Micron Technology (MU): Structural AI Winner or Peak-Cycle Illusion?

An examination of whether Micron's extraordinary profitability reflects a permanent re-rating of memory economics—or the familiar, dangerous capstone of another super cycle.

Disclaimer: This report is for informational purposes only and does not constitute investment advice, a recommendation, or a solicitation to buy or sell any security. All data is sourced from public filings, earnings releases, and third-party research

Section 1

Executive Summary

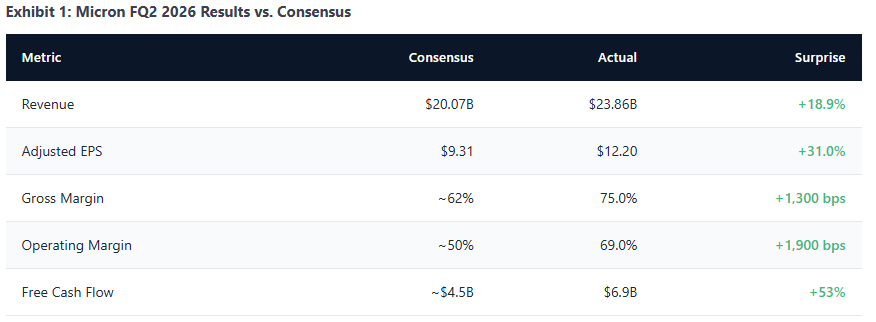

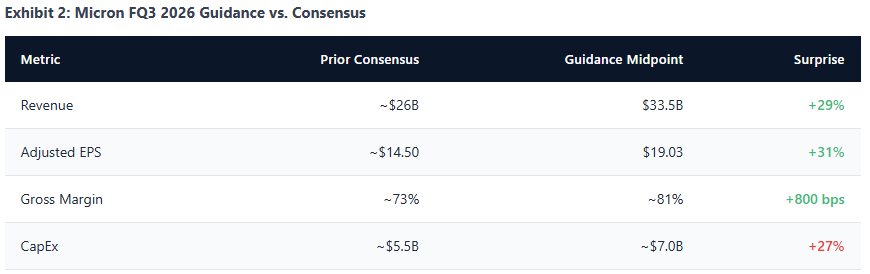

Micron Technology delivered the most extraordinary quarter in its history. Fiscal Q2 2026 revenue of $23.86 billion demolished consensus estimates by 19%, adjusted EPS of $12.20 beat by 31%, and gross margins expanded to 75%—a level that would have seemed inconceivable even a year ago. Free cash flow hit a record $6.9 billion despite $5 billion in capital expenditures. Management then guided Q3 revenue to approximately $33.5 billion with 81% gross margins, numbers that redefine what a memory company can earn at the peak of a supply-constrained cycle.

And yet the stock fell 7% the next day.

That disconnect is the subject of this report. The market’s negative reaction—driven by a capex guidance raise from $20 billion to above $25 billion for fiscal 2026, with a “meaningful” step-up anticipated for fiscal 2027—captures the central tension in the Micron investment thesis. Investors are being asked to decide whether memory economics have permanently shifted due to AI-driven demand, or whether Micron is once again capitalizing peak-cycle conditions that will inevitably normalize.

Our Verdict

Micron is a high-conviction structural beneficiary of AI infrastructure buildout with genuinely differentiated positioning in HBM—but it remains, at its core, a cyclical business now earning well above any defensible mid-cycle estimate. The current revenue run-rate and margin structure reflect extraordinary supply tightness that management itself acknowledges cannot be fully satisfied. When supply eventually catches demand—likely starting in late 2027 or 2028—margins will compress, potentially sharply. The question is not whether normalization occurs, but how far margins fall and how long elevated earnings persist beforehand.

On a forward P/E basis, Micron appears cheap at 10–13x. On a normalized or mid-cycle basis, it is considerably less so. The stock is best understood as a high-quality cyclical trade with structural tailwinds that extend the runway—not a secular compounder that can be held indefinitely without cycle awareness. Investors with a 12–18 month horizon benefit from the most favorable near-term setup in memory history. Those underwriting a five-year hold need to account for material earnings volatility that no amount of AI demand fully eliminates.

