Cisco Posts Record $15.8 Billion Quarter as AI Orders Surge to $9 Billion

A giant long dismissed as ex-growth has found its second act. Fueled by hyperscaler AI infrastructure spending, record networking orders, and a restructuring that bets the company on silicon

Section 01

Quarter at a Glance

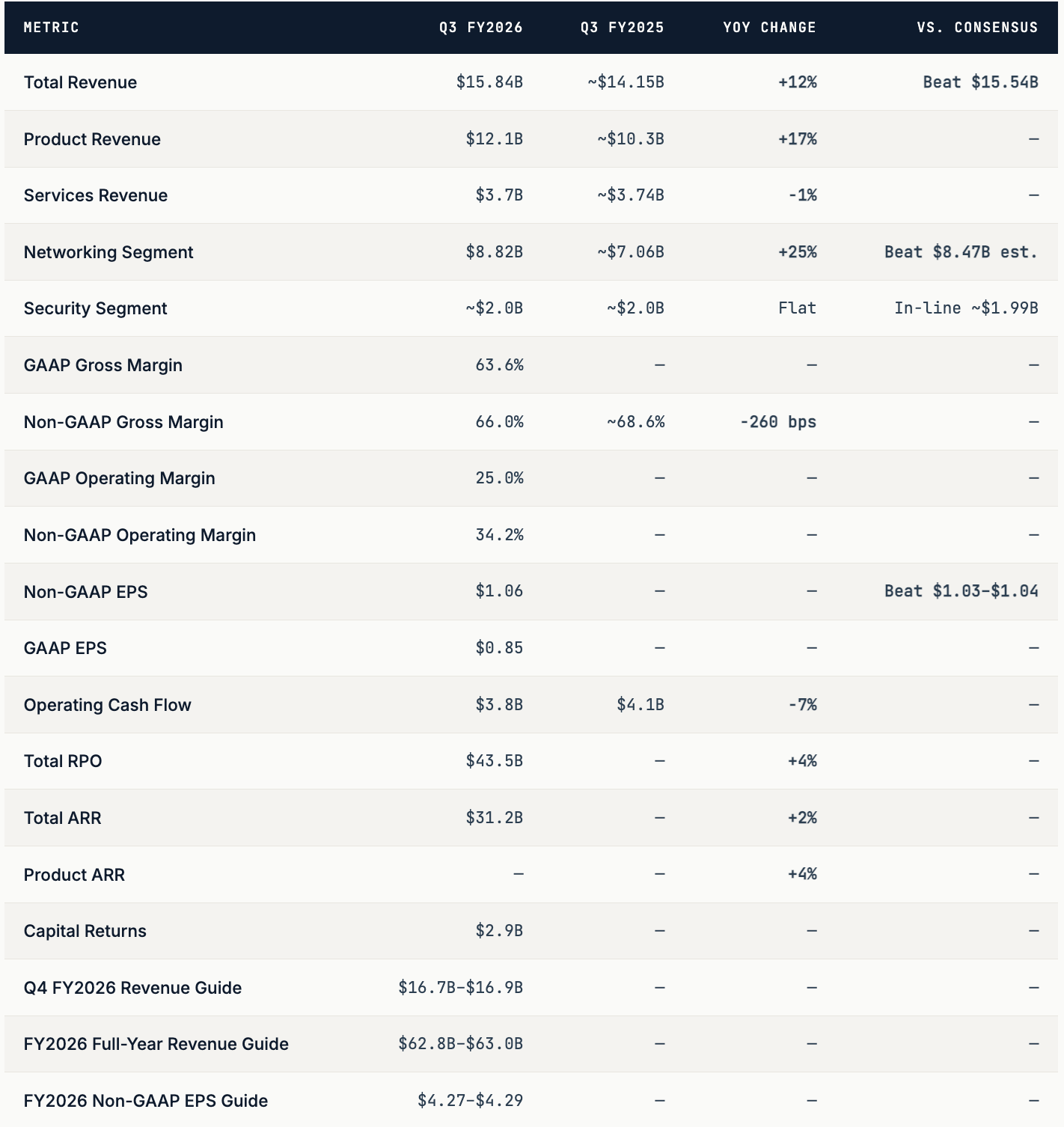

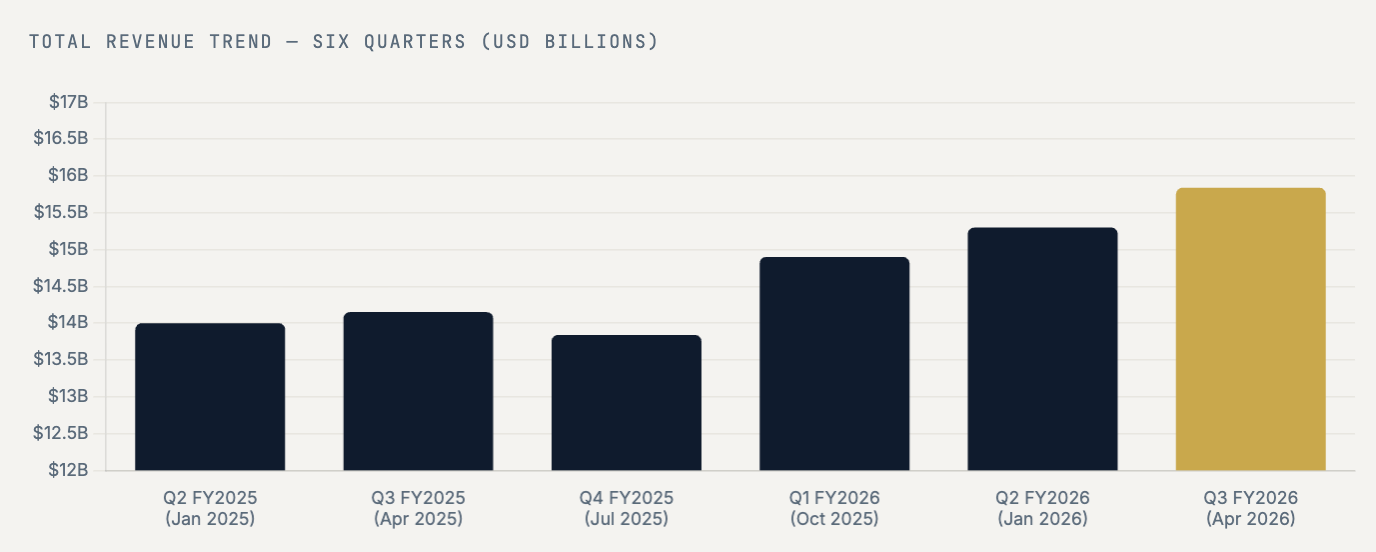

For a company that spent the better part of a decade defending its legacy perch while hyperscalers built their own switches and Arista Networks feasted on data center market share, Cisco’s third fiscal quarter of 2026 is a thunderclap. Revenue of $15.84 billion surpassed both the prior-year period by 12% and analyst consensus estimates of roughly $15.54–15.56 billion. It is the largest quarterly revenue in the company’s 41-year history.

