GameStop: Saved by the Bubble!

GameStop: Saved by the Bubble!

Today in a much stronger situation, they have been given permission to act as a Start-Up

This is our 17th piece at LongYield and on this edition we decided to have a look at the very popular GameStop. We all know what happened recently, how GME stock went from almost being close to zero, close to bankrupt and with high 140% short interest to reach a pre split price of about $480. They nearly bankrupted many hedge funds, forced some research firms out of Short research (Citron) , forced Robinhood to halt trading, made millions to many, but perhaps made long term investors of many more. These long-term investors are not long term investors because they wanted to, they are now long term investors because they came late to the party, they are left holding the bag as they say. The people that made millions most came in late 2020. All of this might have started when Ryan Cohen bought 9% of GME, this happened in August 2020 and might have triggered what happened in early 2021. Today shares of GME are trading at around $25. This is $100 in pre split pricing. GME has a 4 for 1 split in July 2022. So to get back to its $480 high they need to get to $120 in today's share count. Where the company is today and where they were back in 2020 or 2019 is completely different. Their financial position and their strategy is completely different to what they had when they were shorted or called that their business was in “Terminal Decline” by Andrew Left, they writer at Citron research. We will try to find out if they are still in Terminal decline.

Pre WallStreetbets:

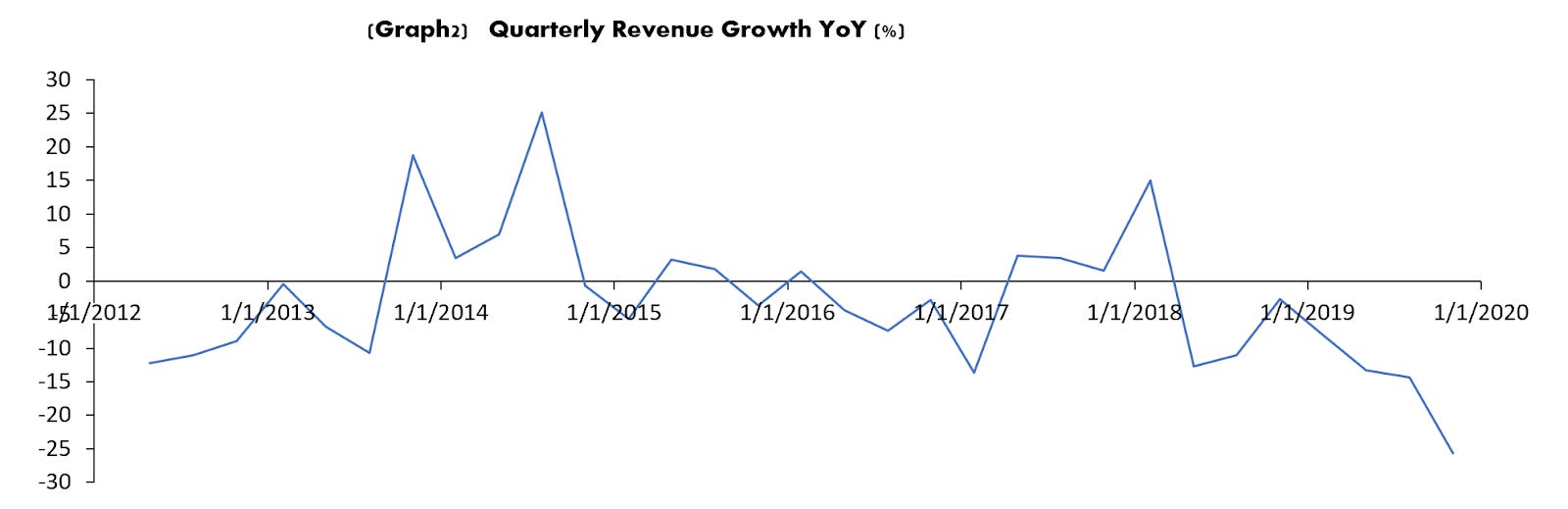

For this company specifically it is important to see how their P&L and Balance Sheet looked before the craziness of early 2021. Revenue was coming down hard since 2016 and the pandemic seemed as the nail in the coffin.

Revenue growth was pretty much dead. There was nothing positive in terms of the top line. The company has been struggling for more than 5 years.

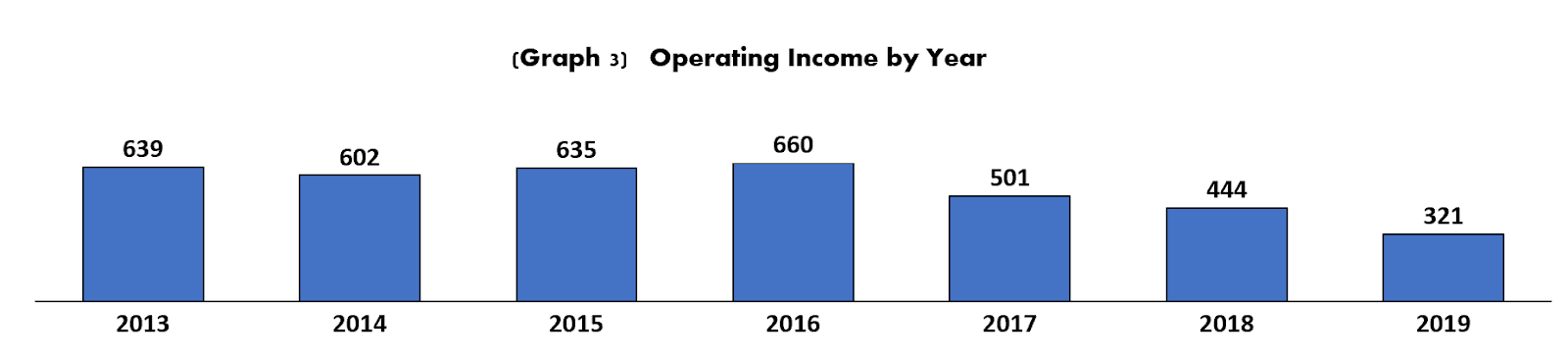

Operating income was turning the wrong way as well. It was not like you could say that bankruptcy was just around the corner, but operating income was cut in half from 2013. They were still making money in 2019, so it wasn’t good, but it sure wasn't a bloodbath but you could understand that it was a matter of time before the trend continued getting ugly. They did have a net loss in 2019 but this came from and impairment expense of $970m and was balanced by divestments during that year, at the end of 2019 their actual cash generated from operations was still around $325 and their full cashflow was positive due to the divestitures, the year brought $771m in cash

