American Express Financial Triumph: Record Revenues and Strategic Growth

American Express Financial Triumph: Record Revenues and Strategic Growth

A Year in Review: Unveiling the Success Story Behind the Soaring Revenues and EPS, and the Strategic Decisions That Shaped 2023

Overall Financial Performance

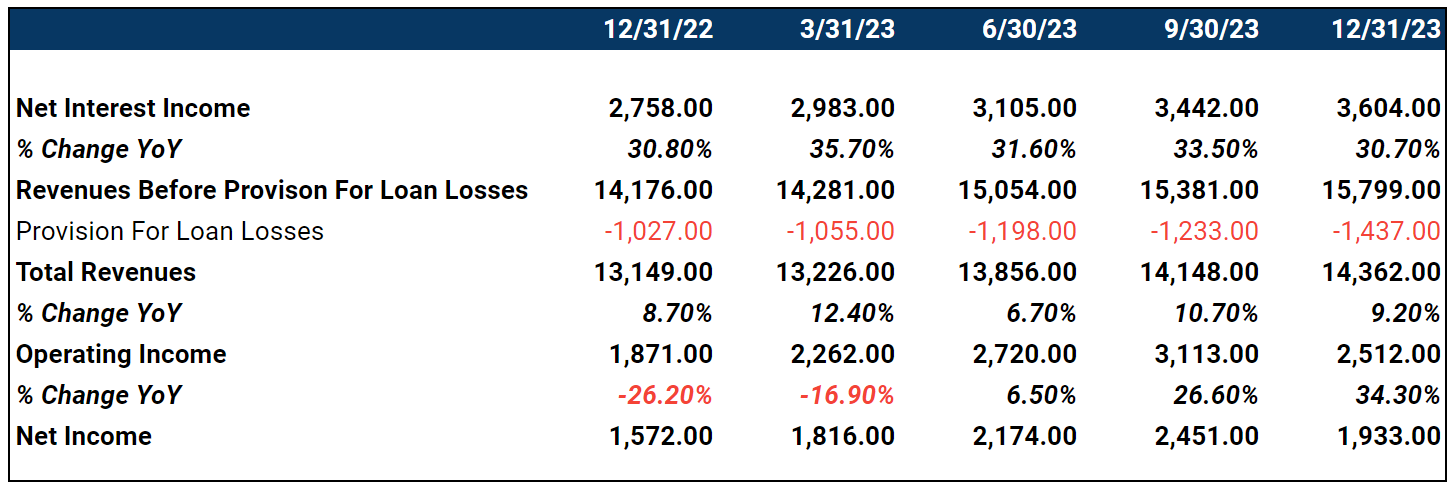

Q4 2022: Exceptional revenue and EPS growth, with record revenues of $52.9 billion for the full year (up 27%) and an EPS of $9.85.

Q1 2023: Robust revenue growth with record revenues of $14.3 billion (up 22% YoY). Guidance for 2023 was set at 15% to 17% revenue growth and EPS of $11 to $11.40.

Q2 2023: Continued strong performance, with record revenues of $15 billion (12% YoY increase) and an EPS of $2.89 (up 12%).

Q3 2023: Seventh consecutive quarter of strong performance, with record revenues of $15.4 billion (up 13% YoY) and an EPS of $3.30.

Q4 2023: Record revenues of $61 billion for the full year (up 15% FX-adjusted), with Q4 revenues nearly $16 billion and an EPS of $2.62.

Next Quarter Estimates:

Market Data:

52 Week High: $204.77

52 Week Low: $140.91

Avg. 3 Month Volume: 3.14 MM

5 Yr Beta: 1.22

Short Interest: 0.9%

Growth:

Fwd 2-Yr Rev. CAGR: 9.0%

Fwd 2-Yr EPS CAGR: 13.6%

Last 3-Yr Rev. CAGR: 18.8%

Last 3-Yr EPS CAGR: 43.8%

Capital Structure:

Market Cap: $145,633.89

Enterprise Value: $1.00

Shares Outstanding: 723.00 MM

LTM Net Debt: $2,000.00

Valuation:

Street Target Price: $198.92

NTM P/E: 16.02x

NTM MC/FCF: 14.13x

Efficiency:

LTM Gross Margin: 60.2%

LTM ROA: 3.4%

LTM ROE: 31.8%

LTM P/E: 17.97x

LTM P/BV: 5.20x

LTM P/NCAV: (29.65x)

Dividend Yield: 1.2%

Return Ratios:

Return on Assets (ROA): 3.0%

Return on Equity (ROE): 28.0%

Return on Common Equity: 27.5%

Margin Analysis:

Gross Profit Margin: 60.5%

SG&A Margin: 38.2%

EBT Excl. Non-Recurring Items Margin: 17.5%

Income From Continuing Operations Margin: 13.5%

Net Income Margin: 13.5%

Normalized Net Income Margin: 10.9%

Net Avail. For Common Margin: 13.3%

Asset Turnover:

Short Term Liquidity:

Current Ratio: 1.75x

Quick Ratio: 1.75x

Strategic Growth and Customer Engagement

Q4 2023: Implementation of a post-COVID growth plan focused on higher annual revenue and mid-teens EPS growth, with innovations and technology advancements in response to customer needs.

Q3 2023: Alignment with growth plans announced in 2022, aiming for over 10% annual revenue growth and mid-teens EPS growth in 2024 and beyond.

Card Member Spending and Demographics

Q1 2023: Global billed business up 16% YoY. Travel and Entertainment (T&E) spending increased by 39% YoY.

Q2 2023: All-time high in Card Member spending, especially strong in U.S. consumer and international segments.

Q3 & Q4 2023: Consistent growth in Card Member spending, with notable increases in fee-based product acquisitions.