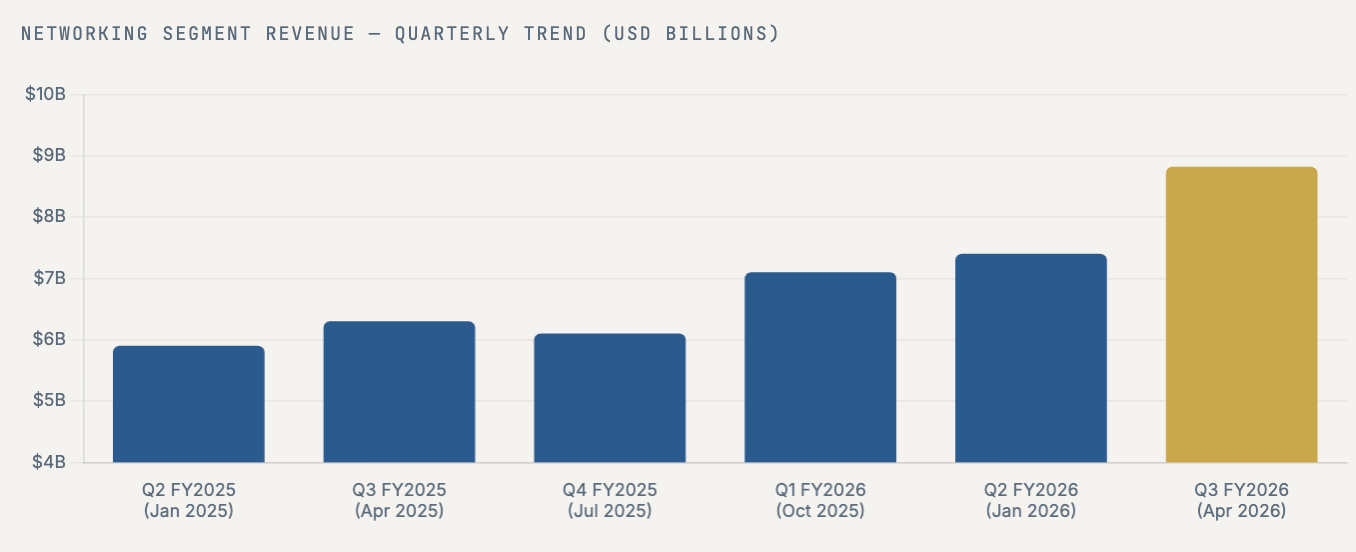

The beat was broad-based and driven by something more durable than a one-time inventory flush. Networking revenue soared 25% to $8.82 billion on the back of hyperscaler AI infrastructure orders that have been accelerating every quarter since the cycle turned. Product orders companywide rose 35% year over year, while networking product orders alone grew more than 50% — with service provider routing and compute posting triple-digit growth and data center switching, campus switching, wireless, enterprise routing, and industrial IoT each delivering double-digit gains.

On the bottom line, non-GAAP earnings per share came in at $1.06, ahead of the $1.03–$1.04 consensus, on non-GAAP net income of $4.2 billion. GAAP net income was $3.4 billion, or $0.85 per diluted share, weighed in part by restructuring charges associated with the company’s announced 4,000-person workforce reduction — a subject we will examine in detail. The market’s verdict was unambiguous: Cisco shares surged approximately 17–20% in after-hours trading on May 13, pushing the stock to its highest level in years.

The guidance raise was equally striking. Cisco now expects full-year fiscal 2026 revenue of $62.8–$63.0 billion and non-GAAP EPS of $4.27–$4.29, both materially above prior-quarter forecasts of $61.2–$61.7 billion and $4.13–$4.17, respectively. For Q4, the company guides revenue of $16.7–$16.9 billion, implying another record sequential quarter.

Section 02

Networking: Riding the AI Wave

The single most consequential data point in Cisco’s Q3 print is the $9 billion. That is the revised full-year fiscal 2026 target for AI infrastructure and hyperscaler orders — up from the prior guidance of $5 billion, which itself was a raise from the original $1 billion target when management first began tracking the metric. Through the first three quarters of the fiscal year, Cisco had already logged $5.3 billion in AI infrastructure orders. In Q3 alone, hyperscaler AI orders reached $2.1 billion, up from $1.3 billion in Q2.

These are not vague aspirations. They represent binding commitments from the world’s largest cloud operators — Microsoft Azure, Google Cloud, Amazon Web Services, Meta, and a constellation of sovereign AI builders — to deploy Cisco networking equipment inside the AI factories now being constructed at a pace that would have seemed fantastical just two years ago. The Ethernet networking ecosystem that Cisco anchors is increasingly winning the AI fabric debate against proprietary InfiniBand alternatives, as hyperscalers seek interoperability, multi-vendor resilience, and cost efficiency at scale.

“Networking product orders grew more than 50% in Q3, driven by triple-digit growth in service provider routing and compute, and double-digit growth in data center switching, campus switching, wireless, enterprise routing, and industrial IoT.”

— Cisco Q3 FY2026 Earnings Release, May 13, 2026

The Cisco Nexus 9000 series — the company’s flagship data center switch — is at the center of this demand surge. Deployed in spine-leaf topologies across AI clusters that may comprise thousands of GPU nodes, the Nexus 9000 benefits from a network effect of sorts: the larger the AI cluster, the more switching capacity required, and the more routing intelligence needed at the edge. Cisco’s Catalyst 9000, meanwhile, continues to drive a campus refresh cycle as enterprises upgrade to Wi-Fi 7 and higher-density access layer architectures that can support AI inference at the edge.