Section 2

What the Quarter Actually Proved

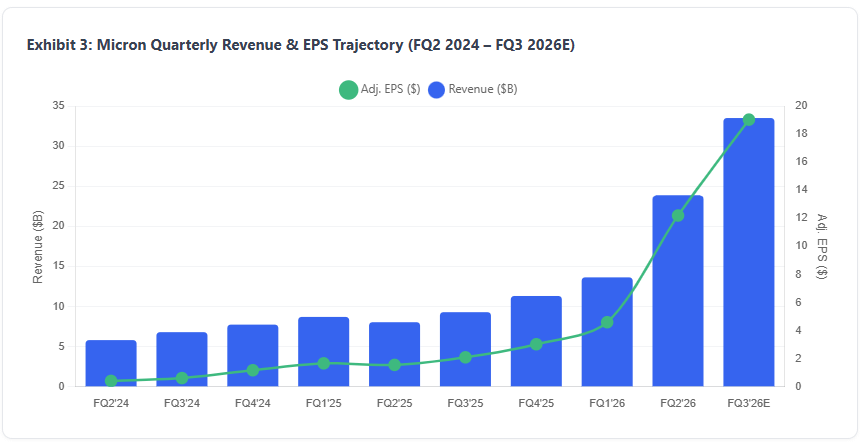

Fiscal Q2 2026 was not simply a “good quarter.” It was a categorical demonstration that AI-driven memory demand has shifted the earnings power of the business to a different order of magnitude. Revenue nearly tripled year-over-year and grew 75% sequentially—a pace of acceleration that is virtually unprecedented for a company of Micron’s scale. Every segment contributed, but the data center business unit was the dominant engine, with core data center revenue surging 139% quarter-over-quarter to $5.7 billion.

Revenue Composition

DRAM accounted for $18.8 billion, or 79% of total revenue, growing 207% year-over-year and 74% sequentially. NAND contributed $5.0 billion (21% of revenue), up 169% year-over-year. The DRAM outperformance reflects the enormous pricing leverage that comes from supply-constrained AI and server DRAM, where contract prices surged approximately 90–95% quarter-over-quarter in the January 2026 negotiation cycle. Cloud memory revenue—Micron’s proxy for hyperscaler and AI demand—reached $7.75 billion, up more than 160% year-over-year.

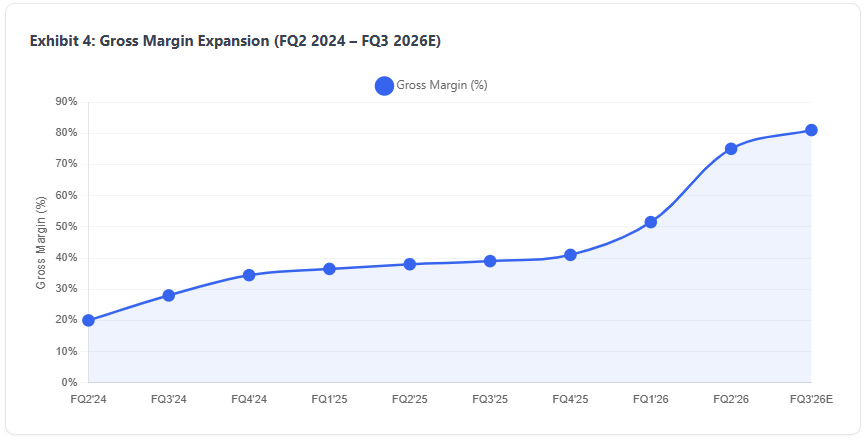

Margin Trajectory

Gross margin of 75% represents an expansion of approximately 1,900 basis points year-over-year and nearly 2,000 basis points sequentially from the 56% posted in FQ1 2026. This is not marginal improvement; it is a wholesale repricing of the memory cost structure driven by three converging forces: supply-constrained pricing power, favorable mix shift toward premium HBM and server DRAM products, and ongoing manufacturing cost reductions. Operating margin hit 69%, translating to operating income of $16.5 billion on a single quarter’s revenue.

Cash Generation and Balance Sheet

Operating cash flow reached $11.9 billion, funding $5.0 billion in capital expenditures and producing $6.9 billion in free cash flow—a record that nearly doubled the prior quarter’s $3.9 billion. The balance sheet stands at roughly $12 billion in cash and investments against $11.8 billion in debt, with total liquidity of $15.5 billion. Management raised the quarterly dividend 30% to $0.15 per share, a signal of confidence, though the payout remains modest relative to earnings power.

Why the Market Sold Off

Despite the blowout results, the stock declined approximately 7% on March 19. The driver was not the quarter itself but the capex guidance: management raised fiscal 2026 capital spending from $20 billion to above $25 billion, with fiscal 2027 expected to include an additional $10 billion or more in construction-related spending alone. For a market that has watched memory companies plant the seeds of their own destruction through aggressive capacity additions at the top of every prior cycle, this was a familiar and uncomfortable signal. Micron has now fallen after earnings in three of the last four quarters, a pattern that suggests investors are increasingly skeptical that peak earnings deserve peak multiples.

