Bloom Energy: AI Data Centers Ignite a Generational Revenue Inflection

Revenue more than doubled (+130%) as hyperscaler demand for reliable, dispatchable power sent Bloom's fuel cell orders surging

Stock: ⚡ The 55-Day AI Power \"Fix\" vs. The $20 Billion Backlog")

The Moment Bloom Energy Has Been Building Toward

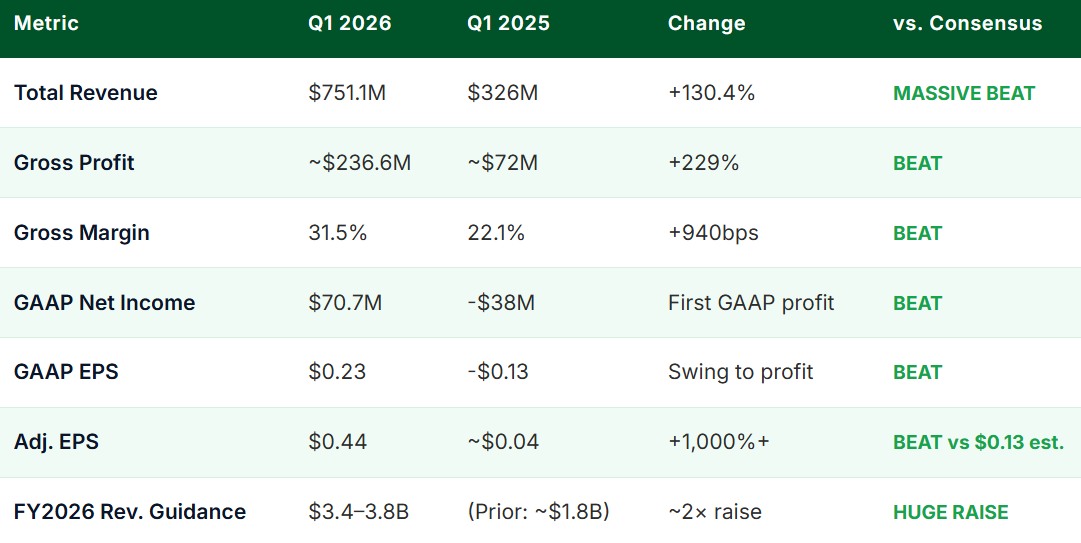

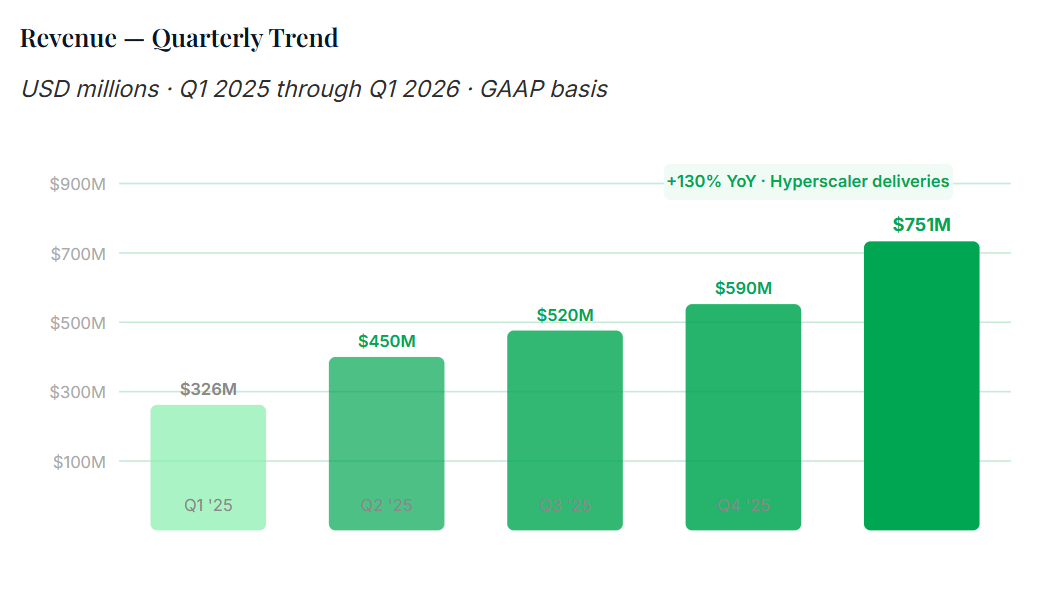

For years, Bloom Energy occupied a paradoxical position in the clean energy investment universe: a company with genuinely differentiated technology, a compelling long-term narrative around on-site power generation, and a frustrating inability to translate those advantages into consistent profitability. That story changed dramatically in Q1 2026. Revenue of $751.1 million more than doubled year-over-year, adjusted EPS of $0.44 beat the consensus estimate of $0.13 by an astonishing 238%, and — perhaps most significantly — the company posted its first materially positive GAAP EPS of $0.23. Net income of $70.7 million was a watershed moment for a company that had been investing heavily in growth for over a decade.

