Nintendo: The Switch 2 Supercycle Meets Fiscal Reality

Nintendo's FY2026 revenues nearly doubled to ¥2.31 trillion on the back of a historic hardware launch — then the stock fell 9% when management opened the FY2027 guidance envelope.

01 — Executive Summary

A Record Year With an Asterisk

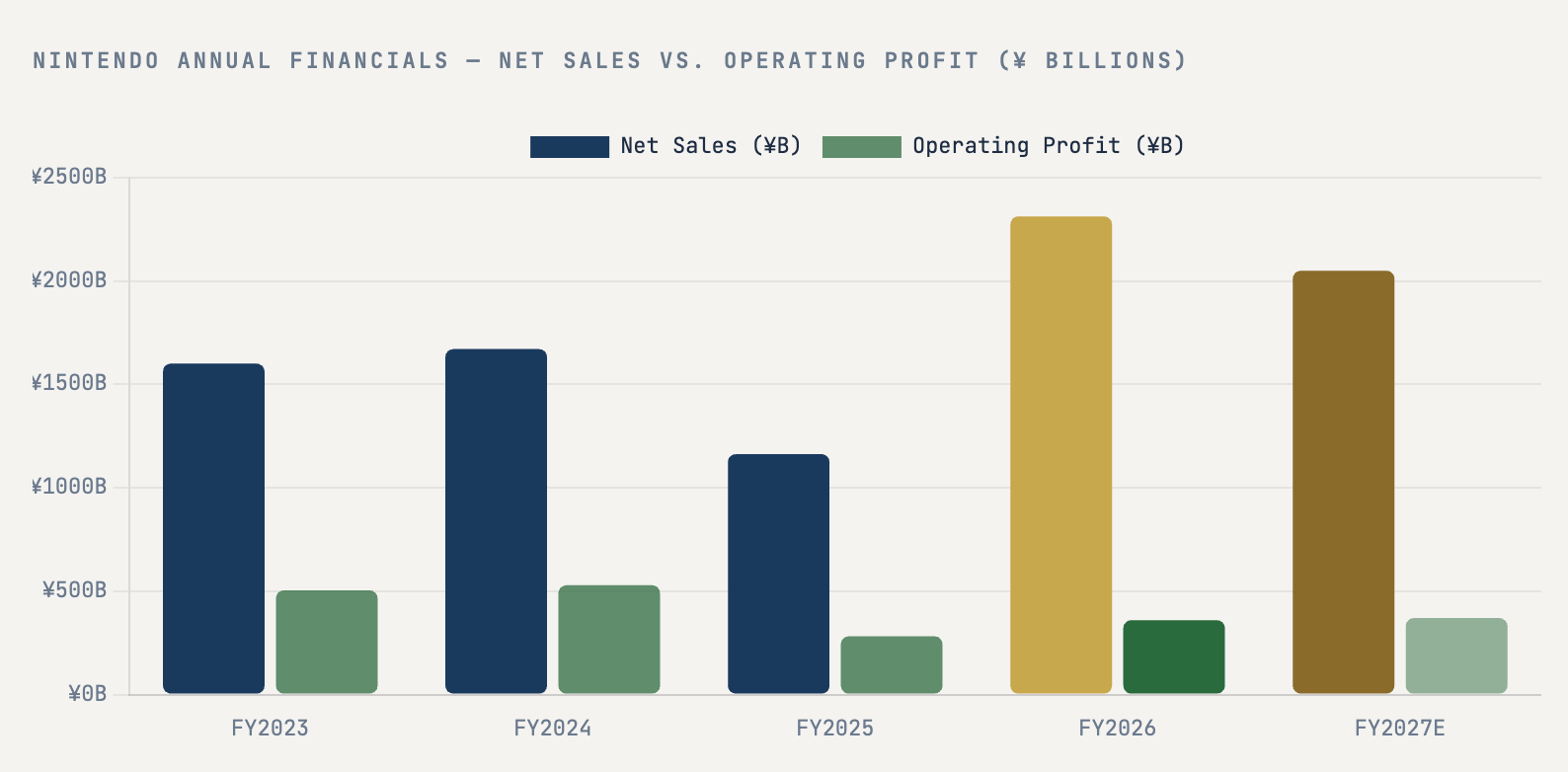

Nintendo’s fiscal year ended March 31, 2026 was, by almost any conventional measure, a triumph. Net sales of ¥2.313 trillion nearly doubled from the prior year’s anemic ¥1.163 trillion — a figure that itself reflected the worst-kept secret in consumer electronics: that the Switch platform was in its twilight cycle, starved of new hardware and running on software fumes. The Switch 2, launched globally on June 5, 2025, was the catalyst the company needed and, with 19.86 million units shipped before the fiscal year closed, it delivered one of the strongest console launches in modern history.

But investors arrived at the May 8 earnings release expecting a clean triumph, and the release delivered a more complicated story. Operating profit, while up 27.5% to ¥360.1 billion, implied an operating margin of just 15.6% — the lowest in more than a decade — as the hardware-heavy launch mix, elevated component costs, and early-cycle manufacturing ramp absorbed the revenue windfall. The contrast was stark: FY2025 operating margins had been a respectable 24.3%, and FY2024 had logged 31.6%. That trajectory line is pointing in the wrong direction.