Section 3

The Real Thesis: Memory Has Re-Entered the Center of Compute

For decades, memory was treated as a commodity input—necessary, fungible, and fundamentally interchangeable between suppliers. The AI revolution has changed that calculus. Memory is now the critical bottleneck in AI system performance, and the bandwidth, capacity, and latency characteristics of the memory subsystem directly determine the throughput and economics of training and inference workloads.

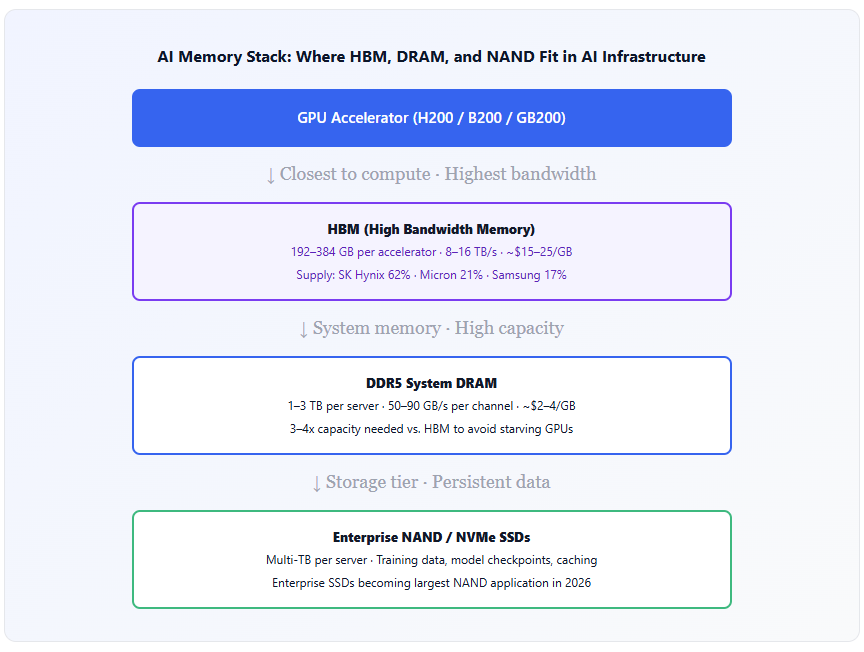

Consider the trajectory. Nvidia’s H100, the workhorse of the initial generative AI buildout, shipped with 80 GB of HBM3 memory delivering 3.35 TB/s of bandwidth. The H200 upgrade increased capacity to 141 GB of HBM3e with 4.8 TB/s. The B200, now in volume ramp, carries 192 GB of HBM3e at 8 TB/s. The GB200 superchip doubles that again to 384 GB and 16 TB/s. Each generational leap in GPU compute demands a proportional and often greater increase in memory bandwidth and capacity, creating a structural tailwind for memory producers that is qualitatively different from the PC and smartphone refresh cycles that historically drove demand.

The critical insight is that a single AI server with eight accelerators now requires approximately 1.6 TB of HBM plus 3 TB of DDR5 system DRAM—compared to less than 1 TB of total DRAM in a traditional enterprise server. This 4–5x increase in memory content per server, combined with explosive growth in AI server shipments, has driven AI-related memory demand to exceed 50% of total industry DRAM TAM for the first time in calendar 2026. One gigabyte of HBM consumes roughly four times the wafer capacity of standard DRAM, meaning the AI buildout is absorbing silicon at a rate that structurally tightens supply across all memory categories.

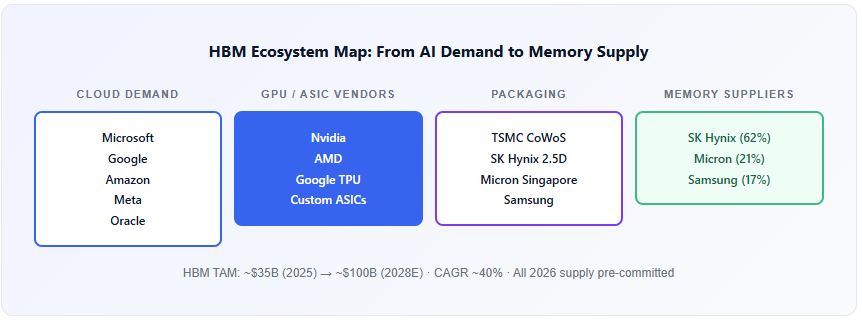

Micron sits squarely in this bottleneck. While the company does not enjoy the brand recognition of Nvidia or the platform leverage of the hyperscalers, it is one of only three companies on Earth capable of producing HBM at scale, and one of only three capable of supplying the DDR5 and enterprise NAND that surround and support GPU accelerators. AI cannot function without memory. Memory cannot be sourced from anyone other than Samsung, SK Hynix, and Micron. This is the structural foundation of the Micron thesis.

