Coupang:Rocket Delivered — Margin Did Not: Coupang's Data Breach Hangover

Revenue beat, stock rose, and Farfetch hit its first positive economics since acquisition. The problem is Adjusted EBITDA fell from $382M to $29M. The question is whether this is temporary

his publication is for informational purposes only and does not constitute investment advice. Financial figures sourced from Coupang Q1 2026 earnings release and management commentary. Segment revenue figures and historical estimates are approximations based on public disclosures and analyst consensus. Past performance is not indicative of future results.

Executive Summary

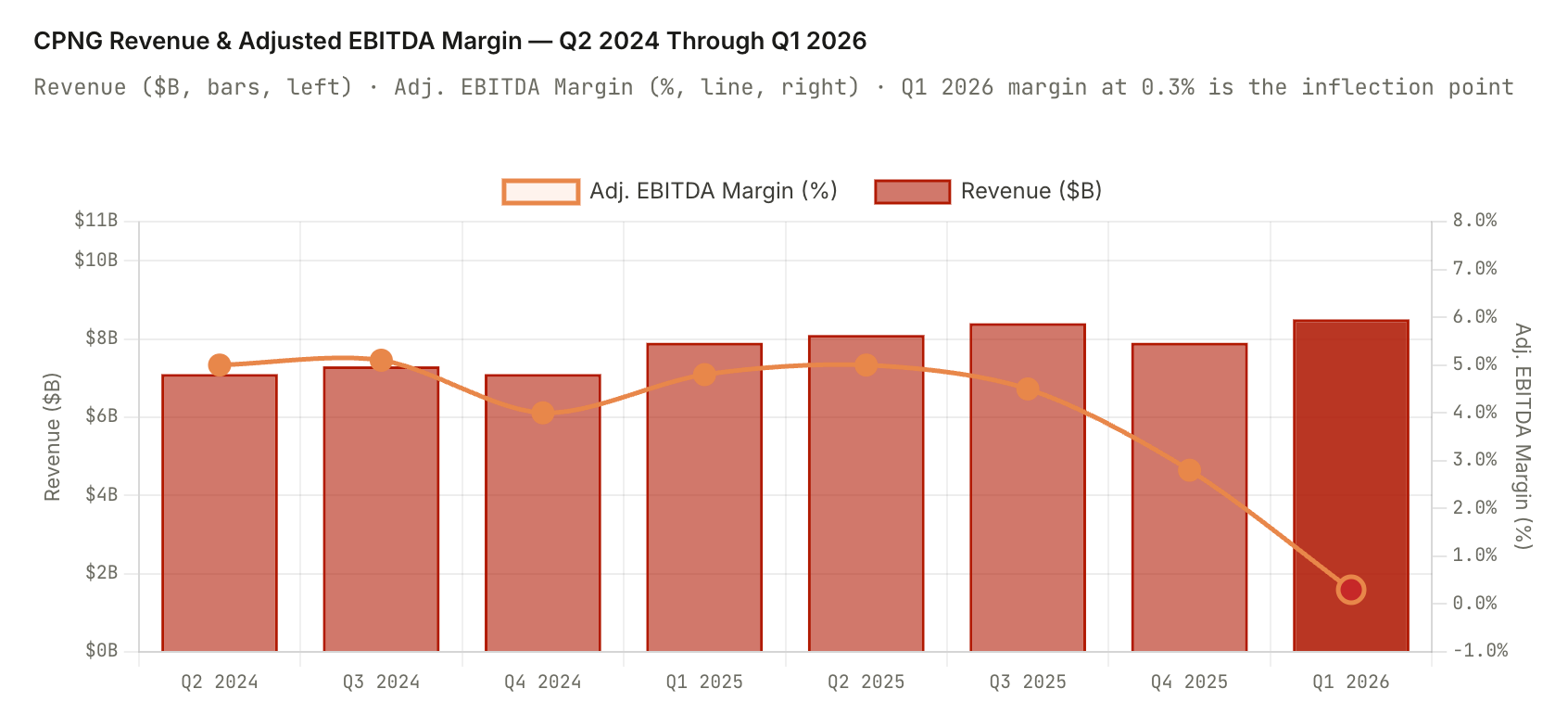

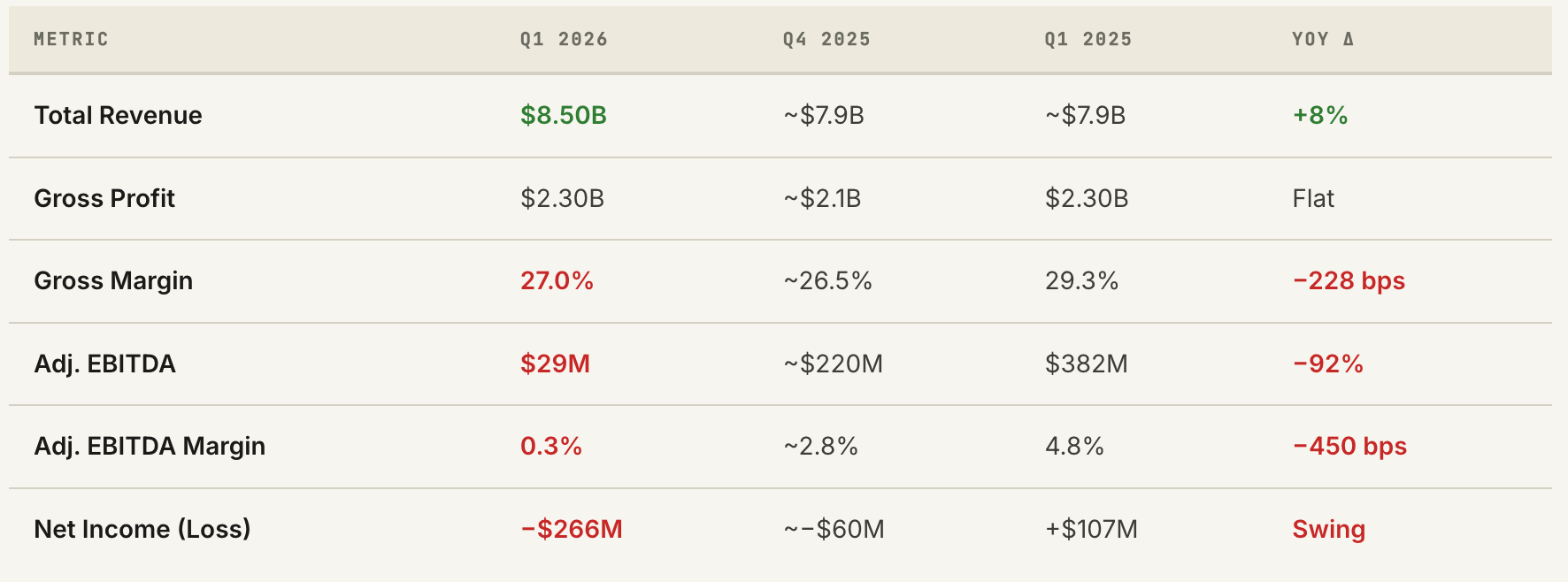

Coupang posted Q1 2026 revenue of $8.5 billion — an 8% year-over-year increase and a narrow beat against estimates. The stock rose on the report. That is the good news. The bad news is that Adjusted EBITDA collapsed from $382 million and a 4.8% margin in Q1 2025 to $29 million and a 0.3% margin in Q1 2026. Net income swung from positive $107 million to a loss of $266 million. Gross margin fell 228 basis points.

The explanation management offered is specific and, if accurate, temporary: the 2025 data breach forced Coupang to deploy aggressive voucher programs to rebuild customer trust and arrest customer churn, and those voucher costs hit Q1 2026 gross margin directly. Additionally, network inefficiencies — the cost of scaling logistics faster than volume utilization catches up — weighed on margins in both the Korean core and in Taiwan and Japan expansion markets. Offsetting this, Farfetch recorded positive year-over-year revenue growth and positive overall economics for the first time since Coupang acquired it. The stock market’s verdict — shares rose despite the EPS miss — reflects a belief that the margin decline is transitory. The editorial verdict in this report is more measured: the data breach hangover is real and temporary; the structural cost of international expansion is real and ongoing; and the durability of the recovery depends heavily on whether Korean e-commerce volume growth can reaccelerate as voucher programs phase out.

