HIMS: After the GLP-1 Wave

The pivot is real, the cost is steep — and the verdict is split

Hims & Hers built one of the fastest revenue ramps in consumer health history by riding compounded semaglutide through the Ozempic shortage. The FDA ended that game. Now the company is executing a painful pivot to branded GLP-1s from Novo Nordisk and Eli Lilly — while trying to prove its core business in sexual health, hair loss, and mental health is enough to justify a multi-billion dollar valuation. Q1 2026 gives us the first clean look at what that transition actually costs.

Q1 2026 · Scorecard

The Numbers: A Miss That Tells a Bigger Story

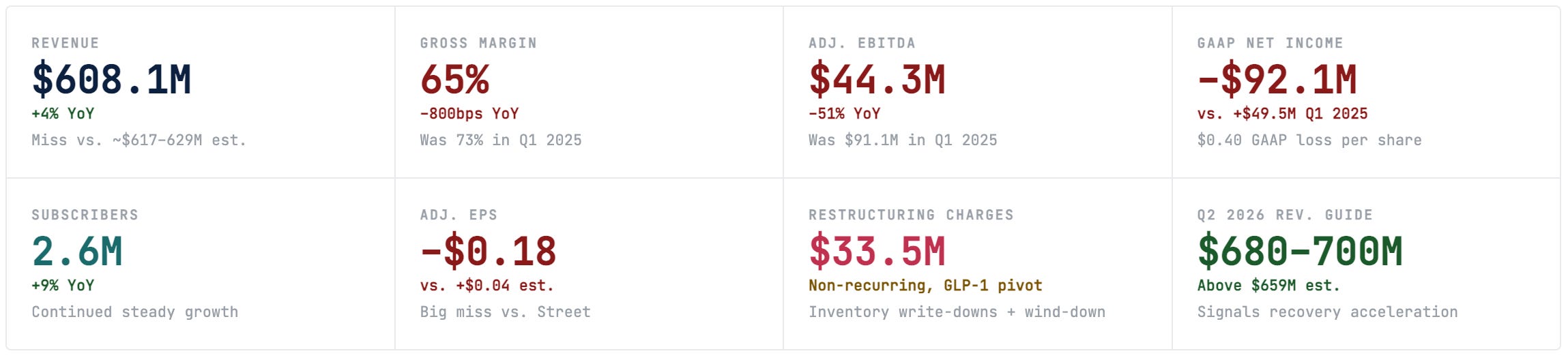

On the surface, Hims & Hers’ Q1 2026 results look like a modest disappointment: revenue of $608.1 million came in roughly $9–21 million below Wall Street’s range, adjusted EPS swung from +$0.04 expected to –$0.18 reported, and the company’s net income turned into a $92.1 million loss. Shares fell 11.5% in extended trading.

But the raw numbers obscure what is genuinely one of the most complex business pivots in recent consumer health history. Strip out $33.5 million in non-recurring restructuring charges tied to the weight-loss offering shift, $17.6 million in fair-value losses on liabilities, and $9.7 million in equity securities markdowns, and the underlying business loss is considerably narrower. The real issue isn’t one bad quarter — it’s whether the business that emerges from this transition can recapture the revenue momentum the GLP-1 wave created.