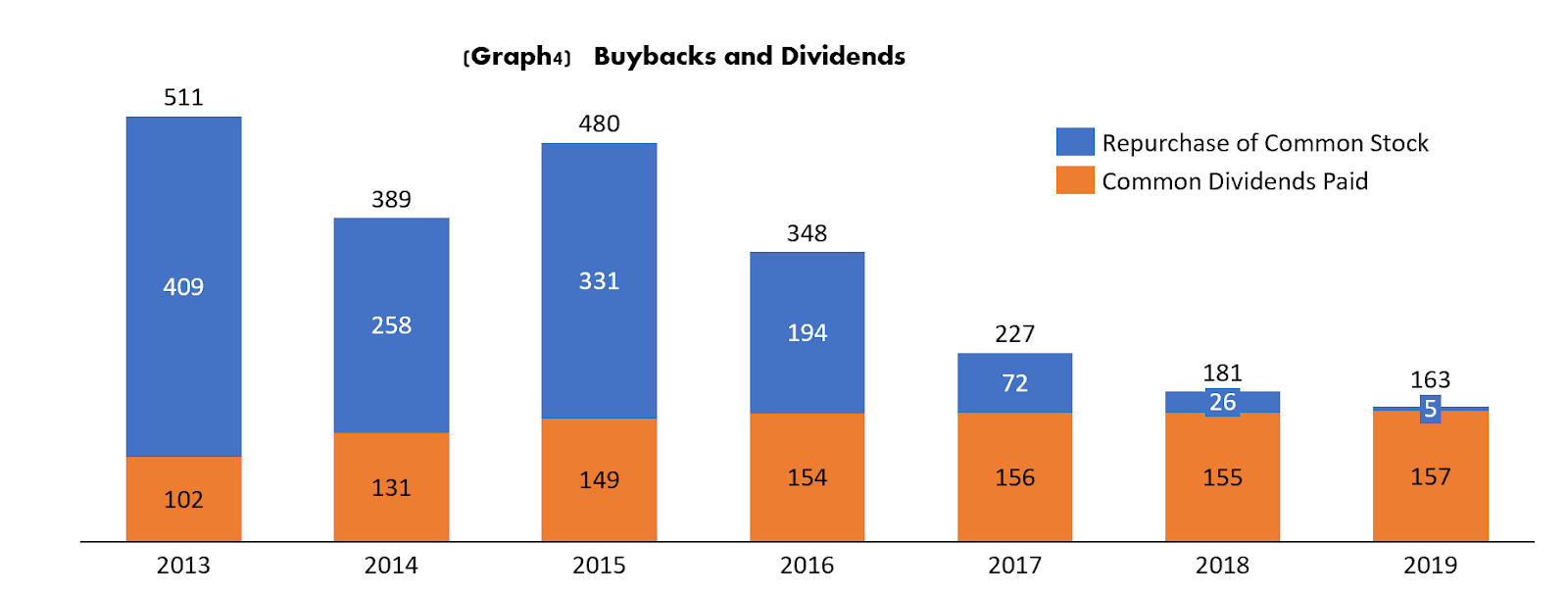

On the balance sheet side debt was rising, it ballooned, from nearly zero to close to a billion by the end of 2019. Their cash went up to $1.6b by the end of 2019, this was achieved thanks to divestitures and the fact that they actually remained cash flow positive through all these years where revenue was slowing down. They actually generated $3.8b in cash from operations from 2013 to 2019. They were even repurchasing stock all this time, they had a net repurchase of $1.2b from 2013 to 2019. And that is not even all, they had $1b in dividends paid over the same period as well. So $2.2b in cash is spent between dividends and buybacks. They were a clear mature company that was trying to become a cash generating company returning money to their stockholders, they were not thinking about huge growth, and were starting to suffer from considerable de-acceleration in revenue due to the shift on how video games are purchased. (Now you are able to just buy them and download online, instead of getting them at a physical store like GameStop) From the graph below you can see that with revenue slowing down, buybacks were close to being done, dividends on the other hand, were still very stable.

The company by the end of 2019 did not have a terrible financial situation at least not yet. They had cash, they were still generating positive cash flow. The only issue was that the brand was damaged, it was more a reminder of the 90’s or the early 2000’s that anything gaming is doing now. The trend more than anything else is what was bringing the heavy short interest. It was thought as an industry being disrupted, or more than an industry, a selling channel being killed and replaced by online downloads. It was just a matter of time until they became cash burners and started to go downhill financially or at least that is the bet that the short sellers had (and the pandemic was just going to accelerate that trend). It just happened that the pandemic also came with a lot of people with free time doing nothing and a lot of these people with free money from the government without any fear of losing it all.

Business Model:

Revenue Streams & Operational Model:

We will focus this section to their new strategy where they are trying to go now instead of what they were pre pandemic (which was pretty much a reseller of video games and video game devices)

Their new strategy is focused on 4 main things:

e-Commerce

GameStop wants to be the top of mind marketplace for anything that has to do in gaming and entertainment. This could be something very close to an electronic e-commerce site, something that does not really exist today. BestBuy could be the closest, but they are more focused on the physical locations side and on the tech support side. And if something has been proven by many players, it is that Amazon plays everywhere, but is not the main player everywhere. It has been shown by Chewy, by Wayfair and many clothing stores. There is space in e-commerce for more specialized players in each space.

