AstraZeneca: The $80 Billion Ambition on Track — Mostly

8% revenue growth, 4 Phase III wins, and a pipeline so deep it reads like a wish list. Q1 26 confirmed that AstraZeneca's transformation from mid-tier British pharma to global oncology powerhouse

Executive Summary

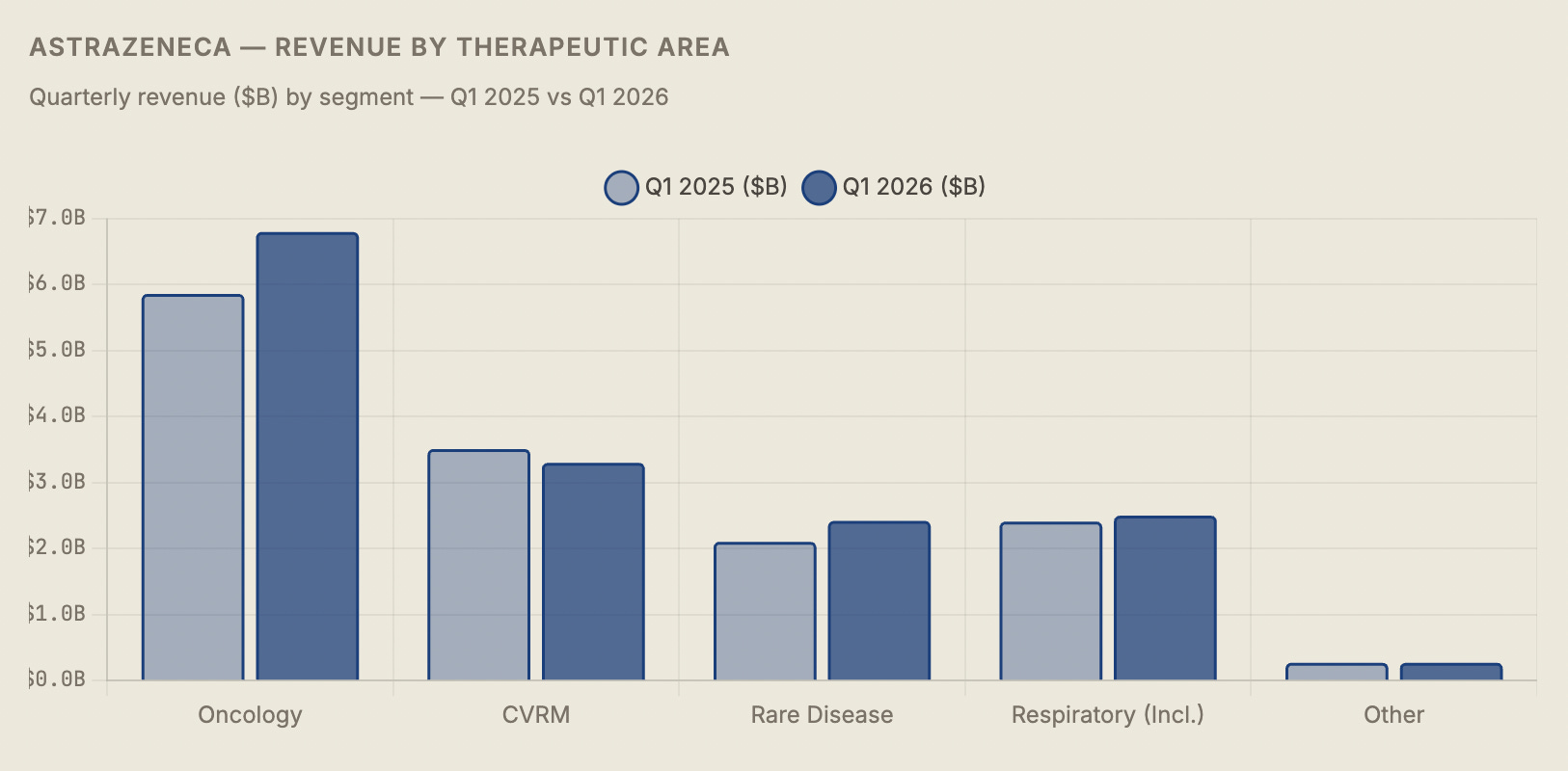

AstraZeneca delivered a clean beat in Q1 2026 — revenue of $15.3 billion (+8%), core EPS of $2.58, four positive Phase III readouts, and a bold reaffirmation of its $80 billion revenue ambition for 2030. The oncology division grew 16% to $6.8 billion, anchored by Tagrisso, Imfinzi, and the rapidly scaling Enhertu franchise which is now annualizing at a $5 billion run rate. Rare Disease added $2.4 billion at 15% growth. The pipeline delivered genuine news: first pivotal data for tozorakimab in COPD and efzimfotase alfa in hypophosphatasia, plus continued Enhertu expansion into earlier-stage cancer settings.