The Key Number to Understand

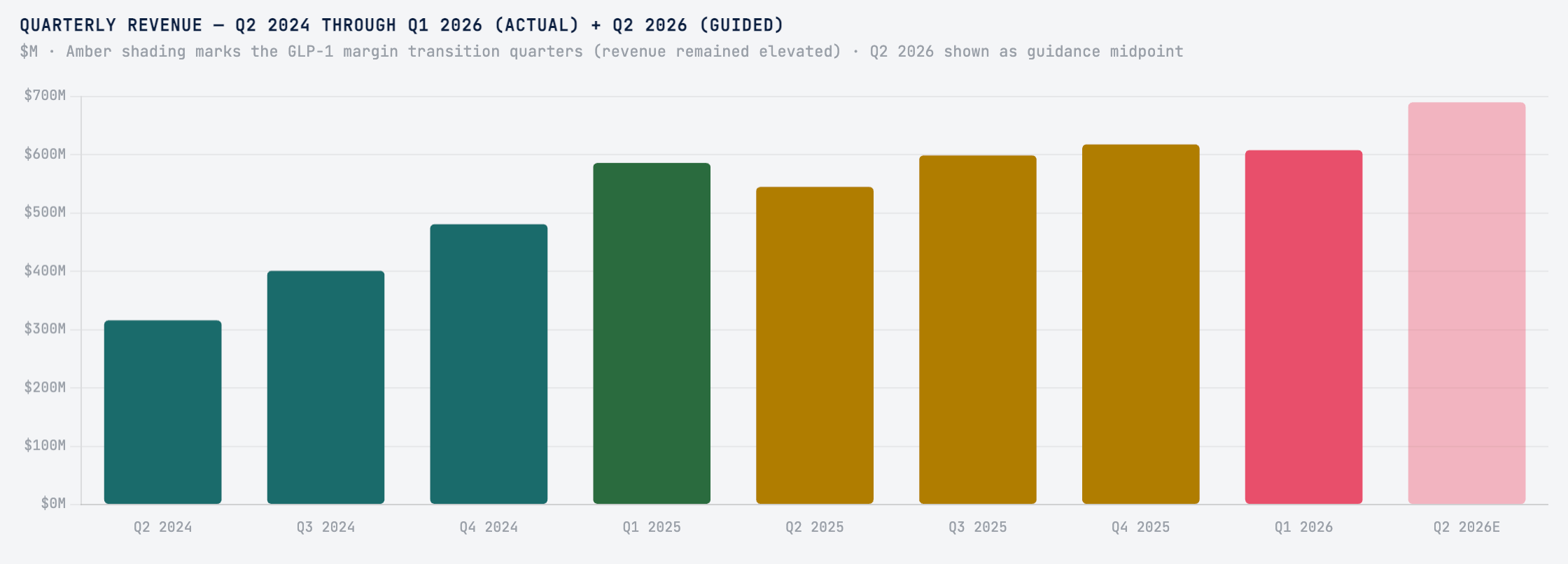

The +4% revenue growth in Q1 2026 compares against a Q1 2025 that itself grew +111% year-over-year. The compounded semaglutide business was the primary engine of that ramp. As that revenue rolls off — and the company transitions to lower-margin branded GLP-1 distribution — the top-line math becomes unfavorable in the near term even as the Q2 guidance suggests acceleration. This is a transition quarter, and the Street is paying full price for it.

