Duolingo: The Owl That Chose Users Over Revenue

Revenue up 27%, stock down 80% from peak. Duolingo is deliberately slowing monetization to chase 100 million daily learners

Executive Summary

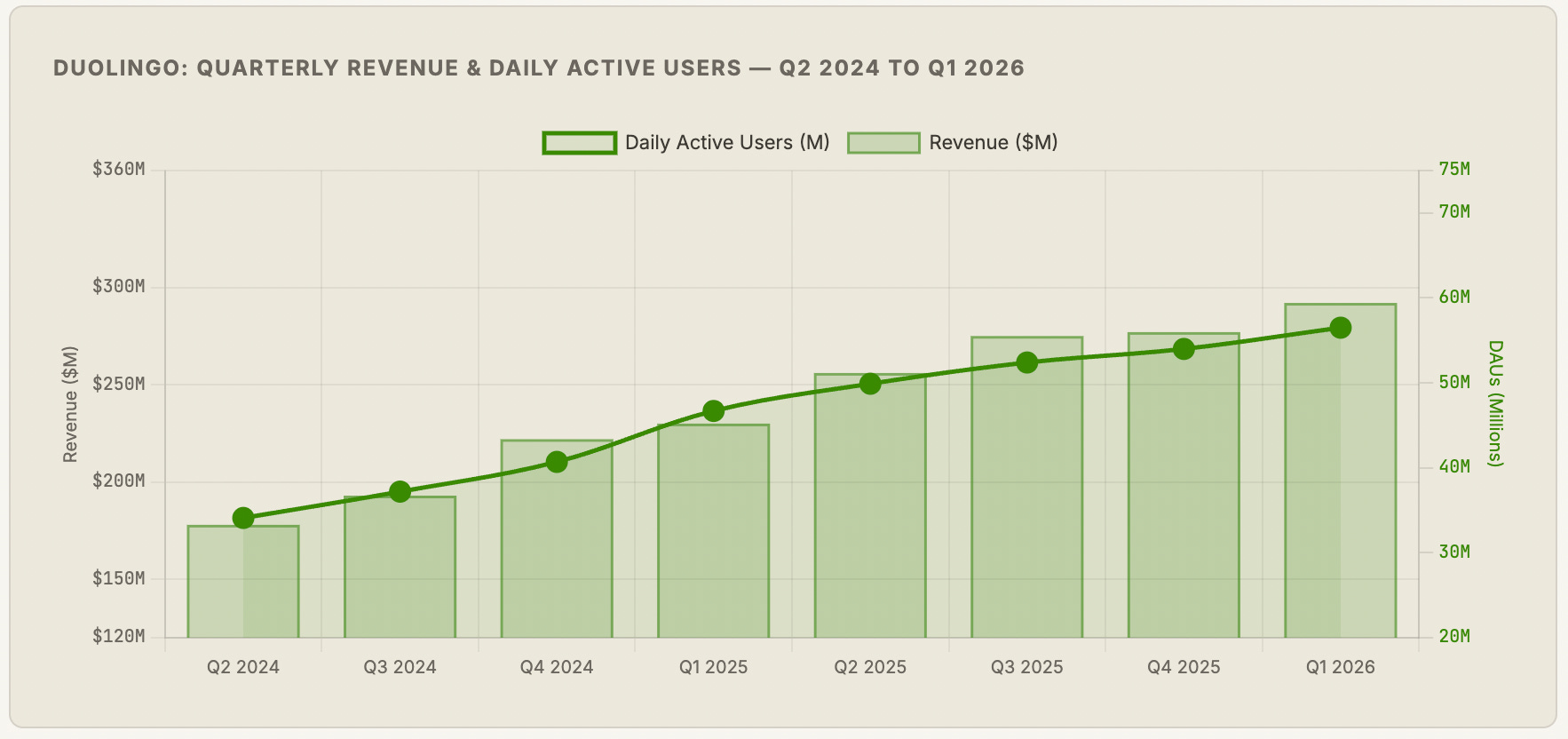

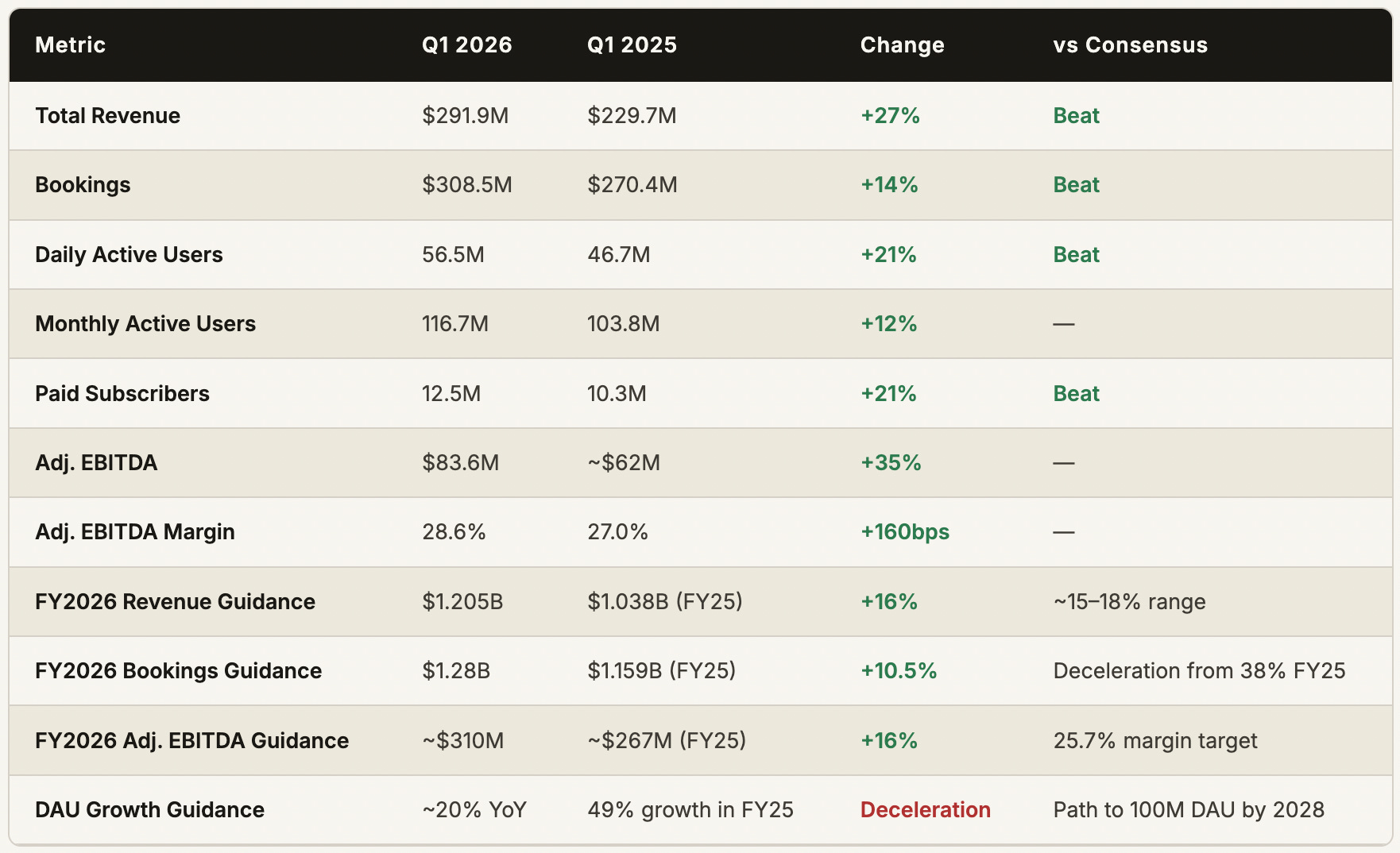

Duolingo reported Q1 2026 revenue of $291.9 million — up 27% year-on-year — with 56.5 million daily active users (+21%), 12.5 million paid subscribers (+21%), and an adjusted EBITDA margin of 28.6%. On every traditional growth metric the company beat estimates. Yet the stock remains down roughly 80% from its $545 all-time high, reflecting not operational failure but a deliberate strategic pivot that the market is still digesting: Duolingo has chosen to grow users faster by reducing monetization pressure. The company moved advanced AI features down from its premium Max tier to the lower Super tier and the free tier, made the product less aggressive about prompting conversions, and guided full-year 2026 revenue growth at 15–18% — roughly half the 38% growth rate of fiscal 2025. CEO Luis von Ahn’s argument is straightforward: the path to a durable business is a 100 million daily active user base, not maximum extraction from 56 million. Get to 100 million, and the monetization opportunity becomes an order of magnitude larger. The bears counter that Duolingo is voluntarily giving up revenue in a macro environment that punishes growth deceleration, that the existential threat of real-time AI translation tools has not been adequately answered, and that the new subjects — math, music, chess — have not yet proven they can scale the way language did. The resolution of that debate is the most interesting investment question in consumer technology in 2026.

