Nike: Just Fix It

Nike Reported Q3 Earnings Today. The Beat Wasn't Enough. Here's Why the Turnaround Is Real — and Why It's Taking Longer Than Anyone Hoped.

Nike beat Q3 estimates on revenue and EPS this morning. The stock fell anyway. Q4 guidance called for another 2–4% revenue decline, Greater China down 20%, and 250 basis points of tariff headwind. Under new CEO Elliott Hill, the strategy is correct. But China is collapsing, tariffs are mounting, and the shelf space that was surrendered to On Running and Hoka doesn't get returned overnight. The question isn't whether Nike will recover — it's when.

Q3 FY2026 Results

The Numbers: A Beat That the Market Didn’t Celebrate

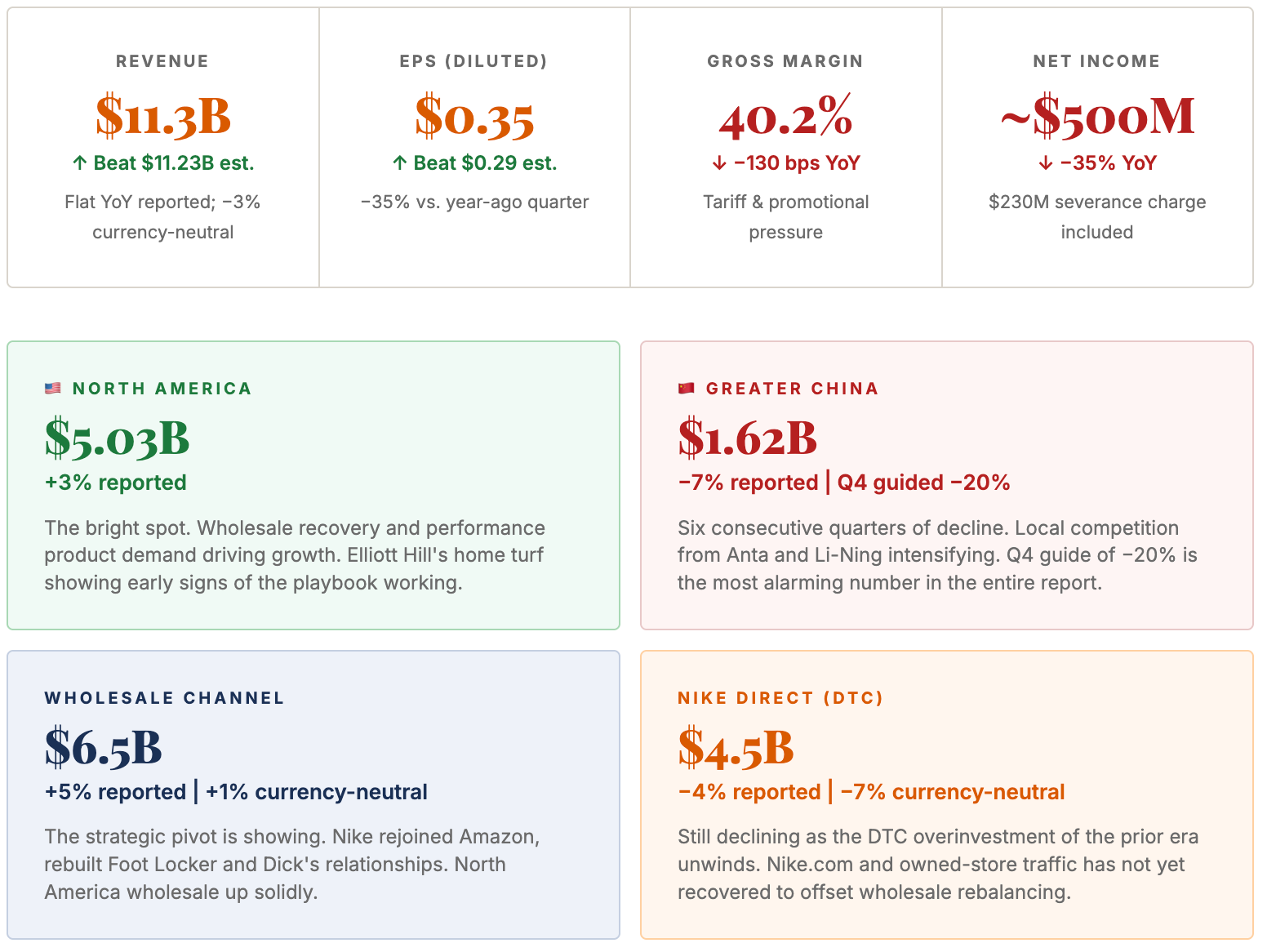

Nike’s fiscal Q3 ended February 28, 2026. Revenue came in at $11.28 billion, essentially flat year over year in reported terms and down 3% on a currency-neutral basis — but above Wall Street’s $11.23 billion estimate. EPS of $0.35 beat the $0.29–$0.30 consensus. Net income fell 35% to approximately $500 million. The market’s reaction was negative: Q4 guidance, particularly the 20% Greater China decline and 250 basis points of tariff pressure on gross margins, outweighed the modest beat.

