Mercadolibre: The e-commerce leader in Latam

Mercadolibre: The e-commerce leader in Latam

… but would you invest your money long-term in a bank from Argentina?

Mercadolibre is a e-Commerce company focused on the Latin America region. A company that has started to grow rapidly in recent years, but a company that is not new at all. The company is almost as old as Amazon, it was founded in 1999, it started as something in the middle of an eBay and an Amazon. It was a platform where sellers could post their products but with fixed prices. In some countries, like Central American countries, they still operate this way. This was never a huge market for them, and you can see it with how they are still pretty much non-existent in Central America. In big countries in Latin America like Mexico, Brazil and Argentina they have invested heavily in becoming more like Amazon. Where they have all the fulfillment infrastructure. The company is an Argentinean company but headquartered in Montevideo Uruguay. Which is pretty much typical Argentine, considering the very lousy past 20 plus years in terms of economic performance. The company has been a late grower, it was stuck in about sub $4b valuation for years, it was until 2017 that they have started to really grow, and have reached highs of close to $100b, if you invested since its IPO and you are still there in 2022, congratulations, they patience you had from 2007 to 2016 of lousy returns is pretty impressive. Today the company looks like a future star, a company that will dominate the latin american e Commerce landscape. We will have an in depth look into the company to better understand the future years and how the past 3 to 5 years have gathered this impressive growth.

Business Model:

Revenue Streams & Operational Model:

Currently the company has 6 main business units or 6 main revenue streams. They have been launched over the years and some have been present for almost as long as the company but have evolved and adjusted to today's world

Marketplace

Currently available in 18 markets, but it is very different from country to country.

They offer very similar services to what you would think today of a traditional e-commerce marketplace including the delivery and fulfillment center infrastructure, with also big stores selling on their platform in the following countries:

Argentina

Brazil

Mexico

Uruguay

Colombia

Chile

Peru

Venezuela

Ecuador

They offer a lower grade marketplace that looks a lot more like a good looking version of craigslist than a real marketplace. This is what the origin of Mercadolibre looked like in all countries at the beginning. A marketplace that looks a lot more like classifieds in the newspaper. With that model it is very difficult to install trust on the general public. One clear example on how this Craigslist type of market is still not a serious market is the fact that you can buy puppies from them, that is right, you read that right, puppies. God knows what else you can get from this ‘’Marketplace” (You can see this also in established marketplaces like Mercadolibre México, but it is a lot more visible in the classified versions, the more their e-commerce platforms penetrate the market, the more this type of sellers will have to disappear)

We could say that this part of their business is a very marginal revenue generator as of now, the good thing for them is that they already have a presence there and could eventually become a real e-commerce market. Central America and the Dominican Republic, for example, together are close to 60 million people. The countries where they currently operate this craigslist esque model are:

Guatemala

El Salvador

Nicaragua

Honduras

Costa Rica

Panama

Dominican Republic

Bolivia

Paraguay

Mercado Envios

A logistics solution that enables sellers on their platform to utilize third-party carriers and other logistics service providers, while also providing sellers with fulfillment and warehousing services.

Sellers that opt into the logistics solutions are able to offer an integrated shipping experience to their buyers at competitive prices, but are also eligible to access shipping subsidies to offer free or discounted shipping for many of their sales on Mercadolibre’s Marketplaces

Envios works like this:

Print shipping tag

Prepare package

Take Package to distribution point. (This has to happen as soon as possible after the sale is received in order to avoid having a negative effect on the seller reputation)

It includes the following benefits:

“Faster payment”: Money is released from 2 to 6 days after the product is delivered (2 days if the reputation of the seller is “good” and the product being sold is new. If there is no reputation or the product is used the money will be released after 6 days)

Mercado Libre protects all deliveries. If anything happens, they cover it

Package tracking, for customer and for the seller

No need to coordinate delivery, customer will do that on the website and have the payment done with MercadoPago

Improved Reputation, it is basically the better they serve the customers the better reputation they will have

Mercado Envios covers all products that can be sent via mail and that are under the maximum package size that each mail delivery provider accepts. Mercado envios also offers discounts for sellers depending on the reputation they have.