01 / BACKGROUND

From CAPTCHA to the World’s Largest Language Classroom

Luis von Ahn is one of the more unusual CEOs in technology. A Guatemalan-born computer scientist who co-invented CAPTCHA at Carnegie Mellon — the wavy-letter tests that proved you were human — he later co-invented reCAPTCHA, the system that simultaneously stopped bots and helped digitize books by having millions of people unknowingly type words from scanned texts. In 2011, he co-founded Duolingo with the explicit mission of making education free and accessible to everyone on earth. The first product was a language learning app built around gamification, streaks, and a cartoonish green owl named Duo who sends users passive-aggressive notifications when they skip practice. It was immediately beloved.

By 2026, Duolingo is the most downloaded education app in the history of the App Store, the top-grossing app in the Education category on both iOS and Android, and the platform through which more people are actively learning a foreign language than through any other means — including traditional schools, Rosetta Stone, Babbel, and every university language department combined. The scale is not subtle: 56.5 million people open the app every single day. More than 500 million registered users have tried it. In terms of daily active engagement for a voluntary educational product, there is nothing remotely comparable in existence.

The business model that Duolingo built on top of that engagement is a classic freemium architecture: the app is free and genuinely useful in its free form, ad-supported for users who tolerate interruptions, and subscription-accessible for users who want an ad-free experience and access to premium features. The subscription tiers — Super