First Republic Q4 2022 Earnings Call Summary

First Republic Bank has been caught up in the recent banking panic, despite having its ''best'' year ever in 2022.

In recent news, First Republic Bank has been making headlines after dropping more than 50% pre-market, causing fears that it may follow in the footsteps of Silicon Valley Bank. To provide more insight into the bank's current state, we will be delving into their latest earnings call and highlighting some key takeaways

First Republic's Financial Performance in 2022

First Republic had its best year ever in 2022, with record loan growth and earnings per share.

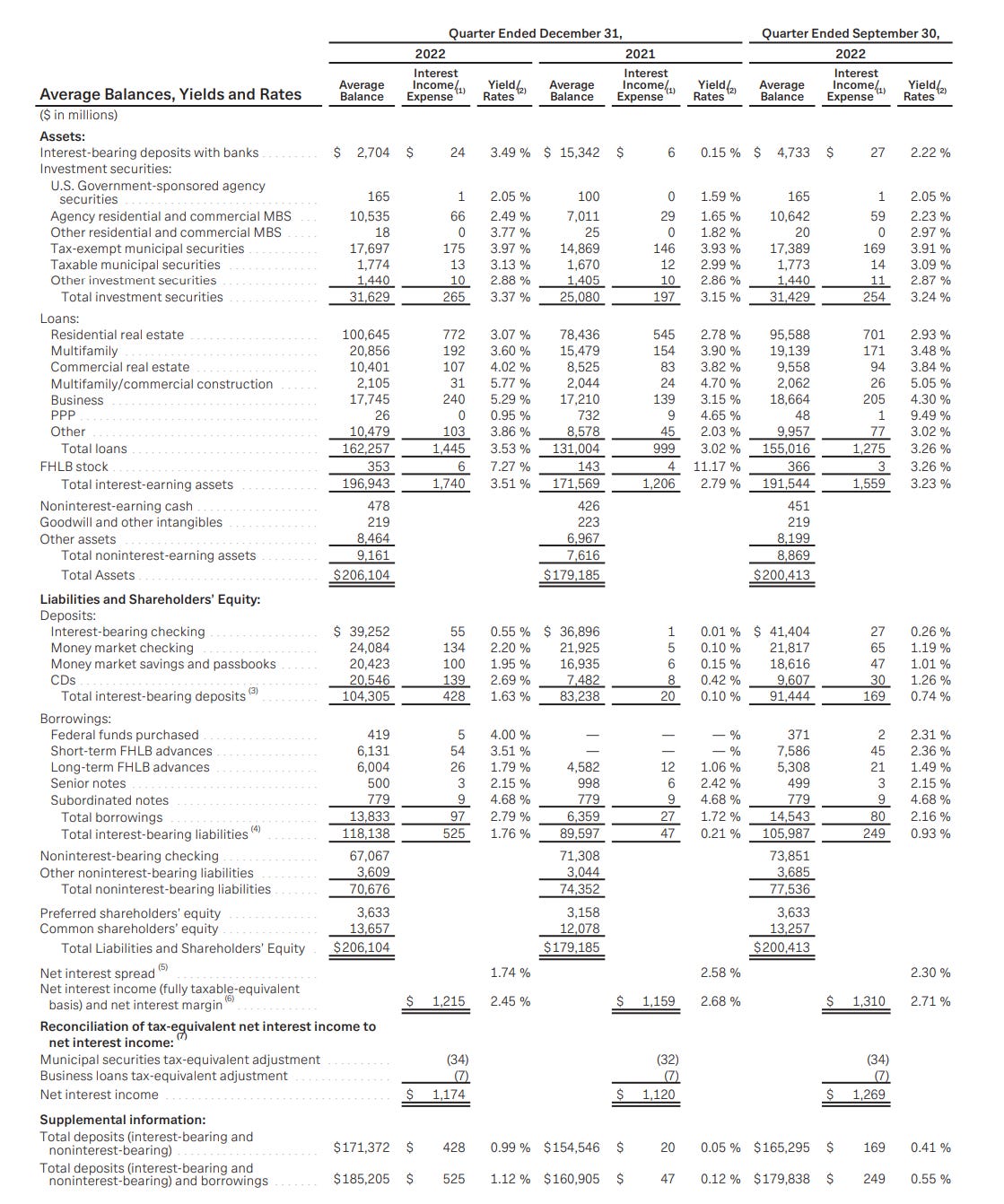

Total revenues and net interest income both grew 17% year-over-year.

Nonperforming assets were just 5 basis points, lower than previous years.

Credit quality remained excellent.

The bank had a strong year in terms of client service and credit performance.

The 2022 results were in line with or better than the expectations communicated at the start of the year.

The bank is experiencing margin pressure due to the rapid rise in rates and the current inverted yield curve.

The Fed funds rate is expected to peak at 5% and then gradually decline in the second half of the year.

The bank's net interest margin for the full year 2023 is expected to be approximately 25 to 30 basis points lower than the fourth quarter.

The bank's net interest income is a key metric for its differentiated business model.

Despite the current margin pressure, the bank expects net interest income for the full year 2023 to be down only 2% to 5%.

The bank expects continued strong loan growth in a more normalized rate environment in 2024.

The bank expects to deliver strong double-digit, net interest income growth in 2024, in line with its past performance.

The years following tightening cycles have historically been strong for the bank.

The bank expects expense growth in the high-single digits for 2023.

The bank is prioritizing its expenses in a way that will not sacrifice client service, growth, or safety and soundness.

The bank has identified $150 million of planned expenses that it will not incur in 2023.

The bank's full-year tax rate is expected to be around 24%.

The bank will continue to deliver exceptional client service, grow new households and provide safe growth in 2023 and beyond.

