Lucid: Will They Make It?

Runway, Saudi Backing, and the Economics of Survival

Executive Summary

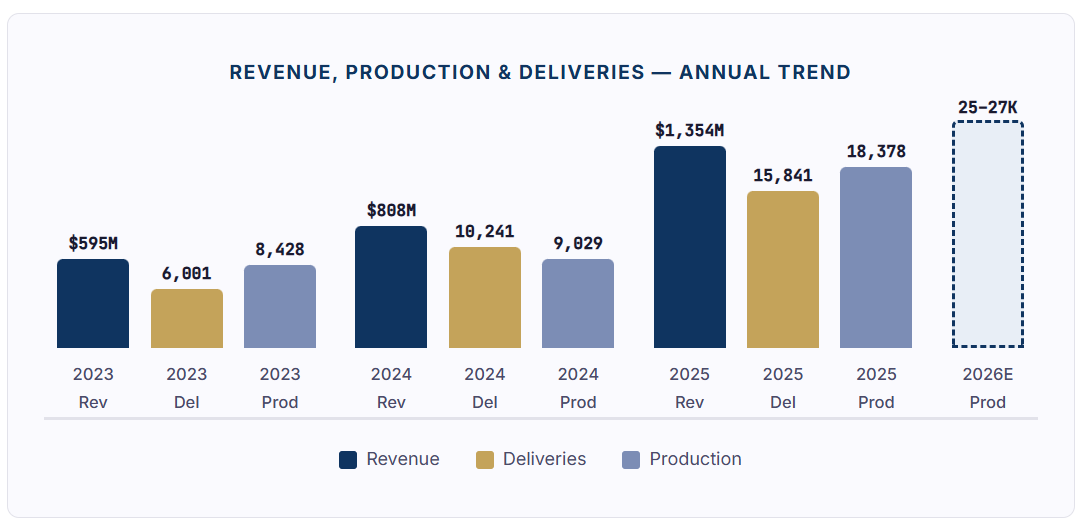

Lucid Group enters 2026 in a deeply paradoxical position. The company produces what many consider the most technologically advanced electric sedan on the market, has launched its Gravity SUV to meaningful early demand, and is backed by Saudi Arabia’s Public Investment Fund with over $9 billion in cumulative capital. It has $4.6 billion in total liquidity, a 2026 production target of 25,000–27,000 vehicles, and has just unveiled a midsize platform that could expand its addressable market by an order of magnitude.

And yet: Lucid burned $3.8 billion in free cash flow in 2025, carries a gross loss of over $1.2 billion, and has never been within sight of profitability. Its market capitalization sits near $3.3 billion — below its annual cash consumption. Manufacturing cost per vehicle is falling, but remains deeply negative on a unit-economics basis. The question is no longer whether Lucid makes good cars. The question is whether the company can survive long enough, with enough capital and enough demand, for its product ambitions to become a real business.

This report provides a detailed, institutional-grade analysis of Lucid’s runway, capital structure, Saudi dependence, geopolitical exposure, and operational milestones. Our central finding: Lucid likely has sufficient liquidity into H1 2027 under current burn rates, but will almost certainly require another major capital infusion before year-end 2027. The critical variable is not product quality — it is whether the rate of operational improvement can outpace the rate of capital consumption.

Key Takeaways

Liquidity is real but finite. $4.6B in total liquidity at year-end 2025 sounds comfortable, but against $3.8B in annual FCF burn, the runway is roughly 14–18 months without improvement or new funding.

