Dell Technologies: The $43.8B Quarter, AI Server Supercycle, and the Architecture of a New Machine

Revenue nearly doubled in a single year. AI server bookings hit $24.4 billion in one quarter alone. The guidance for a $167 billion fiscal year with $60 billion from AI servers

Section 01

The Verdict: AI Infrastructure’s Indispensable Integrator

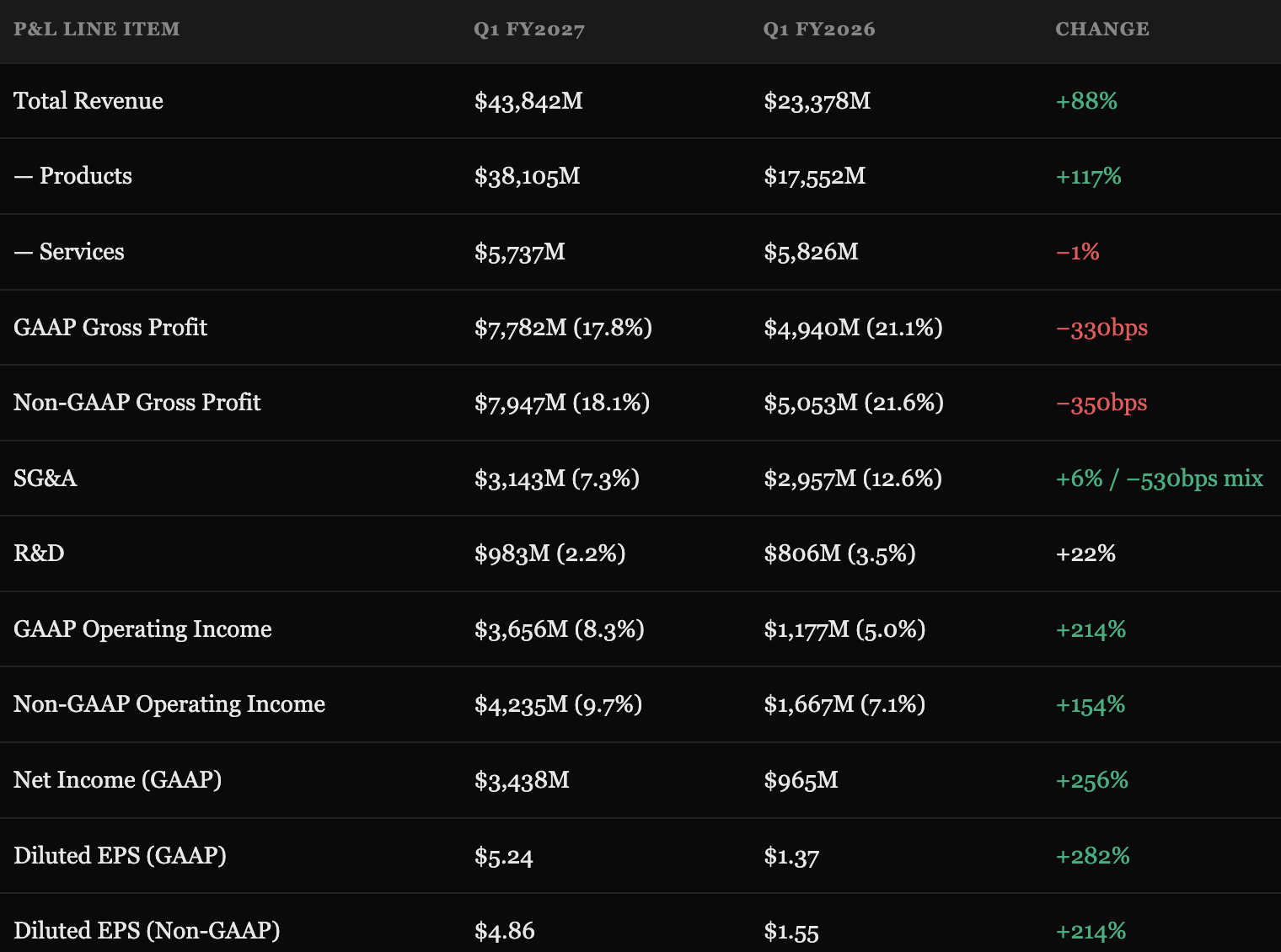

Dell Technologies reported its fiscal first quarter of 2027 on May 28, 2026 — a quarter that, by almost any prior standard of what a $100 billion enterprise hardware company could accomplish, should not have happened. Revenue came in at $43,842 million, an 88% increase over the prior year’s $23,378 million, with infrastructure products nearly tripling and AI server revenue alone expanding by 757%. The non-GAAP diluted EPS of $4.86 beat consensus estimates of $2.93 by 66%, a gap that reflects not analyst incompetence but the sheer pace at which AI-driven demand has outrun every projection made even twelve months ago. The company booked $24.4 billion in new AI orders in the quarter, then guided the full fiscal year to $167 billion in revenue at the midpoint — a figure that would have been Dell’s entire two-year revenue stack as recently as fiscal 2024.