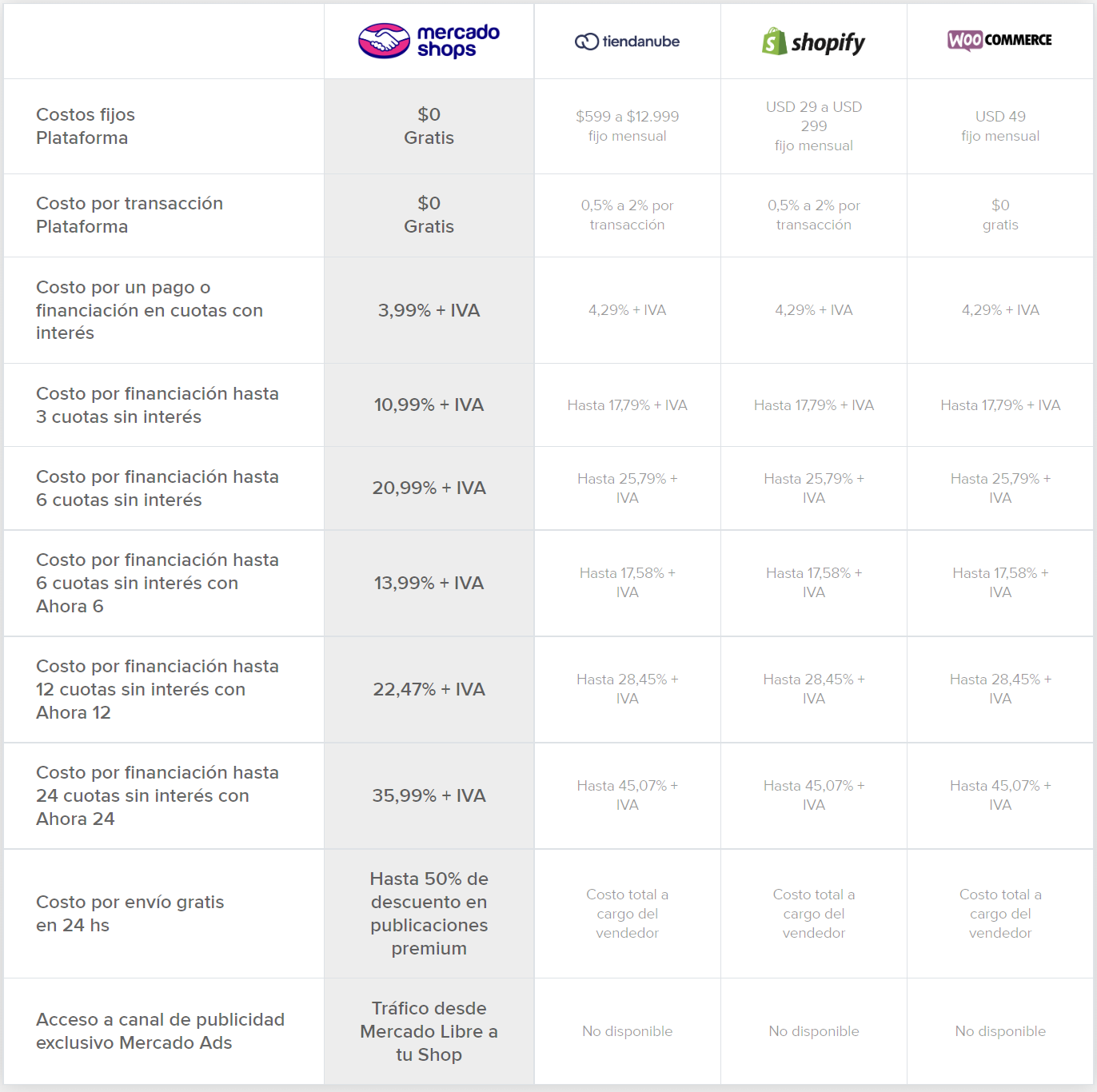

Mercado Shops

Allows users to set up, manage and promote their own digital stores. These stores are hosted by Mercado Libre and offer integration with the rest of their ecosystem, namely the Marketplaces, payment services and logistics services. Users can create a store at no cost, and can access additional functionalities and value added services on commission.

This is their solution that compares with products offered by Shopify and the like. They claim to offer 0 cost for platform use and 0 cost per transaction, better financing rates and discounts of shipping.

Mercado Pago

They generate fees attributable to:

Commissions that are charged to sellers representing a percentage of the processed payment volume in connection with off-Marketplace transactions

Commissions from additional fees they charge when a buyer elects to pay in installments through their Mercado Pago platform for transactions that occur either on or off their Marketplace

Commissions from additional fees they charge when their sellers elect to withdraw cash;

Commissions that they charge from transactions carried out with MercadoPago credit and debit cards

Cash advances and fees from merchant and consumer credits granted under their Mercado Credito solution

Interchange fees from the transactions on their issued cards

Insurtech fees and revenues from the sale of MPOS devices

Mercado Pago is both for customers and merchants. It gives merchants different ways to get paid, POS, QR codes, online link, integrated checkout as well as subscription services.

They also recently launched crypto in Brazil on their wallet app, offering the possibility to trade Ethereum, Bitcoin and a Stable Coin. They use a third party for all blockchain infrastructure and they act mostly as a distributor.

Mercado Credito

Give customers the possibility of paying for items in up to 12 installments. Depends on each customer but as an example they give up to 15K pesos in Argentina. Interest rates are very high in a country like Argentina, given the macroeconomic situation in that country, but their rates move with each country’s situation.

Mercado Ads

Enables businesses to promote their products and services on the internet. Through their advertising platform, brands and sellers are able to display ads on their websites through product searches, banner ads or suggested products. Their advertising platform enables merchants and brands to access the millions of consumers that are on their Marketplaces at any given time with the intent to purchase

Key Metrics / Performance

Revenue and Key KPIs

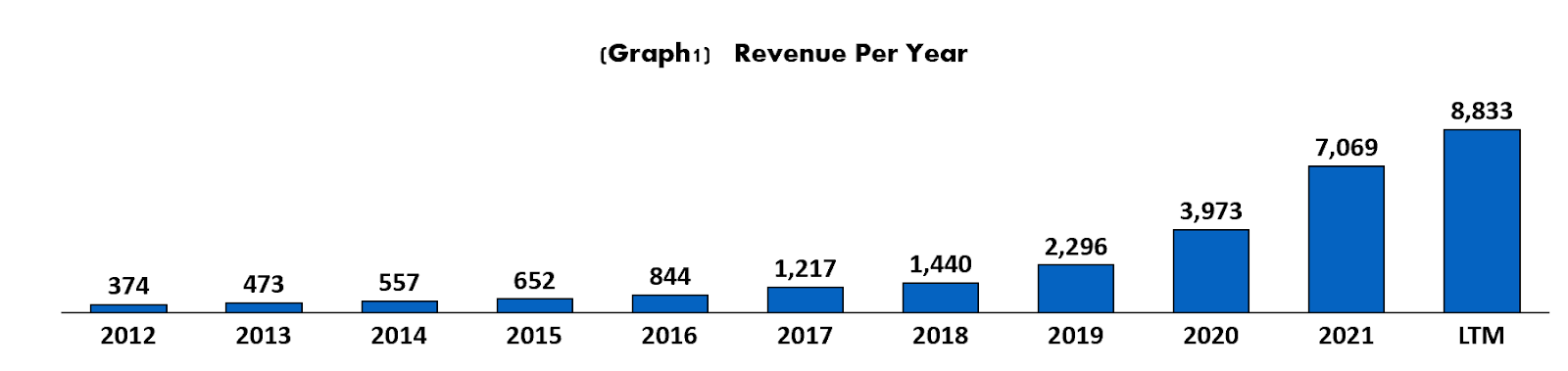

If when looking at MercadoLibre you start by looking at their recent growth percentages you would think that you are looking at a startup, in a way it kind of is, but the company has been around for a while and was not until 2017-2019 that it actually began growing with a convincing pace.

This is mainly related to the region, Latin America is a region that is a bit behind the curve in terms of e-commerce and digitalization of the economy. MercadoLibre before had products that were more similar to classifieds than Amazon. They have changed over the last few years and now they are becoming the “Amazon” of the most populated countries in South America.