GLP-1 Compounding · The Full Story

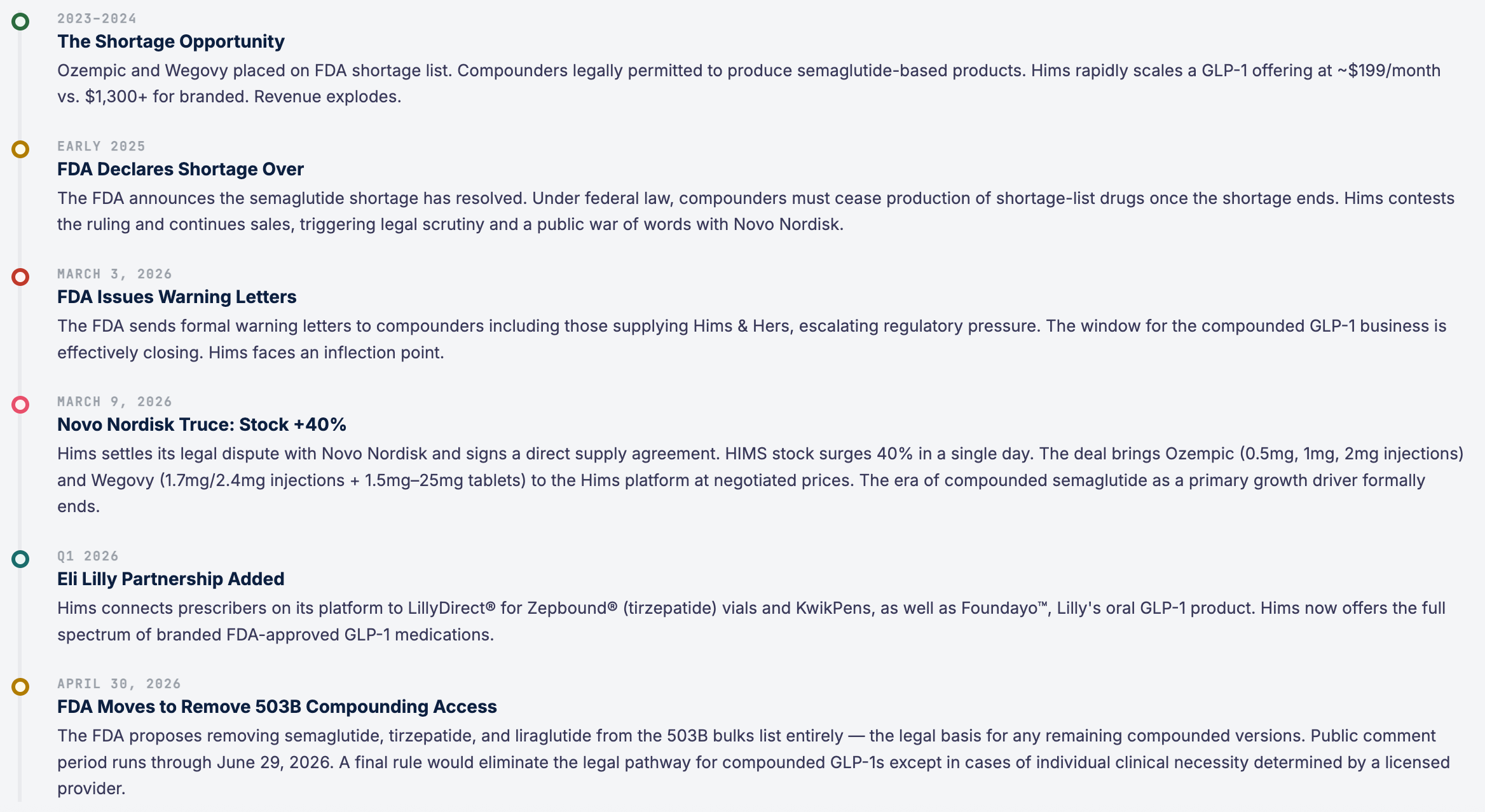

From Shortage to Shutdown: The Rise and Fall of Compounded Semaglutide

To understand what’s happening at Hims & Hers, you have to understand the most consequential regulatory loophole in recent pharmaceutical history. When Novo Nordisk’s Ozempic and Wegovy faced chronic supply shortages in 2023–2024, the FDA placed semaglutide on its drug shortage list. That designation unlocked a provision allowing compounding pharmacies to manufacture and sell semaglutide-based products without the normal FDA approval process.

Hims & Hers moved faster than anyone. The company built a direct-to-consumer funnel — telehealth visit, prescription, compounded semaglutide injection, delivered to your door — and priced it well below the $1,300+ monthly list price of Wegovy. In 2024 and into Q1 2025, GLP-1-related offerings drove an enormous share of the company’s revenue growth, which hit 111% year-over-year in Q1 2025. It was the single most effective growth engine any telehealth company had ever found.

Then the FDA moved. And everything changed.

The Regulatory Overhang Is Not Fully Resolved

As of May 11, 2026, the FDA’s 503B bulks rulemaking is still open for comment through June 29. A final rule removing semaglutide, tirzepatide, and liraglutide from the list would make it substantially harder — and legally riskier — to provide any compounded GLP-1s, even for clinical necessity cases. Hims has indicated it will continue to offer compounded products where providers deem them clinically necessary, but the legal and commercial ground beneath that carve-out is narrowing. Investors should watch the FDA’s final rule, expected later in 2026, as a potential binary event for any remaining compounded revenue.

“As we exit the first quarter, our domestic business is accelerating, we’re expanding into new categories and countries, and more people than ever are relying on us for access to personal, data-driven care.”

