GE Aerospace: The Perfect Beat That Sent the Stock Lower

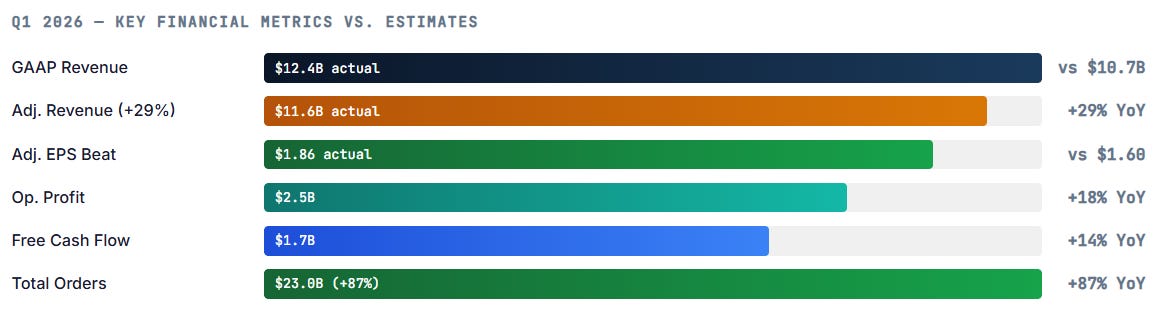

Revenue crushed estimates by $1.7B, orders exploded to $23B (+87%), backlog hit $210B+, and the CEO called guidance trending toward the high end. The stock fell 4.6%.

The Setup

When Perfect Numbers Produce a Down Day

There is a peculiar kind of earnings day that keeps experienced investors humble. GE Aerospace’s Q1 2026 report was one of them. On paper, the company delivered one of its strongest quarters since the 2023 spin-off from GE’s industrial empire — revenue crushed the Wall Street consensus by more than $1.7 billion, adjusted EPS came in at $1.86 against estimates of $1.60, and orders surged to $23 billion, a figure so large it represents more than half the company’s annual revenue in a single quarter’s bookings.

The backlog is now over $210 billion. Free cash flow grew 14%. Management maintained full-year guidance and said it is “trending toward the high end.” By any conventional earnings scorecard, this was a triumph.

The stock dropped 4.6%.

The explanation is not irrational. CEO Larry Culp, during the earnings call, was asked about the conflict in the Middle East — the ongoing U.S.-Israeli military campaign against Iran, now approximately eight weeks in, with the ceasefire agreement from the prior round set to expire. Culp gave an honest answer: if the Strait of Hormuz remains effectively closed, jet fuel prices stay elevated, and airlines begin deferring engine shop visits to preserve cash, GE Aerospace’s highest-margin revenue stream — commercial engine services — would feel the impact.

That single sentence, delivered candidly and carefully, was enough to redirect the market’s attention from a clean beat to an existential risk assessment. This is what rational markets do. The question for investors is whether the sell-off creates an opportunity or correctly prices a risk that isn’t going away.

“If we see airlines begin to defer shop visits due to elevated fuel costs, that’s a pressure point we’re monitoring carefully. We don’t see it in the data today, but the scenario is real.”

— Larry Culp, CEO, GE Aerospace · Q1 2026 Earnings Call

Q1 2026 Results

The Numbers: Orders Are the Lead Story

Let’s establish what actually happened in the quarter before turning to the risk narrative. The headline numbers are strong in almost every dimension, but the order figure demands particular attention because it speaks to the durability of the business over a multi-year horizon.

The $23 billion orders figure is the kind of number that stops analysts mid-sentence. For context, GE Aerospace’s full-year 2025 revenue was approximately $38 billion. In a single quarter, the company booked orders equivalent to roughly 60% of annual revenue. Commercial Engines and Services — the core franchise — drove $17.3 billion of that total, up 93% year-over-year. Defense and Propulsion Technologies added the balance, with orders up 67%.

These are not one-off spikes driven by a single mega-deal. The order surge reflects the structural dynamics of the narrowbody aviation market — Boeing and Airbus have order books that stretch a decade, and every new aircraft needs a GE or CFM engine (CFM being the 50/50 JV with Safran). The services tail from each installed engine lasts 20-30 years. An order book at this level means GE Aerospace’s revenue visibility is essentially locked for the better part of a decade, regardless of near-term turbulence.

The Core Business

Commercial Engines & Services: The Machine That Prints Money

If you own GE Aerospace, you own primarily one thing: the installed base of CFM56, LEAP, and GE9X engines flying on commercial aircraft worldwide — and the services revenue those engines generate for the next 20-30 years. This is the razor-and-blade model at industrial scale, with some of the highest switching costs in any business.