01 — The EBITDA Cliff

$382M to $29M in Twelve Months: Understanding the Margin Collapse

Adrop in Adjusted EBITDA from $382 million to $29 million — a 92% decline — in a single year is not a normal operating variance. For Coupang, a business that was demonstrating credible margin expansion through 2024 and into early 2025, this quarter represents a significant interruption to a narrative that investors had been rewarding with a premium multiple. Understanding whether that interruption is temporary or structural is the central question of this earnings report.

The margin decline has two distinct drivers. The first is the data breach. In 2025, Coupang experienced a significant data security incident that compromised personal data of millions of Korean customers. The company’s response was to deploy substantial voucher programs — essentially discounting purchases — to rebuild customer trust and prevent attrition to competitors including Naver Shopping and C-commerce platforms like AliExpress Korea. These vouchers are treated as a reduction to revenue or an increase to cost of goods sold, depending on their structure, and they hit the gross margin line directly. Coupang described this as the primary cause of the 228 basis point gross margin contraction.

The second driver is international expansion cost. Taiwan and Japan are both in investment phases where logistics network build-out and marketing spending run significantly ahead of the revenue and volume that justifies them. This is the correct operational approach — you build the infrastructure before the volume, not after — but it creates guaranteed near-term margin drag. The developing offerings segment, which includes Taiwan, Japan, Farfetch, Coupang Eats, and Coupang Play, is running at a deliberate loss as the international business matures.

02 — The Data Breach Hangover

What Happened, What It Cost, and When the Drag Ends

The 2025 data breach was one of the most damaging single events in Coupang’s operating history. Personal data — including purchase histories, addresses, and in some cases payment method information — of millions of Korean customers was compromised. In a country where Coupang’s value proposition rests fundamentally on trust (you give Coupang your home address, your credit card, and your entire purchasing history in exchange for next-morning delivery), a breach of that trust strikes at the core of the relationship.

Management’s response was aggressive and expensive. Voucher programs deployed across the customer base offered discounts on orders for affected customers, free WOW membership extensions for members who considered canceling, and expedited delivery upgrades for customers at the highest risk of attrition. The aggregate cost of these programs, flowing through the gross margin line, is the primary explanation for the 228 basis point gross margin contraction from Q1 2025’s 29.3% to Q1 2026’s 27.0%.

The critical question for investors is the duration of the voucher drag. Management indicated the programs were designed to phase out as customer trust metrics — measured by order frequency, retention rates, and WOW membership renewal rates — recover to pre-breach levels. If trust indicators are recovering on the trajectory management described in its Q1 commentary, the voucher programs would be substantially wound down by Q3 2026, and gross margin would begin recovering toward the 29–30% range in Q4 2026. That recovery path is the foundation of the base case scenario: the market looked through Q1 2026 to the recovery trajectory and bid shares up accordingly.

The risk is stickiness. Consumer trust, once broken, does not always recover on schedule. If a portion of Coupang’s highest-frequency Korean shoppers made permanent behavioral changes — resuming comparison shopping on Naver, experimenting with AliExpress Korea, or downsizing their WOW membership to a lower tier — the voucher cost may be necessary on an ongoing basis to hold them rather than as a one-time recovery measure. That scenario does not appear in management’s recovery narrative but should be monitored through Q2 and Q3 2026 order frequency data.

