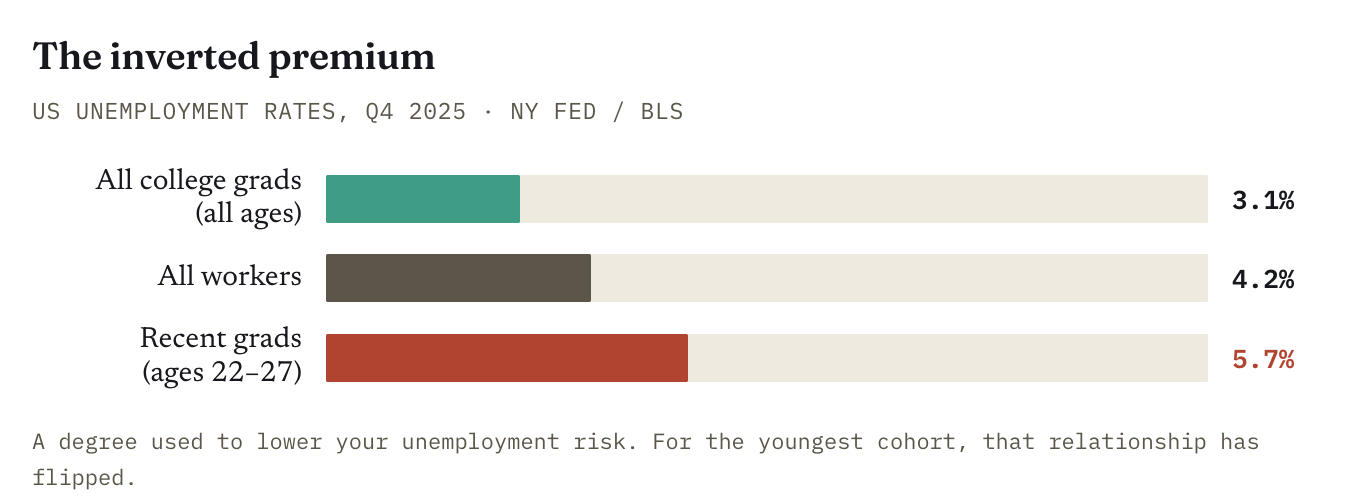

The single most robust labor signal in 2026 is not a layoff wave. It is a hiring freeze at the bottom. Unemployment for recent US graduates aged 22–27 sits near 5.7% against roughly 4.2% for all workers — an inversion of the historic college wage premium that the New York Fed has been tracking since late 2024. Underemployment among new graduates runs near 42%, the highest since the pandemic. Entry-level job postings have fallen approximately 35% since early 2023, according to Revelio Labs data tracking over 100,000 monthly listings — and for highly AI-exposed entry-level roles, the decline exceeds 40%.

The mechanism matters more than the magnitude. As one widely-cited synthesis of the data puts it: AI “isn’t taking the job you already have; it’s taking the job you were going to be hired into.” The Dallas Federal Reserve documented a roughly 13% relative decline in employment entry-rates for AI-exposed young workers aged 22–25 since late 2022. Young-developer employment is off nearly 20% from its late-2022 peak. Mid-career incumbents keep their seats; the aggregate unemployment rate barely twitches. The damage is hidden in a flat headline, concentrated on the rung people used to climb onto — and invisible to economists measuring the stock of employment rather than the flow into it.

The outsourcing engine, running in reverse

The most concentrated damage is offshore. The traits that made business-process work easy to offshore — repetition, predictability, scale — are exactly the traits that make it easy to automate. Two decades of recorded calls, standardized scripts, and digitized workflows are now training data. India’s top five IT firms (TCS, Infosys, Wipro, HCLTech, and Tech Mahindra) added a net 17 employees across the first nine months of fiscal 2026, compared to roughly 17,764 net additions in the same period a year earlier — a near-total collapse in entry-level demand that is concentrated in exactly the junior tiers that historically served as India’s technology-employment ladder.

In the contact-center sector, Gartner projected in 2022 — a forecast the current evidence suggests is arriving roughly on schedule — that conversational AI would cut contact-center labor costs by $80 billion globally by 2026 by automating roughly one in ten agent interactions. In the Philippines, where the IT-BPM industry employs approximately 1.82 million professionals and contributes roughly 8–9% of GDP, providers are racing to deploy the tools that threaten their own model.

There is a darker macro twist here, flagged in the Safety Report: by making domestic automation cheaper than offshore labor, AI may remove the incentive to offshore at all — foreclosing the development ladder that lifted a generation of middle-income economies. The loss isn’t just jobs; it’s a growth strategy that took thirty years to build and may dissolve in a single technology cycle. For countries like the Philippines, India, and Vietnam whose middle classes were assembled in significant part through BPO employment, this is not a labor market adjustment — it is a development-model crisis.

Generic services and the commodity trap

The third loser is any service whose value proposition was “competent and cheap.” Salesforce has attributed thousands of eliminated support roles to AI handling roughly half of inbound queries. Amazon’s ongoing restructuring has cut tens of thousands of corporate and warehouse-coordination positions since late 2025. The pattern is consistent: where the output is standardized and the quality bar is “acceptable rather than excellent,” the human margin is the first thing competed away. What survives, as the industry’s own analysts concede, is the complex, judgment-heavy remainder — higher-value work that plays to depth, not volume. Good news for the deep. Cold comfort for the broad.

§ 03 — The Industry Map