The catalyst is not complicated: artificial intelligence data centers have created a demand for reliable, dispatchable, non-grid-dependent power that perfectly aligns with what Bloom Energy’s solid oxide fuel cell (SOFC) technology offers. Data centers — particularly the large, dense GPU clusters required for AI training — need power that is always available, uninterrupted, and ideally sited as close to the compute load as possible. Grid power, constrained by transmission bottlenecks, renewable intermittency, and grid reliability concerns, increasingly cannot meet that demand alone. Bloom’s fuel cell servers, which run on natural gas (or hydrogen blends) and generate electricity through an electrochemical process with greater efficiency than combustion, are emerging as the preferred on-site power solution for hyperscalers willing to pay for certainty.

The numbers that underpin this story are remarkable. Full-year 2026 guidance was raised to $3.4-3.8 billion — implying that Bloom will generate in a single year what previously took three years of cumulative revenue to reach. The order backlog is growing faster than revenue, and management indicated that multiple large hyperscaler customers have signed multi-year capacity commitment agreements that extend through 2028 and beyond.

Revenue Explosion: Anatomy of the 130% Growth

Bloom Energy’s revenue model has two primary components: product revenue from the sale of Energy Servers (the core fuel cell systems), and service and installation revenue from ongoing maintenance contracts and commissioning work. In Q1 2026, the primary driver was a dramatic surge in product revenue as large, committed hyperscaler orders that were signed in 2025 reached delivery and revenue recognition.

This is a critical distinction for investors: Bloom recognizes product revenue when systems are delivered and commissioned, not when contracts are signed. The dramatic Q1 revenue surge reflects the delivery execution of a backlog that has been building for 12-18 months. The $3.4-3.8 billion full-year guidance implies that Q1’s ~$750 million represents roughly 20% of anticipated full-year revenue, suggesting an approximately even-to-slightly-back-weighted delivery schedule throughout the year.

Why Data Centers Need Bloom Energy

To understand the magnitude of the demand inflection, it helps to understand the physics and economics of data center power. A large AI training cluster running 10,000+ H100/H200 GPUs requires approximately 100-500 megawatts of continuous electrical power. At those scales, the traditional grid-connection approach faces severe constraints: transmission line upgrades take 5-10 years, utility rate cases can delay new substations for years, and renewable power (while cost-competitive) is intermittent — solar doesn’t generate at night, wind doesn’t generate in calm weather.

