Constellation Brands: The Quarter Before the Cup

Constellation Brands opened Nicholas Fink's first full fiscal year with a clean beat, a quiet rotation inside its beer portfolio, and $400 million returned to shareholders — all before a single World Cup match landed in its numbers. The tournament, the tariffs, and the Hispanic consumer will decide what comes next.

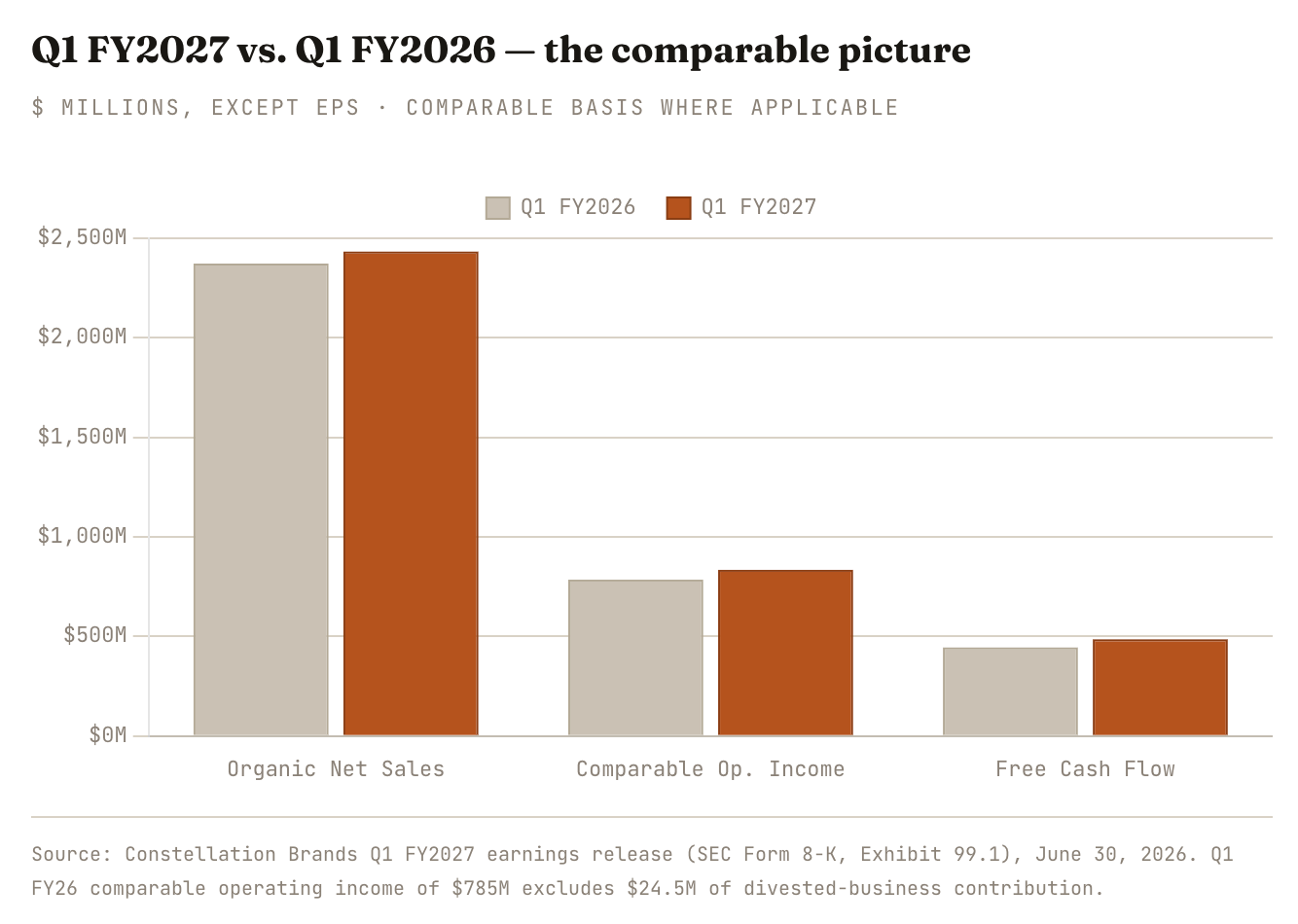

Constellation Brands reported its fiscal first-quarter 2027 results after the close on June 30, and the headline is refreshingly simple for a company that has spent four quarters apologizing: it beat. Net sales of $2.43 billion came in ahead of the roughly $2.39–2.40 billion the Street expected, and comparable EPS of $3.43 topped consensus near $3.21–3.22 by a comfortable margin, growing 7% against a year-ago quarter that was itself under pressure. Reported EPS of $3.79 jumped 31%, flattered by commodity derivative gains and tax valuation-allowance adjustments, but the comparable line — the one management is paid on — did the work honestly: 2% beer net sales growth, disciplined cost control, lower interest expense, and a share count that is 3% smaller than a year ago.