The story here is not complicated: hyperscalers, sovereign AI funds, and enterprise customers are racing to build AI infrastructure, and Dell — with its ability to integrate NVIDIA GPU clusters, custom liquid-cooling systems, high-speed networking, and storage into fully configured, ready-to-deploy racks — has become the default assembly line for the AI era. Its Infrastructure Solutions Group (ISG) is not merely growing; it is redefining what the business is. ISG contributed $29.0 billion of the $43.8 billion total, and AI servers alone contributed $16.1 billion of that — a single product line that is approaching the size of Dell’s entire company just two years ago.

The Verdict in a SentenceDell is no longer a PC and server company that is trying to catch the AI wave — it is the AI wave’s hardware assembly floor, and the backlog suggests this will be true for years.

The complexity in the story — and there always is complexity — lies in the margin architecture. AI servers are, by design, thin-margin assembly operations. Dell sources the GPUs (mostly from NVIDIA), integrates them into rack-scale systems, handles the thermal and networking architecture, and delivers a configured system to the customer. The hardware integration is valuable and proprietary, but it is not a software business. Gross margins fell from 21.1% to 17.8% as AI server revenue overwhelmed the mix. The company more than compensated through SG&A leverage — selling and general administrative costs grew just 6% against an 88% revenue increase — so operating income expanded dramatically. But investors focused on absolute gross margin percentages will find the direction uncomfortable, even if the dollar trajectory is undeniably strong.

Section 02

The Numbers: An Income Statement Transformed

The headline growth rate of 88% is extraordinary for a company of Dell’s scale, but the composition of that growth is even more telling. Products revenue — hardware — grew 117% to $38,105 million. Services revenue, which includes support, deployment, and managed services, actually declined 1% to $5,737 million, a rounding-table concern that the company attributes to the shift in mix toward new AI system deployments that carry shorter near-term service attachment rates. The services base will rebuild as the installed fleet of AI infrastructure ages and requires support contracts, but for now the services line is a modest drag in a quarter that doesn’t need the help.

