Airbus: The World's Largest Planemaker Is Suffering

9,037 aircraft on order, €7.5 b EBIT in the guidance, and a stock that rose on results day. So why did CEO Guillaume Faury use the word "suffering" to describe his own quarter?

Executive Summary

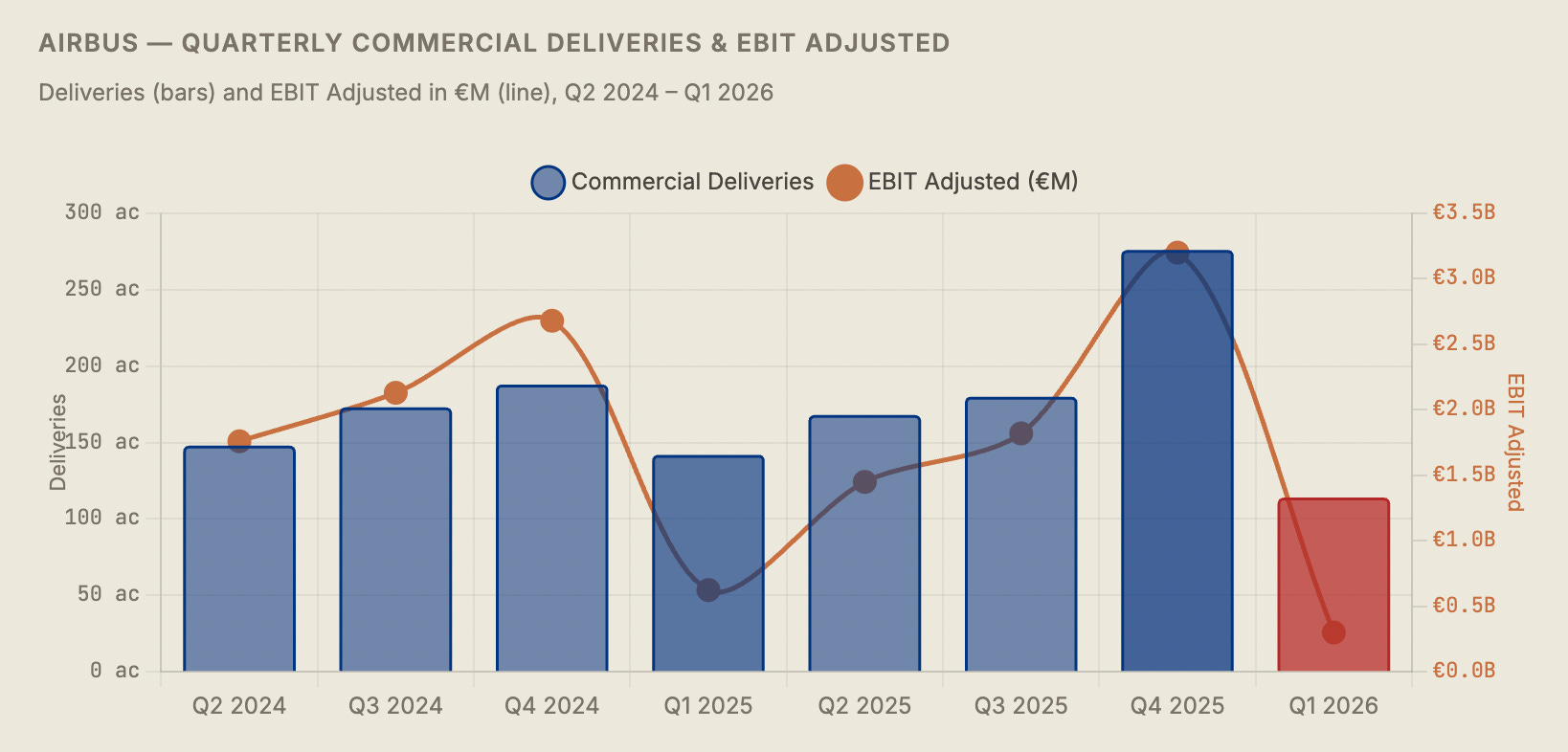

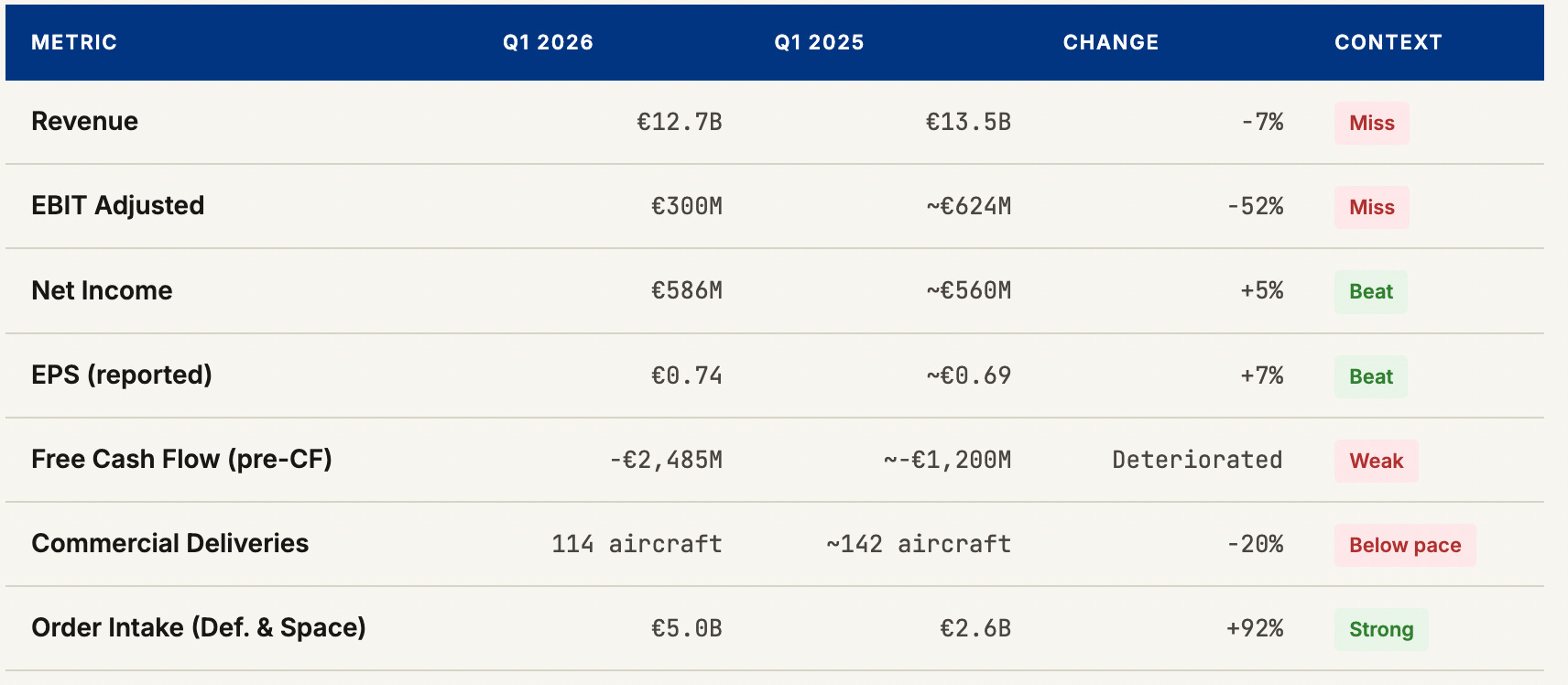

Airbus delivered the weakest Q1 in years on April 28 — revenue down 7%, EBIT adjusted down 52%, free cash flow negative €2.5 billion — and then watched its stock rise. That apparent contradiction tells you almost everything you need to know about how the market thinks about Airbus in 2026: the short-term pain is widely understood and already priced in; the long-term position is stronger than it has ever been. 9,037 aircraft on backlog representing roughly a decade of production at current rates is not a number that changes on one bad quarter.

The quarter’s weakness was not mysterious. CEO Guillaume Faury identified a precise cluster of problems — engine shortages from Pratt & Whitney, panel quality issues on the A320 family, an administrative delay that held up nearly 20 aircraft for Chinese customers, ongoing seating shortfalls, and the continuing distortion of a global tariff war. He called it a “desynchronization between production and delivery.” The factories are running. The inventory is piling up. The planes just can’t leave until the missing components arrive.

