Airbnb: Saved, not killed by the pandemic.

Airbnb: Saved, not killed by the pandemic.

How Airbnb got even stronger from the worse thing that could have happened to them

Airbnb was founded in 2008 by Brian Chesky, Nathan Blecharczyk, and Joe Gebbia. It started as a simple idea, the founders came up with the idea of putting an air mattress in their living room and turning their home into a bed and breakfast. They quickly built a website and offered a short term living space with breakfast included, in what was a saturated hotel market in San Francisco. The company was then named Air Bed and Breakfast. The name comes from their origins as an air mattress in the living room. Since then, the company has grown very fast and it is now present all over the world, giving them a current valuation of close to $70b. At the start of the pandemic , the company found itself in a very difficult position, travel was greatly limited, their IPO was not yet launched and they needed liquidity to hold through the worst of the pandemic, they raised money in the debt markets with very high costs, all to see the other side of the pandemic. Was in 2021 that everything turned for Airbnb and now it finds itself in a very different position and a very different world. These are new customer behaviors, that if they are here to stay, they could be very beneficial for Airbnb for years to come. This week we go in detail into Airbnb to understand how good the opportunity is, for them and for their investors.

Business Model:

Revenue Streams & Operational Model:

Airbnb is a platform where homeowners can post and offer their home for rental . There are many types of lodging options for homeowners, or “Hosts”, as Airbnb calls them. Some of these types are:

Entire home

Individual Room

Tent

RV

Cabins

Private Islands

And many more you could include as a host almost any type of property in their platform (or website) as long as it is legal in the country that is being posted.

In terms of timing hosts can offer their properties for short stays, similar to what is most common with hotels, or for very long stays, week, months, quarters etc.

Every host names their price but market forces make sure that this remains sensible to the value the host is offering (also Airbnb tries to help by offering price suggestions that could help maximize revenue). Every host can set different prices for different dates and different length of stays. Every host sets their rules in terms of free cancellation, on how much the cleaning fee will be, when is the time of arrival, time of check out, etc.

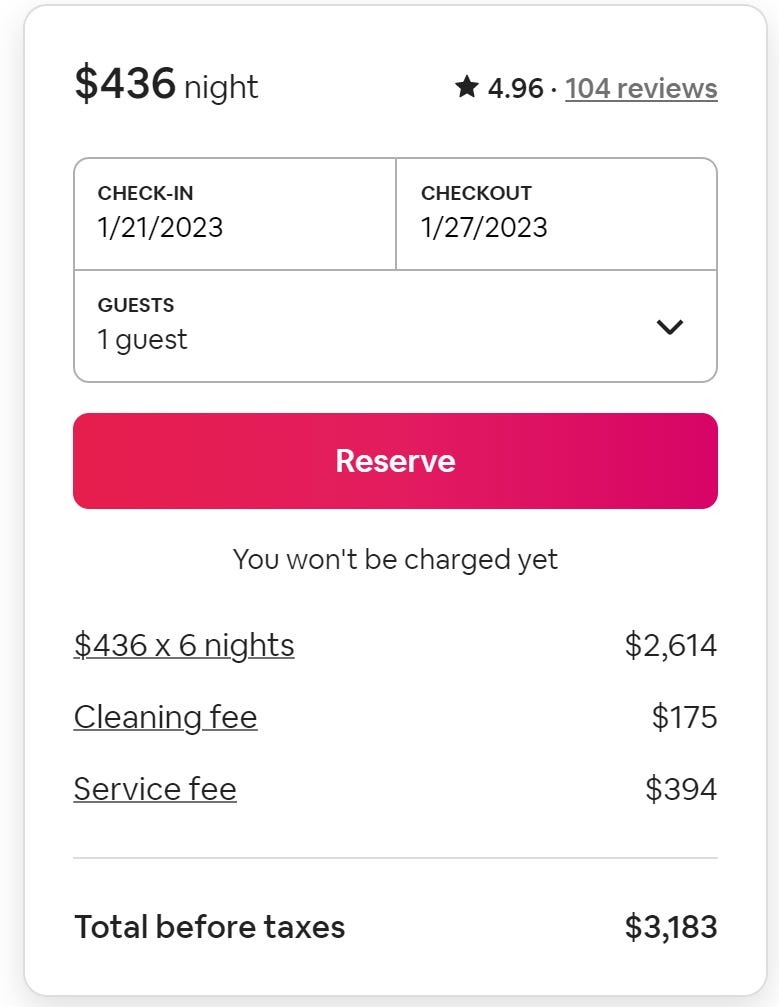

On the customer side, he or she will see three main items that are being charged:

Night fee: This is the fee that the host is charging to stay at their property

Cleaning fee: One-time fee charged by the host to cover the cost of cleaning their space

Service Fee: This is basically Airbnb cut on the service, basically their right to use their platform.

Airbnb makes their money from the service fee it charges the guest, it is usually a fee of around 14% of the booking subtotal. On the host side Airbnb charges in most cases 3% of the booking subtotal. The booking subtotal includes the nights fees and the cleaning fees. So for example in the example above Airbnb would make about $478, that is great when you are only the platform.

Aircover

Airbnb recently also started to offer Aircover for Hosts, this is an expanded expanded coverage for free that includes:

$1 million in Host damage protection and

Pet damage protection

Deep cleaning protection

Income loss protection: AirCover for Hosts reimburses lost income if you cancel confirmed Airbnb bookings due to guest damage

14-day filing window: If guests cause damage, host has 14 days to request reimbursement after they check out—it doesn’t even matter if new guests have already checked in

Quick reimbursements: Reimbursement for guest damage typically within two weeks

Faster track for Superhosts: A host can get priority routing and faster reimbursements

$1 million in Host liability insurance

Bodily injury to a guest (or others)

Damage to or theft of property belonging to a guest (or others)

Damage caused by a guest (or others) to common areas, like building lobbies and nearby properties