GameStop is redesigning its application and its website, a lot of this work has been happening already. Many of changes have been done to the app and the website already and is starting to look a lot like a good e-commerce website.

Expand selection in gaming & entertainment.

They want to go beyond what they had, usually what you saw at GameStop stores before was video games, consoles, a couple of supporting devices, toys, collectibles and used tech. They want to expand this product offering, meaning adding more and more specialized products, they want to become the leader in pc gaming and virtual reality.

Leverage existing strengths and assets

They have a lot of stores, they will use these as a way to have one day delivery. They also want to grow their loyalty program and expand the scope of their buy, sell, and trade business to support expanded offering.

Invest in new growth opportunities

As they scale and expand their core offerings they will simultaneously invest in additional growth, including blockchain, digital assets (including non-fungible tokens ("NFTs")), Web 3.0 technology, and new destination formats for their stores. In January 2022, they entered into partnerships with Immutable X Pty Limited (“IMX”) and Digital Worlds NFTs Ltd. ("Digital Worlds") pursuant to which IMX will become a technology partner and platform for their NFT marketplace, and Digital Worlds will grant up to $100 million in IMX tokens to creators of NFT content and technology. In addition, Digital Worlds agreed to provide up to approximately $150 million in IMX tokens to GameStop upon the achievement of certain milestones.

They want to play in what could be the future of gaming and the future of many things. Web 3.0 is something that today is more like a bet, like a lottery ticket. Nobody knows what will become of web 3.0, its potential is huge, its potential is to change the internet forever, but this is very uncertain at the moment if it will ever fulfil that potential. If they are right, it is pretty much like the internet in the 1990's, it was an environment of many internet players, they all were right in that the internet was going to be huge, but there were still very few Amazons and a lot of Pets.com. We will find out with time if getting into Blockchain will be good or not, what we think is that for a company like GameStop is a good decision to at least play in the space, test the waters you could say. And perhaps, what they start with (NFTs) won’t be what becomes successful for them in blockchain, but they will be playing in the blockchain field and will evolve within.

These four points are their main strategy now, it is more in line with the 21st century economy. Everything happens online now, and having a good ecommerce presence and leveraging current infrastructure (current stores) could be a good way to start rapidly.

PowerUp Rewards

Loyalty programs generally offer their customers the ability to sign up for a free or paid membership which gives their customers access to exclusive gaming related rewards. The programs' paid memberships generally include a subscription to Game Informer® magazine and additional discounts and benefits in their stores and ecommerce properties.

Key Metrics / Performance

Revenue and Key KPIs

GameStop has been restructuring the company for many quarters and the pandemic has been done for a while now. Some revenue improvement has been seen, from the lows since 2020, but still nothing above what they had. The average revenue during Q2 of the 3 years prior to the pandemic was $1.5b, way higher to what they had in 2022. So in terms of revenue, still nothing has changed trend wise.