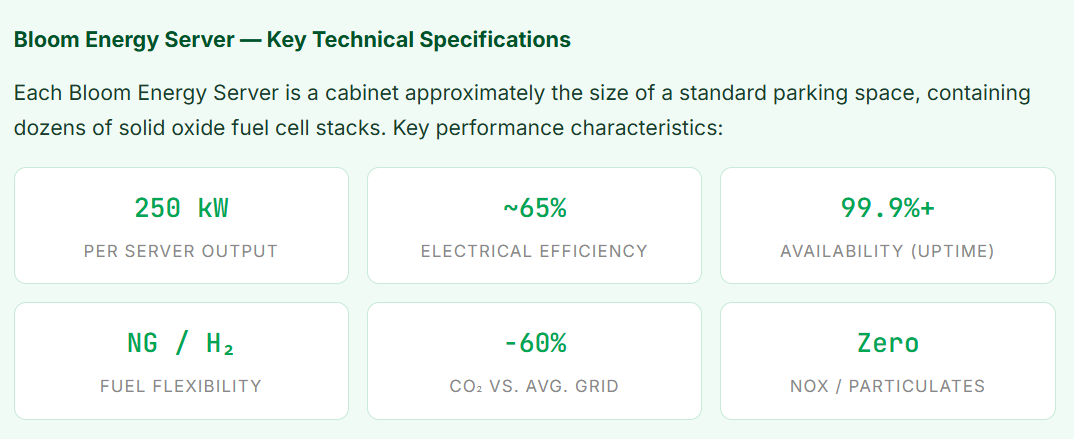

Bloom Energy’s solution is to place Energy Server stacks at or adjacent to the data center footprint, running on pipeline natural gas. A typical Bloom Energy Server generates 250 kilowatts at approximately 65% electrical efficiency — roughly twice the efficiency of a combustion turbine. Multiple servers are configured in arrays to reach tens or hundreds of megawatts of on-site generation capacity. The result is power that is: always available (24/7 dispatchable), grid-independent, sited exactly where needed, and clean enough to satisfy corporate sustainability commitments (lower emissions than grid power in most U.S. states, and compatible with hydrogen blending as the green hydrogen supply chain matures).

The Technology Advantage: Solid Oxide Fuel Cells

Bloom Energy’s technology is worth understanding because it is genuinely differentiated from alternative on-site power solutions and from other fuel cell technologies. Solid oxide fuel cells (SOFC) operate at high temperatures (approximately 800°C), which enables them to reform natural gas internally — the electrochemical process extracts hydrogen from methane molecules and converts it directly to electricity without combustion. The absence of combustion means the process produces no nitrogen oxides (NOx) or particulates, and the CO₂ emissions are approximately 40-60% lower per kilowatt-hour than coal or gas grid power in most regions.

The hydrogen fuel flexibility is the long-term strategic value. As green hydrogen — produced via electrolysis powered by renewable energy — becomes cost-competitive with natural gas (currently projected for the early 2030s), Bloom Energy’s servers can transition from natural gas to hydrogen without hardware replacement, simply by changing the fuel supply. This means customers are not locked into natural gas perpetually; they are buying a platform that can decarbonize progressively as hydrogen economics improve.

Profitability: The Long-Awaited Inflection

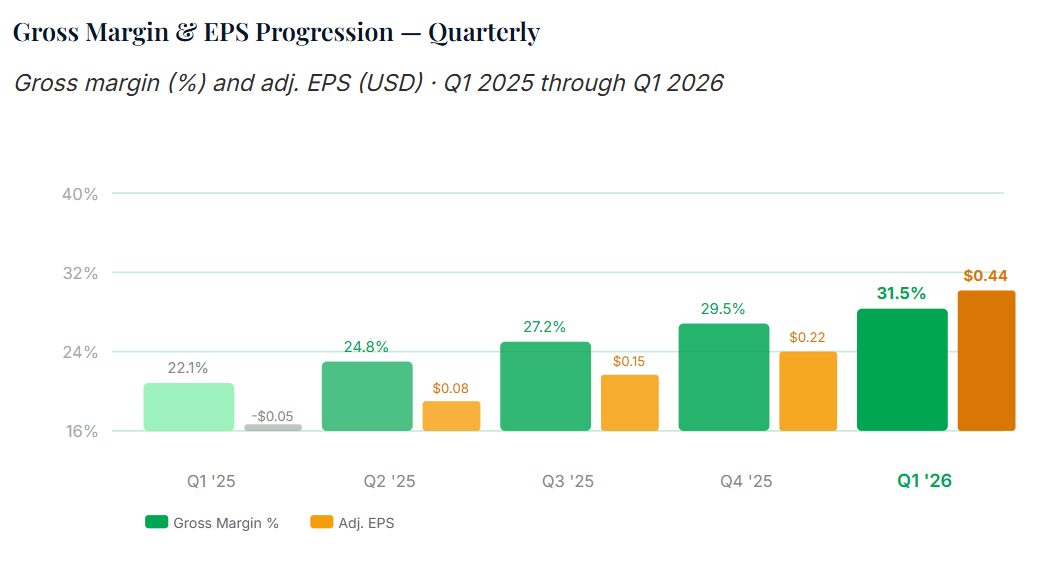

Gross margin of 31.5% in Q1 2026 represents a significant expansion from the approximately 22-24% margins that Bloom was generating 18 months ago. The improvement reflects three drivers: manufacturing scale benefits as production volumes have roughly doubled, more favorable contract pricing as hyperscaler urgency to secure capacity has allowed Bloom to improve contract terms, and a more favorable product mix toward larger, higher-margin enterprise deployments versus smaller commercial installations.

Full Quarter Scorecard