Airbnb: The Platform That Can't Be Replicated

Airbnb is the closest thing travel has to a pure marketplace. It owns no hotels, employs almost no housekeeping staff, and carries no balance sheet inventory risk

Q1 2026 Results · Reported May 7, 2026

A Seasonally Slow Quarter That Proved the Business Is Compounding

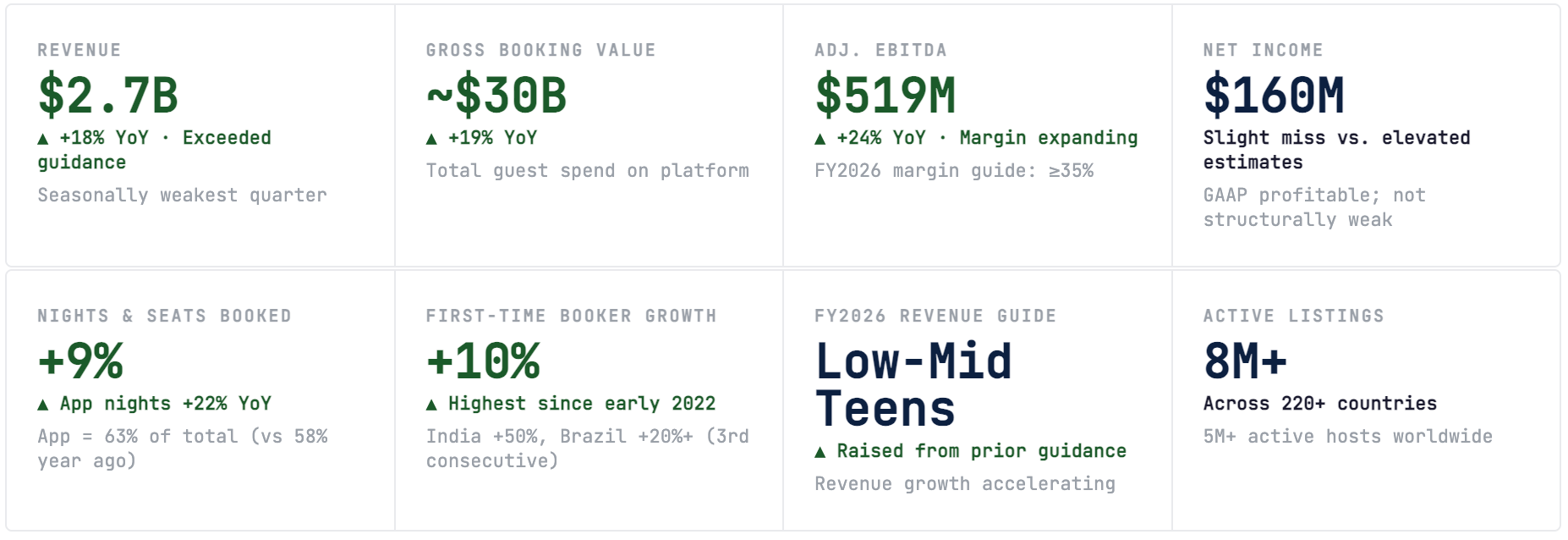

Q1 is Airbnb’s weakest quarter by definition — it captures Northern Hemisphere winter travel, the softest travel season on the calendar. Against that seasonal backdrop, 18% revenue growth to $2.7 billion is not just solid: it demonstrates that the platform has reached the point where even its trough quarter produces genuine compounding. Revenue exceeded the high end of management’s own guidance. Gross Booking Value — the total amount guests spent on the platform — grew 19% year-over-year to nearly $30 billion. Nights and Seats Booked grew 9% year-over-year. Adjusted EBITDA hit $519 million, up 24% year-over-year, with margins expanding. Net income of $160 million was a slight miss against elevated estimates, but is not structurally meaningful. The shareholder letter’s tone was confident: guidance for the full year was raised.