— Andrew Dudum, CEO, Hims & Hers Health · Q1 2026 Earnings Call

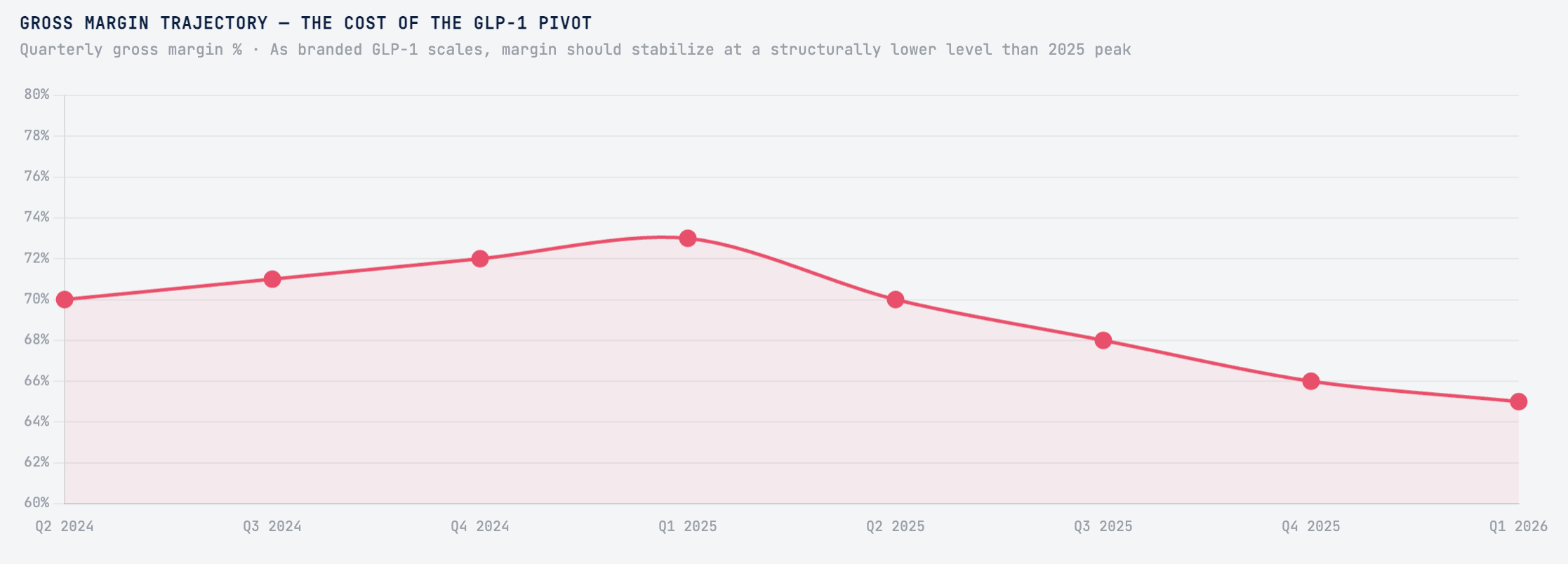

The strategic pivot itself is correct — branded GLP-1s are a far more defensible business than compounded medications whose legal status was always contingent on a drug shortage. But the financial reality of the transition is harsh. Compounded semaglutide carried high gross margins because Hims controlled the formulation, supply chain, and pricing. Distributing branded Novo and Lilly products makes Hims a middleman — earning a transaction or referral spread rather than product economics. That is why gross margin fell from 73% to 65% in a single year, and it could fall further as branded volume scales.

Business Analysis · Beyond GLP-1

The Underlying Platform: Is It Enough Without Weight Loss?