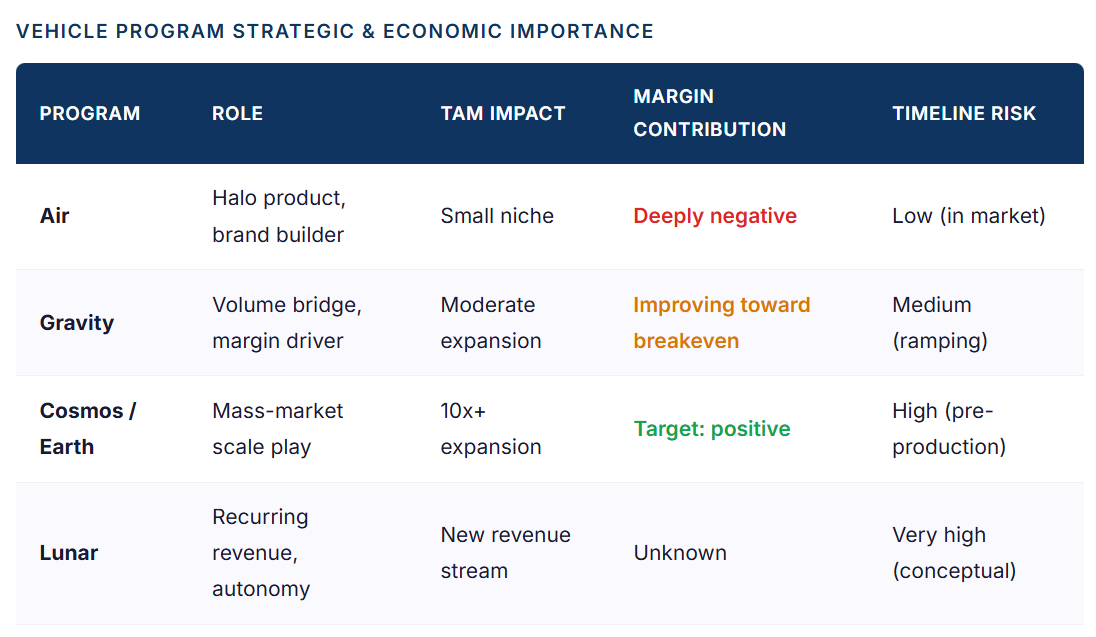

Gravity is the bridge. The SUV is Lucid’s most commercially important product. If it ramps successfully, it accelerates the path to gross-margin breakeven. If it stalls, the funding wall arrives faster.

Saudi support is strategic, not unconditional. PIF views Lucid as a Vision 2030 asset, but the fund cut portfolio spending by 20%+ in late 2024 and is now navigating wartime capital reallocation. Support is likely to continue — but not automatically and not at any price.

Gulf conflict is a double-edged variable. Higher oil prices may improve Saudi fiscal capacity, but PIF’s strategic priorities are shifting toward defense and food security. Lucid is not guaranteed to benefit from oil-price windfalls.

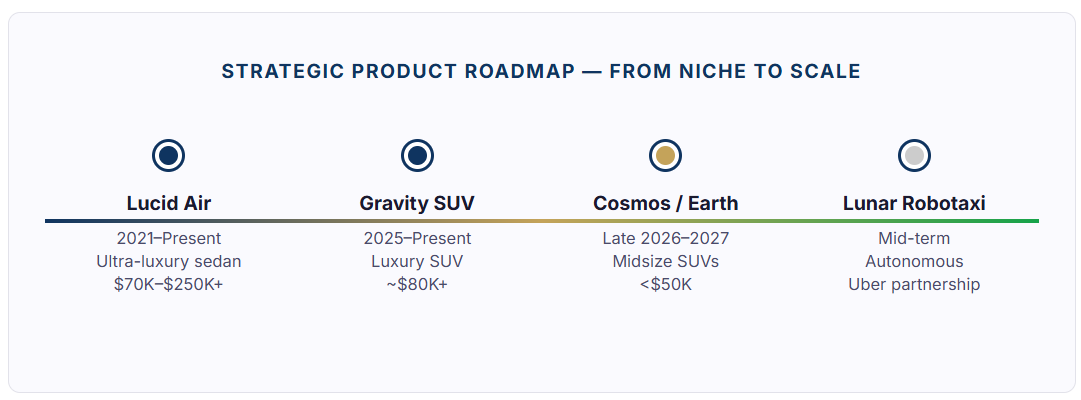

Midsize is the real endgame. Cosmos and Earth, priced under $50,000, could transform Lucid’s volume economics — but production doesn’t begin until late 2026 or early 2027, and scale is years away.