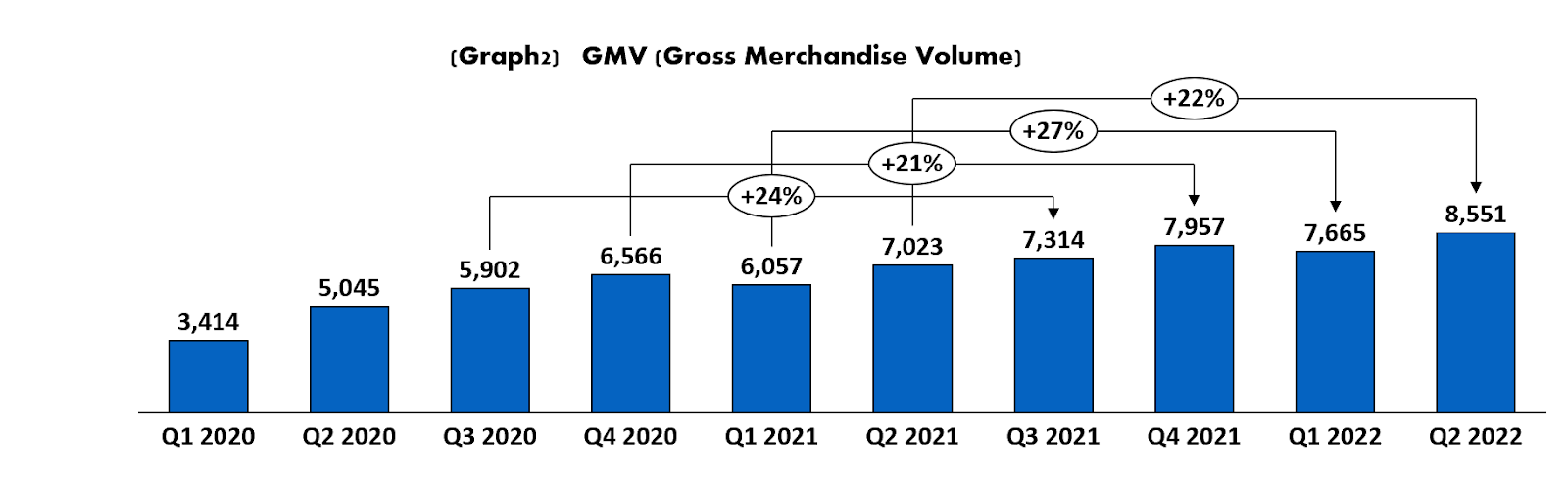

Revenue over the quarters has seen strong growth, last quarter Mercadolibre grew by 52% YoY while they have many business units, their business could be summed up in commerce revenues and fintech revenues. Commerce revenues have been slowing down for the past couple of quarters. This could be justified considering that most of the e-commerce companies saw a huge increase in revenues during the pandemic.

On the fintech side of the company as opposed to Commerce the revenue is still accelerating. Reaching 113% YoY growth last quarter.