Flexibility

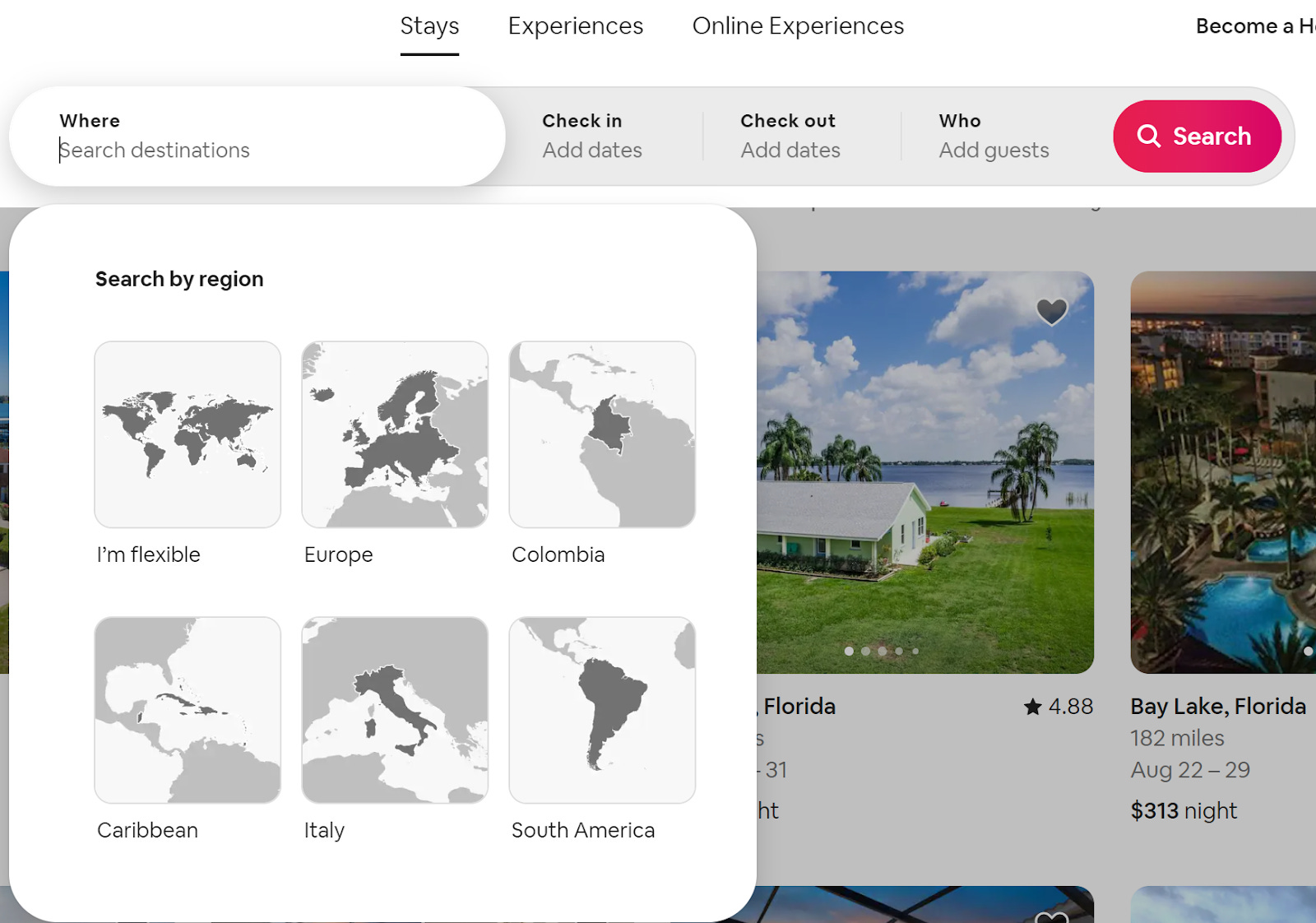

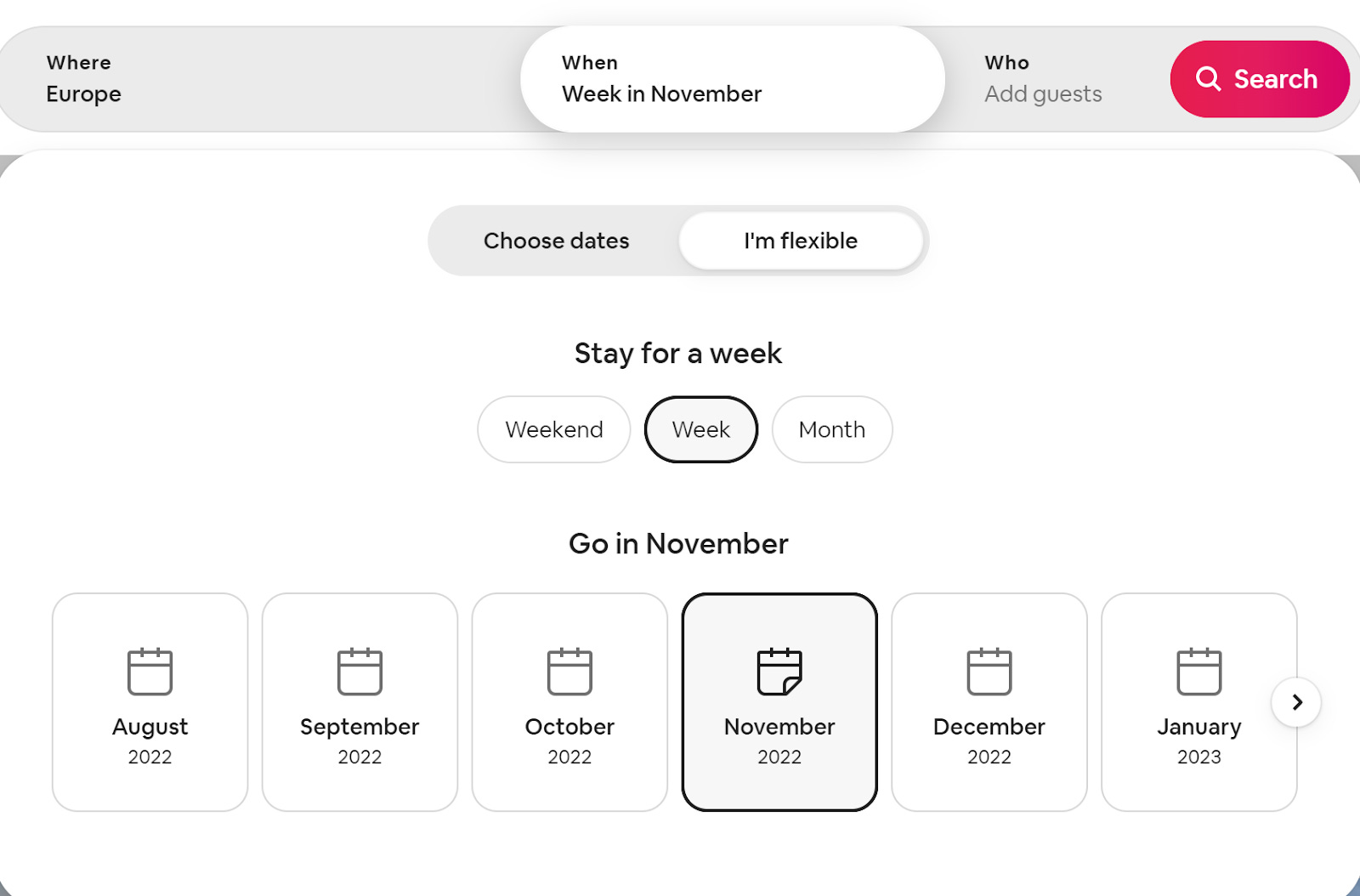

Recently the company has also added new features in their website. The pandemic saw a shift in customer behavior. Ever since the pandemic customers are becoming more flexible when traveling. This was mainly triggered by home office work. Customers can work from everywhere in the world giving the flexibility to travel the world while working and having longer stays. This became an opportunity and an operational change of their platform. Airbnb responded by adding many flexibility features on their website. The main bar now shows three main ways to search for accommodation.

Gives the customer the opportunity to choose from different regions, flexible length of stay, desired timeframe and amount of guests. As a result Airbnb suggests options that fall within those selections. In the background Airbnb is trying to point customers to regions and places where they have supply. They are pointing demand with supply, they have the demand of flexible customers that want to have a long stay somewhere in the world with supply of locations currently listed in Airbnb. This feature has been used close to 1 billion times already and it is having a huge impact on the overall length of stay of customers.

Experiences:

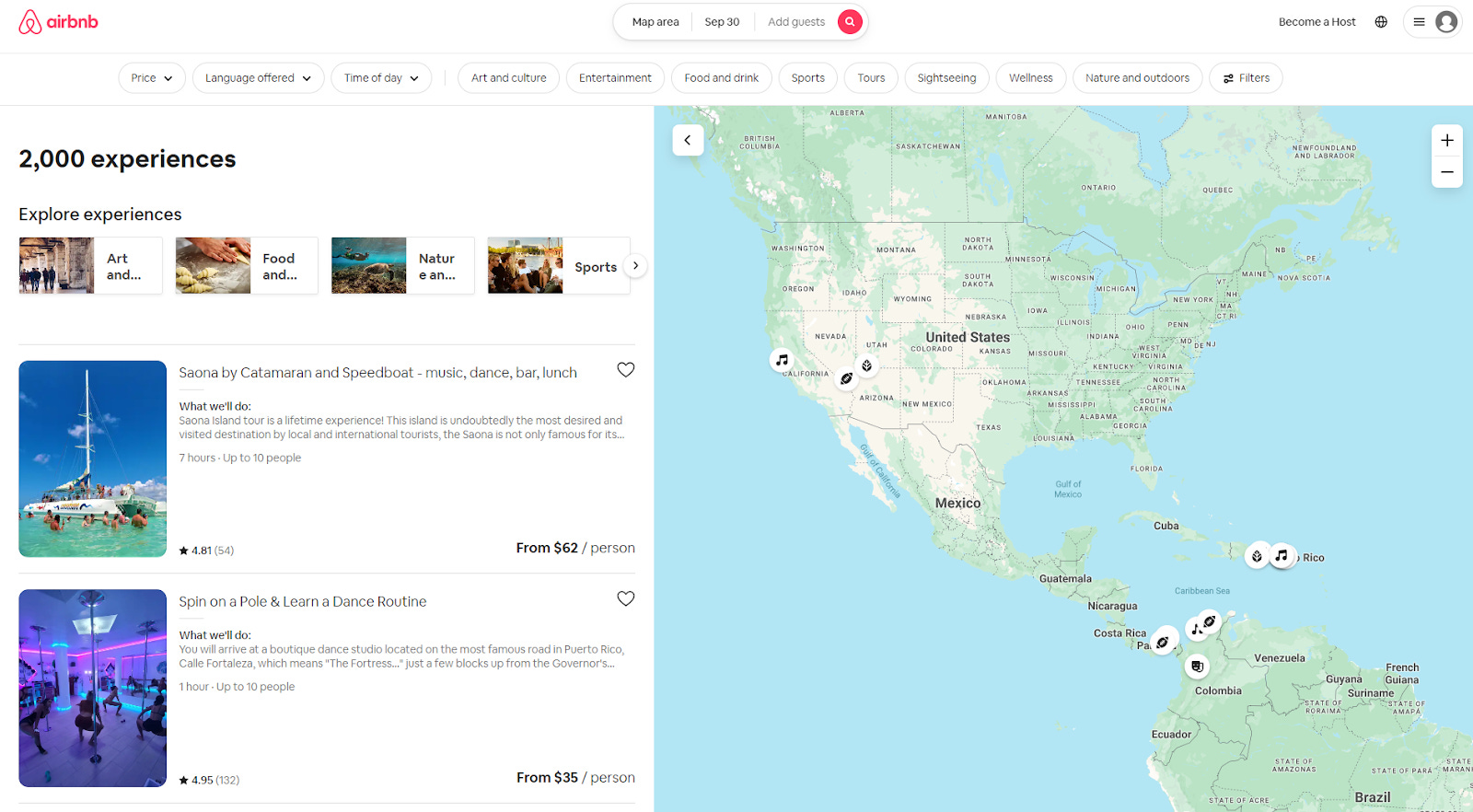

The search bar no longer is only about “stays”, you can also book experiences. These are tours or events or any type of thing you could think of. For example, you could get a tour from a local, you could get to make pasta with a grandma from Italy, visit Rome in a Vespa, etc. Experiences are not limited only to traveling. There are options also for online experiences, for example classes to learn how to cook Thai food, fitness classes, etc, options could be endless.

Similar to what they do from lodging, Airbnb gets a fee for what the customer is paying, this time is generally 20%. The amount of the service fee is calculated from the price that hosts set for their experience. Guests who are browsing experiences are shown the total price that they’ll pay to book. No other service fees are charged to guests at this time. (Airbnb doesn't charge any service fees for social impact experiences—100% of social impact proceeds go to a nonprofit)

Key Metrics / Performance

Revenue and Key KPIs

Being in the traveling industry Airbnb has seen a very volatile number of quarters in the past three years. If you asked anyone in March 2020 that they would be having record quarters in 2022 almost no one would have believed it. But everything has changed since.

During Q2 2020, while the whole world was in lockdown, Airbnb had its worst quarter. Only $335m in revenue. During this quarter Aribnb even had to raise close to $2b in debt. The company during this period was trying to strengthen their balance sheet enough to be able to weather the worst part of the pandemic. During these months they were receiving a storm of cancellations and their respective refunds, all of this forced them to go into this debt during 2020, in 2021 this debt has been refinanced lower than the close to 11% they had during the pandemic. Since then Everything has changed, now Airbnb’s revenue is higher than the $1.6b in revenue that they had in Q3 2019, the highest before the pandemic.

Revenue is up by 58% vs last year, last year by Q2 the world was already being vaccinated. In the US, vaccination was ahead of most of the world but international travel was extremely limited. Most of the restart of Airbnb revenue came from the change in customer behavior given the flexibility that the home office offered. Many in the US became local nomads, people started to work from different parts of the countries. There was a huge exodus from the big cities at the start of the pandemic, and this was pretty much alive after one year.

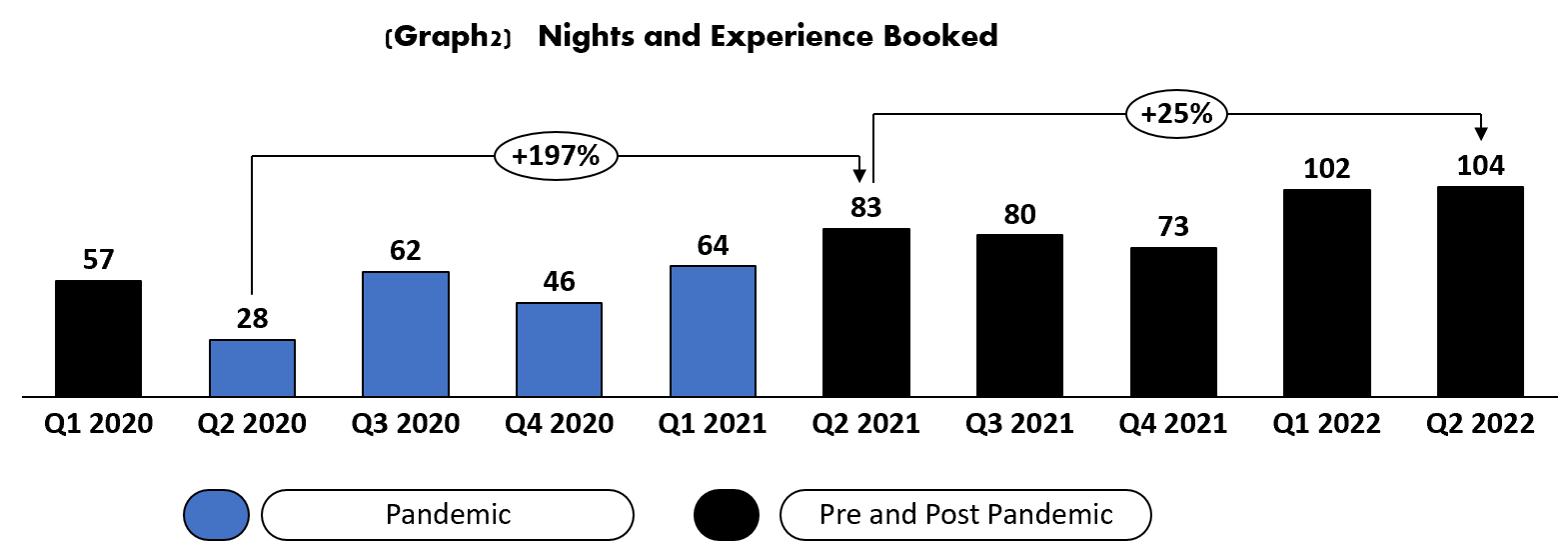

During the pandemic nights booked went all the way down to 28 million at its worst. 2020 was the lowest year in a while with only 193m nights booked. 2022 already by mid year had more nights booked at 205.8 million. The company has said that ever since the pandemic the number of bookings over 28 days has increased dramatically, it was as high as 24% of bookings made at some point in 2021 now it represents 20% of the business and booking above 7 days represent 50% of their business. Clearly Airbnb has established itself as a long term solution for guests. Before the pandemic their biggest market was cross border urban bookings, now this has been replaced by long term flexible bookings.