This is a runway-and-execution story, not an EV growth story. Lucid’s investment case is about capital duration — how long the funding lasts, how fast the burn declines, and whether the product pipeline converts into economic self-sufficiency before the next funding wall.

I

Why Lucid Is Still a Live Question

In the universe of post-SPAC electric vehicle companies, most have already answered the fundamental question of viability. Lordstown is gone. Fisker is bankrupt. Canoo and Arrival are footnotes. Among startups that actually produce and sell vehicles at meaningful scale, the list is vanishingly small: Rivian and Lucid are the names that remain, and both are still far from self-sustaining.

What makes Lucid unusual — and why it remains an active debate among institutional investors — is the gap between its technological credibility and its commercial fragility. The Lucid Air has won nearly every comparison test against competitors. Its powertrain efficiency remains best-in-class. The Gravity SUV, despite early supplier-driven production hiccups, has generated strong demand signals. And the recently unveiled midsize platform, with its Cosmos and Earth models priced under $50,000, represents a credible path to mass-market relevance.

But none of that changes the arithmetic of a company that burned $3.8 billion in free cash flow last year while generating $1.35 billion in revenue. The core debate about Lucid has shifted decisively from product quality to financial survival. It is no longer a question of whether Lucid can build a competitive car. It is a question of whether the company can survive long enough — through capital infusions, operational improvement, and sheer strategic persistence — for Gravity, the midsize platform, and Saudi-backed scale to become a durable business rather than a permanently deferred promise.

II

What the Latest Results Actually Show

Lucid’s Q4 2025 and full-year results tell a story of meaningful operational progress layered atop continuing financial distress. Revenue for Q4 reached $522.7 million, up 123% year-over-year, driven by Gravity deliveries and higher throughput. Full-year 2025 revenue of $1.354 billion represented 68% growth over 2024 — the strongest annual top-line performance in the company’s history.

Production reached 18,378 units for the full year (with a year-end restatement to ~17,840 after adjusting for validation completions), nearly doubling 2024’s 9,029 units. Deliveries of 15,841 vehicles represented 55% growth. Manufacturing cost per vehicle declined approximately 27% year-over-year, with management guiding for an additional 20% reduction by Q4 2026. Importantly, roughly $10,000 per unit in tariff-related costs in 2025 is not expected to recur.

But the financial picture remains deeply challenged. The full-year gross loss exceeded $1.2 billion — Lucid is still spending substantially more to build each car than it receives in revenue. The adjusted EBITDA loss was $2.79 billion. GAAP net loss per share was $(12.09). Free cash flow was negative $3.8 billion for the year, including $1.24 billion in Q4 alone. Operating expenses of $643 million in Q4 included $361 million in R&D and $282 million in SG&A — spending levels that reflect a company still investing aggressively in future platforms while losing money on every vehicle shipped today.

The improvement is real. The gap between what Lucid spends and what it earns per car is narrowing. But the absolute scale of losses is such that even rapid margin improvement does not eliminate the funding imperative for years to come.

III

How Long Is the Runway?

