Disney: Three Engines, One Reckoning

Streaming finally crosses 10% margins. Parks break records on lower attendance. ESPN faces an existential pivot. And a new CEO inherits all of it on day one.

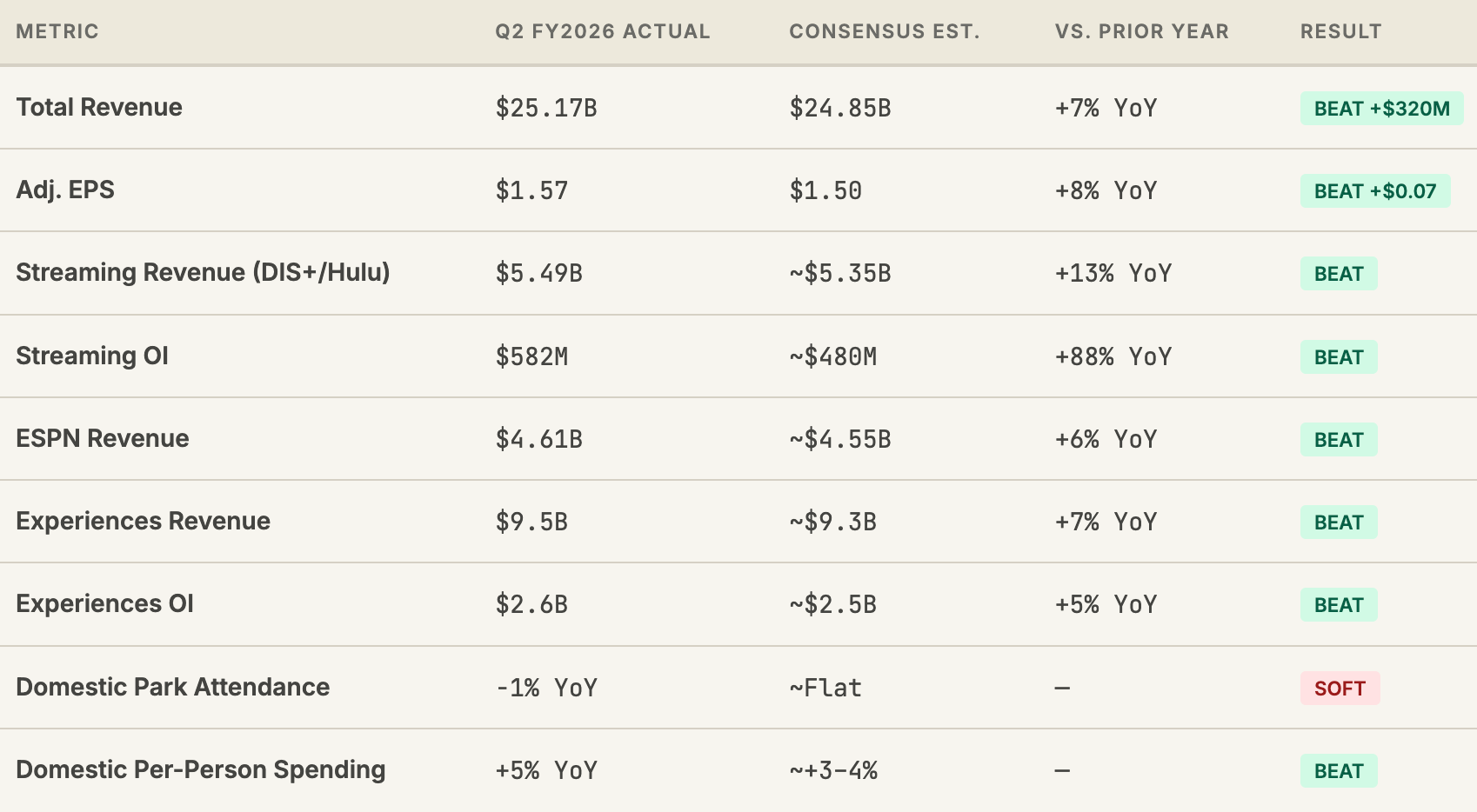

Disney’s Q2 FY2026 results, delivered on May 6 as Josh D’Amaro’s first earnings report as CEO, tell a story that Bob Iger spent five years trying to engineer: a company where streaming is genuinely profitable, parks are generating record operating income, and the foundation for a decade of growth is in place. The headline numbers are clean — revenue $25.2B (+7%), adj. EPS $1.57 (+8%), both above consensus. But the details reveal a more nuanced picture: domestic park attendance actually fell 1% while parks operating income hit a record, streaming crossed 10% operating margin for the first time in its history, and ESPN is navigating a structural transition that still lacks a clear resolution. Disney is executing. The question is whether the execution is fast enough to stay ahead of secular forces that are moving against two of its three core businesses — linear television and traditional park economics — simultaneously.

01 — The D’Amaro Transition

A Parks Man Inherits a Media Empire

When Josh D’Amaro took the stage at Disney’s annual shareholder meeting on March 18, 2026, he became the first CEO in Disney history to ascend from the Parks division rather than from media or entertainment. That matters more than it sounds. Every strategic bet D’Amaro has articulated since his appointment — the $60 billion global parks investment, the emphasis on Disney’s direct consumer relationships, the “category of one” language about Disney’s franchise breadth — reflects the perspective of someone who built his career watching guests pay three-figure daily ticket prices to immerse themselves in IP that Disney already owned. His operating model is not primarily about content creation or distribution economics. It is about converting IP into experiences, and experiences into loyalty, and loyalty into repeat revenue that compounds without the episodic uncertainty of the box office.