Duolingo (ad-free, offline access, unlimited hearts) and Duolingo Max (AI-powered conversation practice, personalized feedback) — convert roughly 10% of monthly active users to paid. That conversion rate, modest on a percentage basis, creates a $1.2 billion annual revenue business when applied to hundreds of millions of users. The funnel is: get as many people as possible using the app daily → convert the segment willing to pay → charge enough per subscriber to fund the product development that makes the free tier more compelling for the next cohort.

For five years, this machine ran in high gear: DAUs doubled from 2021 to 2025, revenue compounded at 40%+ per year, and the stock reached $545 per share as investors priced in a company that could be the dominant consumer learning platform for a generation. Then two things happened simultaneously: large language models made AI-powered language tutoring a commodity that any tech company could offer, and Duolingo made the deliberate choice to decelerate monetization in pursuit of scale. The stock lost 46% in 2025 and another 45%+ in 2026. The question now is whether that repricing is rational or whether it has overcorrected.

02 / FINANCIALS

Q1 2026: Still Growing Fast, But Not Fast Enough for the Prior Multiple

The Q1 2026 numbers are genuinely strong in absolute terms. Revenue of $291.9 million grew 27% year-on-year. Paid subscribers reached 12.5 million — up 21% — with monthly active users at 116.7 million (+12%). Daily active users hit 56.5 million, the highest in the company’s history, growing 21% year-on-year. Bookings of $308.5 million grew 14%. Adjusted EBITDA of $83.6 million at a 28.6% margin is healthy for a growth company of this scale. All of these beat estimates.