Silicon One, Cisco’s proprietary network processor family, is increasingly a strategic weapon rather than a cost center. Originally introduced to serve the hyperscaler custom silicon wave by offering a merchant alternative to Broadcom’s Tomahawk and Jericho families, Silicon One has now been designed into several major hyperscaler networks. The chip handles both routing and switching in a single programmable architecture, a flexibility that matters enormously as AI workloads evolve and traffic patterns shift from conventional east-west data center flows to the all-to-all communication patterns characteristic of large-scale model training.

Networking revenue of $8.82 billion came in 4% ahead of the $8.47 billion analyst consensus. The 25% year-over-year growth rate accelerated from the double-digit pace seen in the prior two quarters, and the order momentum — if sustained — suggests that this is not simply a pull-forward from a pent-up refresh cycle but a new, structurally higher demand regime tied to the AI capital expenditure supercycle that hyperscalers have publicly committed to continue through at least 2027 and 2028.

Beyond the hyperscaler channel, enterprise networking demand is also recovering after the multi-year inventory digestion cycle that suppressed Cisco’s growth through much of fiscal 2024 and 2025. Enterprises that had over-ordered campus switches and wireless access points during the supply chain disruption era have finally worked through that excess, and the combination of Wi-Fi 7 availability and AI-at-the-edge deployments is triggering a new replacement wave. The campus networking recovery is still early, adding another leg to a stool that is already well-supported by AI infrastructure.

Section 03

Security & Splunk: The $28 Billion Bet

When Cisco closed its $28 billion acquisition of Splunk in February 2024, it was the largest deal in the company’s history — a statement of intent that Cisco intended to transform itself from a network equipment provider into an AI-powered security and observability platform. More than two years later, the verdict on that bet is coming into focus, and it is more nuanced than either the bulls or bears anticipated.