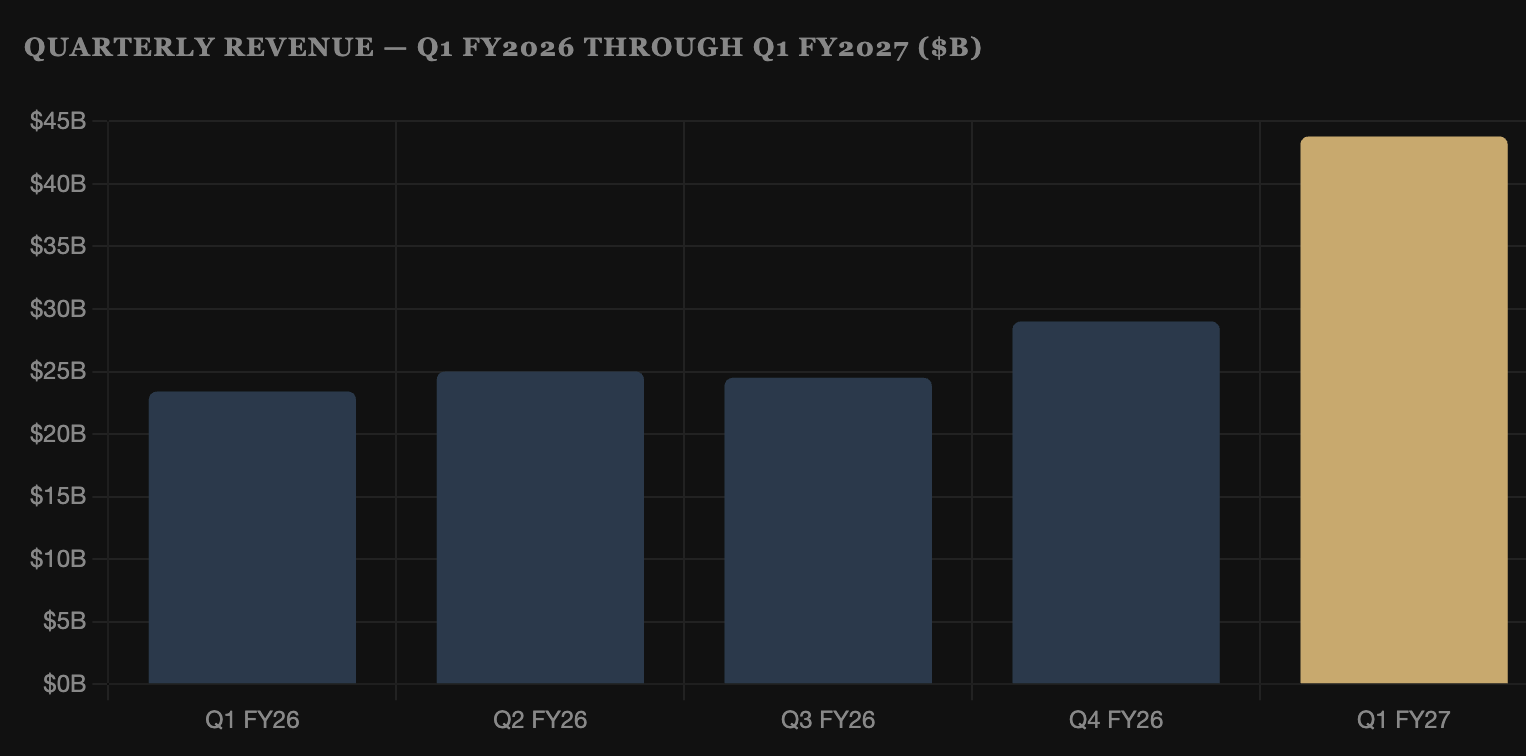

Looking at the five-quarter revenue trend reveals the shape of the inflection clearly. Dell posted $23.4 billion in Q1 FY2026, then moved sideways through Q2 and Q3 — $25.0 billion and $24.5 billion respectively — before beginning a steeper ascent in Q4 FY2026 at $29.0 billion as AI server ramp accelerated. The jump to $43.8 billion in Q1 FY2027 is not a continuation of a trend; it is the arrival of a new demand regime.

The non-GAAP diluted EPS of $4.86 versus the consensus of $2.93 represents one of the largest percentage beats in Dell’s modern history. Consensus forecasters had been anchoring to the company’s prior trajectory; the AI server ramp came in faster and larger than the sell-side had modeled. The GAAP diluted EPS of $5.24 actually exceeded the non-GAAP figure — an unusual inversion that reflects favorable tax and below-the-line items in the quarter.

“We booked $24.4 billion in AI orders in a single quarter. We are not catching up to demand — demand is building faster than we can deploy.”