The stock fell after earnings. Not dramatically — about 6% in after-hours — but the direction underscores the challenge Duolingo faces in a market where “beat and raise” is the only acceptable outcome for a high-multiple growth name. Instead of raising guidance, Duolingo maintained it. Instead of accelerating bookings growth, the company reiterated that 2026 is a year of deliberate investment in user growth at the expense of near-term monetization. The market, which priced the stock at over 30x revenue at its peak, is now trying to figure out what the right multiple is for a company growing revenue at 16% instead of 40%. That repricing process has been brutal — and it is probably not complete.

The gap between revenue growth (27%) and bookings growth (14%) is the strategic pivot made visible. Bookings represent future revenue — cash collected today for subscriptions that will be recognized over coming months. Slower bookings growth than revenue growth means the pipeline of deferred revenue is building less rapidly, which signals slower future revenue recognition. Put simply: Duolingo is growing its current revenues well but building the future revenue pipeline more slowly, because it is deprioritizing subscriber acquisition in favor of DAU scale. That is a choice. Whether it is the right choice is the debate.

03 / THE STRATEGIC PIVOT

Trading Short-Term Revenue for 100 Million Daily Learners

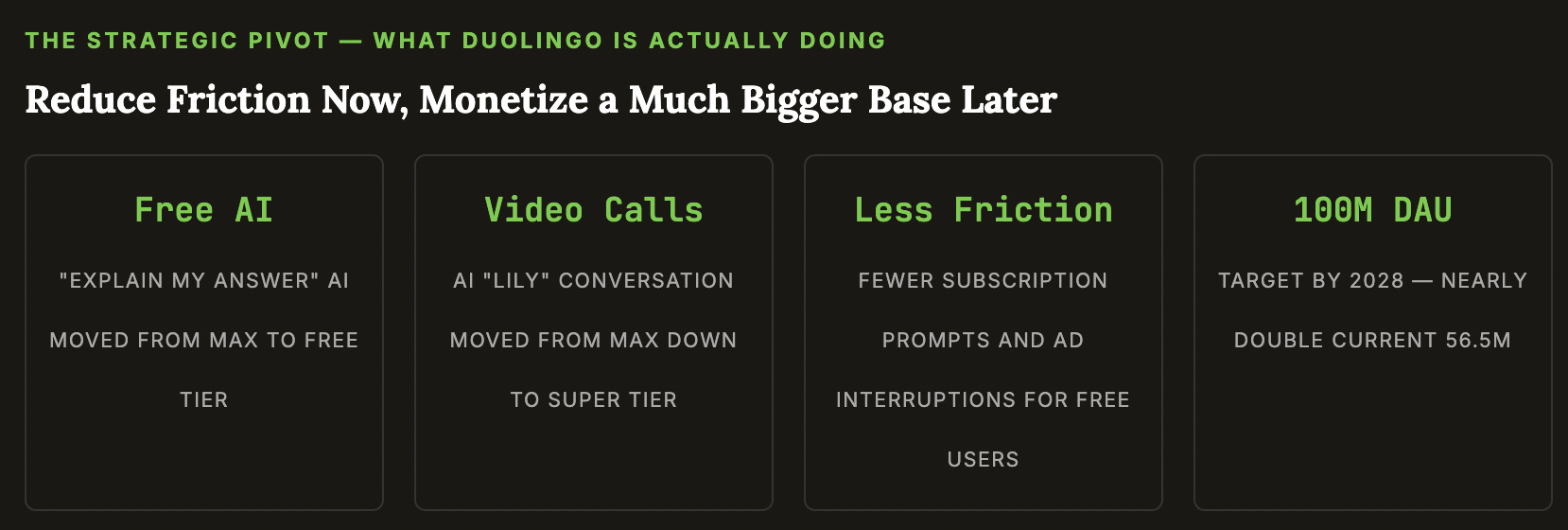

Von Ahn’s strategic logic is worth understanding carefully, because it is more sophisticated than the surface-level narrative of “sacrificing revenue for growth.” The core insight is about the difference between a monetizable user base and a truly dominant platform. At 56 million DAUs, Duolingo is large by almost any standard. At 100 million DAUs, it becomes something categorically different: the default place that human beings go to learn, full stop. The network effects compound, the brand association deepens, the data advantages for AI training widen, and the monetization opportunities — premium subscriptions, institutional licensing, new subject expansion, potential advertising at greater scale — all expand in ways that are not linear with the additional users.