The full-year 2026 guidance was reaffirmed: 870 deliveries, ~€7.5B EBIT adjusted, ~€4.5B free cash flow. That math requires roughly 190 deliveries per quarter for the remaining three quarters — aggressive, historically achievable, but heavily dependent on Pratt & Whitney solving problems that have dragged on for two years. Meanwhile, the Defence & Space division delivered its strongest Q1 in recent memory, quietly providing the earnings cushion that prevented the quarter from being catastrophic.

01

From Pandemic Grounding to Backlog Mountain

To appreciate why a quarter with a 52% EBIT decline left investors relatively unbothered, you have to understand the trajectory Airbus has been on since 2020. The pandemic grounded the global commercial aviation fleet almost overnight. Airlines cancelled orders, deferred deliveries, and parked aircraft in the desert. Airbus delivered just 566 aircraft in 2020, down from 863 in 2019, and burned through cash at a pace that threatened the balance sheet stability the company had spent years building.

The recovery was faster than most predicted. Air travel rebounded sharply from 2022, driven by pent-up leisure demand that proved more durable than analysts expected. Airlines that had spent the pandemic questioning their fleet expansion plans found themselves scrambling to add capacity as load factors hit record highs and yield management became the dominant financial lever. Airbus’s order book, which had deflated during the crisis, began filling faster than the factory could ramp.

By 2024 and 2025, the company faced a paradox it has not fully resolved: demand was so strong and the backlog so deep that the binding constraint on Airbus’s growth was no longer orders — it was manufacturing capacity, supply chain reliability, and the readiness of its engine suppliers to keep pace. The company targeted 800 deliveries in 2025 and delivered 766. It targets 870 in 2026. In Q1, it delivered 114. The arithmetic of catching up from a weak first quarter is unforgiving.

“We are suffering from a desynchronization between production and delivery. The factories are running. The inventory is piling up. We are not short of demand.”