Commercial Engines and Services delivered $8.9 billion in revenue this quarter, up 34% year-over-year. It is the engine room (no pun intended) of the company’s profitability — commercial services carry operating margins estimated in the 25-30% range, dramatically higher than new engine deliveries, which GE essentially sells at cost or thin margin to win the installed base.

Commercial E&S Revenue

$8.9B (+34% YoY) — the services business accelerated this quarter as airlines continued to work through post-COVID flight network restoration and delayed maintenance catch-up. Engine shop visits remain elevated industry-wide as the older CFM56 fleet — which powers thousands of A320 and 737 aircraft — reaches mid-life service intervals simultaneously.

Orders: $17.3B in Commercial Alone

+93% YoY order growth in Commercial E&S. This figure reflects both new engine orders tied to Boeing and Airbus deliveries finally accelerating, and long-term services agreement renewals. Multi-year MRO (maintenance, repair, overhaul) contracts booked this quarter lock in revenue through the early 2030s.

The services model has a compounding quality that pure manufacturing businesses lack. Each engine delivery today generates services revenue for the next two to three decades. The LEAP engine — which powers the A320neo and 737 MAX families — is now accumulating flight hours at scale, and the services wave associated with that installed base is still in early innings. Shop visits for LEAP engines will peak in the 2030s, meaning the business has a long, visible runway ahead.

This is why the backlog number — $210 billion — matters so much. It is not just booked revenue; it is a contractual claim on future cash flows that is largely immune to year-to-year macro volatility. Airlines cannot simply cancel shop visit contracts when jets need to be airworthy.

“The $210 billion backlog is not a number. It is a structural moat. Airlines that skip GE shop visits are grounding aircraft. That is not a choice they make lightly.”

— LongYield Analysis · April 2026

Defense Segment

Defense: Record Orders for This Decade

GE Aerospace’s Defense and Propulsion Technologies segment is often treated as a secondary story behind the dominant commercial franchise. That framing deserves revision. Defense orders in Q1 2026 grew 67% year-over-year, reaching what management described as a record for the current decade. The geopolitical environment — active U.S. military engagement in the Middle East, NATO rearmament in Europe, and persistent Indo-Pacific tension — is creating a multi-year demand cycle for military propulsion systems.

The strategic implication for investors is that defense provides a genuine hedge against commercial cycle risk. If the Middle East conflict suppresses airline activity, defense spending accelerates — GE Aerospace’s two main revenue streams are inversely correlated to the same geopolitical events. That portfolio construction is worth a premium multiple in an uncertain world.

The Key Risk

The Middle East Risk: Shop Visit Deferrals

Here is the bear case in plain terms. The Strait of Hormuz has been effectively closed since approximately March 2026, following direct military action in the Iranian-Gulf theater of the broader U.S.-Israeli campaign against Iranian nuclear and military infrastructure. Brent crude is trading near $96. Jet fuel, which tracks crude with a slight processing premium, has spiked commensurately.

Airlines operate on razor-thin margins at baseline. A sustained period of $96 oil — particularly if it moves higher — compresses cash flow materially. When airlines are cash-constrained, the first thing they examine is the controllable cost base. Engine shop visits are expensive — a typical CFM56 heavy maintenance visit runs $2-5 million — and while contractually required for airworthiness, their timing can often be optimized. Airlines facing a cash crunch will defer a shop visit by 200-300 cycles if the maintenance envelope allows it.

The Mechanism of Deferred Shop Visits

GE Aerospace earns the bulk of its high-margin services revenue when an engine enters a shop for maintenance. If airlines defer shop visits — legally possible within airworthiness limits — GE’s commercial services revenue recognition shifts into future quarters. This doesn’t permanently destroy revenue, but it delays it, impacting near-term EPS.

Fuel Price Threshold

Based on historical airline behavior, sustained jet fuel above approximately $3.50/gallon (roughly correlated with $85+ Brent) begins to motivate deferral decisions. At $96 Brent, fuel is well above that threshold. The question is duration — a 3-6 month spike is manageable; 9-12 months could meaningfully shift shop visit timing.

CEO Culp was explicit that GE sees no evidence of airline deferrals in current data. Shop visit volumes and forward scheduling remain robust. But the candor of his warning — that this is a scenario he is “monitoring carefully” — was honest and appropriate, and the market priced the optionality of that risk accordingly.