Section 4

HBM: Durable Profit Pool or Temporary Gold Rush?

HBM is the highest-margin, highest-growth, and most supply-constrained product in the semiconductor industry today. Micron estimates the HBM total addressable market will grow from approximately $35 billion in 2025 to roughly $100 billion in 2028—a 40% compound annual growth rate—with that $100 billion milestone now projected to arrive two years earlier than prior forecasts. HBM demand is expected to grow 77% in 2026 and 68% in 2027, driven by both GPU-attached demand (Nvidia, AMD) and an accelerating contribution from custom ASIC accelerators, which are projected to represent 33% of total HBM consumption in 2026.

Micron’s Positioning

Micron held approximately 21% of the HBM market as of mid-2025, having surpassed Samsung to become the second-largest supplier behind SK Hynix. The company is now shipping HBM4 in volume for Nvidia’s Vera Rubin platform, with 36 GB 12-high stacks in production and 48 GB 16-high variants sampling. HBM4E development is underway with volume ramp expected in calendar 2027. Management reported that HBM4 production is achieving mature yields faster than HBM3e, a meaningful indicator of manufacturing competitiveness. Micron has expanded its HBM customer base to six accounts and has completed pricing and volume commitments for its entire calendar 2026 HBM supply.

Competitive Dynamics

SK Hynix remains the dominant force in HBM, holding roughly 62% market share and serving as Nvidia’s primary supplier. Goldman Sachs and UBS project SK Hynix will maintain 50–70% share in HBM4, particularly for the Nvidia Rubin platform. Samsung, which suffered HBM qualification delays in 2024 and early 2025, has since recovered: it began HBM3e shipments to Nvidia in late 2025, announced mass production of commercial HBM4 in February 2026, and has already sold out its 2026 HBM4 production. Samsung is targeting a 50% increase in HBM wafer capacity to roughly 250,000 wafers per month by year-end 2026, which could lift its share to 30–35%.

Durability Assessment

The bull case for HBM durability rests on three pillars: demand is structurally growing as each new GPU generation requires more HBM; supply is inherently constrained by the 4x wafer intensity of HBM versus standard DRAM; and the three-player oligopoly limits competitive entry. All three suppliers have pre-committed their entire 2026 production, and management commentary from all three indicates supply will remain tight beyond calendar 2026.

The bear case is equally straightforward: every technology gold rush eventually attracts sufficient capital to erode supernormal returns. Samsung’s aggressive capacity ramp—a 50% increase in HBM wafers by year-end 2026—is precisely the kind of supply response that, historically, marks the beginning of pricing normalization. If Samsung successfully qualifies HBM4 across major customers and expands share to 30–35%, the competitive dynamic shifts from “who can produce enough” to “who offers the best price,” compressing margins across the board. The transition typically takes 12–18 months from the point of supply sufficiency, placing the risk window squarely in late 2027 to 2028.

Our assessment: HBM has permanently elevated Micron’s business quality and customer relevance. It has not permanently elevated margins. The current HBM pricing environment is a function of scarcity, not a sustainable equilibrium. Investors should expect HBM to remain a structurally important profit pool, but should not capitalize current HBM margins into perpetuity.

Section 5

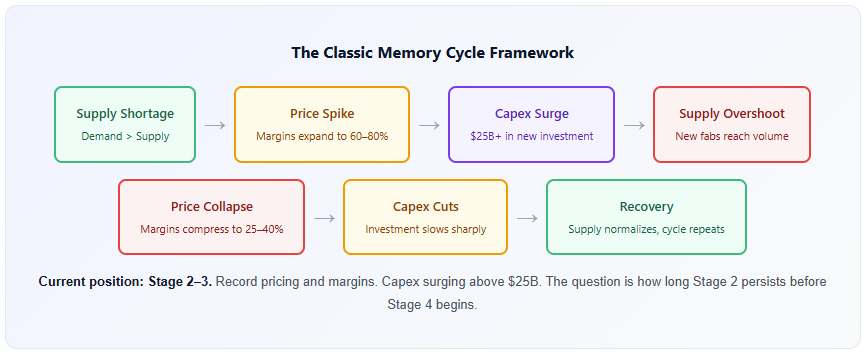

The Old Risk Never Fully Disappears: Memory Cyclicality

Memory has been one of the most reliably cyclical businesses in technology for three decades. The pattern is well-documented: supply tightens, prices surge, producers invest aggressively, new capacity arrives, supply overwhelms demand, and prices collapse. The 2017–2018 supercycle saw Micron’s gross margins reach the low 60s before compressing to 27% during the subsequent downturn. Revenue fell roughly 30% peak to trough. The 2020–2023 cycle saw similar dynamics, with pandemic over-ordering giving way to a severe correction in late 2022 and early 2023.