Credit Metrics and Risk Management

Across all quarters: Consistent emphasis on best-in-class credit performance, disciplined growth, and risk management. High retention rates and stable credit metrics maintained throughout the year.

Investments and Strategic Partnerships

Q3 2023: Investments in value propositions, including Resy acquisition and a new partnership with Formula 1.

Q2 2023: Continuous strategic investments and extension of the Hilton partnership for 10 years.

Expense Management and Capital Allocation

Q4 2023: Effective expense management indicated by total expenses growing slower than revenue. Capital returned to shareholders amounted to $5.3 billion in 2023.

Q1 to Q3 2023: Focused on driving efficiencies in marketing and operating expenses, with full-year expenses anticipated around $14 billion to $14.5 billion.

International Business and Market Dynamics

Q1 & Q2 2023: Strong international growth, particularly in Card Services and T&E spending.

Q4 2022 & 2023: Robust performance in International Consumer and SME segments.

Outlook and Future Projections

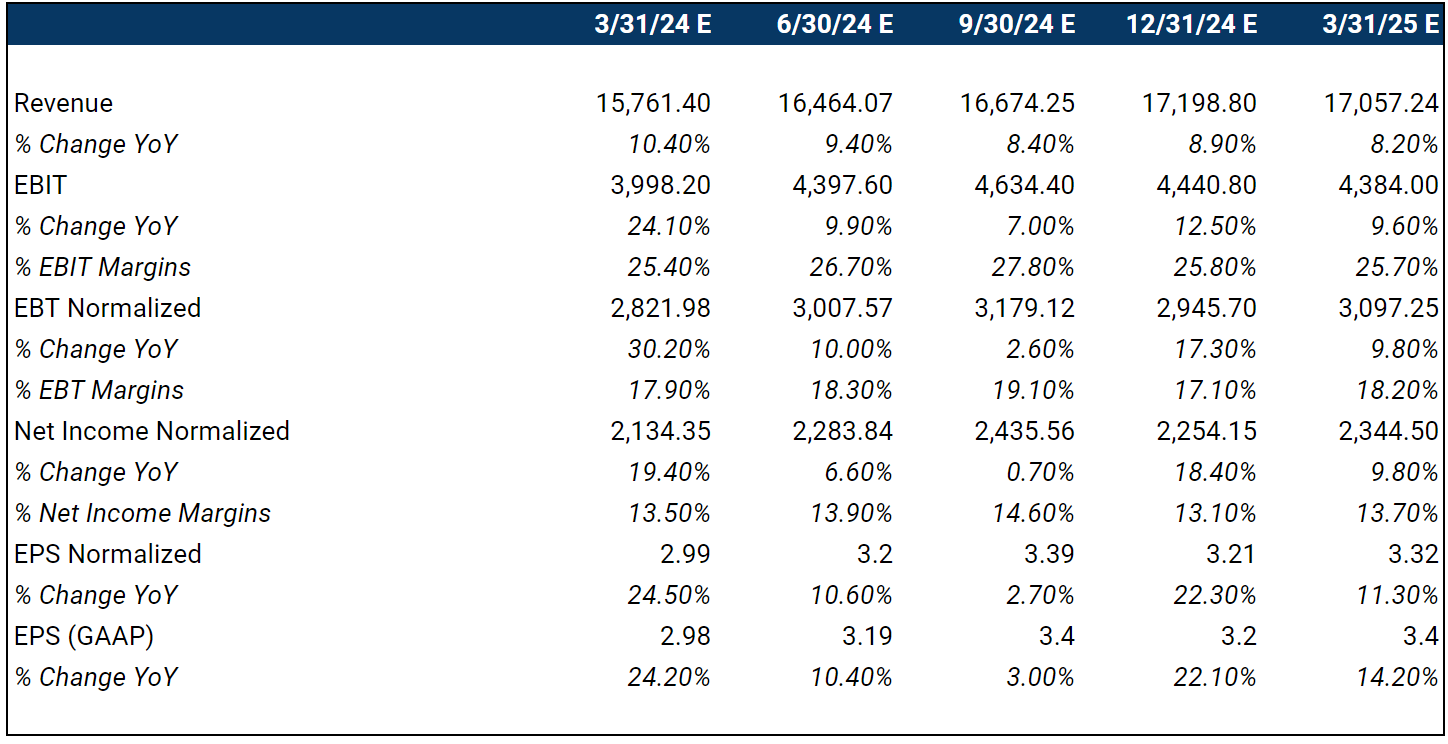

Q4 2023: Anticipated revenue growth between 9% and 11% for 2024, with full-year EPS expected between $12.65 and $13.15. A planned increase in quarterly dividend to $0.70 per share.

Q1 to Q3 2023: Consistent commitment to achieving sustainable revenue growth in excess of 10% and mid-teen EPS growth in a steady-state macro environment.

Premium Customer Base Expansion

Q4 2023: Approximately 25 million new proprietary card accounts added over the last 2 years, with over 70% being fee-based products.

Generational and Geographical Reach

Q4 2023: Strong brand relevance among Millennial and Gen Z consumers, with younger consumers representing a significant portion of new account acquisitions.

Business Segments Performance

Q4 2023: U.S. Consumer segment grew by 7%, Commercial Services showed consistent growth, and International Card Services exhibited strong double-digit growth.

Credit and Loans Dynamics

Q4 2023: Year-over-year growth in loans and Card Member receivables by 13%, with continued strong credit performance.

CFO Transition Announcement

Q2 2023: Jeff Campbell stepped down as CFO, succeeded by Christophe Le Caillec.

SME and Corporate Spending

Q4 2022 & 2023: U.S. SME growth at 2% to 6%, with focus on aiding SME clients in business operations and international expansion.