The specific actions Duolingo has taken to reduce friction are instructive. Moving the “Explain My Answer” AI feature — which gives learners a detailed explanation of why their answer was correct or incorrect — from the $168-per-year Max tier to the free tier is a deliberate sacrifice of premium conversion in favor of engagement. Every free user who now benefits from this feature has less reason to pay for Max, but also has more reason to keep opening the app. The net effect in the short term is lower average revenue per user. The net effect over 18–24 months — the theory goes — is a larger active user base with a higher percentage of deeply engaged daily learners who eventually convert at some tier.

The precedent for this kind of deliberate friction reduction in pursuit of scale is mixed but not discouraging. Spotify went through a similar period where it expanded the free tier’s quality to maximize listening hours before tightening the conversion funnel. Netflix has oscillated between generous and restrictive free-trial policies based on where it is in its growth cycle. The common thread in cases where this strategy worked: the product is genuinely so good in its free form that users become habituated before they face the paywall, and the paywall is then accepted because the habit is already formed. Duolingo’s streak mechanic — the daily reminder that you are on a 47-day streak and really shouldn’t break it tonight — may be the most powerful consumer habit formation tool in consumer software. Making the free product better makes the streak more valuable, which makes the user more engaged, which ultimately makes the conversion to paid more likely even if the immediate conversion pressure has been removed.

The risk is that this logic assumes a level of patience from both investors and from the competitive dynamics that may not materialize. If AI translation tools erode the motivation to learn languages faster than Duolingo builds its 100M DAU base, the entire monetization opportunity shrinks before the base reaches the scale where it becomes defensible. The clock on this strategy is not infinite.