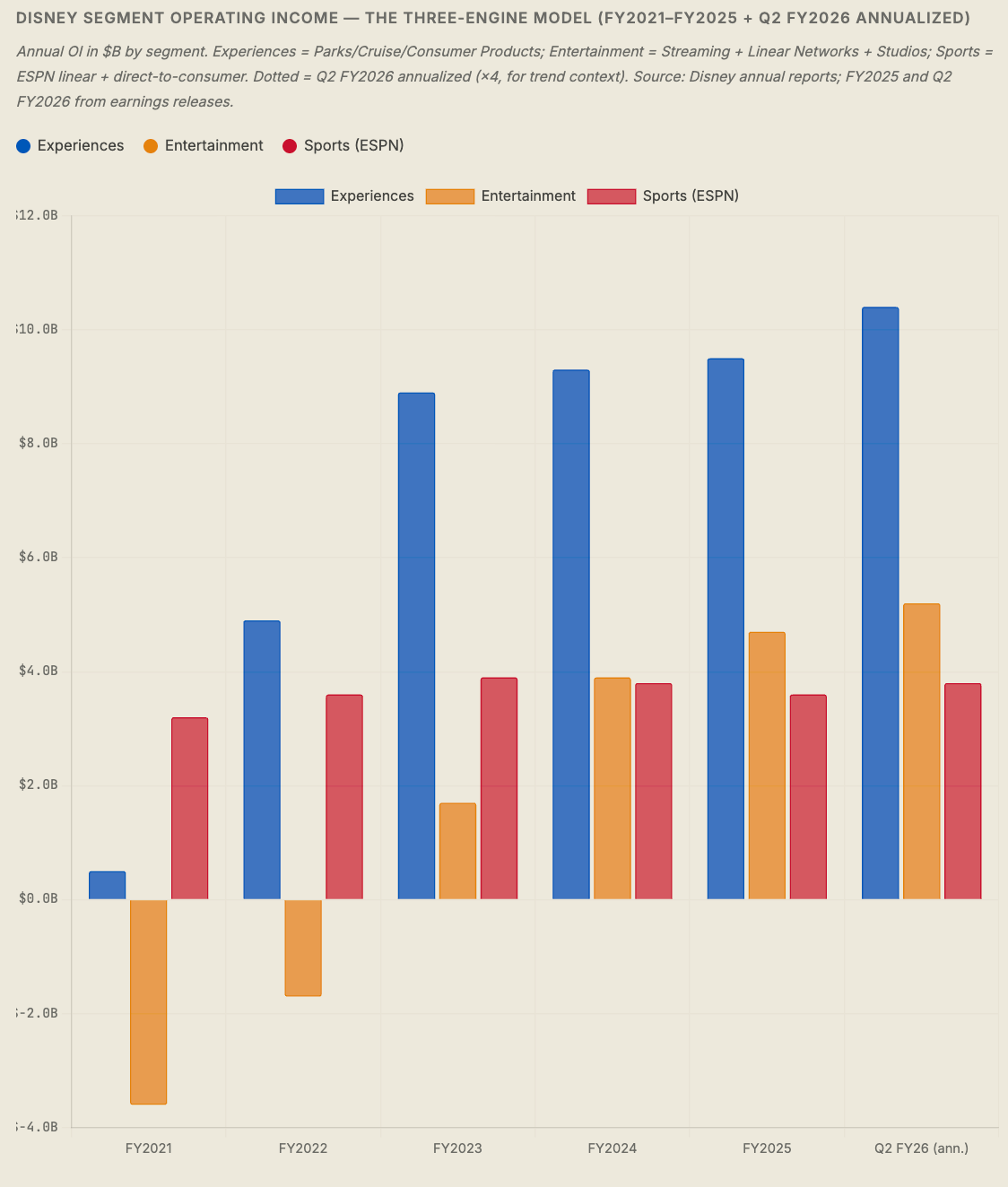

This is both Disney’s greatest structural strength and the source of its most interesting strategic question. D’Amaro inherits a company that has successfully completed Iger’s streaming transformation — Disney+ reached operating profitability ahead of most analyst timelines, and the entertainment segment’s operating income has grown from a $1.7B deficit in FY2022 to a $4.7B positive in FY2025. But he also inherits ESPN, a sports media asset that is simultaneously the most valuable piece of the company and the one facing the most fundamental disruption. And he inherits a parks business that, despite record financial performance, is showing early signs of demand softness — domestic attendance fell 1% in Q2 — that will need to be addressed with product innovation rather than pure price increases.

D’Amaro has laid out three strategic pillars: investing in IP that breaks through and endures; reaching consumers in more seamless ways across streaming, sports, gaming, and experiences; and leveraging technology — including AI — to create more personalized, efficient, and scalable Disney interactions. All three pillars converge on the same thesis: Disney’s competitive moat is the depth of its emotional relationship with audiences, and the company’s job is to monetize that relationship across more surfaces, more frequently, and at higher margin than any competitor can replicate.

02 — Q2 FY2026 Results

A Clean Beat — With Important Asterisks

Disney’s Q2 FY2026 results were broadly strong. Revenue of $25.17 billion came in above the $24.85 billion consensus estimate, and adjusted earnings per share of $1.57 beat the $1.50 estimate. The full-year EPS growth guidance of approximately 12% was maintained, and the company raised its share repurchase target from $7 billion to $8 billion for fiscal 2026 — a signal of management confidence and financial flexibility that the market rewarded with a 7% stock jump on the day.

The important asterisks are in the details. Streaming’s 88% operating income growth is genuinely impressive, but it was partially driven by fall 2025 price hikes whose full-year lap effect will moderate the growth rate in coming quarters. Parks’ record operating income came alongside a 1% decline in domestic attendance and management attribution of weakness to “softness in international visitation” — a carefully chosen phrase that threads the needle between acknowledging macroeconomic headwinds (dollar strength, tariff uncertainty affecting international travel) and avoiding any suggestion that domestic demand itself is softening. ESPN grew revenue 6% with digital subscribers offsetting linear declines, but the long-term transition math remains unresolved.