Commerce Revenues

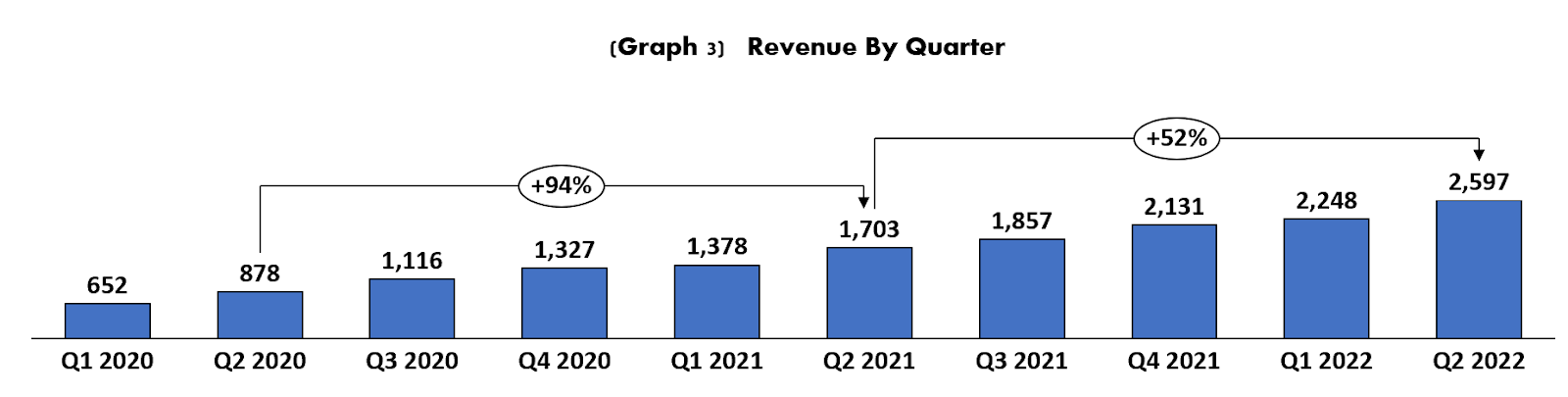

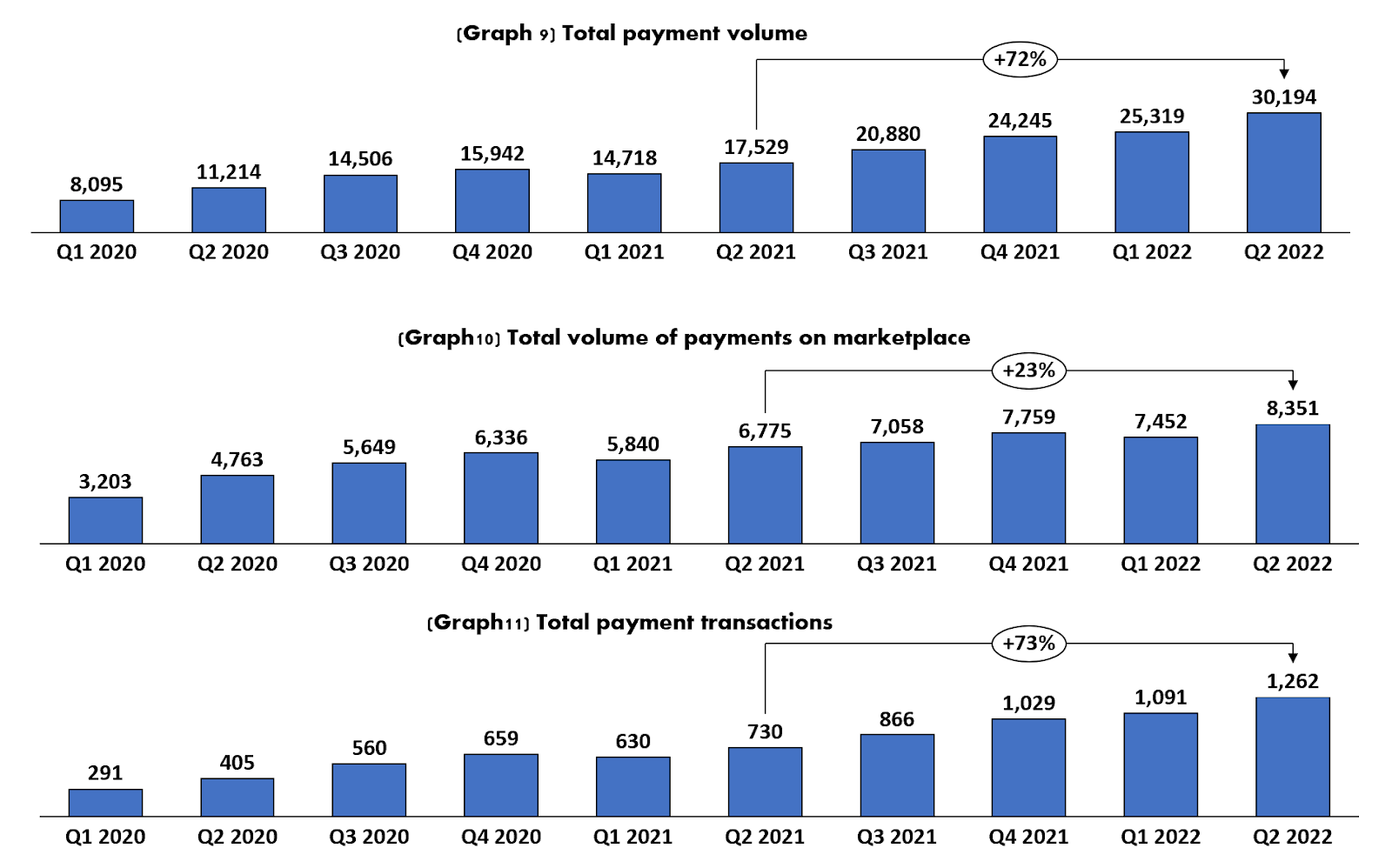

This is a company that is similar but different to the traditional e-commerce player. It is somehow a mix of an uber and an amazon, or an Airbnb and Amazon. They are in some ways a platform. There is a great amount of their marketplace volume that is sold by third party stores. Big stores, imagine for example Best buy or Macy's etc selling through their platform. Given this model you will see that they report a KPI that is very common on platforms like Uber or Airbnb. This KPI is GMV, (Gross Merchandise Volume) the total list value of what is sold in the platform. They had their best GMV quarter to date last quarter and have $31.4b over the last 12 months.

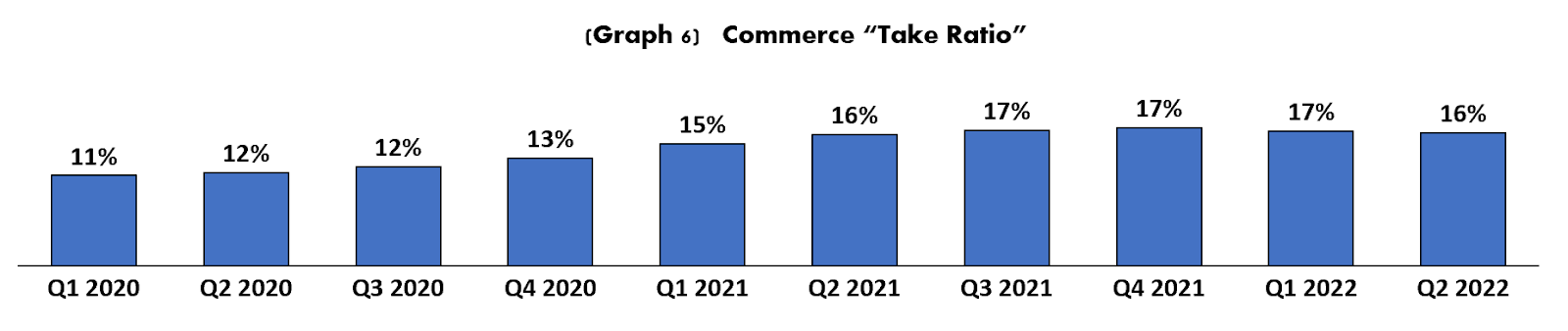

If we take the revenue from commerce and the GMV we can get a calculated take ratio of Mercado Libre. We call it a calculated take ratio because it is not 100% a take ratio like something you could see from an Uber or an Airbnb. Since there are some items that are sold by third parties and some by Mercadolibre, it could be something like a proportion of commerce volume that Mercadolibre takes in revenue. What we see over the last 10 quarters is that this is improving a lot, it has reached decisively the teens, it has remained at around 16%-17% since Q2 2021.

When it comes to price per item sold, they have nearly recovered their previous level from before the pandemic. Each item sold averaged $31 in Q2 2022 vs $32 in Q1 2020. It seems though that it has proven difficult for them to increase this average, what they have done pretty well is nearly triple the amount of items sold since the start of the pandemic. The pandemic accelerated many years in the adoption of e-commerce activity in Latin America, a case of being there at the right time for Mercadolibre.

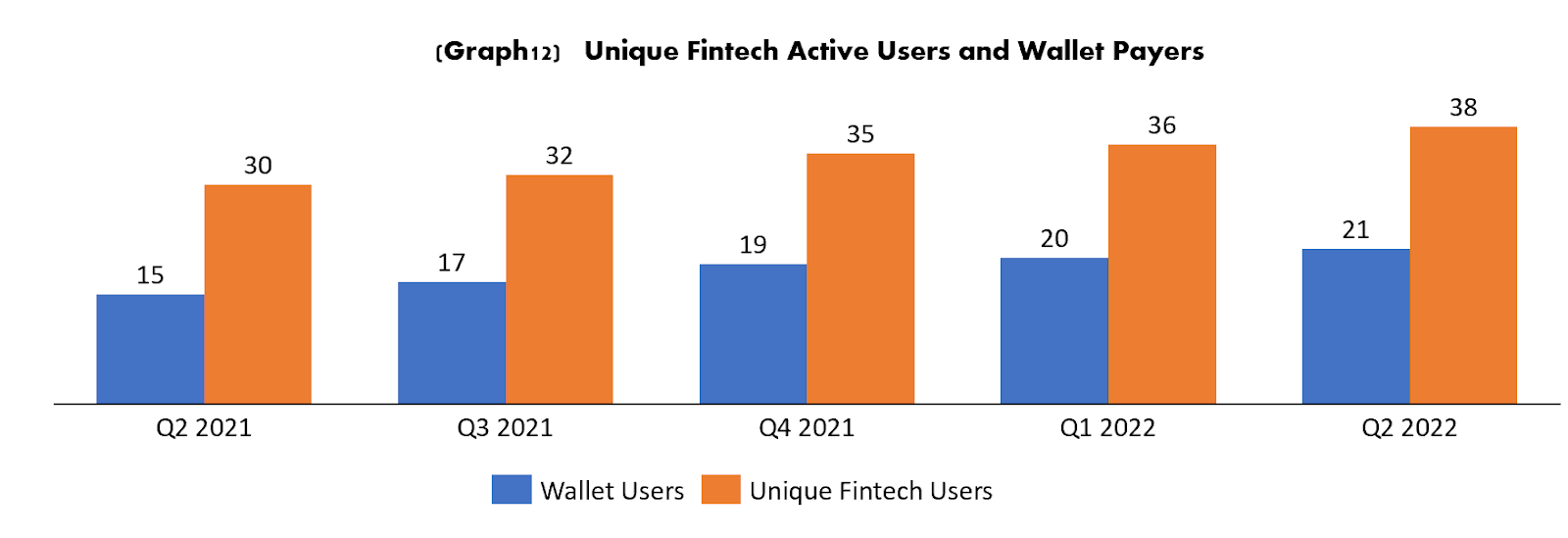

Fintech Revenues

Fintech is the up and coming business for Mercado Libre, this side of the business has not peaked and it is still accelerating every month. During Q2 they achieved a new record in payment volume adding up to $30b. They use their market place as the main way to penetrate their wallet on customers, but volume in the market place was only $8.3b , which shows great success of the company on making it a product that is actually used more outside their marketplace than inside. Also it is very clear that the payment outside the marketplace is growing at far greater speeds, total volume grows at 72% while marketplace only grows at 23%, and this being the fastest growing business for Mercadolibre, it is very clear that their biggest growth generator is outside their marketplace. Dollar amount per transaction is going down, it has gone from $27.84 in Q1 2020 to $23.93 today. Again showing that the transaction and volume growth is outside the marketplace, the transactions outside the platform are usually smaller, for everyday purchases like a small coffee or a regular lunch, while transactions on the market place are usually devices or something with a ticket a bit more expensive, as they continue to grow outside transaction we would expect this to continue going down if they continue to take the role of cash, or every day expense.