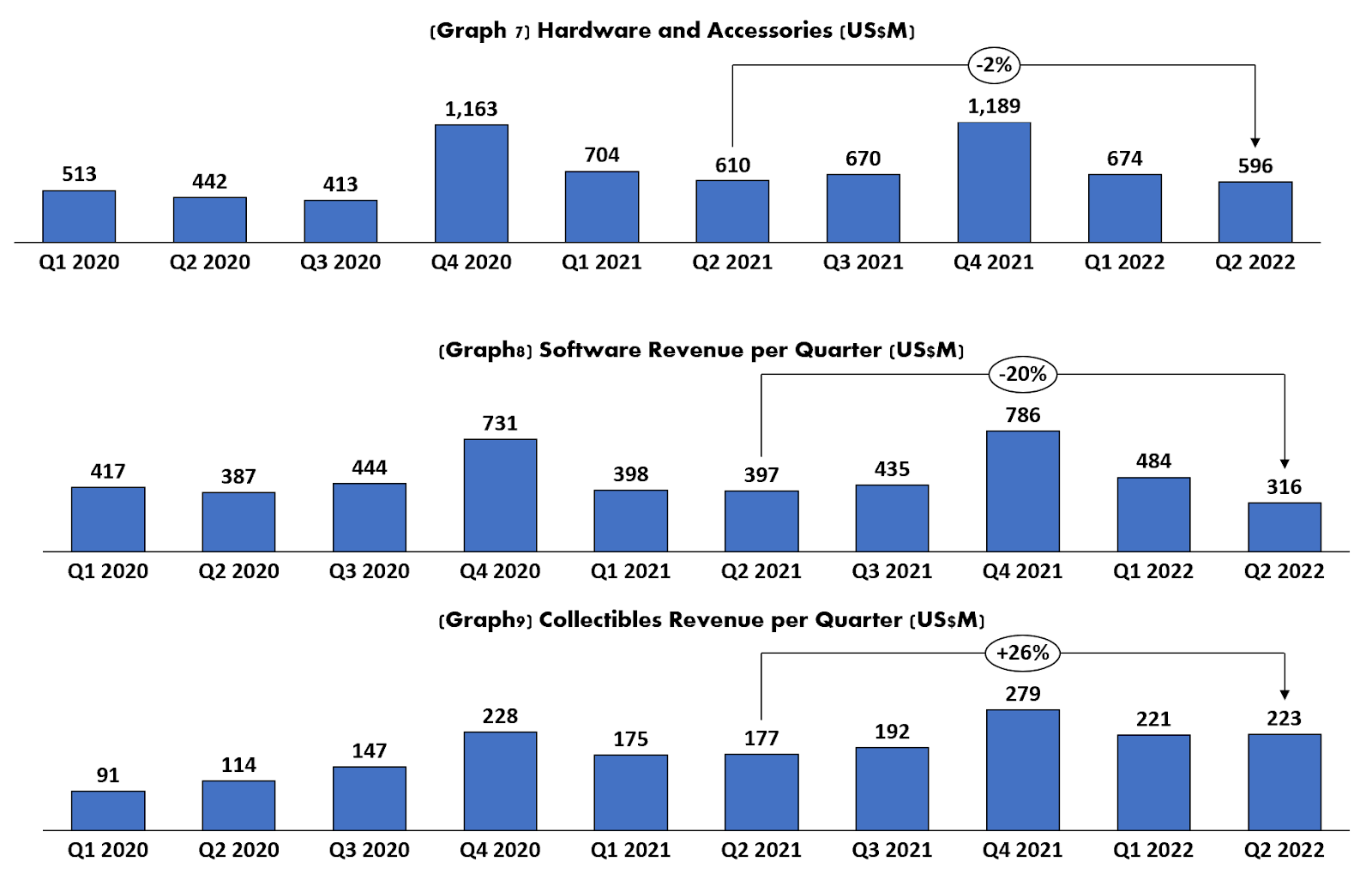

When you stop and look at the revenue in each of their business lines, there are different stories going on. Hardware is pretty much flat, it is down 2%, but Q2 2021 still had some Covid effects, mainly on Covid free money from the government, so that is why we could say that it is pretty much flat. On the Software side the difference is big, they have dropped 20% YoY. Their Software line Includes sales of new and pre-owned gaming software, digital software, and PC entertainment software, so having 20% down here might be a pretty big deal. Software is pretty much what is impacted the most by the downloading of video games, the line that becomes the bigger risk for them, the part that is being disrupted the most. Their Hardware side is one that could grow a lot if their e-commerce strategy is done correctly, hardware includes sales of new and pre-owned hardware, accessories, hardware bundles in which hardware and digital or physical software are sold together in a single SKU, interactive game figures, strategy guides, mobile and consumer electronics, so pretty much everything that could be deliver to a customers house, and everything that can become e-commerce easily.

The one section that is growing pretty well from last year is collectibles, another part that could become very e-commerce friendly.

GameStop is battling against the drop of their Software business. The faster they replace these revenues with other things the better. So if they manage to keep overall revenue flat for the next few quarters would be a good sign, it would be a sign that they are being successful in growing the rest of their business. Software could die for them, unless they enter the platform side, a thing that would be very complicated and not likely, at least not in the short term.

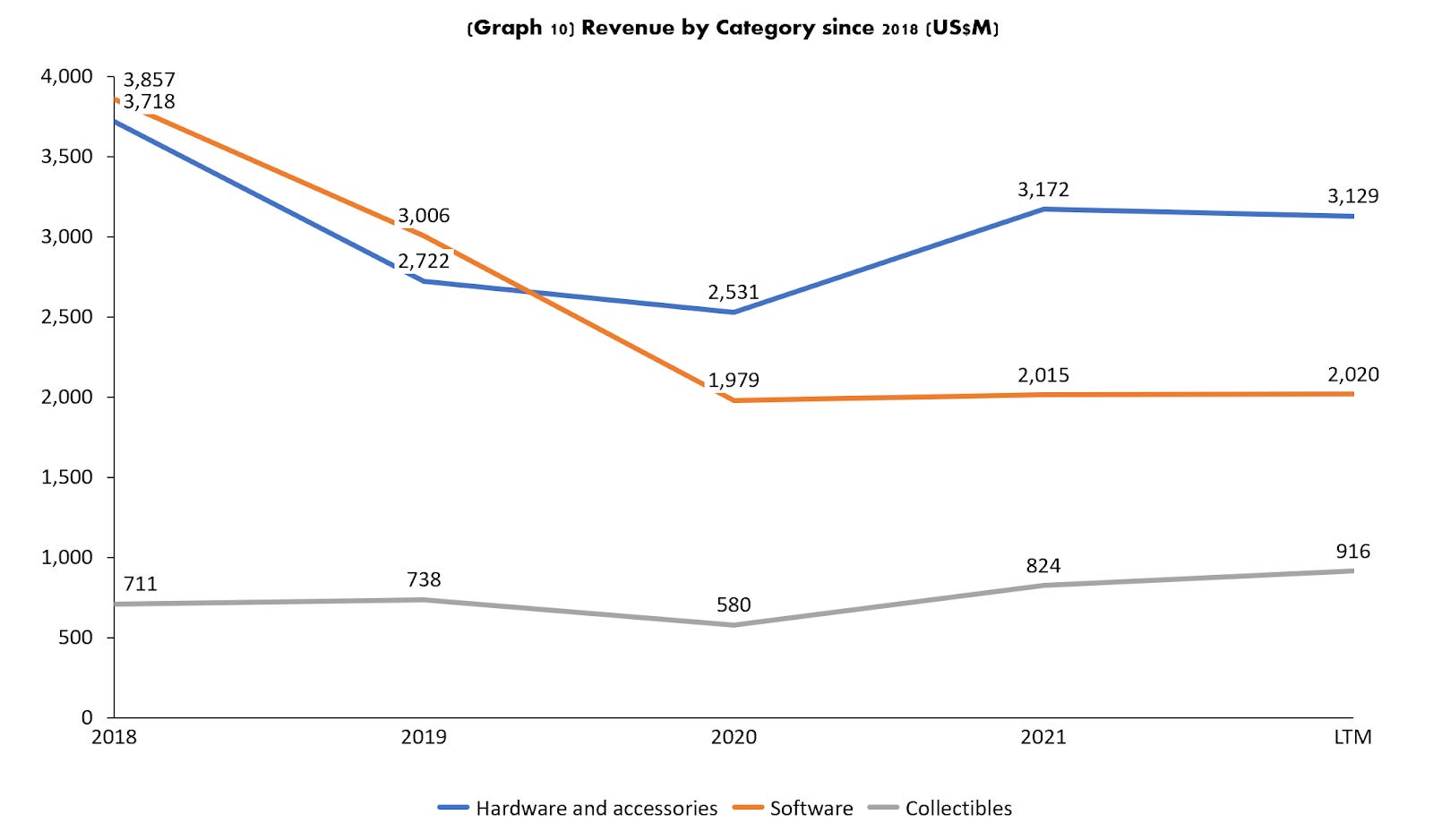

This is all very clear when you look at the bigger or longer term picture. Software is dying. It has not recovered from the pandemic drop. Software lost $1 billion in revenue from 2019 to 2020 and has not recovered almost anything. A different story you see from Hardware, they lost about $200 million and today they are about $400 million above their 2019 Hardware revenues. Collectables also are above their 2019 revenues. Software is by far their biggest issue; they have lost almost half their 2018 revenues, when software was their biggest business at $3.8b.