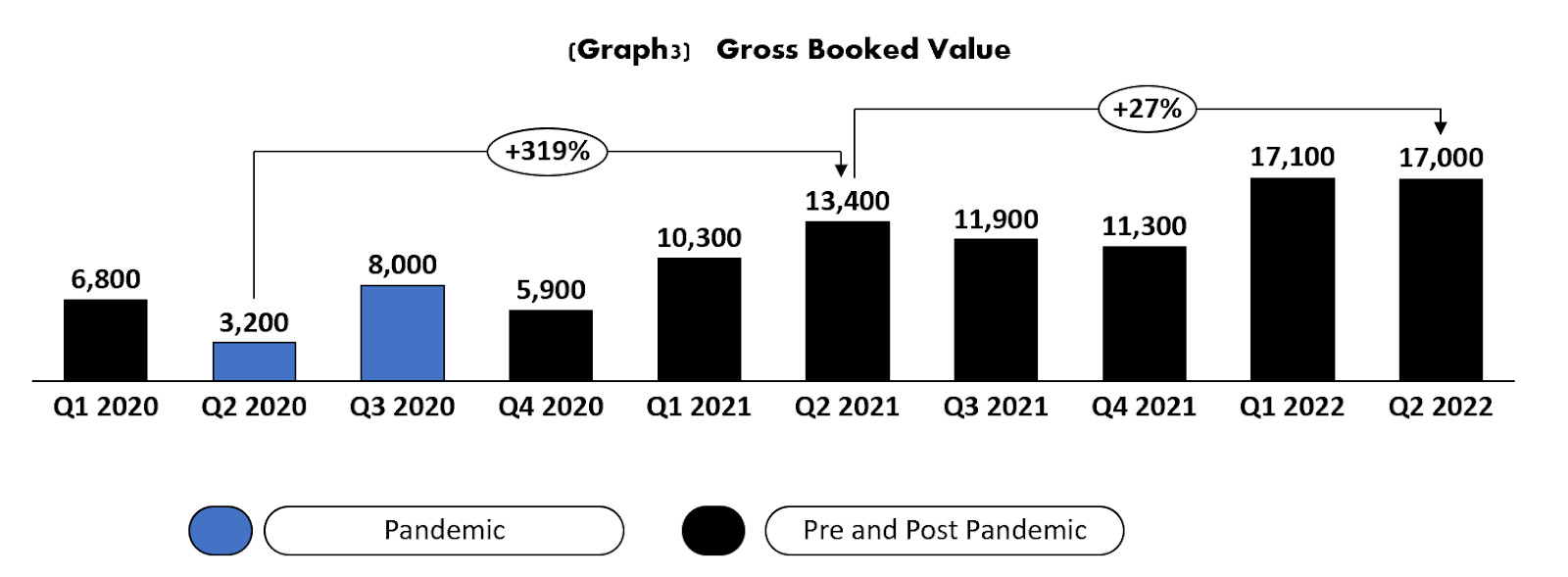

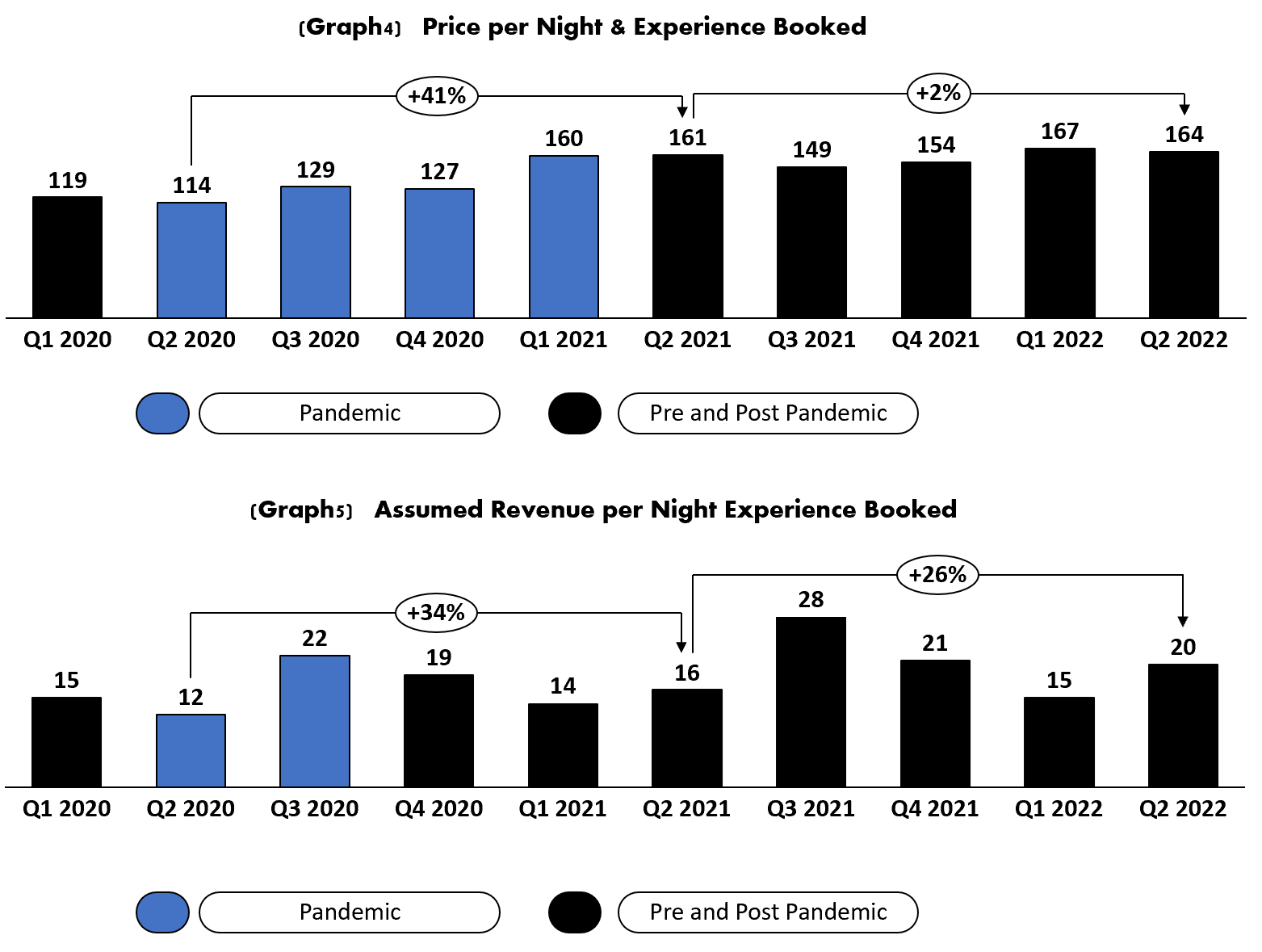

Gross booked value has generally followed the same trend as bookings with some slight differences, for example, value went down in Q2 while night went up. But overall the price per night booked has continued to grow. Price per night has sustained a higher level than pre pandemic levels and during 2022 has reached over $160 per night booked. This is up by $50 per night from the pandemic low. There is some seasonality between quarters, like summer etc. But as of now it is very difficult to see these effects, because there has been so much change during the past 24 months that each season had something different on top. In the future this will be more clear.

Airbnb’s take ratio has been very volatile during the last two years, it is better to look at it year by year since the revenue from the booking is recognized upon check-in while GBV represents the dollar value of bookings on the platform in a given period, GBV is then a leading indicator of revenue. A lower take ratio during the worst of the pandemic would make sense, the best thing that they could do during this period is to keep as many hosts as possible. Hosts are everything for Airbnb, without them they don’t have a business. So 2020 especially was a time to be focused on helping their partners and not about maximizing profits. When looking at yearly take ratios of ‘19 to ‘21 there is no major change in its trend, so it seems that they did not protect their host from this side, we will see below in their margins how they handled this. They went into debt during 2020 to strengthen their balance sheet in order to give as much support as possible to their hosts. So this should be seen in their P&L. (2022 has the lowest take ratio so far since it is not over, it should be adjusted higher later)

The US has recovered and continued to grow quickly, 2021 revenue was 1.7 times the revenue level it had in 2019, while international markets revenue was still 98% of the level it had in 2019, still great, it has recovered almost all of it, but they are not following the rapid growth seen in the US. This is mainly due to stronger Covid restrictions internationally throughout most of 2021 (Asian and Europe were still locking down people in 2022)