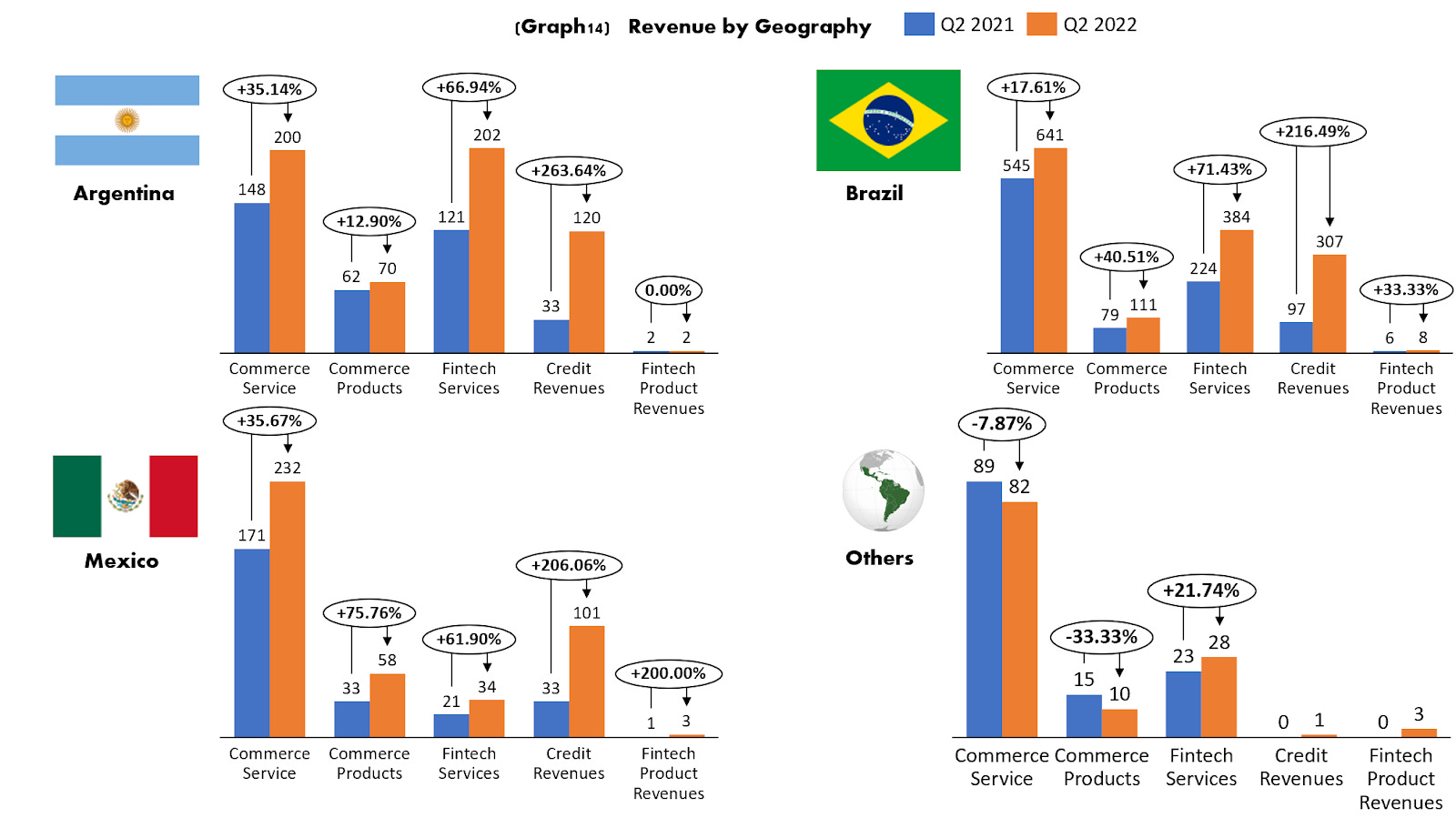

Geographies

Brazil is by far their biggest market, making up 55% of their revenues over the last 12 months. This goes in line with the fact that Brazil is the most populous country in Latin America. Mexico would be the second most populous country in Latin America but is yet to become the second biggest market for Mercadolibre. That place is taken by Argentina. Mercadolibre’s executive team has good hopes on Mexico becoming a more important market for them, the opportunity is there, but also competition is a lot more complicated there, we will see this later in the competitive landscape section. Argentina, Brazil and Mexico are all three growing at a very healthy pace around 60%. When looking at “Others”, which includes 15 countries, the revenue is both small and flat for a while, Q2 is even below the 2021 level. They claimed on their earnings call that Chile specifically has a rough comparison YoY because they performed pretty well in 2021 ( but that means that has slowed rapidly and will not continue with their 2021 pace) and that Colombia is indeed underperforming. Colombia is not just any market, it is the third most Populous country in Latin America.

You could see this underperformance in a negative way, as if they are not doing pretty well in most of their countries, or a positive way, as in they still have a great amount of markets to penetrate. (Though Mexico, Brazil and Argentina account for close to 400 million people, that is more than half the population of Latin America)

When looking in detail at “Other” countries, it is clear that the business lagging in this region is commerce, both services and products have shrunk vs last year, on the other hand, the fintech business in this region has continued to grow, but it is very small for now, representing only $31 million.