— Guillaume Faury, CEO, Airbus SE — Q1 2026 earnings call, April 28, 2026

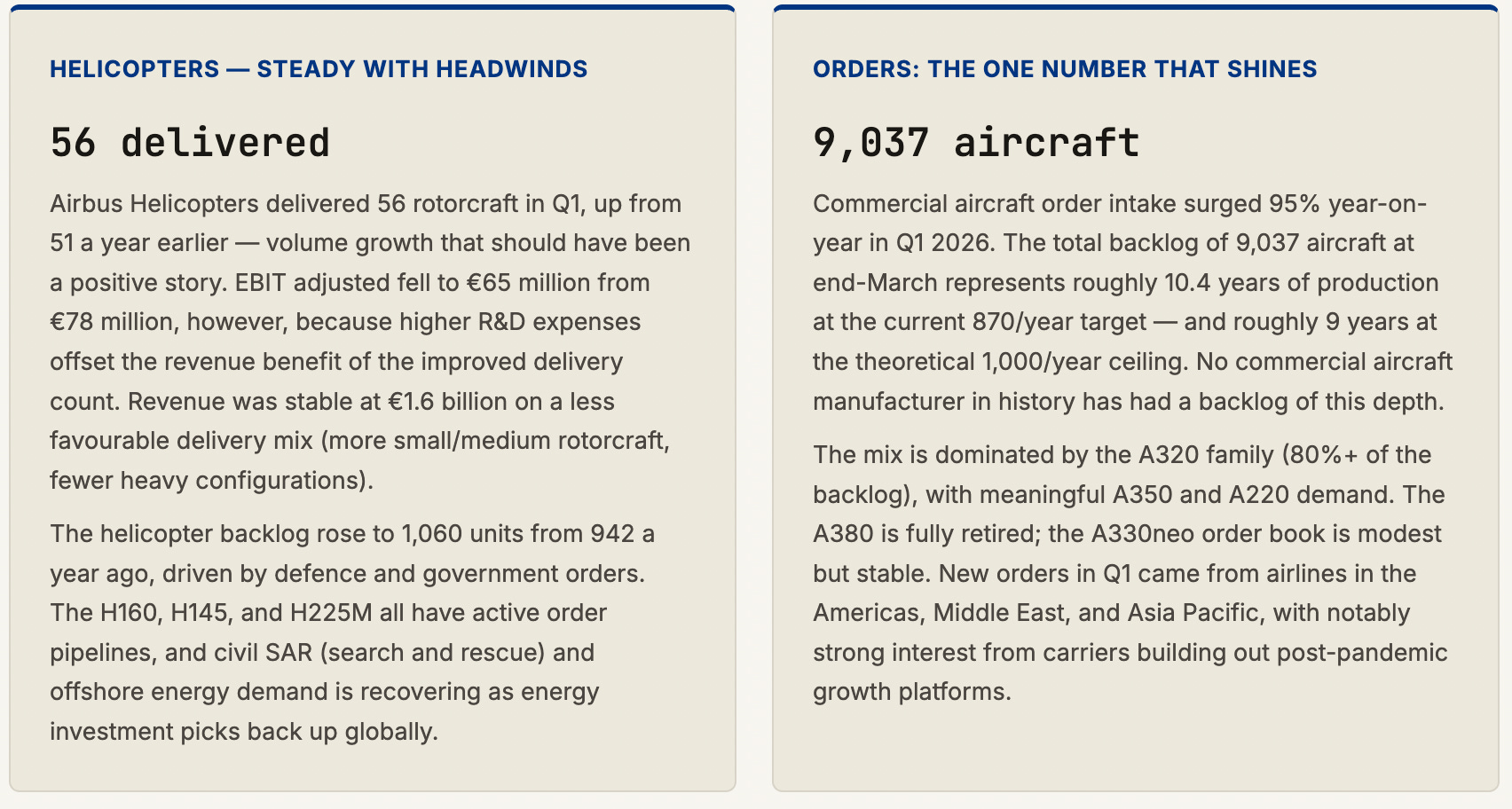

The backlog number — 9,037 commercial aircraft at the end of March — is the context that makes everything else interpretable. At the current delivery target of 870 per year, Airbus has more than a decade of work in its order book. At the 1,000-plus delivery rate Faury has discussed as a long-term ambition, it still represents more than nine years. No quarterly delivery shortfall changes that reality in any meaningful way. What it does is delay the translation of that backlog into cash flow — and that delay compounds, because customers waiting longer for their aircraft sometimes get impatient.

02

The Q1 Numbers: A Difficult Quarter by Any Measure

The headline figures from Q1 2026 were genuinely weak. Revenue of €12.7 billion represented a 7% decline year-on-year. EBIT adjusted — the metric Airbus uses to strip out one-off items and focus on operational performance — fell 52% to €300 million, from roughly €624 million in Q1 2025. Free cash flow before customer financing came in at negative €2.5 billion, reflecting both the low delivery count and the planned inventory build-up associated with the production ramp.

The disconnect between EBIT adjusted (−52%) and net income (+5%) is worth unpacking. Net income benefited from below-the-line items — financial income, tax effects, and other non-operational adjustments — that masked the operational deterioration. This is not an unusual pattern for Airbus in weak delivery quarters, but it can mislead investors who focus on the bottom line without understanding that EBIT adjusted is the metric that tracks the underlying health of the aircraft business. On that measure, Q1 2026 was genuinely poor.