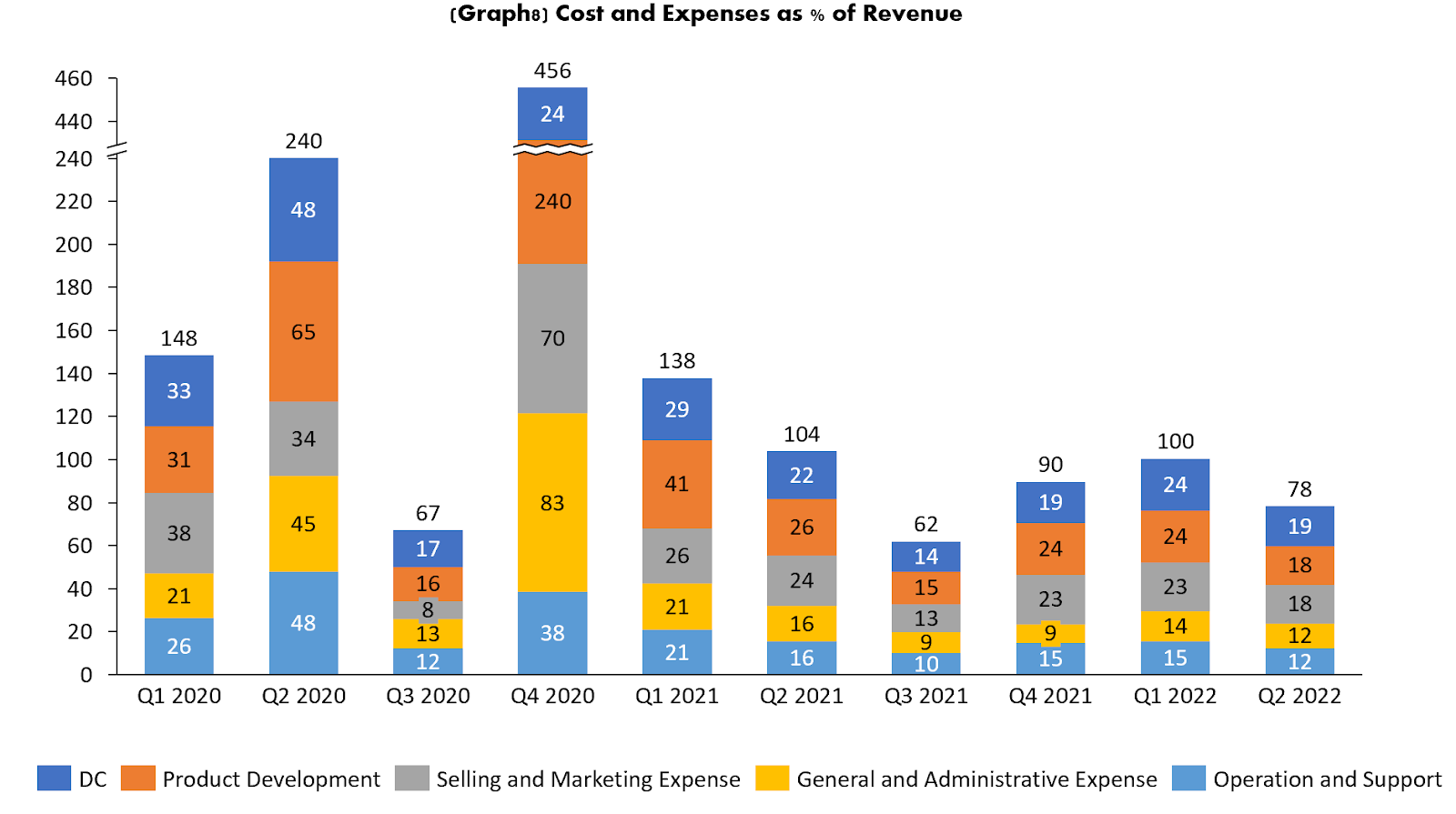

Costs and Expenses

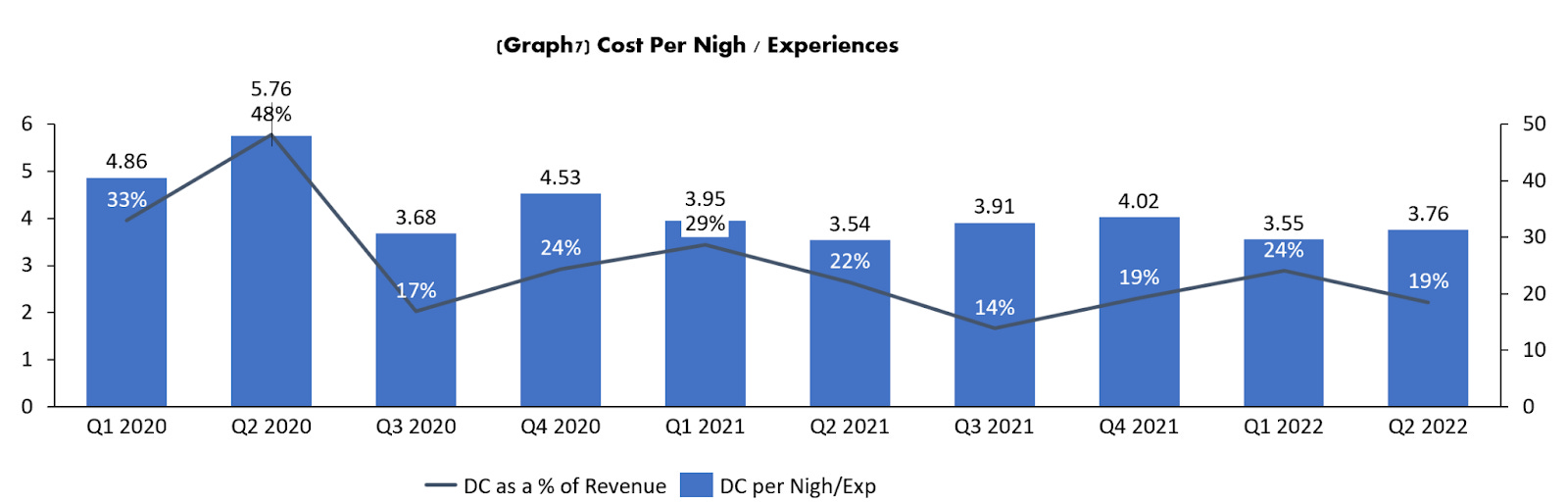

Direct cost as a percentage of revenue is volatile during the year, it moves with the seasons, being higher in Q1 and the lowest in Q3. At the start of the pandemic due to the loss of scale, direct cost went up all over to 48% of the revenues. All the structure in place to generate a whole lot more revenue suddenly was too heavy on the business. In terms of the cost per night the natural average seems to be between $3.6 to $4.0

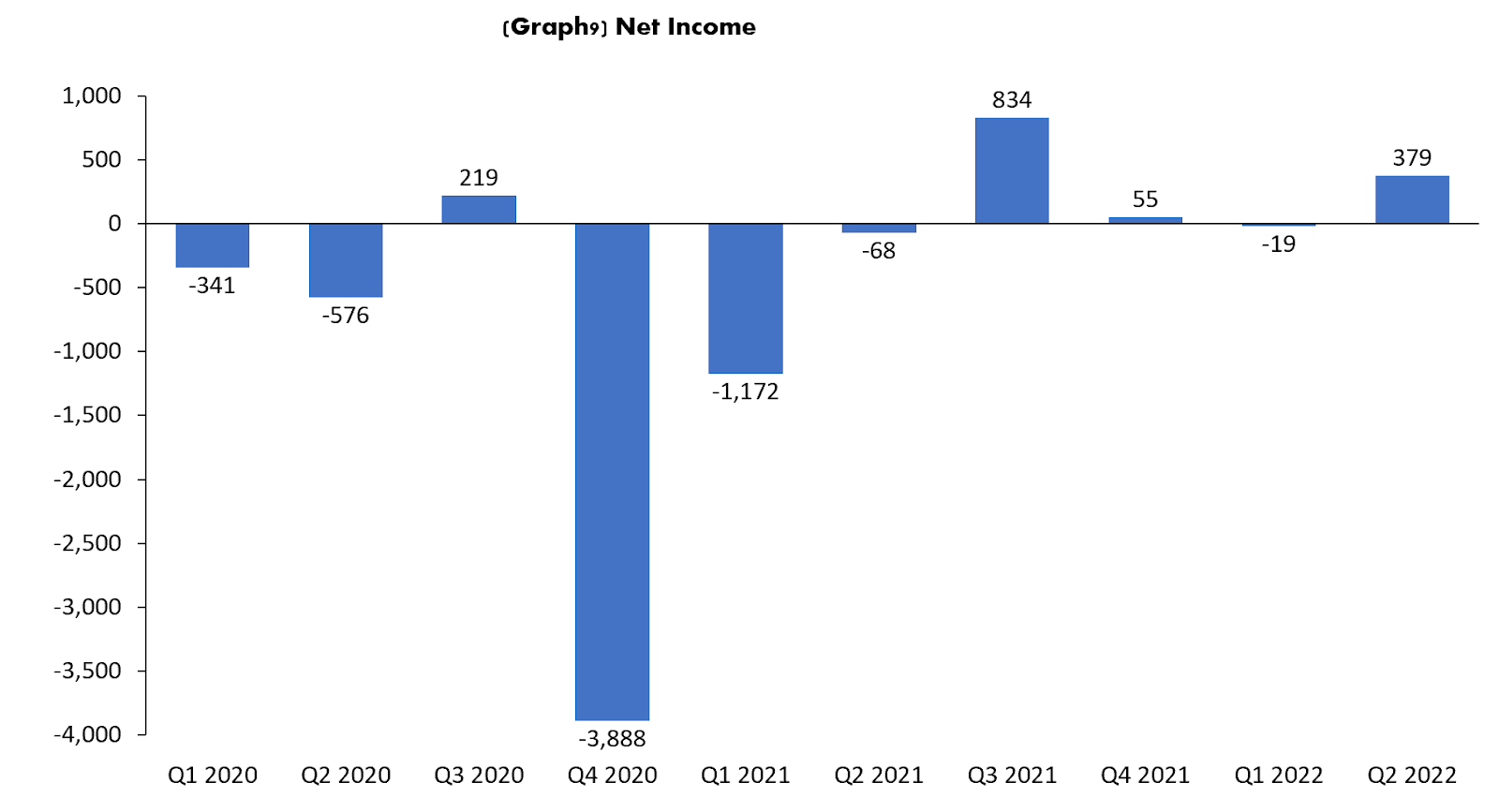

Over the last 12 months Airbnb has improved their scale tremendously; it has managed to have 3 out the last four quarters with an operating profit. It did not have this consistency even before the pandemic, let alone during the pandemic, in 2020 alone, the company had a net loss of $4.5b. Though this includes heavy impact from stock based compensation (SBC) that was triggered by the IPO, in Q4 2020 alone SBC had an impact of $2.9b. 2022 so far it has had $360m in profits and over the last 12 months $1.2b.