Costs and Expenses

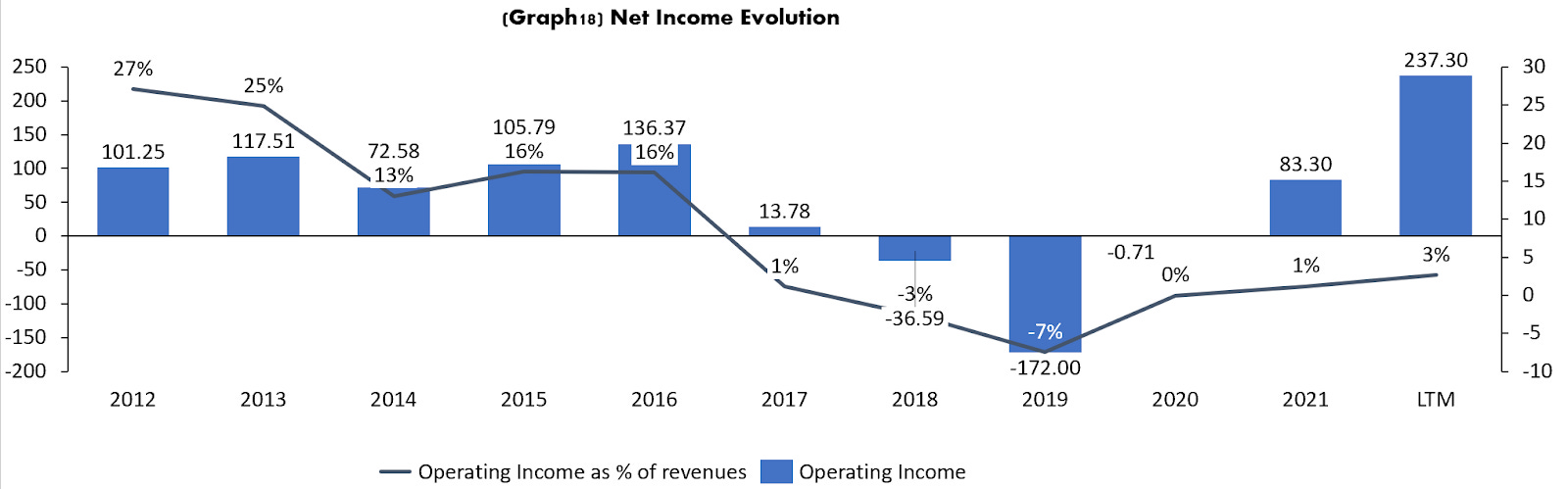

Mercadolibre has been deteriorating its gross margin over the past few years The company has gone from having 20% in direct cost to 48% today. Despite the rapid growth in Fintech business, the e-commerce business has been growing a lot as well, retail in general is a low margin business. Today, e-commerce takes about 66% of their revenues, while it was 58% in 2018. The growth in cost of goods sold started around the year 2017, close to the same period as the revenue finally started to accelerate for the company.

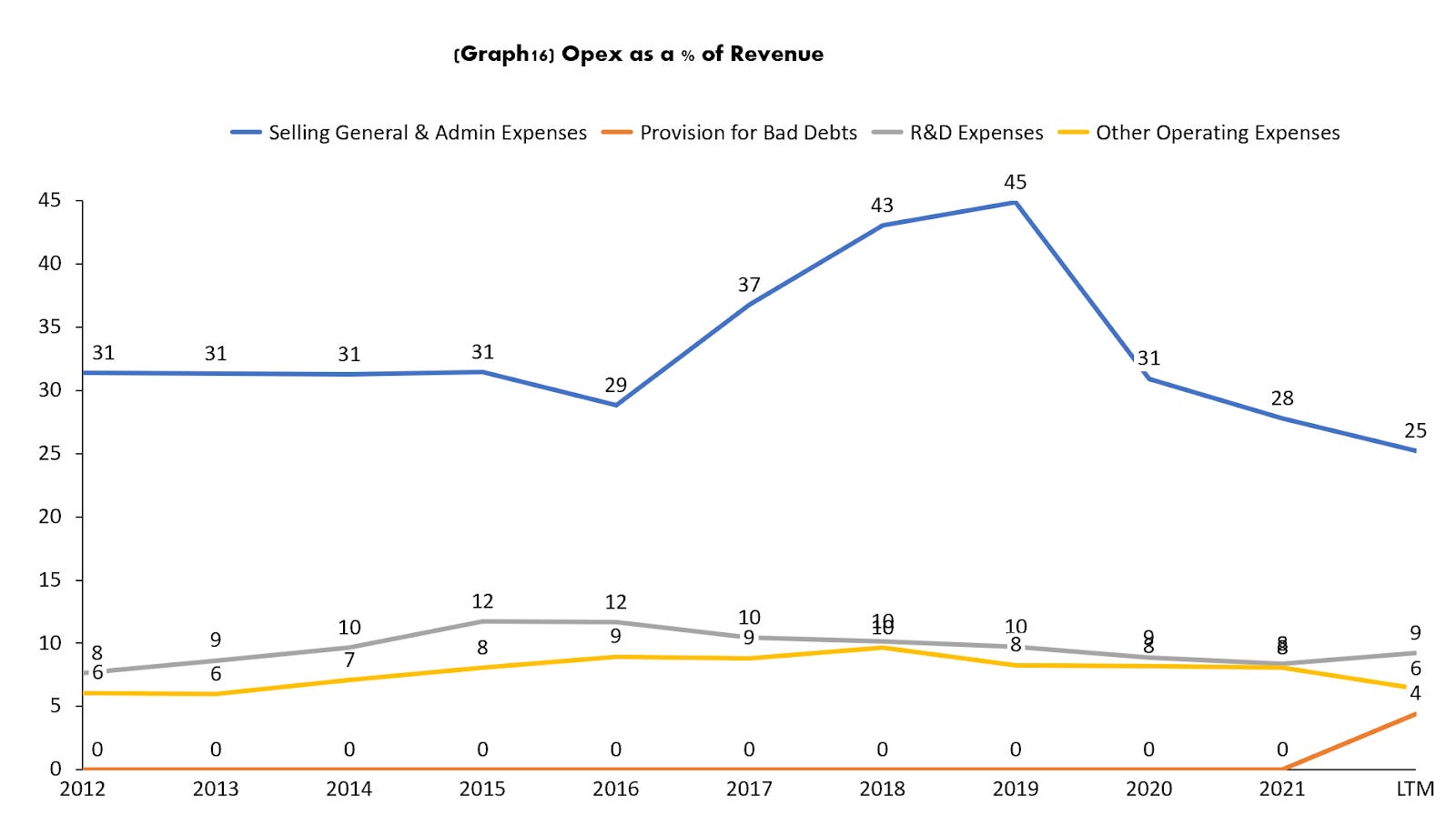

Opex had a peak during the 2018 and 2019 period but has come back down and is reaching their best situation so far. SG&A has dropped considerably to 25% from 31% in 2012 and a high of 45% in 2019, R&D has remained stables as a percentage of revenue while other has had similar performance to SG&A having their best performance recently at 6%

Overall it seems that Mercadolibre spent a lot around the years of 2018 and 2019, this generated a great acceleration in revenue. The company suffered a couple of years of negative operating income, but since has stayed profitable at levels slightly below 10%. This is a company that historically managed very high operating income levels. This was not accelerating penetration at all, it was until they lowered their margins that their growth finally skyrocketed. You can see below that when the margin dropped, they started to get more money as a result in absolute dollars. The company had a high margin from 2012 to 2016, but a very weak growth potential. In 2017 this all started to change, now they have lower margins, better growth, and more dollars in net income. This is very similar to what Silicon Valley companies do, they sacrifice margins for a while, for penetration and growth. Their margins were high enough that even after sacrificing a great deal in terms of percentage points they are still profitable today and growing at double digit levels.