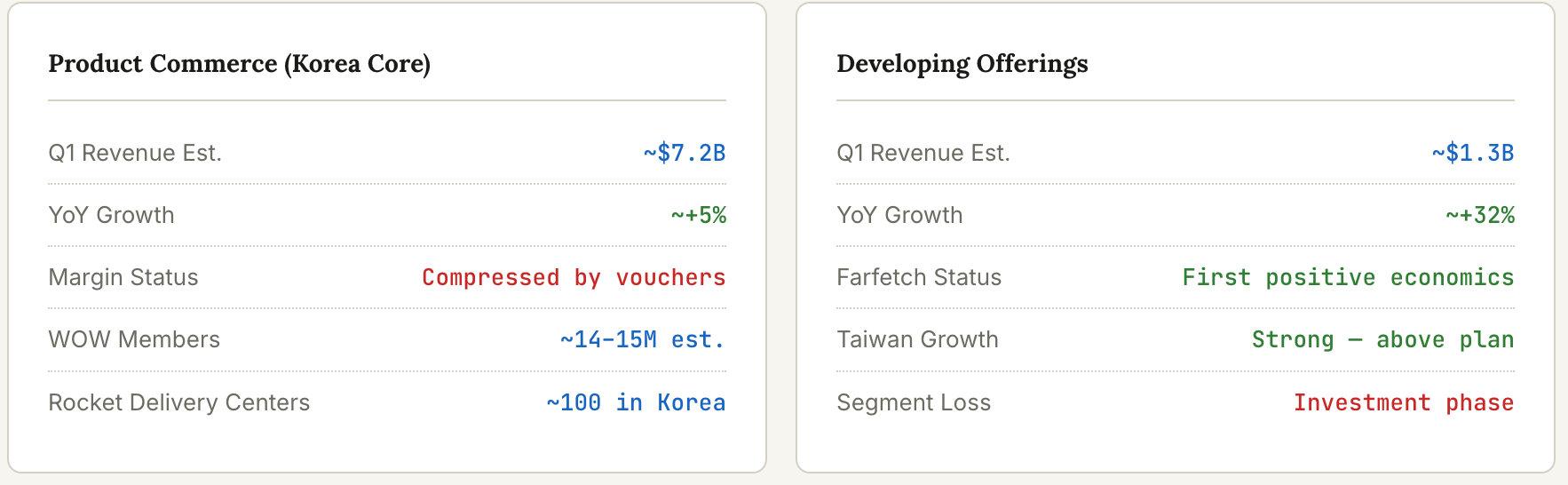

03 — Product Commerce: Korea’s Core Business

The Rocket Delivery Machine and the WOW Membership Flywheel

Coupang’s Product Commerce segment — Korean e-commerce, grocery delivery, and direct retail — is the business that funds everything else. It generates the revenue, the operating leverage, and the logistics infrastructure that makes Coupang’s value proposition unique. Understanding it requires understanding why Korea became the only country in the world where next-day delivery was replaced by next-morning delivery as the standard consumer expectation — and who built that infrastructure.

Coupang built approximately 100 fulfillment and logistics centers across South Korea — a country roughly the size of Indiana — over a decade of capital-intensive investment. The density of this network means that the vast majority of Korean consumers live within a few kilometers of a Coupang facility, enabling the “Rocket Delivery” promise: order by midnight, receive by 7 AM. No other competitor in Korea has replicated this logistics density. Naver Shopping, the primary competitive alternative, operates as a marketplace connecting third-party sellers — it lacks Coupang’s first-party inventory and logistics control. AliExpress Korea and other C-commerce platforms offer lower prices but longer delivery windows, serving a different price-sensitivity segment.

The WOW membership — Coupang’s equivalent of Amazon Prime — is the strategic flywheel that locks in the logistics investment’s return. For approximately $8–10 per month, WOW members receive unlimited free Rocket Delivery, free returns, access to Coupang Play (its streaming service), and discounts on Coupang Eats. The membership fee covers a portion of logistics cost while increasing the frequency with which members shop on Coupang rather than alternatives. Members order significantly more frequently than non-members and have dramatically higher retention rates. Every WOW member is both a revenue stream and a demand guarantee for the logistics network.

04 — Farfetch: From Acquisition Disaster to First Positive Economics

The Unlikely Turnaround That Changed the Q1 2026 Narrative

When Coupang acquired Farfetch out of financial distress in late 2023 for approximately $500 million — a fraction of the $5.8 billion valuation Farfetch commanded at its IPO peak — the transaction was widely viewed as opportunistic at best and reckless at worst. Farfetch was a luxury fashion marketplace that had never been profitable, burned cash at a prodigious rate, and operated in a market — high-end fashion e-commerce — that seemed antithetical to Coupang’s utilitarian, next-morning delivery value proposition.

Q1 2026 delivered the first concrete evidence that Coupang’s turnaround thesis has merit. Farfetch generated positive year-over-year revenue growth and, more importantly, positive overall economics for the first time since its acquisition. This is a milestone that many analysts had projected would take another 18 months to reach. While the specific financial contribution remains modest, the directional change — from cash-consuming liability to nascent contributor — materially changes the narrative around Coupang’s portfolio of non-core businesses.