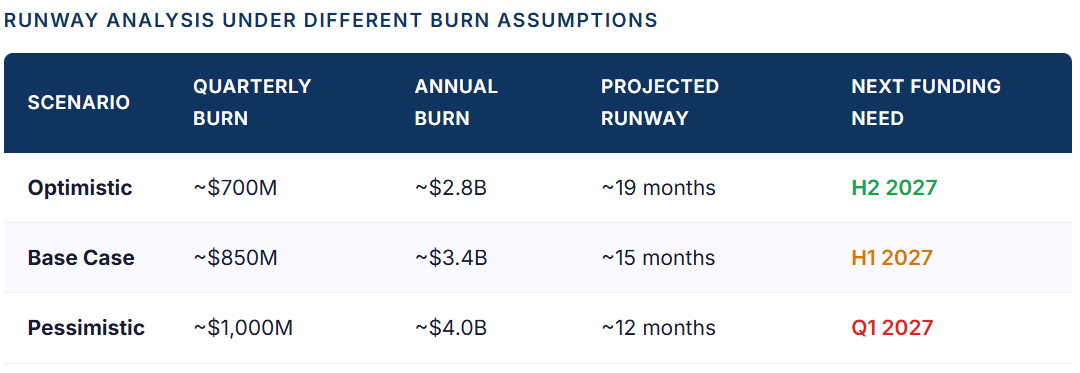

Lucid ended 2025 with approximately $4.6 billion in total liquidity, comprising roughly $998 million in cash and cash equivalents, short-term investments, and approximately $2.5 billion in undrawn committed facilities. This is a meaningful liquidity buffer — but it must be evaluated against the scale of the company’s cash consumption.

In 2025, Lucid consumed $3.8 billion in free cash flow. Even adjusting for one-time items and ramp-related inefficiencies, the underlying quarterly burn rate in Q4 was approximately $1.24 billion. If we assume moderate improvement in 2026 — say a quarterly burn rate declining to $800–900 million as Gravity scales, cost-per-vehicle drops 20%, and the workforce reduction begins to yield its targeted $500 million in cumulative savings — Lucid would still consume roughly $3.2–3.6 billion in cash during 2026.

Under a base-case scenario, this implies liquidity exhaustion in H1 2027, consistent with management’s implicit guidance that current resources support operations into that timeframe. Under a more optimistic scenario where Gravity ramps strongly, gross margins approach breakeven, and burn declines more sharply, the runway could extend into H2 2027. Under a pessimistic scenario — production hiccups, demand softness, or margin stagnation — the funding wall could arrive as early as Q1 2027.

Why Reported Liquidity Is Not Strategic Flexibility

A $4.6 billion liquidity figure sounds comfortable in isolation. It is not. Auto manufacturing requires substantial working capital buffers for supplier commitments, raw material procurement, and production continuity. Lucid cannot spend down to zero and remain a going concern — the company needs to maintain a meaningful minimum liquidity threshold (likely $1.5–2.0 billion) to sustain operations, honor supplier agreements, and retain market confidence. The practical “spendable” runway is therefore considerably shorter than the headline number implies.

Analytical Insight

Lucid is best understood as a runway-and-execution story, not simply an EV growth story. The central investment question is not about top-line growth rates or vehicle quality — it is about whether the rate of operational improvement can outpace the rate of capital consumption before the next funding wall arrives. Every quarter of margin improvement buys additional months of independence. Every quarter of stagnation accelerates the dependence on external capital.

IV

Demand, Deliveries, and the Gravity Question

Lucid’s commercial challenge has always been the tension between product excellence and addressable market size. The Air sedan, priced primarily above $70,000 and competing in the ultra-luxury segment, faces a naturally constrained buyer pool. Growth in deliveries has been meaningful — 55% year-over-year — but the absolute numbers remain small by automaker standards. At roughly 16,000 annual deliveries, Lucid produces fewer vehicles in a year than Toyota builds in a few hours.

The Gravity SUV changes this equation, but how much depends on execution. Early signals have been positive: Lucid has reported strong reservation interest and accelerated production after resolving initial supplier constraints. As an SUV priced from approximately $80,000, Gravity addresses a substantially larger market segment than the Air sedan — SUVs represent over 50% of the U.S. luxury market. Gravity’s contribution is already visible in Q4 results, where its mix helped drive the 123% revenue increase and the 18-point sequential improvement in gross margin.

But Gravity alone does not solve the volume problem. Even at the high end of 2026 production guidance (27,000 units), Lucid remains a niche manufacturer. The real strategic inflection comes with the midsize platform — the Cosmos and Earth models, priced under $50,000 — which would place Lucid in direct competition with the Tesla Model Y, Hyundai Ioniq 5, and other mainstream EVs. At Lucid’s March 2026 investor day, the company outlined production starting at AMP-2 in Saudi Arabia by late 2026 or early 2027, with full capacity expected by 2029.

This is the strategic crux: Gravity is the bridge between the ultra-luxury niche and commercial viability, while the midsize platform is the destination. The question is whether Lucid can cross the bridge without running out of fuel.

V