Same story you saw at the net income level, their margins were absurdly high for a company that was trying to grow. It is not really common for a company that is trying to disrupt a market to keep that high of a net income margin. Net income margins are lower today, but as they penetrate and consolidate their presence in these markets this is a better way to go, they are still showing profits in the end and continue funding their business with their own cash. They mentioned in their last call, that their path will be to continue to grow market share while growing profits. We would imagine that they are referring to absolute dollars but that they will hang around these new lower levels of net income.

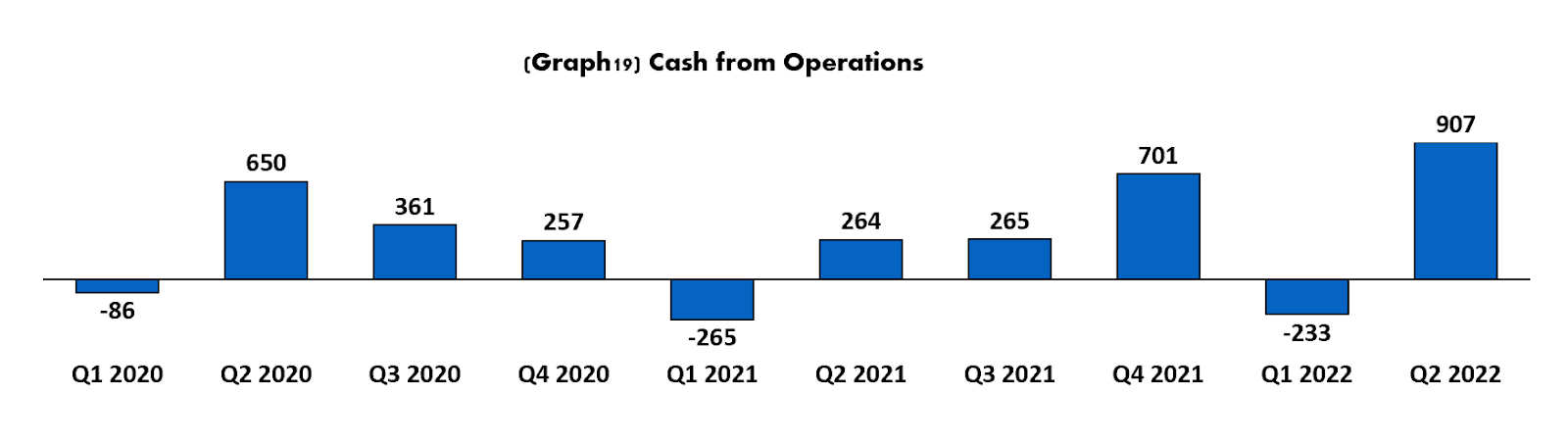

Cash Flow

At the cashflow level, from their operations they continue to generate great results, over the past 12 months they generated $1.6b in cash, but for a company like Mercadolibre this is only half the picture. They also do a lot of cash use on the investing side.

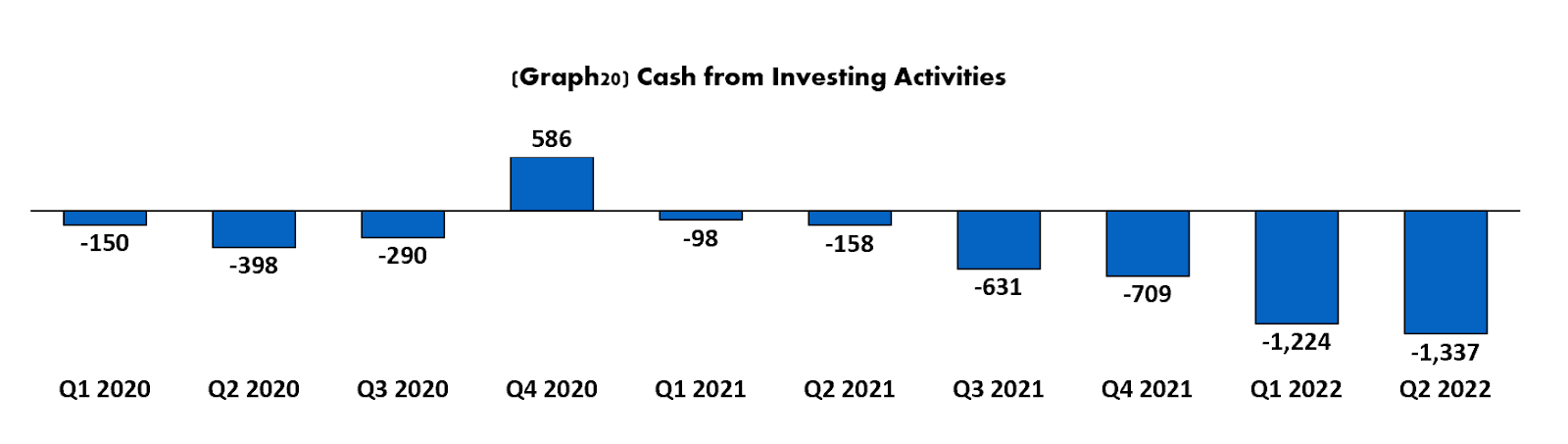

It is their cash from “investing activities” that is taking most of their cash at the moment. Over the past 12 months they used $3.9b on “Investing activities”. A lot of money moves very quickly here. Since the “investing” side of the cash flow is very important for the operations with Mercado Libre. Adding the two operations and investing we have a clearer picture of the level of cash used in its operations. In graph 21 you can see that they have accumulated over the past 12 months a cash use of $2.2b. By cash use we mean actual negative cash flow.

Balance Sheet

After looking at how much money they have used from investing and operation it is more understandable what they have been doing for the past 10 quarters in terms of financing. Since the start of the pandemic they have had a net issuance of $1.8b in debt as well as they issued $1.5b in common stock in Q4 2021, at the same time during that period they have repurchased $614 million of their own stock. Excluding other forms of financing they have gotten $2.7b from all these movements in debt and common stock

This has left the company at the end of the last quarter reported at $2.2b in cash and $4.9b in total debt.

The company has at a P&L level great profitability, it is when we see how much cash is needed (not necessarily lost but needed to run the fintech business) that we see that the company is still needing to keep growing more to sustain their own cash use.

Competitive Landscape

Mercadolibre’s competition is very broad and varied, it has very different situations in each country. Their biggest rival would be Amazon, they have presence in their most important markets, Brazil, Mexico and Colombia (soon). The only county of their big population countries that Amazon does not have presence is Argentina, which makes sense since this is a very established Mercadolibre’s territory, being their native land.