First Republic's Client Service and Growth

First Republic's 2022 Net Promoter Score, which measures client satisfaction, was the highest ever.

The bank's exceptional service and focused lending led to safe organic growth during the year.

Millennial households grew 17%, contributing to the bank's long-term growth.

First Republic's exceptional Net Promoter Score demonstrated its ability to deliver differentiated client service.

First Republic's Business and Wealth Management

Business client base grew by 18%, and business loans and line commitments were up 14% year-over-year.

Total assets under management in First Republic's wealth management business were down only 3%.

Wealth management fee revenue was up more than 15% from the prior year, with strong growth in brokerage, trust, insurance, and foreign exchange services.

First Republic's integrated banking and wealth management model continued to make it a very attractive destination for successful wealth professionals.

Deposit Growth and NIM Outlook

The rate being paid on checking balance has more than doubled from the prior quarter.

The average balances still came down about $9 billion.

The bank continues to focus on the relationship with clients to ensure they're leaving the right balances in checking for their operating needs.

The bank communicated a low 30s beta on overall deposits in the past and feels like 30% to 35% is about the right range still at this point.

The bank expects to fund loan growth largely with deposits and borrowings.

The growth rate will probably be greater in CDs than in checking given where the rates are this year.

The bank's NIM outlook has been impacted by the inversion of the yield curve, which won't last a very long time.

Margin and Interest Income

The company expects a deposit beta of 30% to 35% to hold, but it may increase slightly if rates hold for an extra quarter or two.

The beta is dependent on the macro outlook, which the company doesn't control.

The net interest income is expected to stabilize in the middle part of the year and increase towards the back half, with a positive trajectory into 2024.

The company expects low double-digit NII growth in 2022.

The company expects strong operating leverage in 2024, with opportunities to optimize and prioritize for efficiency.

Loan Growth

The pipeline is healthy, although it's down from the last quarter, with headwinds on the refinance side.

Business banking, PLP, PLOC, and securities lending are doing well and contributing to the pipeline.

CPRs are down, which gives the company a good base to grow.

Market Share and Growth

The disruptive moment in the mortgage market is an extraordinary opportunity for the company to take share.

The disruption in the mortgage market is handing the company an opportunity on a silver platter.

The company's service and availability are more important than pricing on short-term assets like 4- or 5-year mortgages.

The company is seeing caution but still active investors in the capital call business, with a slight tick up in private equity activity overall.

Deposits

Clients are currently more inclined towards 8- and 10-month CDs rather than shorter ones.

Rollover opportunities present a chance for the company to demonstrate extraordinary client service and engage with clients about their needs.

The company's CD duration has been in the 4- to 7-month range, which makes sense if the cycle rolls over midyear.

CDs and Customer Acquisition

Majority of CDs likely to reprice in the next 3 to 6 months.

CDs preferred over FHLB funding due to their customer acquisition benefits.

CD pricing is more attractive than FHLB.

CD offerings used to acquire new customers and develop relationships.

Good percentage of CD customers also open checking accounts.

Relationship building with customers is prioritized over rate offering.

Service level meant to differentiate from other offices.

Expenses

Expense reduction is broad-based.

Efficiencies gained from new core system result in less need to hire in certain areas.

Compensation levels adjusted given the mix of business.

Spend prioritized and optimized for safe, stable growth.

Two teams hired in Wealth Management.

Loan Growth

Mid-teens loan growth expectation.

Mix of loan categories consistent with previous years.

Good time to acquire clients at First Republic.

Refi mix was 36%.

Noninterest Income and Wealth Management

Double digit noninterest income growth expectation.

Investment management to be around $150 million for Q1.

Expect a strong year in terms of overall growth in investment management fees.

S&P up since September 30.

LTV and Commercial Real Estate

Median LTV on commercial real estate origination is just under 50%.

Expect very conservative underwriting.

NIM and CD Mix

Net interest spread does not factor in noninterest income.

Focus on net interest income over margin.

CD mix expected to continue into 2023.

CDs used as a tool to acquire new households and deepen relationships.

Derivatives

Bank historically does little with derivative financial instruments.

Yield on cash does not change how the bank thinks about derivatives

Margin and Efficiency:

Market response indicates expected difficulty in 2023 and 2024.

First Republic's natural efficiency ratio projected to be 62-64%.

Deposit costs depend on client appetite and checking ends up above 50% of deposits.

BOLI Run Rate:

Q4 had a benefit from the life insurance policy, and mark-to-market on insurance contracts.

Run rate for the quarter without the 2 items is still within 20-22.

New Offices and Checking Account Attrition:

Focused on relationships with the full breadth of services.

Around 6 offices expected in the existing footprint.

No significant change in the checking account attrition rate.

Credit Quality:

No expected issues going forward, business as usual.

Sticking to their knitting, being cautious, selective, and focusing on relationships.

Wealth Management Team Profitability:

Typically takes within a year to 18 months for teams to reach run rate profitability.

Teams hired generally have a lot of traction with their clients.

Closing Remarks:

First Republic Bank is optimistic about the future and looks forward to the year ahead.

Key Takeaways from what was said on the Call:

First Republic had its best year ever in 2022, with record loan growth and earnings per share.

Total revenues and net interest income both grew 17% YoY, and credit quality remained excellent.

The bank's net interest margin is expected to be approximately 25 to 30 basis points lower than the fourth quarter, with margin pressure due to rapid rate rise and inverted yield curve.

The bank expects continued strong loan growth in a more normalized rate environment in 2024, with mid-teens loan growth expectation.

The disruptive moment in the mortgage market is an extraordinary opportunity for the bank to take share, with its service and availability being more important than pricing.

First Republic's focus is on exceptional client service, growth, and safety and soundness, with expense growth in the high-single digits, but with $150 million of planned expenses that it will not incur in 2023.