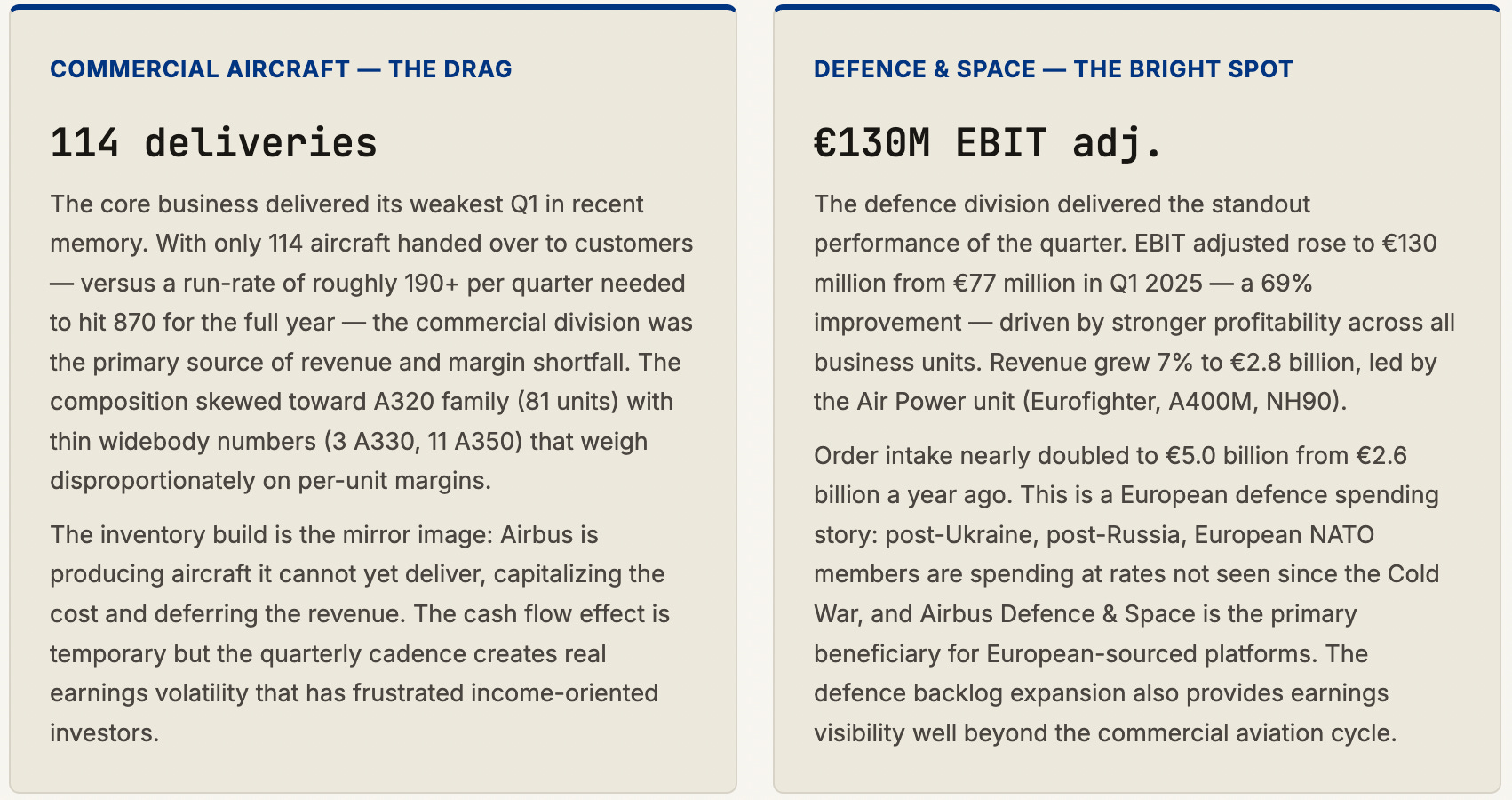

The delivery composition tells a further story. Of the 114 commercial aircraft delivered, 81 were A320 family — the narrowbody workhorse that generates the bulk of revenues and margin. Only 11 A350s were delivered, a widebody number that reflects both the production ramp-up challenges and the persistent supply chain issues that have made the A350 program a continuing source of earnings volatility. Three A330s completed the widebody count, with 19 A220s rounding out the deliveries.