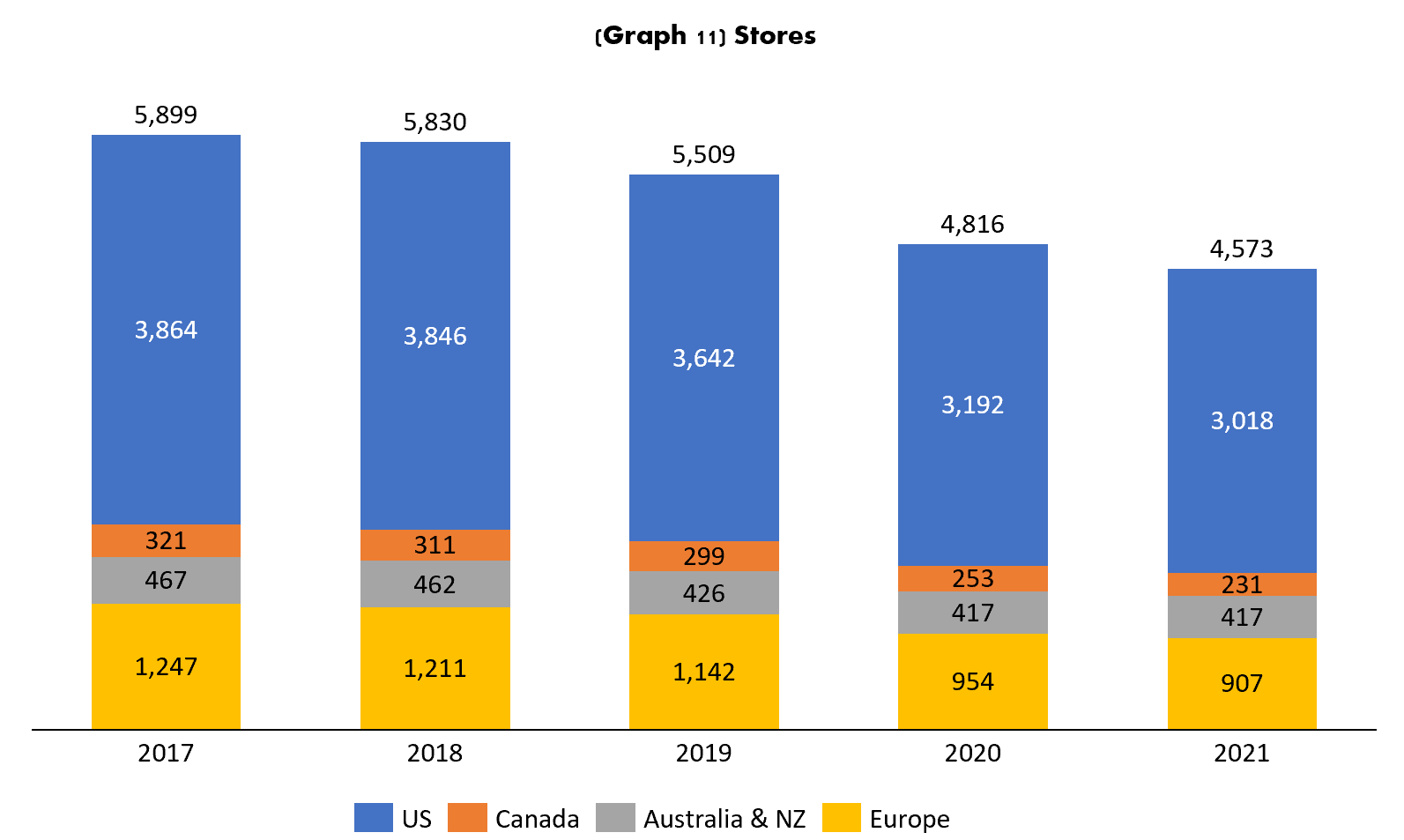

One of their biggest assets today is their presence all over the country (and also presence in Europe, Canada, Australia and New Zealand) They have 3K stores in the US and another 1.5K internationally. They have reduced their presence over the past few years but now this infrastructure might come in handy for fast same day delivery on their ecommerce business.

Revenue by region has similar trends between them, they all have lost a great amount of revenue since 2018, they all are pretty much flat since 2021. But when looking at revenue per store it has improved a little in Canada and Australia while reduced in the US and Europe, yet they are all better today than in 2019 (Graph 13)