The Farfetch turnaround strategy rested on cost rationalization rather than revenue acceleration. Coupang reduced Farfetch’s operational complexity, consolidated its technology infrastructure onto Coupang’s existing logistics and payments backbone where practical, and focused the business on its highest-margin brands and geographies. The luxury customer segment Farfetch serves — high-net-worth consumers in Europe, the Middle East, and Asia who buy $500+ fashion items online — does not require the same logistics density as Korean next-morning delivery. The unit economics of luxury fashion e-commerce, when stripped of the growth-at-all-costs overhead that characterized Farfetch pre-acquisition, are workable.

◎ Why Farfetch Matters More Than Its Revenue Contribution

Farfetch’s first positive economics quarter is important not because it generates meaningful Adjusted EBITDA — it almost certainly does not yet. It matters because it removes the largest explicit liability in Coupang’s developing offerings portfolio. Prior to this quarter, Farfetch was a guaranteed drag: every analyst model included an ongoing Farfetch loss that had to be overcome by growth elsewhere. If Farfetch is now self-sustaining or better, the developing offerings segment’s path to profitability is primarily a Taiwan and Japan scale question — both of which have clearer playbooks based on Coupang’s Korean success — rather than a Farfetch survival question.

Separately, Farfetch validates Coupang’s claim that it can acquire distressed e-commerce businesses, rationalize their cost structures using Coupang’s operational discipline, and convert them from cash-burning liabilities to contributors. If this playbook works, it is a template for future acquisitions in markets where Coupang wants to enter without building logistics infrastructure from scratch.

05 — International Expansion: Taiwan, Japan, and the Long Game

Replicating the Korean Playbook in New Markets — With Saudi Arabia’s Timeline, Not Korea’s

Coupang International Expansion Map — 2024 Through 2028

Market maturity stages across the developing offerings footprint

Early Scale — 2023–Now

Taiwan

Strong above-plan growth. Rocket Delivery replicated using Taiwan’s dense urban geography. $10B annual revenue target by 2030. Already 2+ years into network buildout; becoming the first international proof point.

Early Launch — 2024–Now

Japan

Market entry ongoing. Largest e-commerce market in Asia outside China. Amazon JP dominates but same-day grocery is underpenetrated. Coupang targets urban corridors first. Investment phase: losses guaranteed for 2–3 years minimum.

Scoped — 2025 Onward

Southeast Asia

Vietnam, Indonesia, Philippines flagged as 2030 targets. $20B combined revenue target ambitious. C-commerce (Shopee, Lazada) entrenched. Requires local logistics partnership or significant capital investment.

Turnaround — Ongoing

Farfetch (Global)

First positive economics in Q1 2026. Luxury fashion e-commerce in Europe, Middle East, Asia. Cost rationalization complete. Revenue growth resumed. No longer a guaranteed drag on segment.

Taiwan is the international market that matters most right now. Coupang began building its Taiwanese logistics network in 2023, importing the Rocket Delivery playbook into a geography with favorable characteristics: dense urban population, high smartphone penetration, strong e-commerce adoption, and relatively underpenetrated next-day delivery. The results have been strong and above Coupang’s internal plan — management has highlighted Taiwan in multiple consecutive earnings calls as a market where customer adoption and order frequency are tracking ahead of the equivalent metrics from Korea’s early growth period.

The Japan expansion is at an earlier and more expensive phase. Japan is the world’s third-largest e-commerce market and the most logistics-sophisticated market in Asia — consumers already expect reliable next-day delivery from Amazon JP, Rakuten, and domestic players. Competing there requires matching an already-high standard before attempting to exceed it. Coupang’s Japan losses in Q1 2026 are investment-phase losses, not evidence of a failing market entry. The question is whether the Korean playbook — first-party inventory, owned logistics, WOW membership flywheel — can create sustainable differentiation against Amazon JP’s own Prime infrastructure. That answer will take several years and several billion dollars of patient capital to determine.

06 — Coupang Eats and the Food Delivery Wars