Business Model

Zero Inventory, Pure Network — and a Take Rate That Compounds

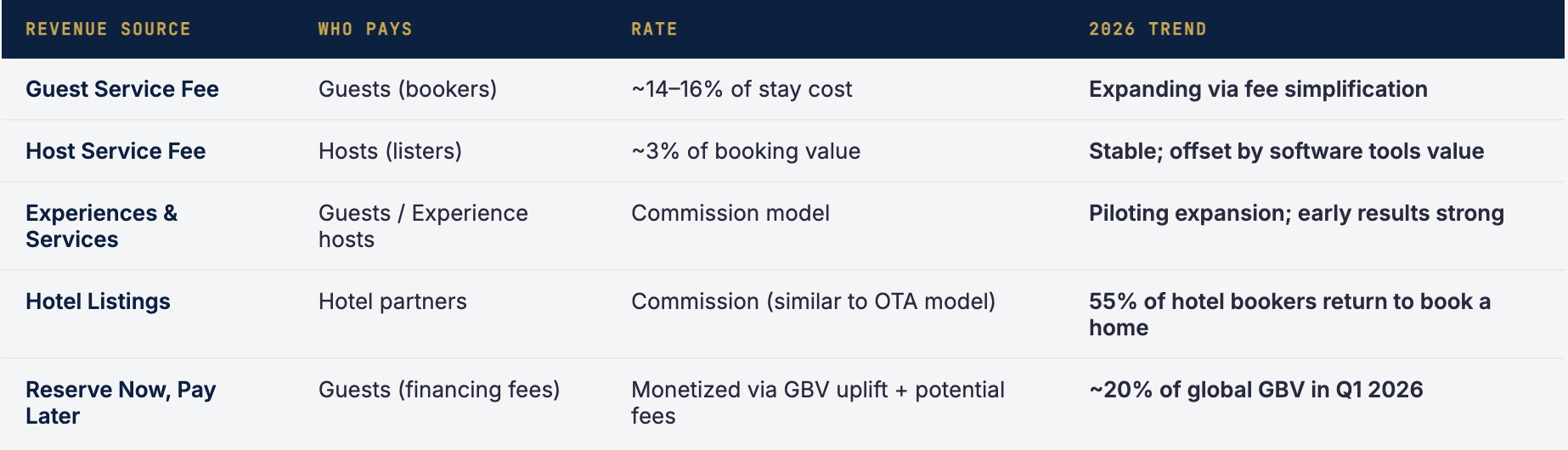

Airbnb’s economic model is one of the most elegant in consumer technology. The company owns no real estate, employs no cleaning staff, and carries no inventory on its balance sheet. Its entire business is a software layer between two groups of people: hosts who have space they want to monetize, and guests who want to stay in that space. Airbnb takes a commission on every transaction — approximately 3% from the host and 14–16% from the guest, for a blended take rate of around 18%. On $30 billion in gross bookings per quarter, even a small expansion of that take rate adds hundreds of millions of dollars to revenue.

The zero-inventory model creates extraordinary operating leverage. When demand spikes — a World Cup, an Olympics, a major festival — Airbnb does not need to build more hotels. Supply already exists in the form of the millions of homeowners and property managers listed on the platform. When demand softens, Airbnb does not carry stranded assets. Hotels have fixed costs that must be covered regardless of occupancy. Airbnb has none of those. This structural advantage becomes most visible during demand shocks — exactly when Airbnb’s model shines and its hotel competitors suffer.

The Flywheel: How the Network Compounds

More guests attract more hosts (hosting income is real money — average ~$13,800/year per host). More hosts attract more guests (greater variety, better pricing, more destinations). More transactions generate more data, which improves search ranking, pricing tools, and fraud detection. Better tools attract more professional hosts and more discerning guests. The flywheel spins faster with each revolution. After 18 years and 2.5 billion total guest arrivals, Airbnb’s network is the single hardest asset in travel to replicate from scratch — not because the technology is complex, but because the trust, the critical mass of reviews, and the brand recognition would take a decade and tens of billions of dollars to rebuild.

Growth Vectors

Three Acts of Growth — Core, Platform, and Efficiency

Brian Chesky returned from his post-IPO period in 2022 with a clear-eyed diagnosis of what had gone wrong: Airbnb had become too complex, too expensive, and too inconsistent. The product was bloated. The host experience was frustrating. The guest experience was unpredictable. His response was to strip the company back to fundamentals and rebuild systematically. That rebuilding phase is now largely complete, and the company is entering what it calls an expansion phase — growing both the supply side (more hosts, better tools) and the demand side (international markets, new product categories).

Act One · The Core

Fixing What Was Broken — Then Accelerating It

The core product improvements are showing in the data. App nights booked grew 22% year-over-year in Q1 2026 — significantly faster than total platform growth of 9% — and the app now accounts for 63% of total nights booked, up from 58% a year ago. This matters because app users have higher lifetime values: they book more frequently, cancel less often, and generate more host-side referrals. The migration of bookings toward the app is a structural quality improvement, not just a channel mix story.

First-time booker growth accelerated to 10% year-over-year — the highest rate since early 2022 — with particular strength in Brazil, Japan, and India. These are markets where Airbnb has historically been underpenetrated relative to its brand awareness, and where local competitive dynamics (less established hotel infrastructure in secondary cities, younger demographics comfortable with sharing economy models) favor the platform. India origin nights booked grew approximately 50% year-over-year in Q1. Brazil has posted 20%+ growth for three consecutive quarters. Expansion markets are growing at roughly double the rate of Airbnb’s core markets.

Act Two · The Platform

Experiences, Services, and Hotels — New Entry Points Into the Ecosystem

The most strategically interesting development in the Q1 shareholder letter is the early data on Experiences and Services. Airbnb has been piloting both categories in select cities, and the conversion data is striking: nearly 25% of guests who are new to Airbnb and book an experience go on to book a stay. Roughly one in three experience bookers books a stay within 90 days. Experiences are functioning as a demand flywheel — a lower-commitment first entry into the Airbnb ecosystem that converts into the higher-value home-stay product.