How We Got Here

Five Years of Strategic Mistakes, Compressed Into a Timeline

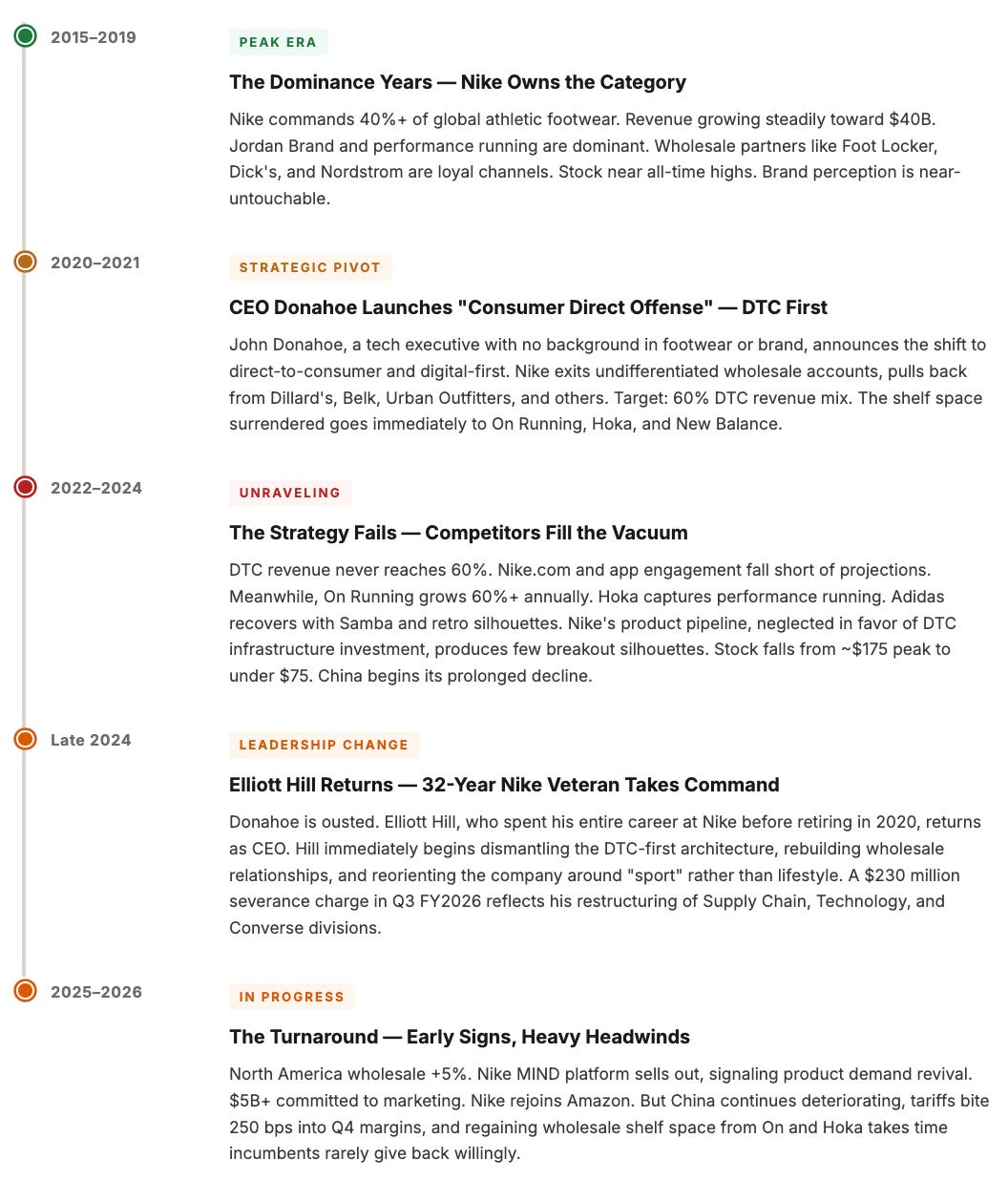

Nike’s current situation is not the result of competitive failure — at least not primarily. It is the result of a sequence of strategic decisions made between 2020 and 2023 that systematically weakened the company’s distribution muscle, strained its wholesale relationships, and starved its performance product pipeline in favor of lifestyle and DTC economics. Understanding the path in matters for evaluating the path out.