The context makes the beat matter more than its size. This was the first reporting period fully under new CEO Nicholas Fink, who took the chair in mid-April after the company’s bruising fiscal 2026 — a year that ended with beer margins absorbing a 340-basis-point hit from aluminum tariffs and higher depreciation in Q4 and management withdrawing its fiscal 2028 outlook entirely, citing tariff and macro uncertainty. Consumer sentiment remains at recessionary depths (the University of Michigan index sat near 45 heading into the print), and the Hispanic consumer — roughly half of Constellation’s beer buyers — remains squeezed by cost-of-living pressure and, more distinctively, anxiety around immigration enforcement that has dampened both social occasions and purchasing behavior. Against that backdrop, a quarter of organic growth, stable 39% beer margins, and reaffirmed guidance reads as evidence that the floor is holding.

The LongYield Take

This was a stabilization quarter, not an inflection quarter — and that’s exactly what the stock needed. Beer shipments grew 1.8%, depletions were essentially flat (−0.3%), and the company kept its 39% segment margin despite heavier marketing spend and tariff drag. The real story is the rotation happening inside the portfolio: Pacifico depletions surged ~21% and Victoria ~14% while Modelo Especial slipped ~2% and Corona Extra fell over 5%. Constellation’s growth engine is changing brands mid-flight.

The setup for Q2 is the most interesting in years. The quarter closed May 31 — eleven days before the 2026 World Cup kicked off across the U.S., Mexico, and Canada. Management is front-loading marketing above 10% of net sales into Q2 and Q3 to capture it. Whether that spend converts a flat-depletion business into a growing one is the single biggest swing factor in the FY27 guide.

01 — The Print

A beat built on execution, not luck

Strip out the noise and the quarter’s mechanics are clean. Enterprise net sales fell 3% on a reported basis to $2,433 million, but that decline is entirely an artifact of the 2025 Wine Divestitures — the June 2025 sale of the mainstream wine portfolio removed $142 million of year-ago revenue from the comparison. On an organic basis, which excludes the divested brands, net sales grew 3%. Comparable operating income rose 6% to $834 million, lifting the comparable operating margin 120 basis points to 34.3%. Reported operating income surged 18% to $845 million, helped by a $49 million swing in undesignated commodity derivative marks and much lighter impairment charges than a year ago.

Below the operating line, two structural tailwinds did quiet work. Net interest expense fell 13% to $86 million as the company redeemed its 3.700% senior notes due 2026 and refinanced. And the diluted share count dropped to 172.4 million from 178.0 million — the compounding residue of a buyback program that repurchased $324 million of stock fiscal-year-to-date through June. Add it together and comparable net income of $591 million (+3%) translated into 7% comparable EPS growth. The company returned over $400 million to shareholders in the quarter across buybacks and its $1.03 quarterly dividend, while holding to its ~3.0x comparable net leverage target and continuing construction of its third Mexican brewery at Veracruz.

Cash generation kept pace with the P&L. Operating cash flow of $662 million rose 4%, and free cash flow of $485 million grew 9% as capital expenditures moderated to $177 million — Constellation is now past the peak of its Mexican capacity build, with the modular Veracruz project absorbing a declining share of a ~$800 million full-year capex budget. On a trailing basis the company converts roughly a fifth of revenue into free cash, which is what funds the shareholder-return flywheel while debt sits near $10.5 billion gross against a ~$24 billion market capitalization.

02 — The Beer Engine

Flat depletions, and why that’s a win

The Beer Business — roughly 94% of enterprise revenue post-divestitures — grew net sales 2% to $2,284 million on 1.8% shipment growth and continued favorable pricing. Segment operating income rose 2% to $891 million, holding the operating margin essentially flat at 39.0% versus 39.1% a year ago. That flatness deserves respect: it was achieved while absorbing unfavorable mix, higher marketing spend ahead of the World Cup, and the ongoing aluminum tariff drag that crushed margins two quarters ago. Volume growth and pricing added $29 million and $3 million respectively to operating income; SG&A took back $13 million.

Depletions — the sell-through measure that tracks what distributors actually move to retailers, and the truest gauge of consumer demand — declined 0.3%. In isolation that sounds anemic. In context, it’s the best depletion print in several quarters for a company whose core consumer is under documented stress, and management noted the business outperformed the total U.S. beer category by nearly 3 percentage points in year-over-year dollar sales across Circana tracked channels. Constellation was once again the #1 dollar share gainer in U.S. tracked channels, with five of the top fifteen share-gaining brands in the entire American beer category. The category is shrinking; Constellation is taking its shelf.

The cadence within the quarter tells the macro story better than any survey. On the call, management described a strong March that softened through April and May as gasoline prices rose and squeezed discretionary spending, followed by a modest — not full — recovery in early June. That’s a consumer buying beer paycheck-to-paycheck, and it’s why management resisted the temptation to raise the comparable guide despite the beat.

“Despite a discerning and value-conscious consumer environment, we grew organic net sales” — and took share doing it.

— Nicholas Fink, President & CEO, Q1 FY2027 earnings release

03 — The Rotation