Costs and Expenses

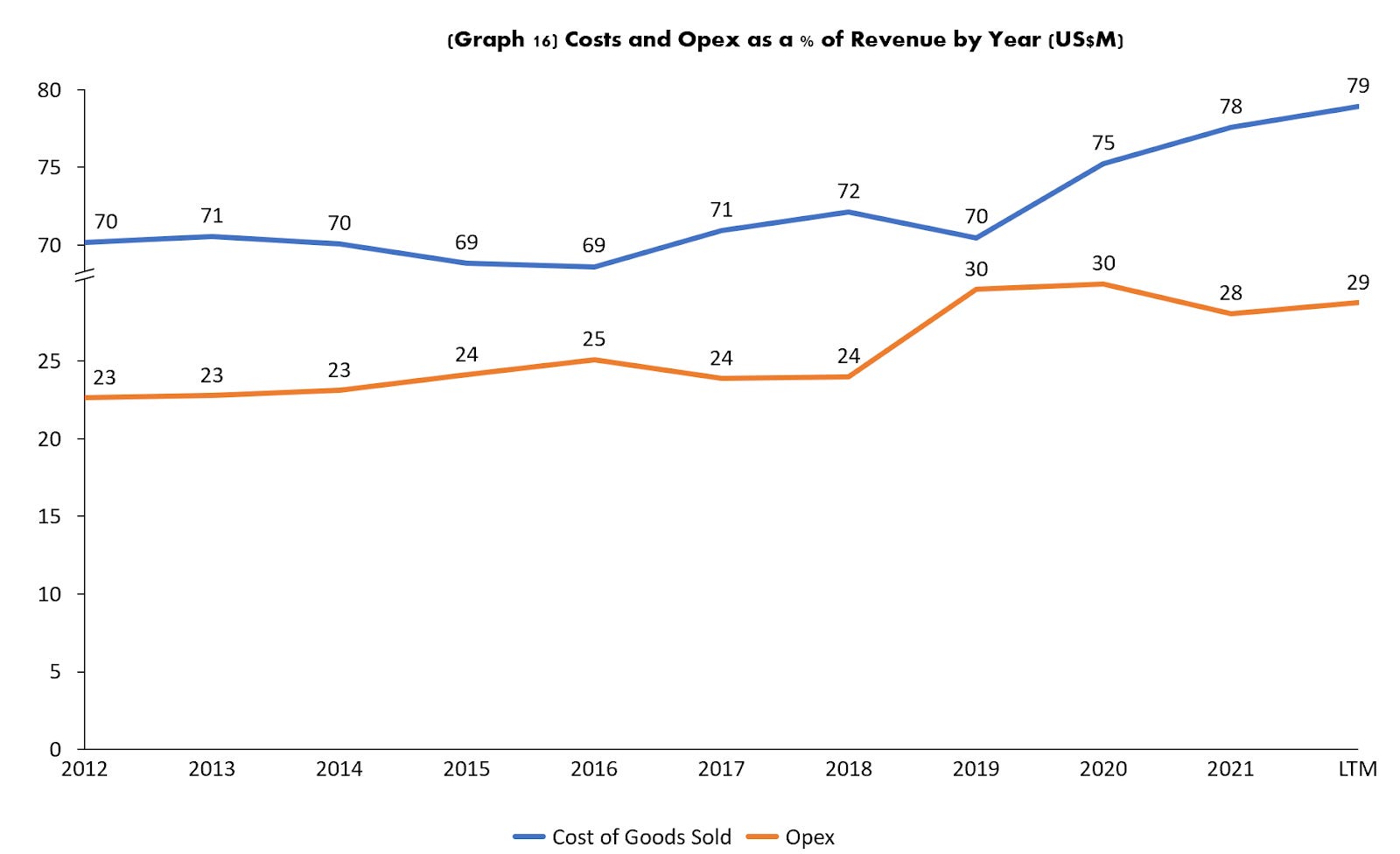

Cost and OpEx have remained overall flattish (a bit above but not considerably higher taking into account that they went through the pandemic and the start of heavy restructuring) since the start of 2020.

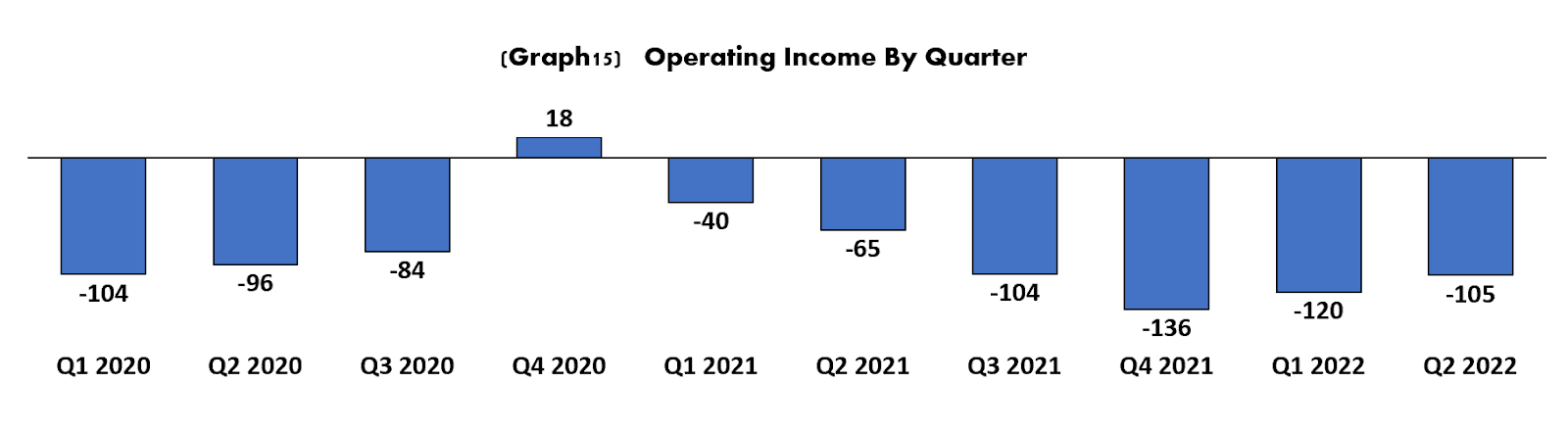

As we saw in the pre pandemic section, GameStop was still profitable by 2019, since 2020 they have been losing money every year. Over the past 10 quarters they have accumulated losses for $835m. They had only one positive quarter which was during the 2020 holiday season. In a way, we could say that we should expect GameStop to have losses for many quarters from now on. This is not the same old 90s company, this is basically a new company that got a reboot since the WallStreetbets drama, it has started a new “growth” strategy, we could expect that this company will behave a lot more like a startup, losses are expected to continue even if revenue starts to grow.