The bull counterargument: GE Aerospace’s commercial services contracts often include take-or-pay provisions. Airlines that defer today are often contractually obligated to catch up within a defined window, or pay penalties. The revenue is not lost — it is deferred. And if the Hormuz situation resolves within 6-9 months, as prior Middle East episodes have historically resolved, the shop visit queue simply compresses into future periods.

“Deferred shop visits are a timing issue, not a revenue destruction issue — unless fuel stays at $96 for two years. No one is seriously modeling that. The market may be mispricing the permanence of the risk.”

— LongYield Analysis · April 2026

Tariff Situation

The Tariff Story: A Favorable Reversal

One underappreciated element of the quarter was a $100 million reversal of a previously recorded tariff-related charge. GE Aerospace had taken a precautionary accrual in a prior quarter for expected tariff impacts on its supply chain — imported titanium, aluminum, and precision components that flow through the company’s manufacturing network. The subsequent resolution of certain trade uncertainty (or re-examination of applicable tariff categories) allowed that accrual to be reversed, providing a one-time tailwind to operating profit.

$100M Tariff Charge Reversal

A $100 million reversal of prior tariff-related charges boosted Q1 operating profit. This reflects either improved clarity on tariff applicability for aerospace components — which often benefit from exemptions for national security-relevant manufacturing — or renegotiated supply arrangements.

$1B US Manufacturing Investment

GE Aerospace also announced a $1 billion commitment to U.S. manufacturing investment. This serves dual purposes: supporting the political narrative around domestic industrial policy, and practically deepening the domestic supply chain to reduce tariff exposure over time.

The broader tariff picture for aerospace is more nuanced than in consumer goods or automotive. The U.S. aerospace industry is considered strategic, and export licensing and tariff structures generally favor American primes. GE Aerospace’s global supply chain is well-established, and the company has decades of experience managing trade policy changes. The $100M reversal suggests the initial concern was somewhat overstated.

FY2026 Outlook

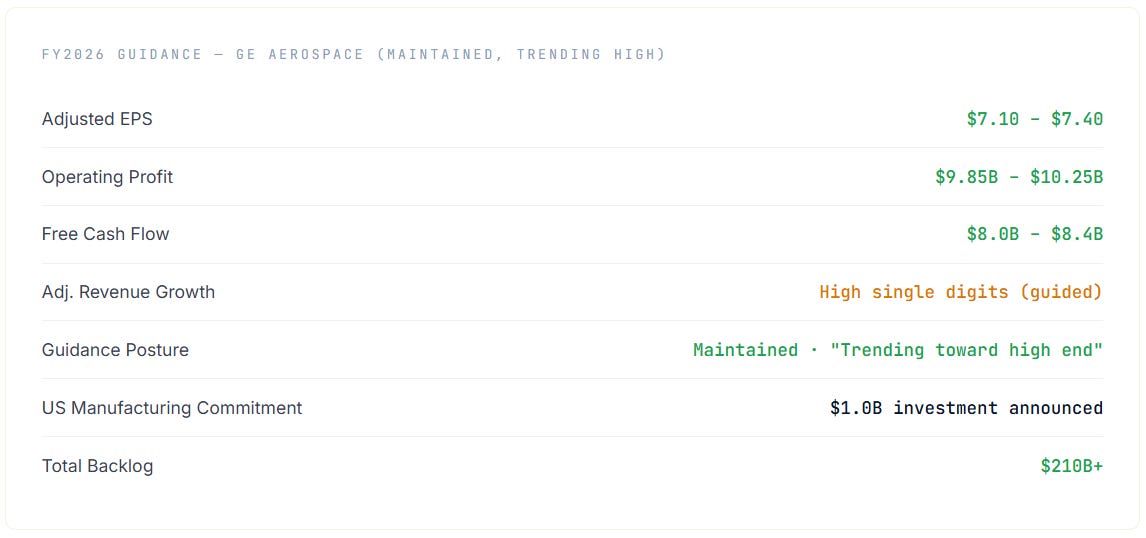

Guidance: Maintained and Trending High

Management maintained full-year 2026 guidance across all three key metrics and explicitly noted the company is “trending toward the high end” — a signal that internal tracking is running ahead of the midpoint of guidance ranges.

The FCF guidance of $8.0-8.4B for the full year against a Q1 print of $1.7B implies significant back-half weighting, which is typical for aerospace businesses. Large contract milestones and year-end deliveries tend to compress cash receipt timing. Investors should not be alarmed by the apparent mismatch between Q1 FCF and full-year guidance; the trajectory is consistent with prior years.

“Trending toward the high end” is notable phrasing — it is about as close to a guidance raise as management delivers mid-quarter without actually raising guidance. It signals confidence without creating a formal obligation.

Investment Framework