The hotel pilot is similarly encouraging. Approximately 55% of guests who book a hotel on Airbnb come back to book a home. Hotels are a complementary product, not a substitute — they attract guests for city-center stays where home supply is constrained or regulatory bans limit listings, and those guests then discover the broader Airbnb platform and return for the home-stay experience. The Summer Release on May 20, 2026 is expected to include significant announcements about the expansion of experiences, services, and hotels to more markets globally.

The World Cup Playbook

FIFA World Cup 2026 is expected to be the largest single event in Airbnb’s history. Since October 2025, over 100,000 homes across the 16 World Cup host cities have listed on Airbnb for the first time. Airbnb’s Milan Olympics experience showed the template: nearly 200,000 guests stayed via Airbnb, supply in host markets grew approximately 30%, and Airbnb generated around 1 billion marketing impressions. Hosts recruited for major events tend to continue hosting after the crowds leave — creating a lasting supply expansion that benefits the platform long after the event ends. The World Cup is simultaneously a demand spike, a brand moment, and a host acquisition engine.

Act Three · AI Efficiency

60% AI-Coauthored Code, 40% AI-Resolved Support — and Compressing Unit Costs

Airbnb’s AI adoption numbers are among the most concrete in the consumer technology sector. Nearly 60% of the code Airbnb engineers produce is now coauthored with AI — roughly twice the industry average. This is not a pilot or an aspiration; it is the current production state of the engineering organization. The result is faster iteration, more frequent product releases, and more improvements shipping per quarter than was possible at the same headcount two years ago.

The customer support numbers are equally concrete. For guests who contact support through Airbnb’s AI Assistant, over 40% of issues are now resolved without a human agent — up from roughly 33% in Q4 2025. Resolution times are significantly faster. Cost-per-booking decreased approximately 10% year-over-year in Q1 2026. This is the AI productivity dividend arriving in a tangible, measurable form: fewer support escalations, lower cost per transaction, and faster resolution for the end user. Management expects the trajectory to continue through 2026 as the AI support system is further refined.

“When tariff uncertainty resulted in fewer people traveling to the U.S., they still came to Airbnb and found somewhere else to go. We have millions of homes, everywhere in the world, at every price point, and that’s something most travel companies can’t replicate.”

— Brian Chesky, Co-Founder & CEO, Airbnb — Q1 2026 Shareholder Letter

Revenue Track

From Pandemic Nadir to Sustained Double-Digit Growth

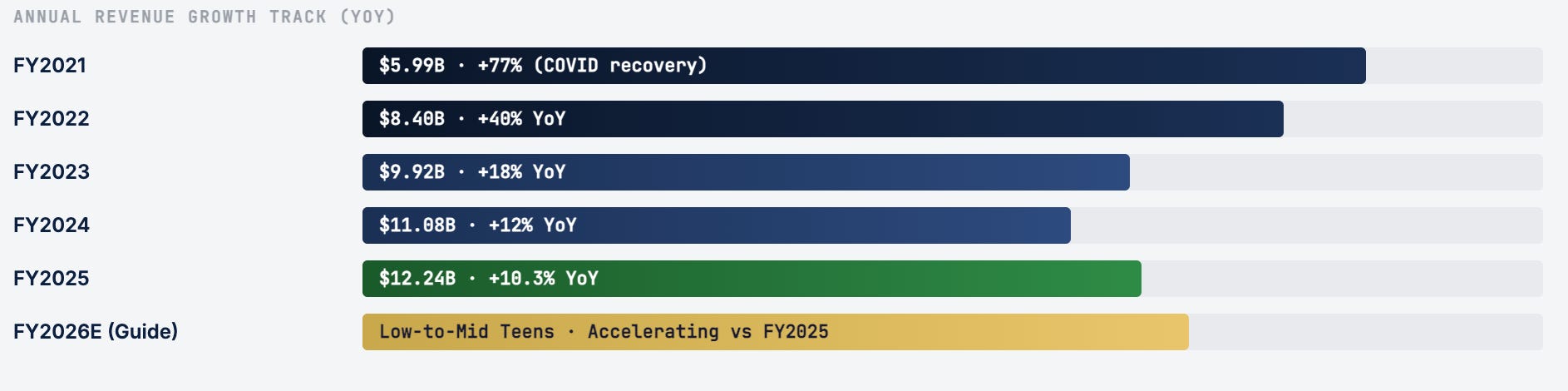

Airbnb’s revenue trajectory since its December 2020 IPO tells the story of a business that emerged from COVID-era disruption not just intact but structurally stronger. The pandemic forced a reset — Airbnb laid off 25% of its workforce, cut marketing spend dramatically, and discovered that the business was profitable at lower revenue levels than management had assumed. That discovery shaped everything that came after: a leaner cost structure, a more disciplined approach to growth investment, and a genuine focus on margin expansion alongside revenue growth.

Key Risk #1

The Regulatory Drag — City by City, Law by Law