03

The Pratt & Whitney Problem: Two Years and Counting

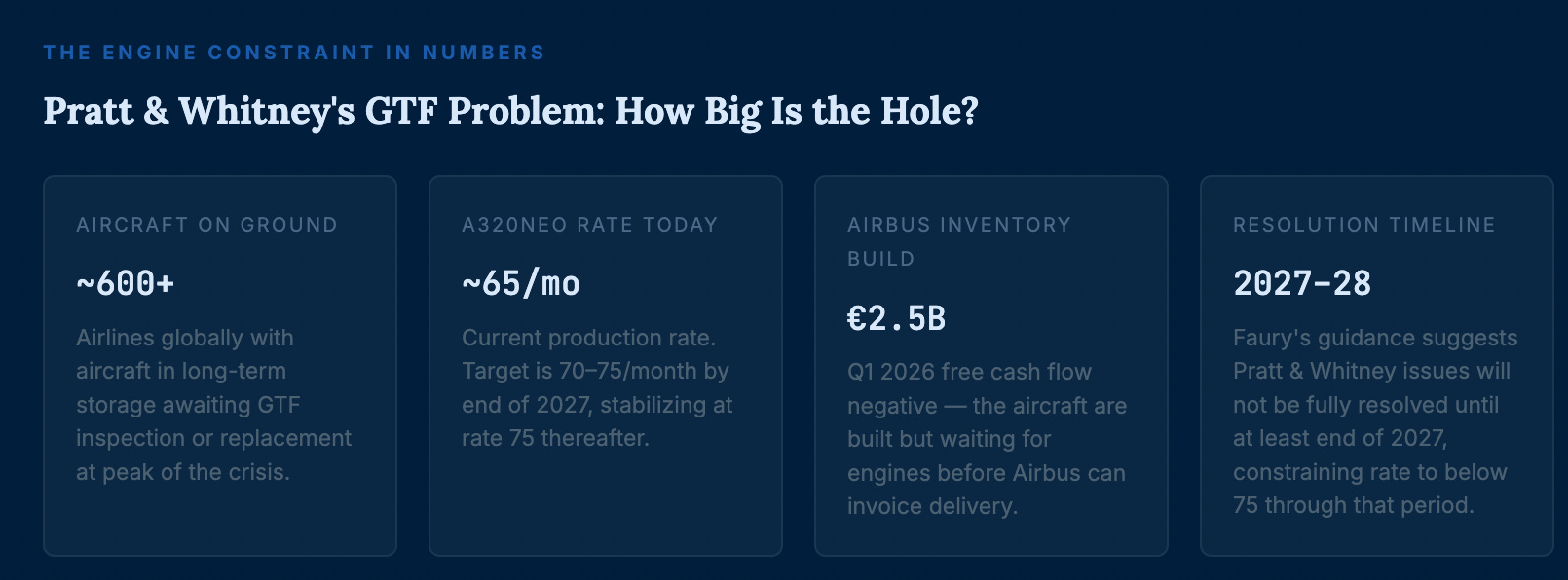

The single most important constraint on Airbus’s ability to deliver aircraft — and therefore to generate revenue and cash flow — is a problem it does not control and cannot solve directly: Pratt & Whitney’s inability to supply GTF engines at the rate the production ramp requires. CEO Faury named Pratt & Whitney explicitly as “the key pacer of the ramp-up trajectory, impacting both 2026 and 2027.” This is not a new observation. The engine issue has been the central limiting factor for two years.

The GTF (Geared Turbofan) engine — which powers the A320neo family, the dominant narrowbody in Airbus’s portfolio — developed a manufacturing defect in its powder metal components that required engines in service to be inspected and in many cases removed for checks. The resulting shortage of serviceable engines created a dual problem: airlines grounding existing aircraft for inspections, and new aircraft sitting on Airbus’s ramp at Toulouse and Hamburg waiting for engines before they could be delivered and accepted by customers.

The economic mechanics of the engine problem are especially irritating for Airbus. The company does not manufacture the GTF engine — that is Pratt & Whitney’s product. But when an aircraft can’t be delivered because an engine isn’t available or certified, Airbus doesn’t recognize revenue. The aircraft sits on the ramp as work-in-progress inventory, consuming cash and capital, contributing nothing to the income statement. The company has been building planes faster than it can deliver them for the better part of two years, creating the unusual situation of negative free cash flow alongside strong order intake and rising backlog.

The situation also creates complications with Chinese customers specifically. Airbus noted that “administrative difficulties” — a diplomatic euphemism that almost certainly involves trade tension residue and aviation authority certification processes — held up the delivery of nearly 20 aircraft to China in Q1. China represents a significant share of the A320neo order book, and any sustained delivery disruption to that market creates both near-term revenue headwinds and longer-term relationship risk at a time when COMAC’s C919 is beginning to compete for domestic Chinese airline orders.

04

Segment Breakdown: Where the Quarter Was Won and Lost

Airbus operates in three segments — Commercial Aircraft, Helicopters, and Defence & Space — and their Q1 2026 performance diverged sharply. The commercial division dragged; Defence & Space carried. Understanding each segment is essential to forming a view on where the full-year recovery will come from.

05