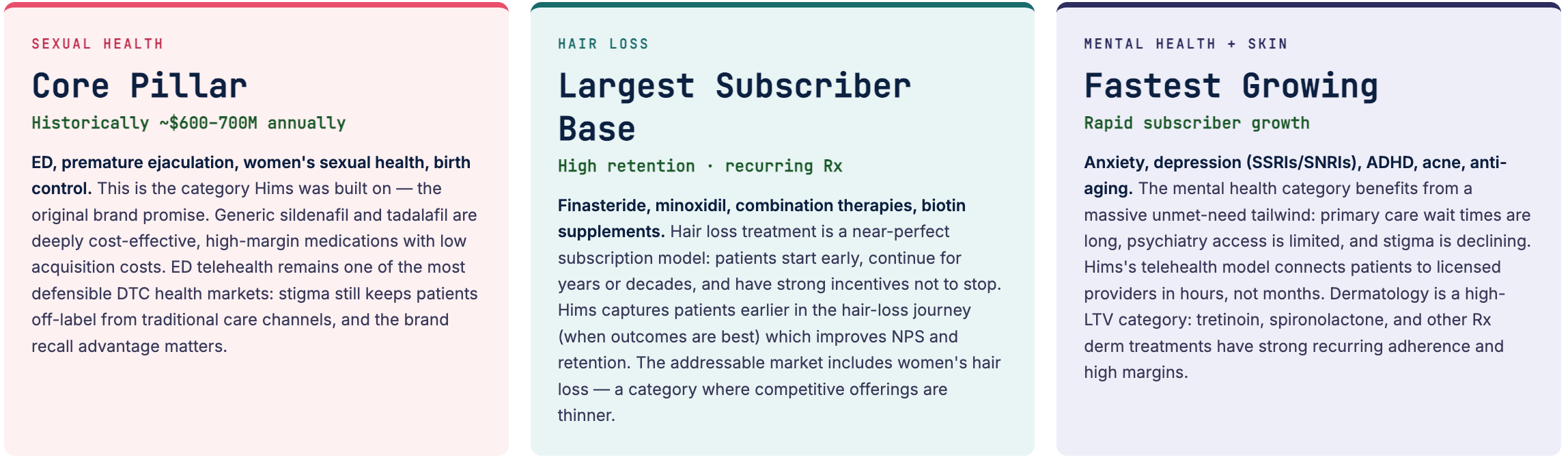

Before GLP-1 became a household conversation, Hims & Hers was building a quietly formidable direct-to-consumer healthcare business around three durable categories: sexual health (primarily ED medications and women’s sexual wellness), hair loss (finasteride, minoxidil, prescription and OTC combinations), and mental health (primarily anxiety and depression treatments via telehealth). These categories don’t have drug-shortage wildcards. They are structurally growing markets with high treatment adherence and strong recurring revenue characteristics.

The company does not break out revenue by category in its press releases, but management commentary and SEC filings indicate that these three legacy pillars, combined with skin/dermatology, remain the majority of revenue by subscriber count if not yet by dollar volume. With 2.6 million total subscribers growing at 9% year-over-year, the platform retains strong engagement — the GLP-1 noise obscures what is actually a well-run subscription health business.

The Case for the Platform

The 2.6 million subscriber count growing at 9% year-over-year tells a different story than the revenue deceleration. Subscribers are the leading indicator; revenue per subscriber is where the mix shift shows up. As the GLP-1 weight-loss product suite transitions from high-margin compounded to lower-margin branded — but higher-volume — the platform’s breadth across categories provides natural diversification. No single FDA ruling can close down the hair or mental health businesses.

What Hims is building, if management’s vision executes, is the Costco of consumer health — a subscription platform where the membership relationship drives cross-sell across a wide catalog of clinical services. The average subscriber who starts with hair loss often adds ED treatment. The patient who starts with anxiety meds may eventually enroll in the GLP-1 program. The unit economics of cross-selling within a subscribed user base are vastly superior to customer acquisition for each discrete condition.

Guidance · Profitability Path

Can the Numbers Work After the Pivot?