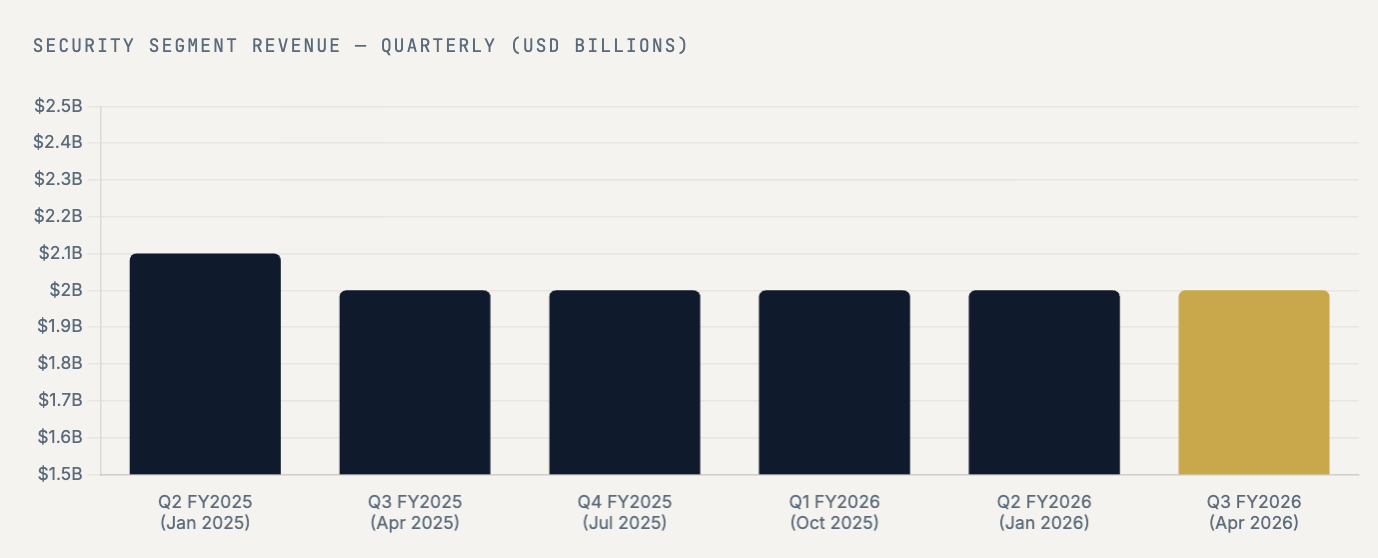

Security segment revenue was flat at approximately $2 billion in Q3 FY2026, landing right around the $1.99 billion analyst consensus. Flat is not exactly the growth profile investors hoped to see from a business anchored by a freshly acquired $28 billion asset, but management has been consistent in explaining the dynamic at work. Cisco is deliberately migrating Splunk from an on-premises perpetual-license model — where customers pay large upfront fees — to a cloud subscription model that recognizes revenue more gradually and predictably. This transition, while creating a near-term revenue headwind as large on-premise contracts roll off, sets the foundation for durable, high-margin recurring revenue.

Splunk by the Numbers

Total ARR reached $31.2 billion, up 2% year over year, with product ARR growing 4%. Splunk added approximately 500 new customer logos in the first half of fiscal 2026 and remains on pace to exceed its target of 1,000 new logos for the full year. The mix of cloud business is expected to continue growing into Q4, with the transition from on-premises to cloud subscriptions serving as the primary driver of near-term security revenue softness.

The strategic rationale for the Splunk deal was always about more than the revenue line. Splunk’s SIEM platform, now rebranded under Cisco Security Cloud, ingests and analyzes security telemetry at massive scale — precisely the kind of capability that becomes more valuable, not less, as AI introduces new attack surfaces across enterprise networks. Cisco’s ambition is to fuse Splunk’s observability depth with its own network-native visibility to deliver what management calls an AI-native security operations platform.

This positioning addresses a genuine and growing market need. As enterprises rush to deploy AI agents, AI-powered applications, and AI infrastructure, the attack surface expands exponentially. Every new GPU cluster is a potential entry point. Every large language model API endpoint is a potential vector for data exfiltration. The combination of Cisco’s network traffic intelligence — which, as the dominant provider of enterprise routers and switches, Cisco can observe at a depth that no pure-play security vendor can match — with Splunk’s log aggregation and threat detection capabilities creates a theoretically differentiated SIEM-plus-network-intelligence product.

The integration is also progressing on the go-to-market front. Cisco’s security portfolio now spans Extended Detection and Response (XDR), Secure Access Service Edge (SASE), Zero Trust Network Access, and cloud-native firewall capabilities. The company’s pivot to selling security as a platform, rather than as a collection of point products, is philosophically aligned with how enterprise security buyers increasingly want to consolidate their vendor relationships — particularly in a macro environment where IT budgets remain under scrutiny and CISOs are under pressure to demonstrate ROI.

That said, the competitive pressure in security is fierce. Palo Alto Networks and CrowdStrike have both built deeply entrenched customer relationships in enterprise endpoint and cloud security, and both have been successfully executing their own platform consolidation strategies. Cisco must compete not only on technical capability but on the strength of its channel relationships — an area where its scale and partner ecosystem remain genuine assets — and on the speed of its Splunk integration. Investors will be watching security ARR growth and the pace of Splunk’s cloud transition closely in the quarters ahead.

Section 04

The Subscription Transition

Beneath the headline revenue and EPS figures lies a more consequential transformation in how Cisco earns its money. The company has been executing a multiyear pivot from a predominantly product-and-maintenance model — sell a router, collect a year of service contract — to a subscription-first model where hardware, software, and cloud services are bundled into annual or multi-year contracts that renew predictably.