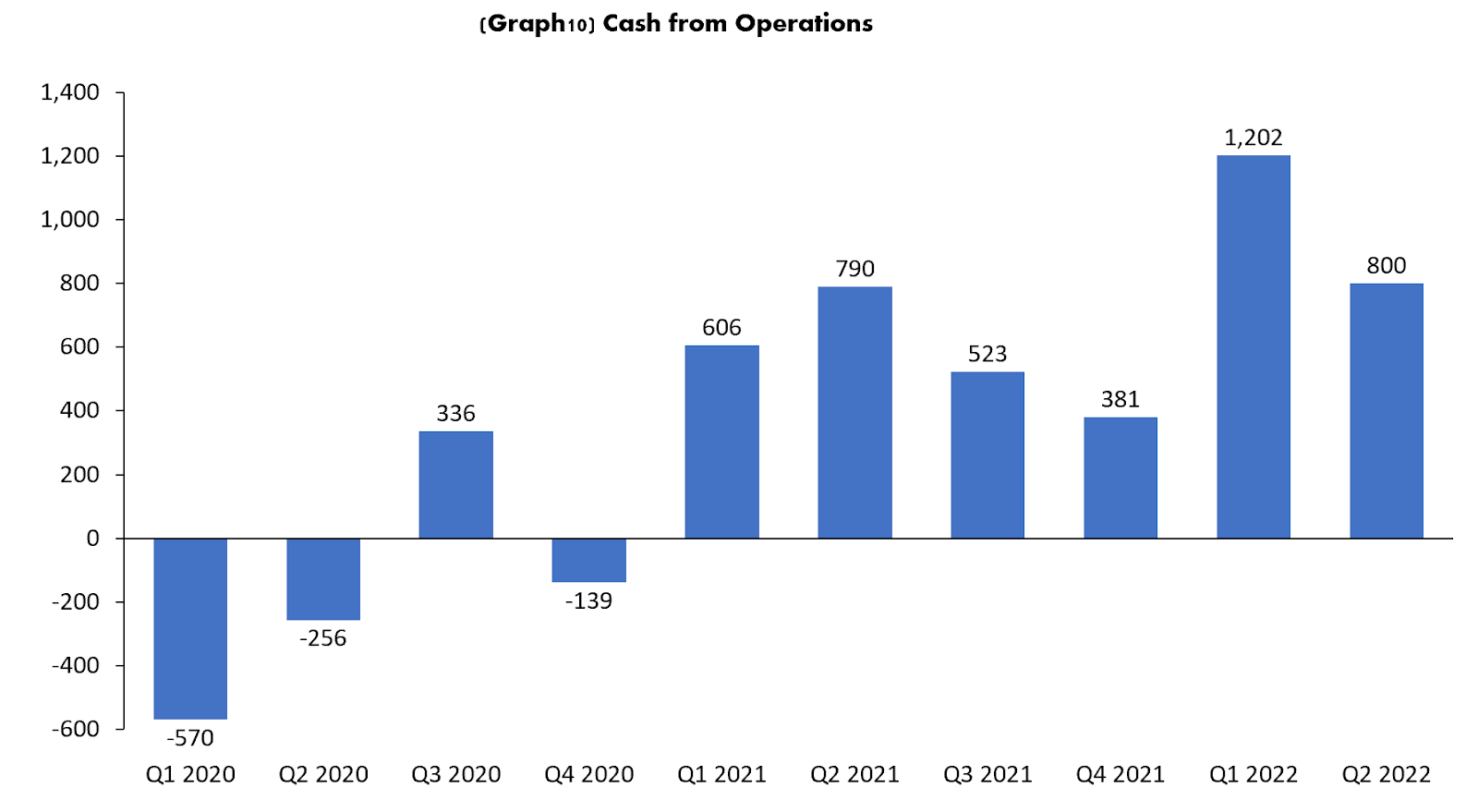

Cash Flow

The IPO and the pandemic have changed everything for Airbnb in terms of cash flow. The IPO gave them more possibilities to continue to take advantage of stock based compensation. It gave them the opportunity to use their stock as a good currency for growth, while the pandemic changed the behavior of the customer. It brought a behavior that is very beneficial for Airbnb, giving them just a short period of an emergency, they were back to aggressive growth in just a few months. It is all reflected when we see in detail the level of cash used for operations in 2020. Airbnb used a surprisingly low amount of cash during the pandemic year, only $629m. A completely different story from the $4.5b seen at the net income level. They accomplished this by using non-cash expenses, mainly the very popular tool in tech, SBC. SBC for 2020 was $3.0b other non-cash expenses like depreciation and amortization help with an additional $103m. All of this is seen as well through 2021 and 2022 and has managed to become +$3.67b in cash generated since 2020.

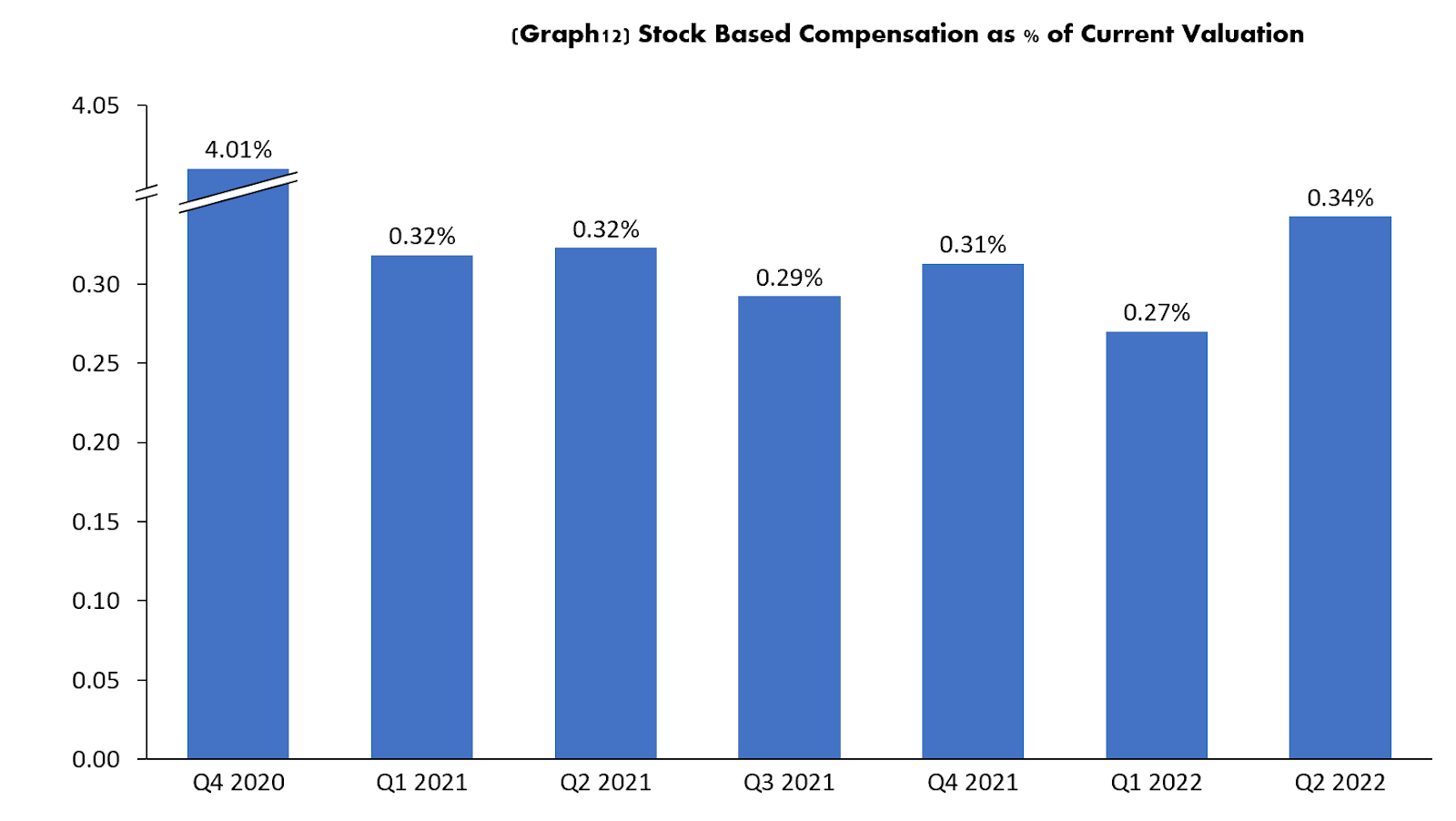

With the current level of SBC over the past 4 quarters the company is using about 1.22% of their current market cap per year. Nothing to worry about for now and very common in the tech industry and something that they should compensate for with growth of revenues and growth in valuation.