The headline exception is the CVRM (Cardiovascular, Renal, Metabolism) division, which declined 6% to $3.3 billion as Farxiga — once positioned as a blockbuster bridge across diabetes, heart failure, and chronic kidney disease — faced its first material loss-of-exclusivity headwinds, falling 3% to $2.2 billion. Brilinta’s generics-driven collapse (−67%) compounded the problem. BioPharmaceuticals as a whole was down 2%.

The strategic picture remains compelling: AstraZeneca is the only large-cap pharma with a multi-therapeutic pipeline that can credibly replace expiring blockbusters through organic R&D rather than M&A alone. The $80 billion by 2030 target — which would represent more than a doubling of 2022 revenues in eight years — is aggressive but increasingly supported by the data. The China risk, however, is the unresolved variable that deserves more attention than it typically receives in sell-side coverage.

01

The Transformation: From Blockbuster Hangover to Pipeline Machine

To understand why AstraZeneca’s Q1 2026 results matter beyond the quarterly numbers, you have to go back to 2012. That year, AstraZeneca was a company in serious trouble: its two biggest products — the blockbuster cholesterol drug Crestor and the blood thinner Brilinta’s predecessor — were approaching patent cliffs, its pipeline was widely regarded as thin, and its share price was in multi-year decline. Pfizer made a hostile takeover approach in 2014; then-CEO Pascal Soriot famously called it “inadequate” and turned it down, betting that AstraZeneca could rebuild itself from within.

What followed was one of the most consequential pharmaceutical turnarounds of the modern era. Soriot and his team made a deliberate decision to concentrate R&D investment in three therapeutic areas where AstraZeneca had scientific adjacency and room to build genuine franchise depth: oncology, cardiovascular/renal/metabolic disease, and rare disease. They licensed aggressively — the deal to co-develop Enhertu with Daiichi Sankyo for $6.9 billion in 2019 now looks like one of the best pharmaceutical business development transactions of the decade. They entered the COVID vaccine race (AZ-Oxford), generating cash and credibility even as the vaccine itself was eventually discontinued.

By 2026, the results of that bet are visible in the financials in a way that would have seemed improbable in 2014. Revenue has grown from roughly $26 billion in 2022 to a $61 billion annualized run-rate, and the $80 billion target for 2030 is now backed by a pipeline with over 180 projects and a track record of clinical success that is genuinely unusual in an industry where most drugs fail. The Q1 2026 quarter is a check-in on a decade-long thesis — and the score is mostly positive.

“Strong revenue growth and positive readouts from high-value NMEs reinforce confidence in our 2030 ambition. We have the pipeline depth to sustain mid-to-high single-digit growth for the rest of the decade.”