The Strategic Autopsy

Why the DTC-First Strategy Was Structurally Flawed From Day One

Nike’s Consumer Direct Offense assumed that a brand with 40% market share could sustain revenue by selling more directly to consumers who were already buying from wholesale partners — with higher margins on each sale. The arithmetic was correct. The strategic assumption was wrong. When Nike pulled back from wholesale accounts, it did not pull consumers with it. Consumers bought On Running and Hoka instead. The shelf space vacancy was filled within months. The revenue that Nike lost in wholesale did not flow to Nike.com — it flowed to competitors. The lesson: in a category with strong competitive alternatives, you cannot withdrawal-force customers into a preferred channel. They simply go elsewhere.

The Turnaround Plan

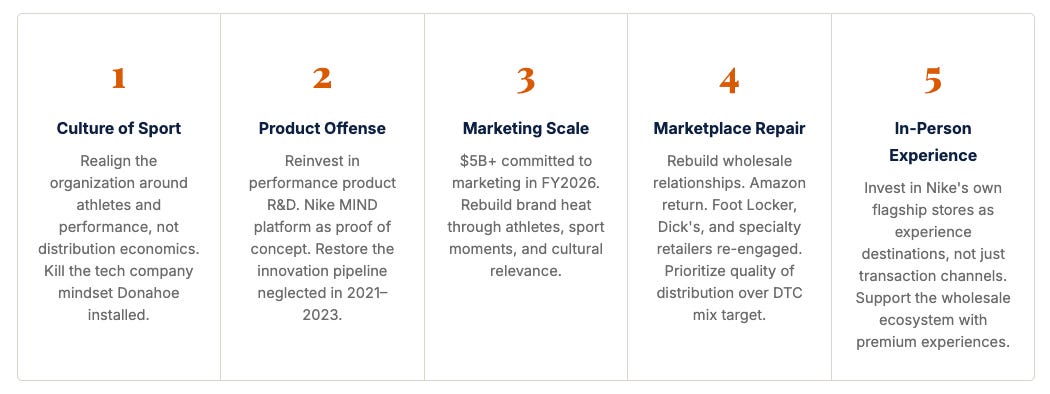

Elliott Hill’s “Win Now” Playbook: Five Pillars

Hill has articulated a five-pillar turnaround framework that is straightforward and consistent with what worked during Nike’s dominance years. The question is not whether the strategy is correct — it is — but whether the execution timeline is fast enough given the simultaneous China deterioration and tariff headwinds.