03 — Streaming

The Margin Inflection — Real, Durable, and Still Early

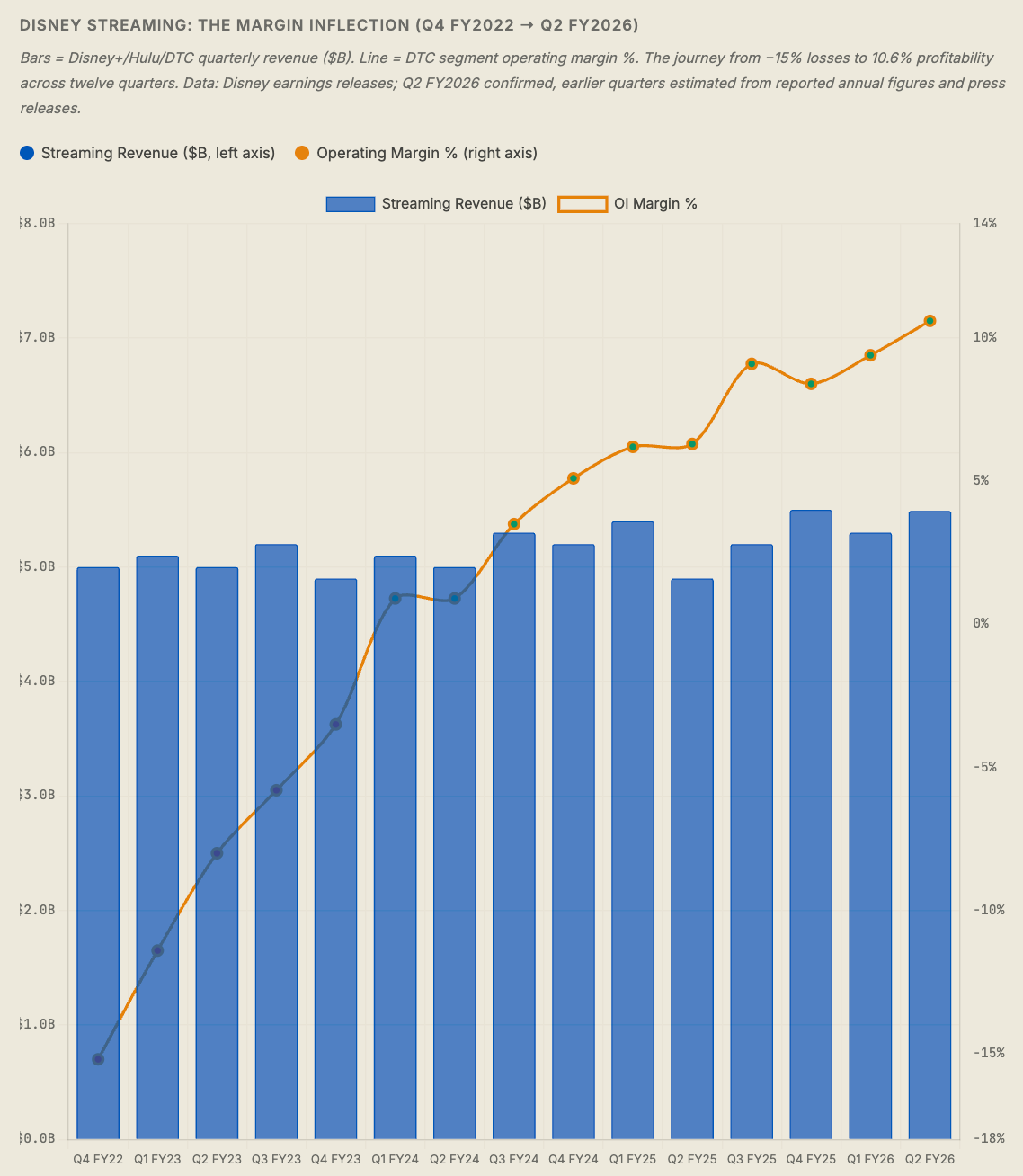

The most important number in Disney’s Q2 FY2026 report is not the headline revenue or EPS. It is the 10.6% operating margin in the streaming segment — the first time Disney’s direct-to-consumer entertainment business has crossed double digits since it launched Disney+ in November 2019. The journey from the -$3.8 billion operating loss that Disney’s streaming segment posted in FY2022 to $582 million in operating income in a single quarter is one of the most significant operational pivots in modern media history.