Looking at the broader picture, the cost has grown by 9 percentage points and Opex by 5 percentage points.

Cash Flow

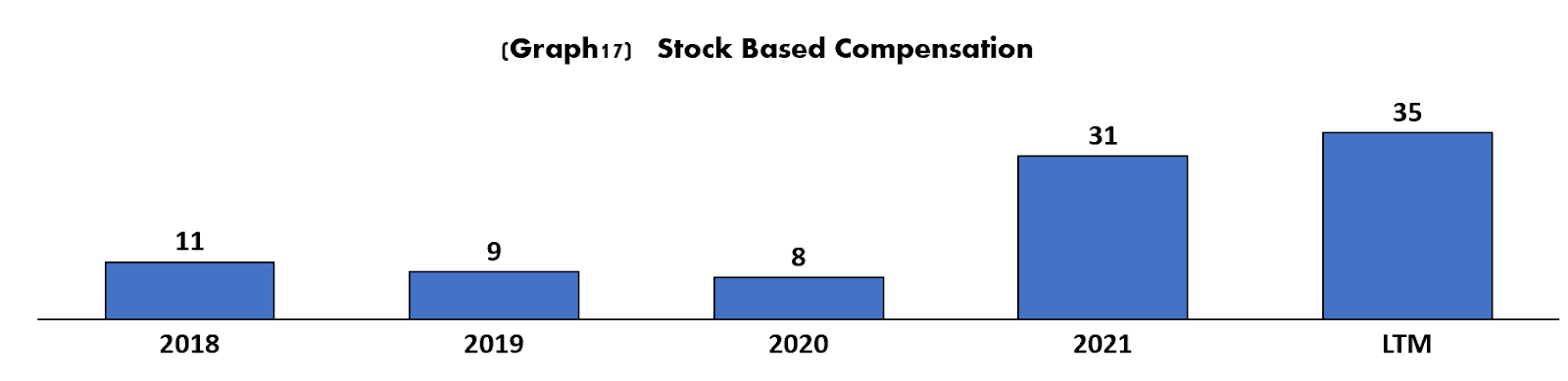

One clear change that the company has made is giving a lot more focus to use Stock based compensation. They have multiplied it by close to 3 times what they had in 2018. This is a classic move by startups and tech companies to save cash. They must use this as much as possible, and they pretty much have said that they would with decisions like having the board fully paid in stock, it helps a company like this to attract better talent, young talent that wants the challenge to take the company to their future growth opportunity and become rich in the process. (with Stock compensation)

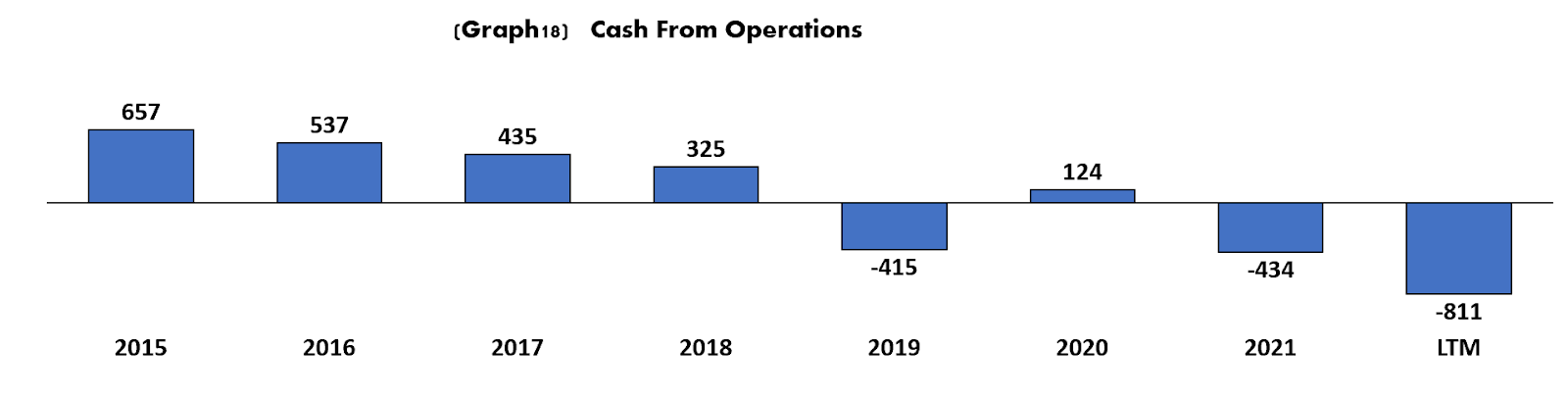

They have been using a good amount of cash over the past 12 months though, even taking into account the SBC, they used $811 million. A lot of that cash has been working capital moves, change in inventory was $161m (understandable since part of their new strategy is to improve their product offering). The large inventory rise was done during Q3 2021, this could also be a case of stocking for an uncertain period in the supply chain. The change in inventory during that period was $546 million, the 3 following quarters consumed $385 million of the $546 million. Accounts payable $185m (also understandable since they are expanding their e-commerce operation) One could say that this will not become something normal and consistent. These working capital movements will have to go back once they reach the level of growth acceleration that they want to reach and also when supply chains normalize

Capex has remained stable, so it seems that their growth is focused so far in using current infrastructure and expand their inventory to improve their e-commerce rather than going all in on new fulfillment infrastructure

On the Debt side they repaid pretty much all their long term debt and on their cash side they managed to take advantage of the wall street bets craziness and raised $1.6b in stock since then. It basically has given GameStop the luxury of having new life, they are pretty much a new company, they have a lot more cash, lower debt, new employees from the tech industry, etc. They went from old brick and mortar to tech startup. At least on paper so far.

Balance Sheet

They closed Q2 2022 with $909 million in cash while $602 million in debt. The last quarter they consumed about $100 million from operations, the average over the past 12 months is about $200 million per quarter adding about $60 million for capex. They have about 1 year of cash right now.