04 / PRODUCT ARCHITECTURE

Languages, AI, Math, Music, and the World’s Fastest-Growing Chess Platform

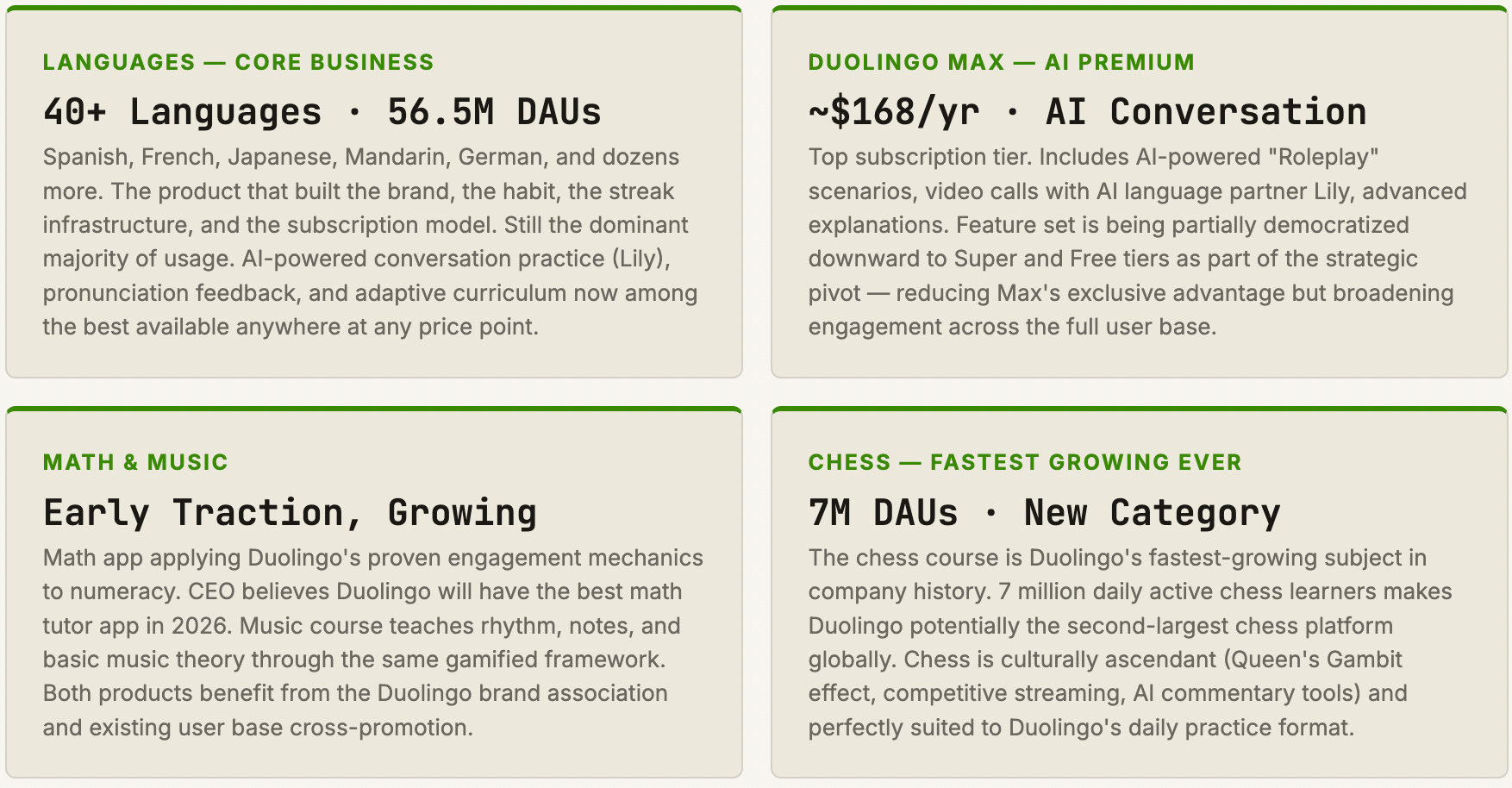

Most people think of Duolingo as a language app. Von Ahn thinks of it as the infrastructure for all learning that benefits from daily practice, gamification, and adaptive feedback. The distinction matters enormously for the long-term total addressable market. The language learning market — however you define it — is finite. The market for any learning that can be delivered in the Duolingo format is essentially unbounded.

Chess is the most interesting new subject both as a data point and as a thesis validator. Chess was not an obvious Duolingo category — it is not a language, not a traditional academic subject, and not typically associated with mobile app learning. But it has exactly the properties Duolingo’s product excels at delivering: it rewards daily practice, has clear progressive difficulty, benefits from immediate feedback (”that move loses a bishop”), and has an intrinsic motivation loop (the desire to beat better opponents). The fact that 7 million people are doing chess on Duolingo every day — a number large enough to make Duolingo a major chess platform in its own right — validates von Ahn’s “learning platform” thesis. If chess works, the question becomes: what other skill-based domains benefit from the same delivery mechanism? Coding? Mental math? Music theory? Historical knowledge? The answer is potentially most of them.

Math is the most strategically important new subject for long-term revenue, because the math learning market is substantially larger than the language learning market. There are approximately one billion people learning mathematics in the world at any given time — students in primary and secondary education, adults trying to improve quantitative skills for professional reasons, and lifelong learners. If Duolingo can deliver even a portion of that instruction as effectively as it delivers language learning, the TAM expansion is enormous. Von Ahn’s claim that Duolingo will have “the best math tutor app in the world in 2026” is a bold one, but it is grounded in the reality that generative AI has made adaptive math tutoring — previously extremely expensive to personalize — achievable at essentially zero marginal cost per additional student.

05 / THE AI PARADOX