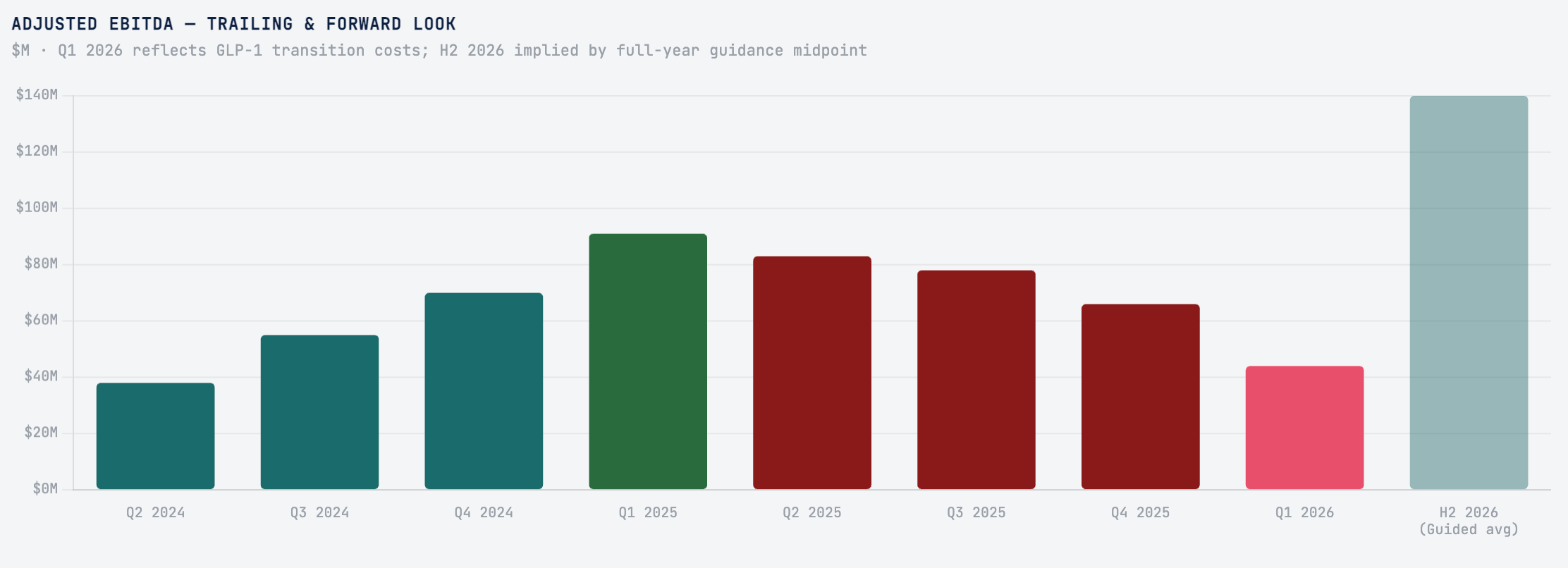

Management’s Q2 2026 revenue guidance of $680–700 million is the most important datapoint in this earnings release. It is $21–41 million above the Wall Street consensus of ~$659 million and implies a significant sequential acceleration from Q1’s $608 million. If Hims can hit even the low end of Q2 guidance, it would suggest that the GLP-1 restructuring charges are indeed one-time and that the branded drug distribution model, combined with continued core business growth, is creating a new growth baseline.

The full-year 2026 guidance of $2.8–3.0 billion implies average quarterly revenue of $700–750 million through the back half of the year. That is a meaningful step-up from Q1, and management has also guided adjusted EBITDA of $275–350 million for the full year — implying margins recover as the restructuring costs fade. At the midpoint, that’s approximately $312 million in EBITDA on roughly $2.9 billion of revenue, or an EBITDA margin of about 11%.

The Path to GAAP Profitability Is Still Unclear

Hims & Hers achieved GAAP net income of $49.5 million in Q1 2025 — a genuine milestone at the time. The swing to a $92.1 million net loss in Q1 2026 is partly non-recurring, but it highlights how dependent the income statement is on mix effects. As branded GLP-1 distribution scales with thinner margins, and as the company invests in international expansion and new categories, GAAP profitability may not return until 2027 at the earliest. The EBITDA guidance of $275–350 million is encouraging but is not the same as GAAP earnings.

The longer-term trajectory that management is selling: a consumer health platform generating $3+ billion in revenue by 2027, expanding into Europe and new clinical categories, and leveraging data from 2.6+ million subscribers to personalize care in ways no traditional healthcare system can match. It is an ambitious vision. It is also the same vision they were selling in 2024 — before the GLP-1 wave temporarily made the numbers look easy.

Investment Case

Bull vs. Bear: Hims & Hers After the Pivot