— Paraphrase of management commentary, Q1 FY2027 earnings call, May 28, 2026

Section 03

Segment Breakdown: ISG Rewrites the Company’s Identity

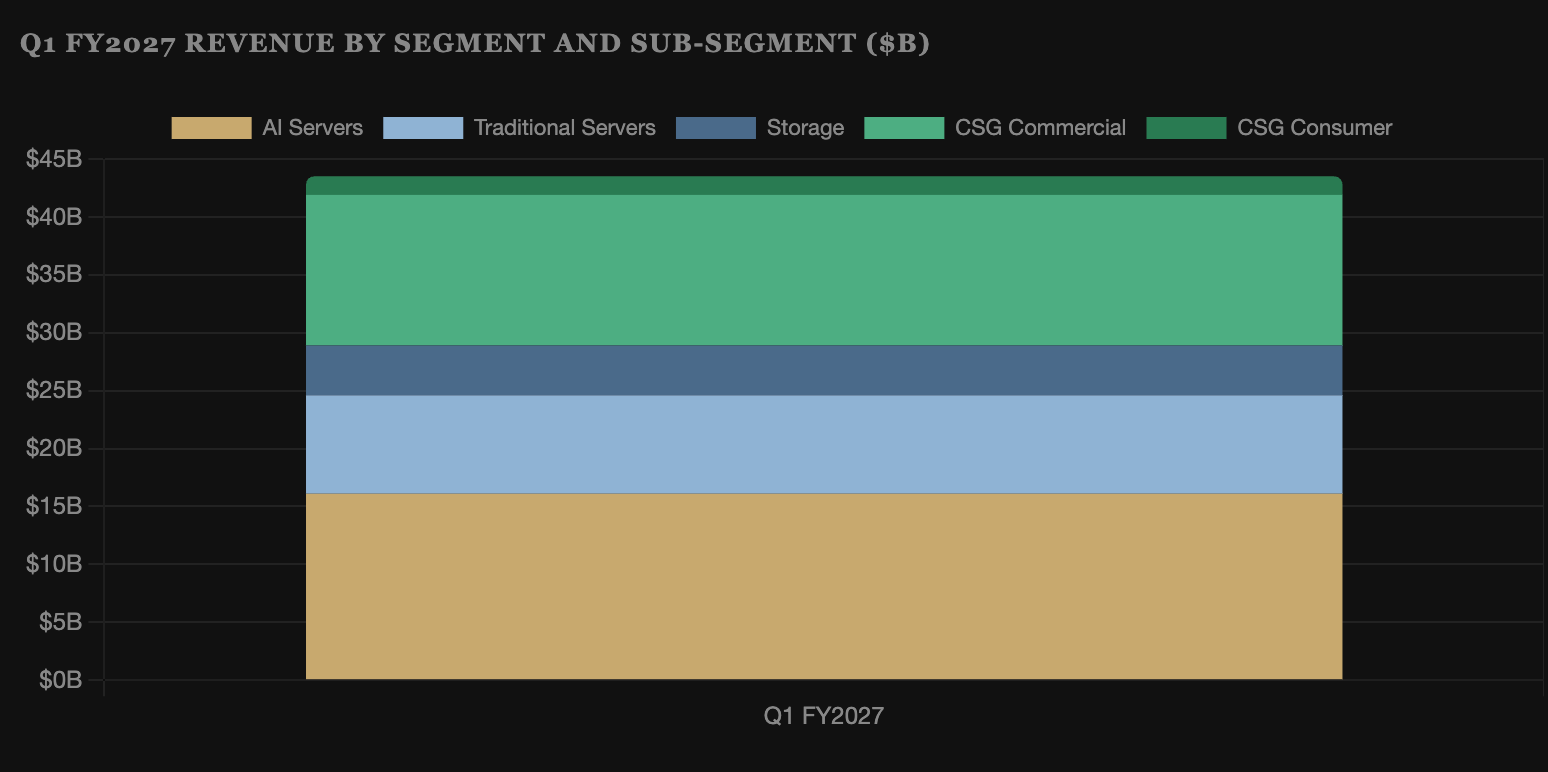

Dell reports in two segments: Infrastructure Solutions Group (ISG) and Client Solutions Group (CSG). Historically, CSG — the PC and commercial laptop business — was the revenue anchor, providing steady cash generation that funded Dell’s technology and services ambitions. That dynamic has been fully inverted. ISG now generates $29.0 billion of quarterly revenue, or 66% of the company’s total, against CSG’s $14.6 billion, a reversal from the prior year when CSG held a narrow majority of revenue.

Within ISG, the further decomposition is revelatory. AI servers — PowerEdge systems configured with NVIDIA H100, H200, and Blackwell GPU clusters, alongside the networking and thermal systems necessary to operate them — generated $16,132 million in the quarter, up 757% from $1,882 million in Q1 FY2026. Traditional servers (non-AI compute) contributed $8,543 million, itself up 92%, as the broader server refresh cycle and enterprise data center modernization continued. Storage added $4,334 million, growing a more modest 8% — a healthy number for a mature business that gets less attention in a quarter dominated by explosive AI figures.

CSG’s performance deserves more credit than the headline might suggest. A 17% increase in PC and commercial laptop revenue — reaching $14.6 billion in a single quarter — is a genuinely strong result. Commercial PCs grew 18%, driven by enterprise refresh cycles as AI-capable PC hardware (Copilot+ and NPU-enabled systems) creates incremental demand beyond simple replacement. Consumer PCs grew 9%, a slower but positive trajectory. The CSG operating margin of 8.0% represents healthy profitability for a hardware distribution business, and the segment continues to generate meaningful absolute operating income: $1,170 million in the quarter.

ISG’s operating margin of 10.5% — $3,055 million on $29.0 billion of revenue — is the central tension in the Dell story. That is a very thin margin for what appears to be explosive growth. The answer lies in the margin architecture of AI server assembly, which is discussed in full in Section 05.

Section 04

The AI Infrastructure Thesis: $60 Billion Is a Floor, Not a Ceiling