They have continued using stock issuance during the last few quarters and have gotten another $224m from their stock as currency. Capex is not a big investment for a company like Airbnb they have used only $21m.

That cashflow situation has improved so much for Airbnb recently that they announced during last quarterly call that they will do their first ever buyback for $2b, even when they are still in the growth stage, so they feel pretty comfortable with the level of cash that the company will be bringing in the coming quarters, they sound that they are convinced that they will manage to fund all the future growth with what will come from the business and what they already have.

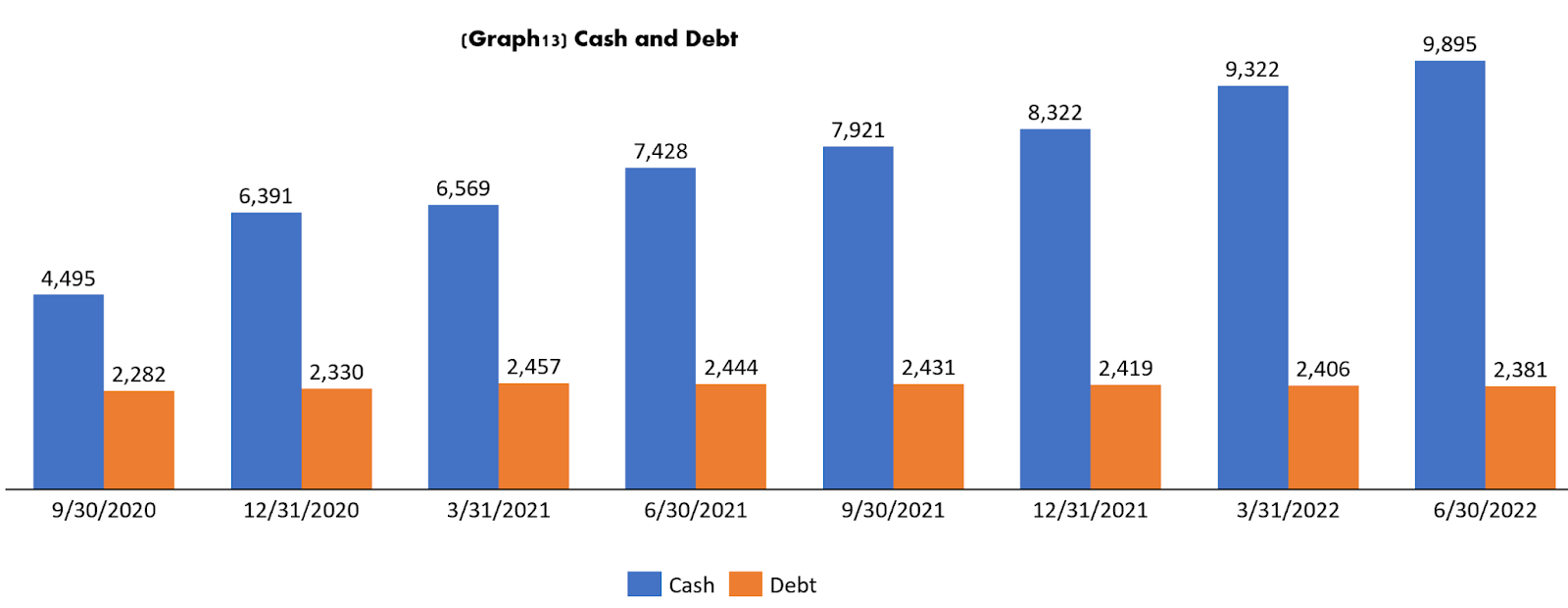

Balance Sheet

Like mentioned above, the cash position for the company is very strong, they went from $3b to start 2020 to $9.8b by the close of the second quarter of 2022. On the debt front the major change was the amount that they got to survive the pandemic during summer of 2020. This level of debt has remained in their balance sheet. But was very quickly re-financed. Even with this their debt level is not high, it was only $2.4b by the close of the quarter

Competitive Landscape

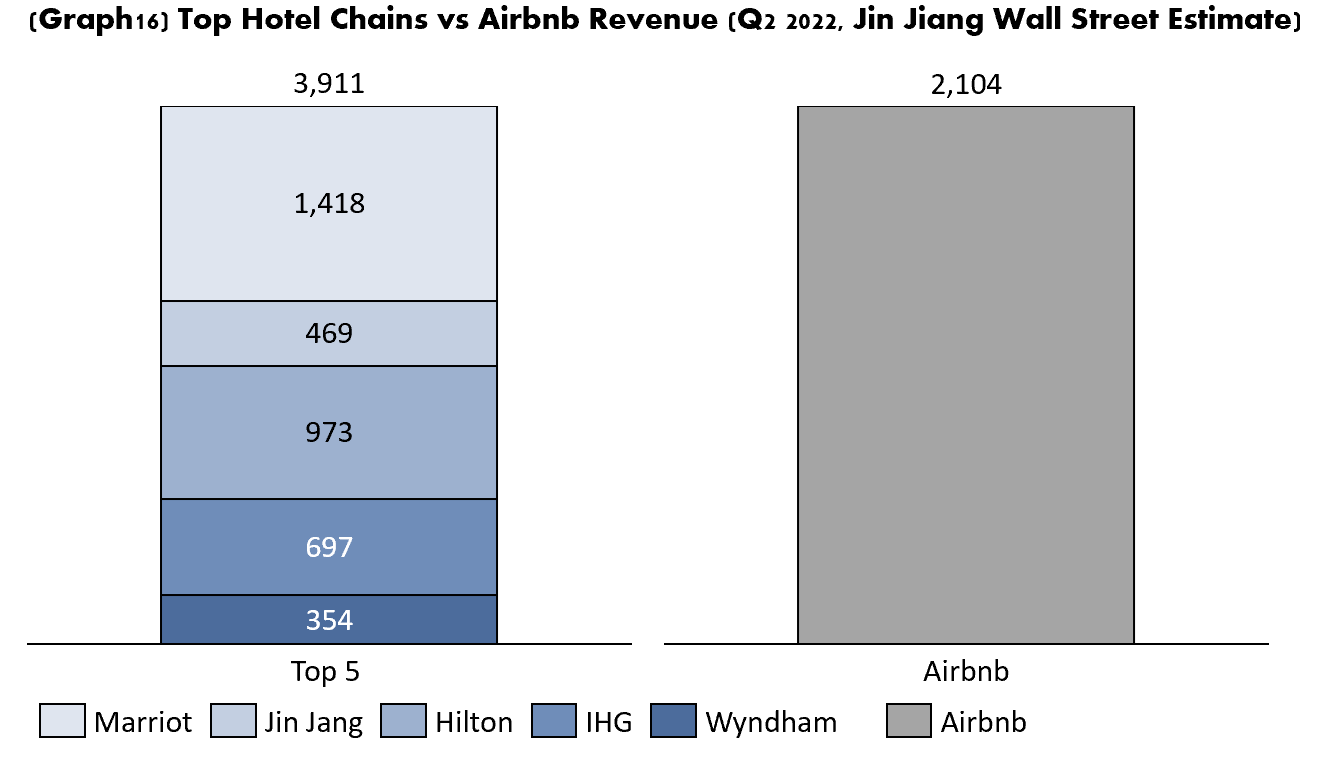

Airbnb has more competition than one would think. There are not many platforms similar to Airbnb, one could only think of Vrbo, yet there are a lot of ways to book stays and experiences. Hotels are the main competitor of Airbnb, they compete directly with them. Hotels have a wider presence all over the world, but a lot less concentrated. There are millions of hotel rooms all over the world. While there are only about 4 million Airbnb hosts with about 6 million active listings. Some of the biggest hotel competitors for Airbnb would be:

Marriott International: 7,500 hotels with about 1.4 million rooms in 2021

Jin Jiang: 10,000 hotels with about 1.1 million rooms in 2021

Hilton: 6,200 hotels with about 1 million rooms

International Hotel Group: 6,000 hotels and about 886K rooms

Wyndham Hotel Group: 8,491 hotels and about 796K rooms

The top five hotel chains in the world have close to the same amount of rooms that Airbnb does. Revenue though is a very different picture. They get a bigger portion of the room fee, yet the revenue for the top 5 hotel chains together is not that far from the revenue that Airbnb has every month. Comparing Q2 Airbnb GBV to Revenue for the Top 5 hotels chains we get nothing but surprise, Airbnb had $17b vs $3.9b for the hotels. Great performance, they do have more active listings, but you can see that the listings have higher value, bigger houses and longer stays sure make a difference here. The two numbers are not 100% comparable though, given that Airbnb offers experiences and hotels mostly don't, yet it is impressive how Airbnb is getting very close in revenue when they only get a portion of the gross booked value.