Despite being faced with a strong competitor in Brazil and Mexico Mercadolibre, for now, is the e-commerce leader in these countries. Unfortunately Amazon does not share details on revenue or any type KPIs on the performance both in Brazil or Mexico. Given this, the information we do have is how many visits their website traffic in these regions. In Mexico these are the monthly visitors each website has:

Mercadolibre: 127.6m

Amazon: 63.8m

Walmart Mexico: 27.7m

Coppel 23m

Liverpool 22m

For Brazil the monthly visits to the top 5 players in e commerce are:

Mercadolibre 261m

Americanas 135m

OLX 99m

Amazon 55m

Magazine Luiza 50m

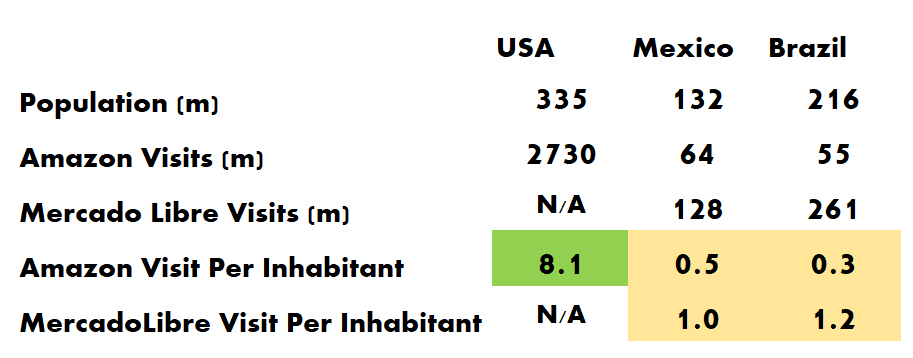

Mercadolibre has a clear lead in both markets. But what is really clear, is that the penetration of these markets is just beginning and this all could change dramatically over the next few years. Looking at the number of visits per inhabitant we see the clear differences between a Mexican and Brazilian Market and what the US market has today. For now, it is clear the big difference between a developed e-commerce market and the one in Latin America. In the US Amazon has on average 8.1 visits per month while Mercadolibre is just at 1.0 in Mexico and 1.2 in Brazil. A country like Spain you could say is still in the middle of their journey, perhaps around 2012-2013 they were at the point Latam is today. Amazon, the leader in Spain, has 4 visits per inhabitant per month, four times the common number for Mercadolibre. clear potential for all the players in Latin America to continue capturing penetration. The market will grow, it is the future in Latin America, we are just at the beginning. The big question for now is who will be the leader. Branding and customer fidelity will be key, Amazon has a big wallet and is very experienced at growing and penetrating markets. These very big populous countries will be very profitable one day and Amazon will be for sure a big headache for Mercadolibre, at least in Brazil, Mexico and Colombia and Area of 400 million People, bigger than the US.

The Fintech market is a very high growth Market for Mercadolibre and a very fragmented market in most of the Latam countries. In Mexico for example, there are 140+ Fintech lenders with 13 different types of credit products, according to a survey conducted by Addem Capital.

Brazil has a very similar situation. There are many big players having great success in the market. Nubank, Creditas and Pagseguro are some of the players that compete in this market.

Nubank is the largest fintech bank in Latin America, they have presence in Mexico, Brazil and Colombia. Making it the most direct competition to Mercadolibre in this space. Looking at the revenues for the last quarter for both companies, in the markets they both share (and that they share details, Mercadolibre does not give details on Colomba) Nubank leads overall, has a slight lead in Brazil, the bigger market, and Mercadolibre leads in Mexico, a smaller market for both.

But that is not the only competition that Mercadolibre has in Brazil, there is also Pagseguro, they had $732M in Fintech revenues over the past quarter, higher than Mercadolibre but lower than the leader, Nubank. As you can see, the Brazilian fintech market is very competitive but also just getting started, this could become a much bigger business but a very high cash intensive business to manage to penetrate and be competitive. There will be a rush for customer acquisitions.

Some of the possible risks for the company are:

Fintech business, this business might be one of the most promising for the company but we all know what happens in Latin América, specifically in geographies like Argentina, Mexico and Brazil. We all know about el corralito in the early 2000s. We all know that Argentina goes into an economic crisis almost every 5 to 10 years. Mexico has been far more stable for a while, but its economy has had very big economic crises in the past. This is a risk with any bank you could say, but in some of these countries you could say that historically has become more possible. (This also impacts the ecommerce side of their business as economies slow down, but could have a huge blow on their banking side) Ask any person in finance if they would think starting a bank in Argentina is a good idea for the long term?

Competition: The market in Latin America is one of the most delayed in terms of e-commerce adoption. A player like Amazon will be interested for sure in attacking and developing a higher penetration in these markets. This could eventually make it a lot harder and a lot more expensive to achieve the level of penetration in developed markets like the US.

Penetration in both e-commerce and fintech could slow down and return to a very slow adoption. Populations in Latin America are very unequal, there are populations in the high income brackets that could make the migration from offline to online commerce. This has been brought forward very fast by Covid. But for the coming years the adoption could slow down again as the population that still does not use their products is usually the type of population that are still offline in most of their purchases.

What could be the case for Mercado Libre being a good opportunity for the next 10 years?

Penetration levels: ecommerce overall is almost non existent yet when compared with developed nations. These markets have a long way to go for future growth. Mercadolibre has a very good opportunity to achieve high growth for many years to come and they even had an impact in some of their operations. Regions like Central America + Dominican Republic have a population of close to 60 million people, this region has yet to come online into this e-commerce space.

Population of their markets. The population of their markets is bigger than the population of the EU or the Population of the US. They have growth for years to come. The question would be the speed.

Branding and current Position: Mercadolibre is the leader in ecommerce where they operate they should be able to hold this or at least they must.

Valuation

Mercadolibre is currently trading at $41b higher than other ecommerce players in the world like Coupang, Sea, it is even bigger than eBay. Their revenues, though, are lower than Coupang, Sea and eBay. Their growth and profitability should the factors playing into a better valuation. But we calculated once again a DCF analysis to find out whether the company is valued correctly at $41b, we produced three scenarios, base, conservative and aggressive. In our base case we see that the company will continue to penetrate and grow its revenue reaching maturity somewhere around 2027, margins continue to improve yet given the region where they operate discount rate we assumed is a bit higher than you average tech American company, the result of our Base Case is a valuation of $595 per share, or about $30b , our conservative case assumes a slower revenue growth and a slower improvement in margins. The result for our conservative case is $315 per share or about $16b, for our aggressive scenario the results are $805 per share, close to what is trading today.

The company has a great opportunity to seize the market in Latin America, but in terms of whether it is well priced or not, it seems that is slightly expensive as of now, it is close to our aggressive scenario in which a lot of good things have to go right. Difficult when we might be entering a big global recession where liquidity will be very tight for a while.