Turnaround Scorecard

Where the Playbook Is Landing and Where It Isn’t

The Structural Headwinds

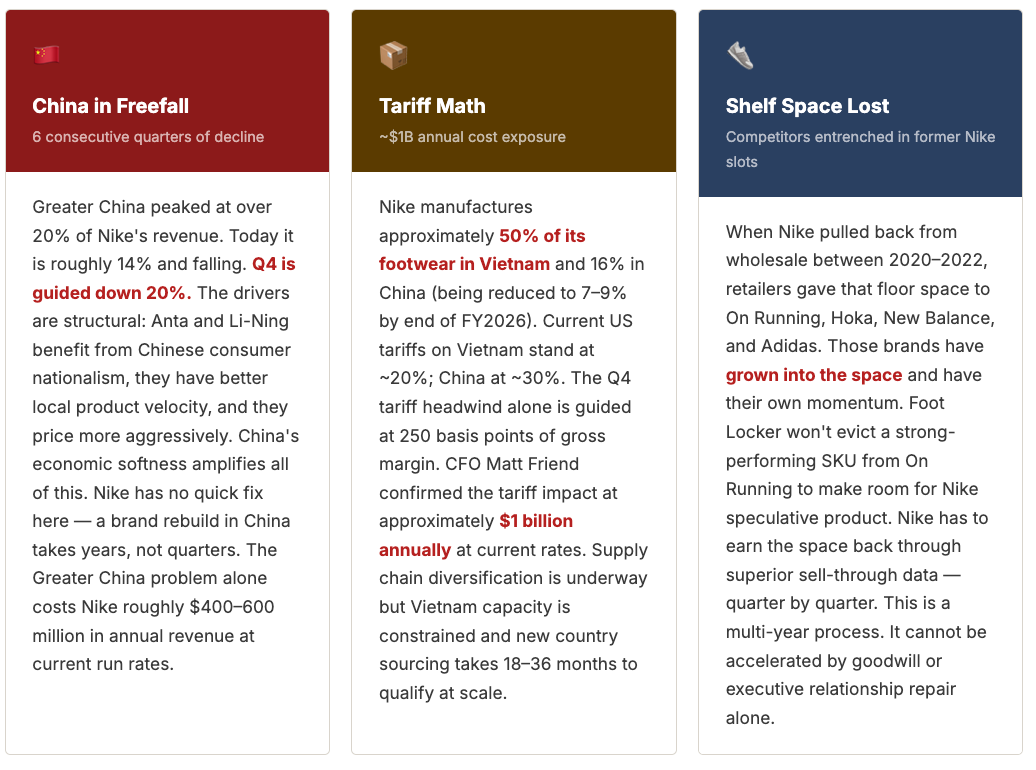

Three Problems That Don’t Fix Quickly

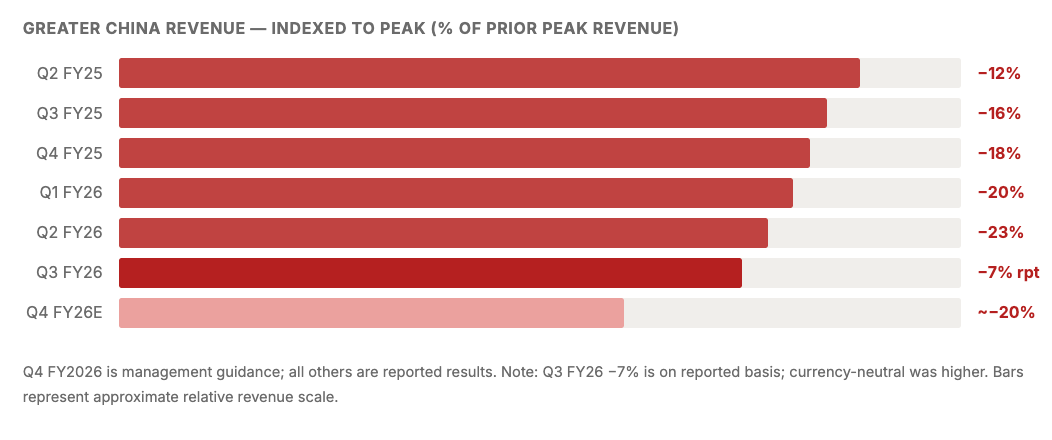

Greater China Revenue Trend

Six Quarters of Decline — With No Floor Yet in Sight

Greater China was once Nike’s highest-growth engine and margin contributor. It is now the company’s most acute strategic liability. The decline has been driven by a combination of local competition, Chinese consumer nationalism (preferring domestic brands post-COVID), economic softness, and Nike’s own inability to localize product and marketing fast enough. Q4 guidance of −20% suggests the deterioration is accelerating, not stabilizing.