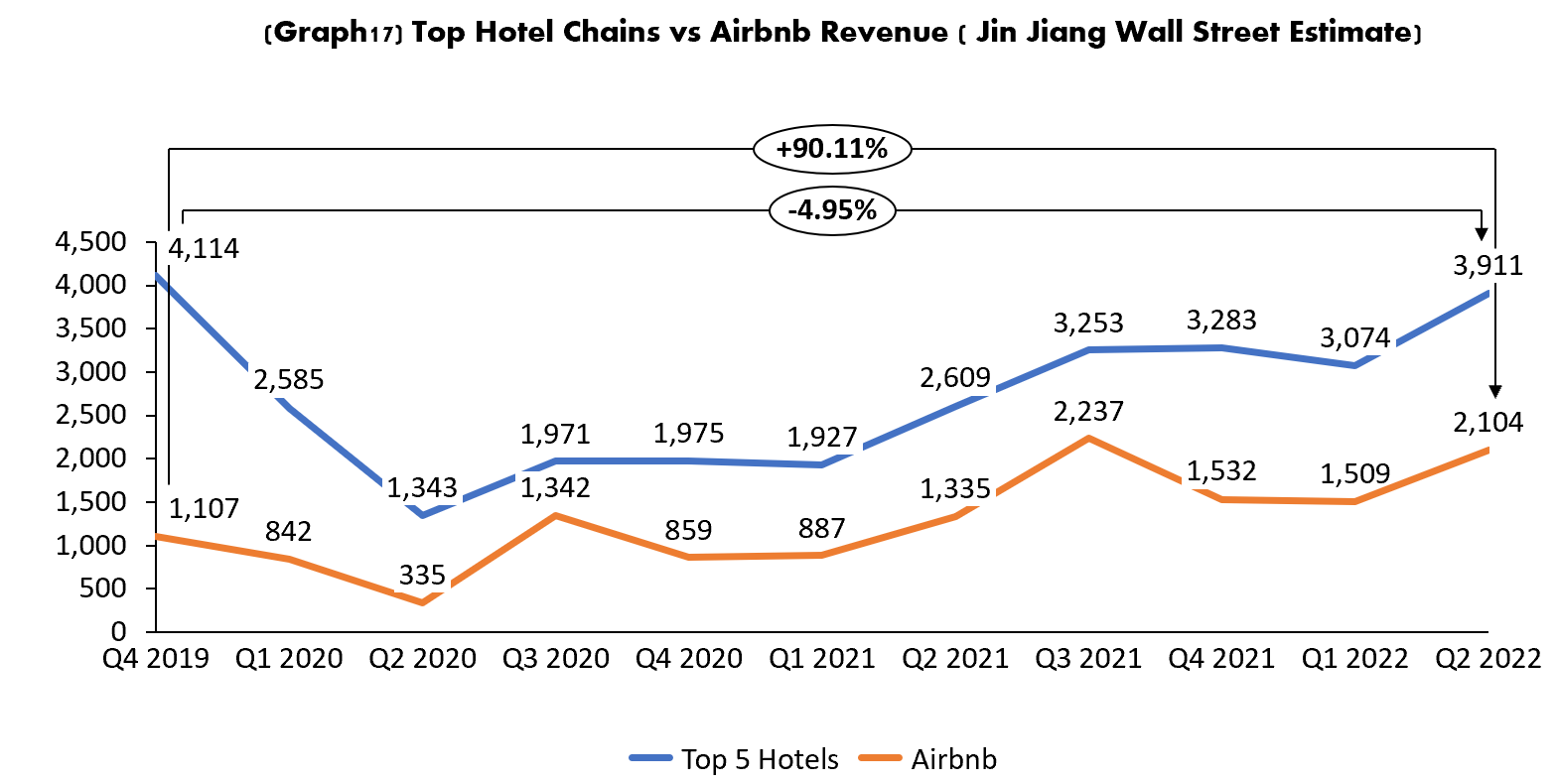

The recovery for hotels has been very strong, on the graph below you see that Airbnb and the top five chains nearly follow each other's trend since June 2020, but you also see that the fall from Q4 2019 was far greater for hotels than for Airbnb. This is easy to understand if one begins to think that hotels are for Covid purposes very crowded spaces while an Airbnb could be easily a no contact experience. So even though Airbnb fell as well, it still had something to offer during that time for people that needed to travel, perhaps due to emergencies during that time.

While hotels have reclaimed almost all of its revenue from Q4 2019, Airbnb has grown by 90% when compared to the same period.

How is vrbo doing compared to Airbnb. They do play almost in the same field so their comparative performance would tell us a lot. Vrbo is part of the Expedia group, they trade in the stock market but as a part of Expedia. Since 2020 unfortunately Expedia stopped reporting vrbo as a separated line. The last information they gave was that vrbo had $1.3b revenue for 2019 that was 28% of Airbnb's revenue.

Some of the possible risks for the company are:

Easy target: The company will always be an easy target for politicians. They will always be the bad guy, for two main things.

First, a lot of countries like to protect their local tourist players, including local hotels. The situation could become highly regulated or they could even get banned in some markets. This danger will always be alive, every time there is a change of government in a country anything that the previous stood for could disappear and so could any deals or agreements with Airbnb.

Second, they will always be the bad guys for rising prices for housing. Especially in very important tourist locations throughout the world it will be very attractive for property owners to put their property for rental because the return they get from Airbnb would be a lot better than putting the place for rent. This reduces supply and could likely raise rent prices giving politicians a perfect excuse to go against them and gain popularity, and this again could end in either limiting the amount of places (which happens a lot in many places already) and possible banning.

Competition: So Airbnb currently takes around 15% of the revenue just for being a platform. This is a very fast changing world and competition that could come and cut that percentage could threaten their revenue generation. Vrbo already takes about 8% of any web3.0 competitor that could be created in the future could even have a platform and takes them out all together and contacts the host with the guest directly. The risk is there, they disrupted the lodging industry, they could easily get disrupted as well.

What could be the case for Airbnb being a good opportunity for the next 10 years?

Big Market: Airbnb in its S1 calculated their TAM as $3.4 trillion that being $1.8 trillion in short term stays, $210 billion in long term stays and $1.4 trillion for experiences. Their serviceable addressable market (“SAM”) would be $1.5 trillion, including $1.2 trillion for short-term stays and $239 billion for experiences. The market is huge and they just have started, you could even say that since their S1 was first published long term stays addressable market could have grown dramatically, the work from home is here to stay, perhaps not at the level of the pandemic, but it will be something that will give a lot of people, generally with good incomes, the ability to work from anywhere in the world.

World Presence: We mentioned above that one of their risks is that they are an easy target for governments. That will always be true, but the fact that they are everywhere in the world helps mitigate the hit from any of these bans or limits. This helps not suffer huge hits from a sudden ban.

Cash Generation: It is definitely clear that Airbnb is approaching heavy cash generation. This could likely continue, it would fuel a lot of growth and a lot of buybacks. The $2b that they recently announced will be only the beginning.

Valuation

We have calculated a DCF analysis with our common three different scenarios.

For our base scenario we have kept the revenue growth around 20% for the next few years, EBIT improves, and as they become better at generating cash they also start doing some recurring buybacks. Our Base Scenario values Airbnb at $97 per share, close to what it is currently ($113) Our Optimistic scenario with better revenue growth and better margins goes up to $132 per share or about $85b. Airbnb currently trades in the middle of our base and optimistic scenario. As of our conservative scenario, growth becomes more challenging, more Airbnb, more regulatory issues and limits on how many active listings are possible in many cities. They basically saturated most cities. This could be the less likely scenario, but we wanted to model this in case this could be a possibility, the result was $63b per share or about $40b

Airbnb was trading as high as $212 per share recently, we think that the stock got ahead of itself in the meme-stock bubble. The company seems to be strong and performing pretty well. But fundamentally it was trading far from reality , it was trading at around 33 times sales. Today is trading at more comfortable levels, about 10 times LTM revenues and about 7 times next years. A much better level that is further away from bubble territory.