Competitive Landscape

Competition within the market that GameStop seems to be targeting is broad, but not consolidated, at least not consolidated in the way that GameStop seems to be trying to achieve. GameStop will be playing in the electronics market, the gaming market and the blockchain space.

Some of their stronger competitors today are Amazon, Best Buy and Walmart. On the blockchain side the competition in terms of NFT markets is very large and at the same time it is also too soon, this space will likely consolidate

First let's have a look at their electronics competition. The first one would be BestBuy. BestBuy is a very large electronics brick and mortar player that has survived even with the threat of e-commerce giants like Amazon. They have been able to stabilize and grow their business considerably for the past few years. Best buy today is 35% larger to the size it had in 2012. The company didn’t even have a considerable drop during 2020, it went up in terms of revenue, a clear sign that a lot of people were running after devices for working from home, school from home or even gaming for entertainment while inside.

What we can see from BestBuy, is that the possible market for GameStop could be very large, if they become the go to place for electronics and gaming they can get some of the market share away from BestBuy. Though BestBuy sells a broader electronics offering when compared to GameStop. Best Buy sells things like washing machines, printers. GameStop is not selling this type of electronics so their target market is smaller but still Best Buy has shown that the market is big.

Amazon and Walmart are more difficult to tell how big their electronics market is today, since they are in many other markets and do not report electronics specifically, they are clear players here. You could even say that perhaps they are bigger than BestBuy in electronics. The below is an old statistic, but one could use it to assume that Amazon actually passed BestBuy even if BestBuy kept growing its revenue, the category has kept growing so there was growth for everyone.

Last but not least, the gaming market is growing, and growing fast. GameStop was going against its own trend, they were becoming smaller while the industry was growing rapidly, but this mainly because most of its revenue was related to software and software had gone online and bypassed completely a distributor like GameStop. The gaming market is expected to reach $546 billion by 2028 worldwide with a CAGR of 13%.1. That is a great healthy market, a market in which GameStop could still find its place outside software.

Some of the possible risks for the company are:

Software: Their Software business is dying and it will die. They need to control how quickly this business dies (Well control it as much as possible) If this business , currently at $2 billion, dies a more rapid death, this will become very painful in term of cash generation, they need this business to hang around a little bit longer to give them a comfortable opportunity to pivot away from software and fully achieve their ecommerce penetration.

Future dilution: This is more a risk to the current stockholders than anything else. GameStop could continue to use their stock as a way to finance their plans to restructure. They continue to be a very popular stock and this could easily be exploited by management. Just have a look at what AMC did with APEs. They could continue offering stock diluting current stockholders.

Down to one Bullet: This is it, if e-commerce does not work it's likely the last breath from GameStop. They would likely have to go back to reducing the amount of stores, with revenue going down, they would have to reduce stores and with that reduce the possibility of any ecommerce growth.

What could be the case for GameStop being a good opportunity for the next 10 years?

Brand: GameStop brand is very popular and has very strong nostalgic bonds with young adults. The brand also now enjoys very strong bonding with people that invested with them during the WallStreetbets craziness. All of these branding positives have to be exploited and taken advantage of to establish their e-commerce presence.

Market: Gaming is a very big and high growth market, something that they need to exploit as well. The growth that will be seen in this area is still yet to be seen, and if the metaverse becomes a thing, there will be a lot of great bunch of devices and gadgets that will be needed that do not even exist, that will be purchased at ecommerce places like this. GameStop must establish itself as the ecommerce gaming place to take advantage of all these future trends in gaming.

Brand new company: The company got a free get out of jail free card. They were slowly going the way of Sears or Blockbuster, etc. They got new life when they became the poster child of the memestock craziness. This gave them the opportunity to clean up their debt, to get a lot of cash and to get a new strategy and new people. This basically has given them a reboot, this is not the same company that they were in 2019. They are now basically a startup and the gamer customer for now is an orphan, they don’t have a gaming place to go for electronics.

Valuation

This company has gone through heavy swings in valuations ever since 2021. Today they sit at around $7.7b, this is 1.28 times last twelve months revenue. This seems low considering what we see as an average from S&P companies (around three times) but when compared to its likely main competitor, Best Buy, they are trading at a higher revenue multiple than them (0.29 times revenue for Best Buy). We have calculated a DCF analysis for GameStop and this time actually could be counted as two aggressive scenarios and one conservative or pessimistic. We would be missing the base scenario here. The reason why is because we see that GameStop has a very binary future, either their latest strategy starts to show growth in the next 24 months or the company will start slowly going down to zero. So the first of our aggressive scenarios takes the company as having success with their new strategy enough success to replace software revenues and having decent consistent growth over the next few years, for us the result of this scenario is $19 per share or about $5.8b valuation, lower than today but still a huge win for pre 2020 stockholders, the valuation was below $1b in 2020, so a 5X return on that is not bad at all. For our second aggressive scenario we take more aggressive growth, it is not only that they actually replace their software revenue but that they grow rapidly their e-commerce business. The results from this is $31 per share or about $9.4 valuation, again great return over their 2020 value. Our last more pessimistic or conservative scenario is just enough to keep slow growth and recover some of their software revenue through new revenue streams from e-commerce. This scenario gives us a valuation of $11 per share or about $3.3b valuation. The last possible scenario is that nothing is successful in terms of new strategy and they go to zero or get acquired. We did not model this but it is also a possibility, one that we believe is unlikely at this point given their improved financial situation and strong branding.

Still, remember that we have two aggressive scenarios, a lot of things have to go right, and the risk here is big, the reward, since the company already gained a lot of value, might not be that great, it is very small actually when taking into account the risk. (unless it becomes crazy again, which could happen and has nothing to do with their fundamentals)

Nice write-up. Think you nailed it. There just isn't enough progress being made or reward on offer for the risk involved.