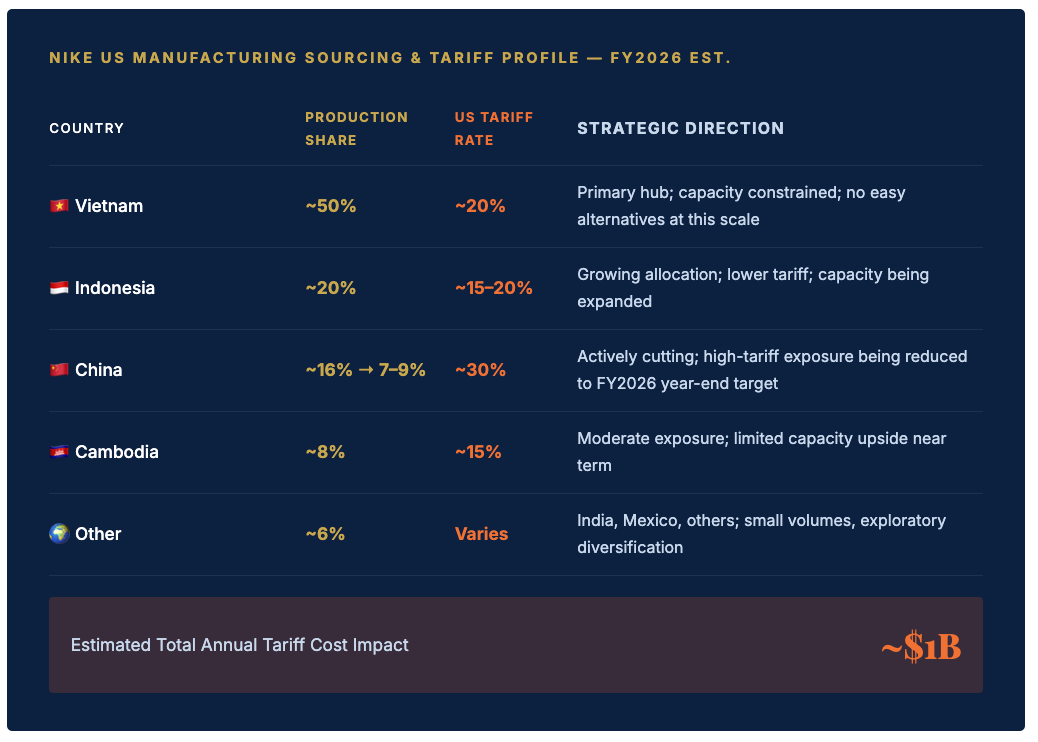

Tariff Exposure

The $1 Billion Annual Tax Nike Didn’t Budget For

Nike’s manufacturing is concentrated in three countries with very different tariff profiles under current US trade policy. The company is actively reshuffling toward lower-tariff jurisdictions but the process takes 18–36 months per new factory relationship. In the meantime, the tariff cost flows directly into gross margin — hence the 250 bps headwind guided for Q4.

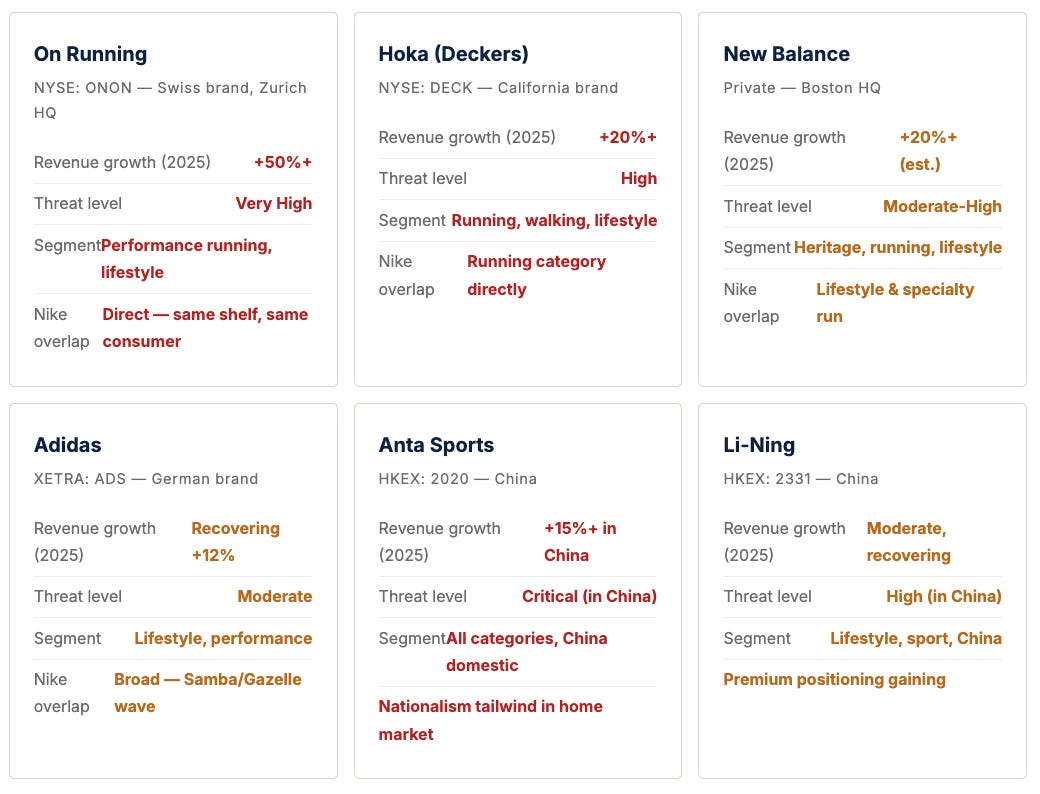

The Competition

The Brands That Took Nike’s Lunch — and Won’t Give It Back Easily

Nike’s DTC retreat created a vacuum. The athletic footwear market rewards incumbency and shelf space — brands that are present when consumers shop tend to get purchased. The brands that filled Nike’s vacated shelf space have since built genuine consumer loyalty, strong sell-through data, and retailer prioritization that is now hard for Nike to displace.

“The turnaround strategy is correct. The mistake was thinking turnarounds happen in two quarters. Brand damage from five years of neglect takes five years to repair.”

LongYield Analysis — April 2026