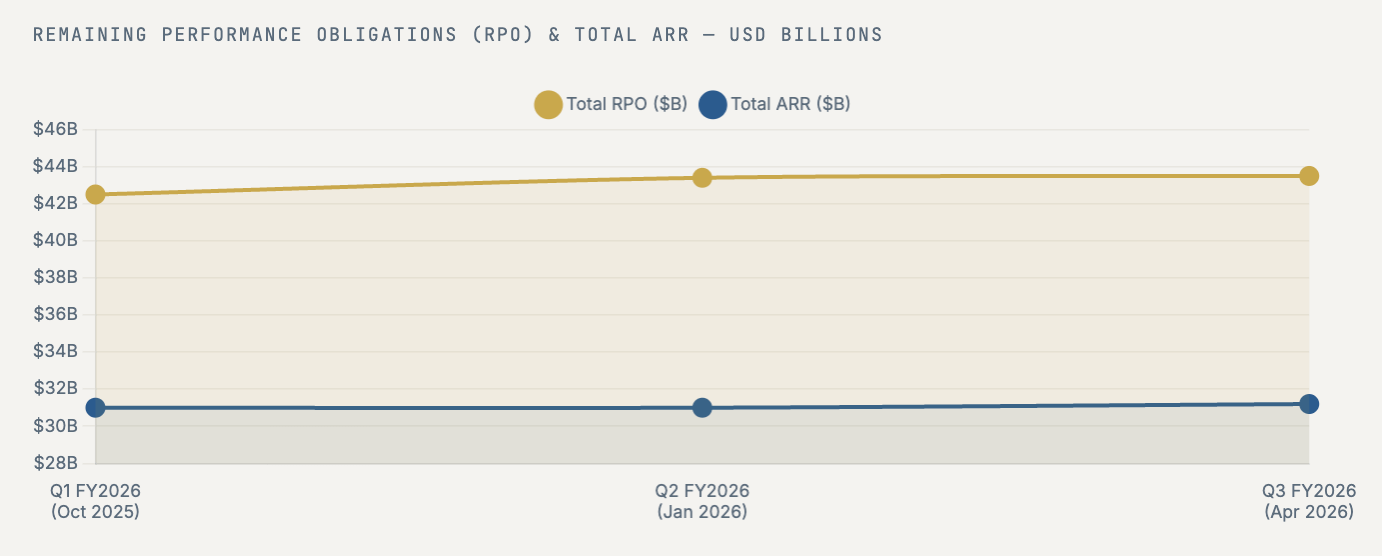

The most visible evidence of this transition is Remaining Performance Obligations, the accounting measure of contracted revenue not yet recognized. Cisco’s total RPO stood at $43.5 billion at the end of Q3 FY2026, up 4% year over year. Product RPO grew 6%, with the long-term portion — contracts extending beyond twelve months — rising to $11.7 billion, itself up 6%. These figures represent a growing forward revenue backlog that provides visibility well beyond the current quarter and insulates the business from the kind of order lumpiness that historically made Cisco’s product revenue volatile.

Annual Recurring Revenue, the subscription-economy metric that captures the annualized value of active recurring contracts, reached $31.2 billion, up 2% in total with product ARR growing 4%. The 2% total growth rate reflects the ongoing Splunk transition dynamic described above — as on-premise contracts are not renewed in favor of cloud subscriptions, there is a temporary gap in recognized ARR before the cloud contracts ramp. This accounting headwind is expected to ease through fiscal 2027 as the installed base completes its cloud migration.

The more important question for long-term investors is whether Cisco’s networking products — historically sold as capital expenditure — can successfully transition to a subscription basis. Cisco has been pushing its Catalyst Center software (formerly DNA Center), which unlocks premium networking features and management capabilities on a subscription basis, as well as Cisco Plus, its as-a-service networking and infrastructure offering that allows enterprises to consume switching, routing, and wireless capacity on an operational-expenditure basis. Adoption of these programs has been growing, though the base remains modest relative to the overall business.

The AI networking wave actually complicates the subscription transition narrative somewhat. Hyperscalers typically buy networking equipment as capital expenditure — they want to own the hardware in their data centers — and they have the scale and sophistication to negotiate directly against Cisco’s list price. The subscription mix for AI infrastructure is therefore likely to remain lower than for enterprise campus networking. Management will need to demonstrate that it can grow software and subscription attach rates on top of the hardware wins, rather than simply growing the hardware volume.

Cisco’s guidance of $4 billion in full-year AI infrastructure revenue — up from a prior target of $3 billion — is an important signal in this context. Revenue lags orders by several months as product ships and is deployed, and the $4 billion target implies significant hardware-recognition in the current fiscal year. The subscription layers on top of that hardware foundation are where the real long-term value creation opportunity lies.

Section 05