— Pascal Soriot, CEO, AstraZeneca — Q1 2026 earnings call, April 29, 2026

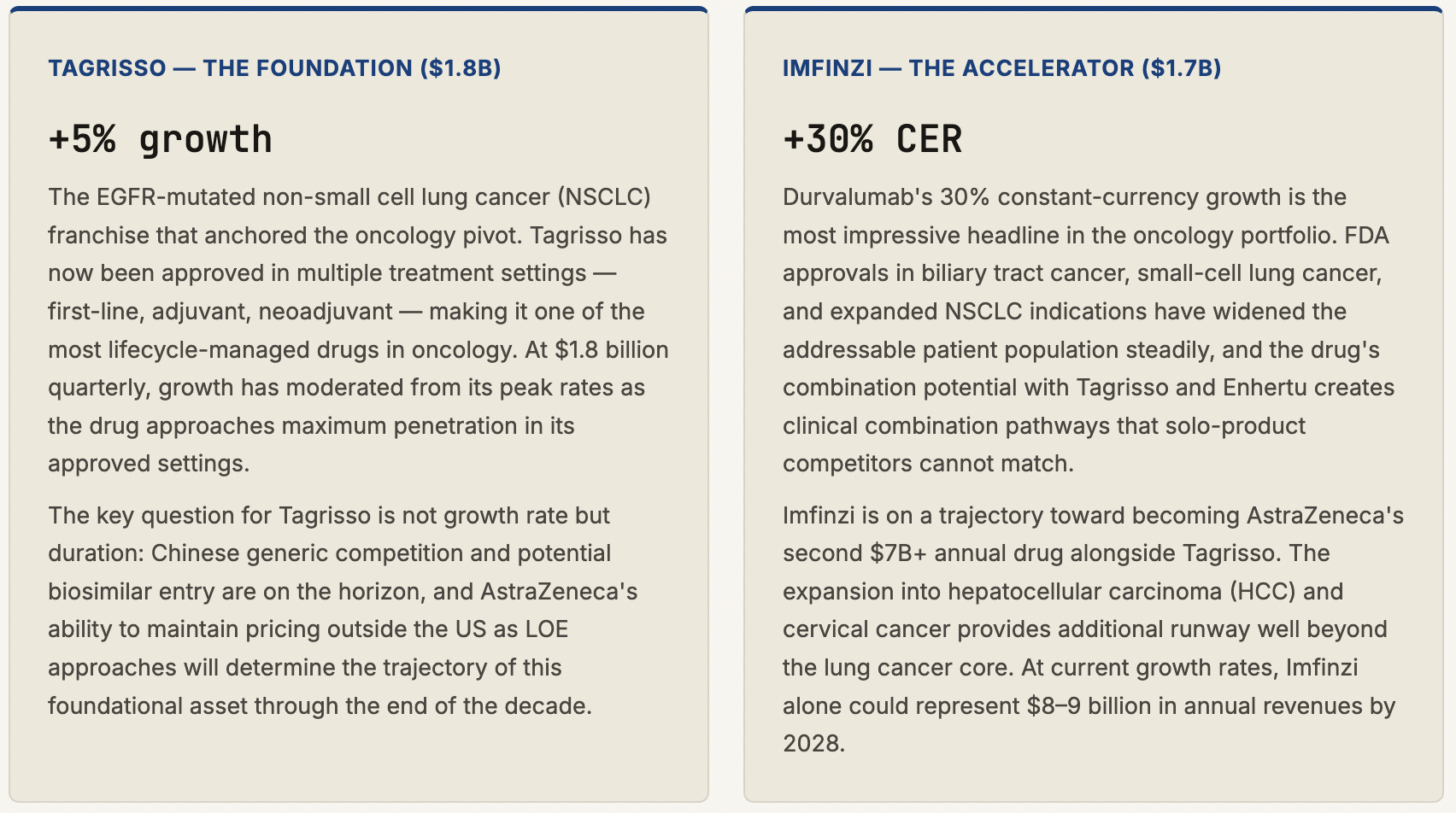

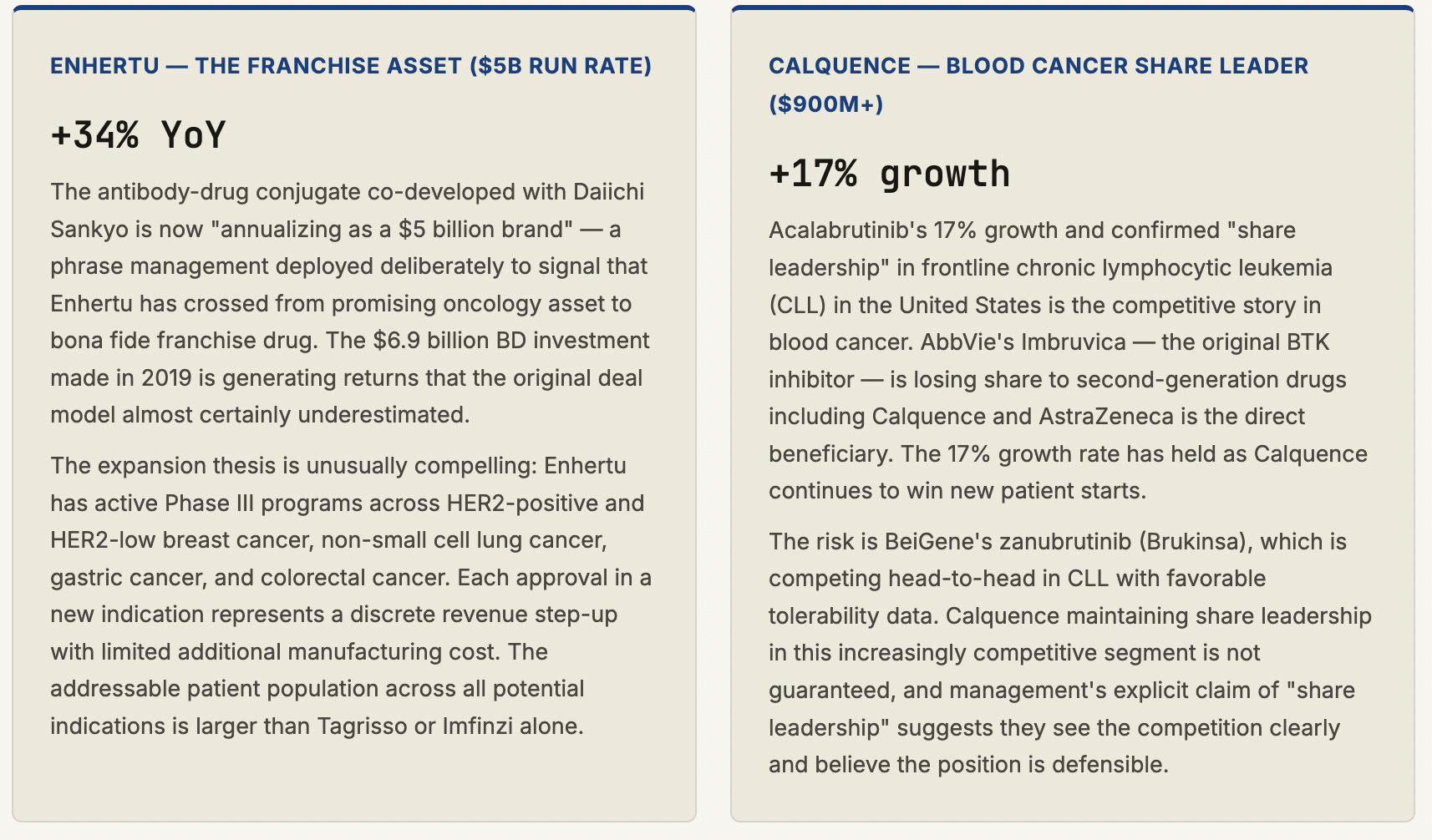

The Enhertu trajectory alone validates the transformation thesis. When AstraZeneca committed $6.9 billion to co-develop the antibody-drug conjugate with Daiichi Sankyo — a bet that looked expensive and risky at the time — it was purchasing access to a technology platform and a lead compound that has since been approved in multiple cancer indications, generated more than $3 billion in annual revenues, and is now “annualizing as a $5 billion brand.” The royalty-bearing nature of the Enhertu agreement means AstraZeneca gets revenue from a drug it did not invent but is jointly commercializing — a partnership model that has become central to the company’s R&D strategy and one of the most studied deals in the industry.

02

Q1 2026 Results: The Numbers Behind the Beat

The headline read was a clean beat against consensus. Revenue of $15.288 billion came in above the $14.9 billion analyst estimate — a 2.6% beat on the top line that is meaningful for a company of this scale. Core EPS of $2.58 exceeded the $2.54 forecast. Operating profit grew 12%, faster than revenue, reflecting the operating leverage inherent in a pharma business where R&D spending is largely fixed and commercial scaling carries attractive incremental margins.

The segment mix shift visible in this table is the central narrative of AstraZeneca’s investment story. Five years ago, CVRM was the growth engine and oncology was a promising but unproven bet. Today, oncology at $6.8 billion is 44% of quarterly revenues and growing at 16% while CVRM is shrinking. The company has successfully executed a product mix rotation that most pharmaceutical companies attempt and few complete. The question for the next five years is whether the pipeline can do it again — replacing Farxiga’s eventual LOE cliff with new products in the CVRM space, particularly in obesity and metabolic disease where AstraZeneca recently made its largest external bet.

03

Oncology: The Engine That Runs AstraZeneca

AstraZeneca’s oncology division is not a portfolio of drugs. It is a franchise — a collection of deeply interconnected assets that reinforce each other across cancer types, treatment lines, and combination strategies. Understanding it requires examining each major product not as a standalone revenue line but as a node in a network of clinical evidence that is self-reinforcing and increasingly hard for competitors to replicate at scale.

04