Three distinct forces drove the inflection. First, price discipline: Disney has executed five meaningful price increases across Disney+ and Hulu since 2022, with the most recent set of hikes in fall 2025 contributing significantly to the revenue-per-subscriber improvement that shows up in the +13% streaming revenue growth despite the company’s decision to stop reporting subscriber counts. Second, content cost rationalization: the post-Iger content spend reduction — which saw Disney cut hundreds of millions from its streaming content budget through 2024 — reduced the margin drag from content amortization without materially impairing the quality signal that drives subscriber retention. Third, advertising tier penetration: the Disney+ ad-supported tier, which launched in 2022, now represents a meaningful and growing share of the subscriber base, and the advertising revenue it generates carries incremental margin well above the subscription-only baseline.

The sustainability question matters here. The fall 2025 price hikes created a revenue tailwind in Q2 FY2026 that will anniversary in Q3 FY2026, moderating the growth rate. Subscriber growth, absent the quarterly reporting, is opaque — the company’s stated rationale is that engagement metrics are more meaningful than raw counts, but the practical effect is that investors cannot independently track whether churn is elevated. What is observable: the revenue trajectory is up, the margin trajectory is up, and Disney’s guidance of 12% full-year EPS growth implies the streaming segment is expected to remain solidly profitable through the back half of fiscal 2026 and beyond.

04 — Parks & Experiences

Record Numbers on a Softening Foundation

Disney Experiences — the umbrella segment covering theme parks, cruise lines, and consumer products — posted Q2 FY2026 record revenue of $9.5 billion (up 7%) and record operating income of $2.6 billion (up 5%). Both figures are the highest ever recorded for a fiscal second quarter. The parks business, which D’Amaro built his career within, is performing at the absolute peak of its historical financial trajectory. And yet the underlying attendance data tells a story that deserves careful attention.

Domestic park attendance fell 1% year-over-year in Q2 FY2026, with management attributing the decline primarily to softness in international visitation. International visitors — particularly from Latin America and Europe — are a disproportionately high-spending cohort at Disney’s U.S. parks, and the combination of a stronger dollar, tariff-related economic uncertainty, and some consumer pullback on discretionary long-haul travel appears to have reduced that inbound flow. Importantly, per-person spending at domestic parks rose 5% — meaning Disney is earning more per guest even as it admits fewer of them. That is the explicit operating strategy: optimize for revenue and margin per visit rather than pure attendance volume.

The strategy works until it doesn’t. Disney has raised ticket prices, food prices, hotel rates, and the cost of “premium” add-ons (Genie+, Lightning Lane, early park entry) steadily since the post-COVID reopening. At some point, the price ceiling for the core middle-class family that has historically been Disney’s park customer will be reached — and when attendance softness shifts from “international headwind” to “value perception problem,” the pricing lever becomes much harder to pull. The $60 billion capital investment plan is, in part, a bet that adding new product (new lands, new rides, new cruise ships, new park locations) will attract enough new visitors at maintained price levels to prevent that ceiling from becoming a structural constraint.

05 — ESPN

The Most Valuable Asset With the Hardest Future

ESPN is simultaneously the most valuable franchise in Disney’s portfolio and the one that keeps executives up at night. In Q2 FY2026, ESPN revenue grew 6% to $4.61 billion — a solid result driven by the direct-to-consumer app that launched in August 2025. The company said ESPN digital subscriber revenue “more than offset” secular declines in the linear subscriber universe. That is progress. But “more than offset” is not the same as “solved.”