Management then compounded market unease with FY2027 guidance that implied a reversion: net sales projected at ¥2.05 trillion (down 11% from FY2026), operating profit of ¥370 billion, and — most jarring — net income of just ¥310 billion, a -27% decline. The guidance embedded a Switch 2 hardware unit forecast of 16.5 million units for FY2027, a 17% step-down from FY2026’s achievement. Add in a May 2026 price hike in Japan (from ¥49,980 to ¥59,980) and imminent US price increases, alongside a software pipeline that analysts described as “thin,” and the market’s reaction — a ~9% single-day decline in Tokyo on May 11 — was understandable, if arguably excessive.

This report dissects the full FY2026 print, maps the Switch 2 hardware trajectory against historical console cycle math, examines the real cost of the tariff headwind emanating from Nintendo’s Vietnam manufacturing base, and lays out the bull and bear cases as the company navigates the treacherous middle innings of a new platform cycle.

02 — FY2026 Financial Results

The Revenue Surge That Margin Forgot

Nintendo’s top-line rebound was nothing short of dramatic. After three consecutive years in which the company’s revenue profile slowly deteriorated as the aging Switch lost momentum, FY2026 exploded upward. The ¥2.313 trillion print was the largest annual revenue in Nintendo’s history, surpassing even the peak Switch years of FY2021–FY2022 when pandemic tailwinds supercharged demand for living-room entertainment.

The geography of that revenue is telling. Approximately 77% of FY2026 net sales came from outside Japan, underscoring how thoroughly the Switch 2 launch was a global rather than domestic event. Americas and Europe together likely accounted for over 60% of total revenue — a structural fact that simultaneously represents Nintendo’s greatest strength (massive diversified demand) and its greatest macro risk (yen volatility and US tariff exposure).

Margin Compression: The Launch-Year Tax

Nintendo has historically been one of the most profitable hardware companies in the world. During the peak of the Switch 1 cycle (FY2020–FY2022), operating margins regularly printed north of 30%, reflecting the platform’s near-zero incremental manufacturing cost as yields matured, combined with high-margin software and digital revenues that grew disproportionately in the back half of a console’s life. The FY2026 margin of 15.6% is therefore not a disaster — it is largely the expected consequence of launching a new hardware platform.

“Every Nintendo console launch looks identical in hindsight: revenue spikes as hardware ships, margins crater as silicon costs and manufacturing ramp absorb the windfall, then software and digital revenues slowly rebuild the margin story over the next three to five years.”

What concerns analysts is the trajectory relative to historical precedent. The Switch 1, launched March 2017, saw its operating margin recover from a low of ~17% in launch year FY2018 to a spectacular 36.4% in FY2021 — a ~1,960 basis-point recovery in three years. If the Switch 2 follows a similar glide path, the margin pessimism implied by FY2027 guidance is temporary. If the platform encounters structural headwinds — tariff-elevated bill-of-materials costs, a software drought, or slower-than-expected attach rates — the recovery could prove shallower and longer.

On a segment basis, software revenue was the hidden strength within FY2026’s results. Nintendo did not break out exact software vs. hardware splits, but channel checks and sell-through data suggest that Mario Kart World — the marquee Switch 2 launch title — drove outsized software attach rates in the June–September 2025 window. Digital download revenues, which carry margins approaching 90%, are estimated to have reached approximately 30% of total software revenues, up from roughly 23% in the equivalent Switch 1 launch window. That structural shift toward digital is quietly transforming Nintendo’s long-run margin profile in ways that per-unit hardware economics cannot capture.

One important nuance: Nintendo’s net income of ¥424 billion exceeded operating profit of ¥360 billion, a rare configuration explained by substantial ordinary income (¥542.1 billion ordinary profit, up 45.6%), which includes investment income from Nintendo’s famously conservative balance sheet. The company has long held an enormous net cash position — typically exceeding ¥1.5 trillion — and the interest and investment returns from that hoard meaningfully pad bottom-line results in ways that pure operating performance does not capture.

03 — Switch 2: The Hardware Bet

Engineering the Next Decade of Nintendo

When Nintendo officially unveiled the Switch 2 in January 2025, it had a nearly impossible act to follow. The original Switch, launched in March 2017, had shipped 155.92 million units by the end of FY2026 — making it the second-best-selling video game console of all time, narrowly trailing the PlayStation 2’s estimated 160 million. The Switch was not merely a commercial success; it was a cultural phenomenon, a paradigm shift in how consumers thought about gaming hardware, and the foundation of Nintendo’s most profitable decade ever.

The Switch 2 is Nintendo’s answer to a deceptively simple question: how do you follow a generational product? The answer, it turns out, was refinement at scale rather than reinvention. The Switch 2 retains the core hybrid concept — a tablet-style device with detachable Joy-Con controllers that docks to a TV — but upgrades virtually every component specification in ways that matter to both casual and enthusiast audiences.

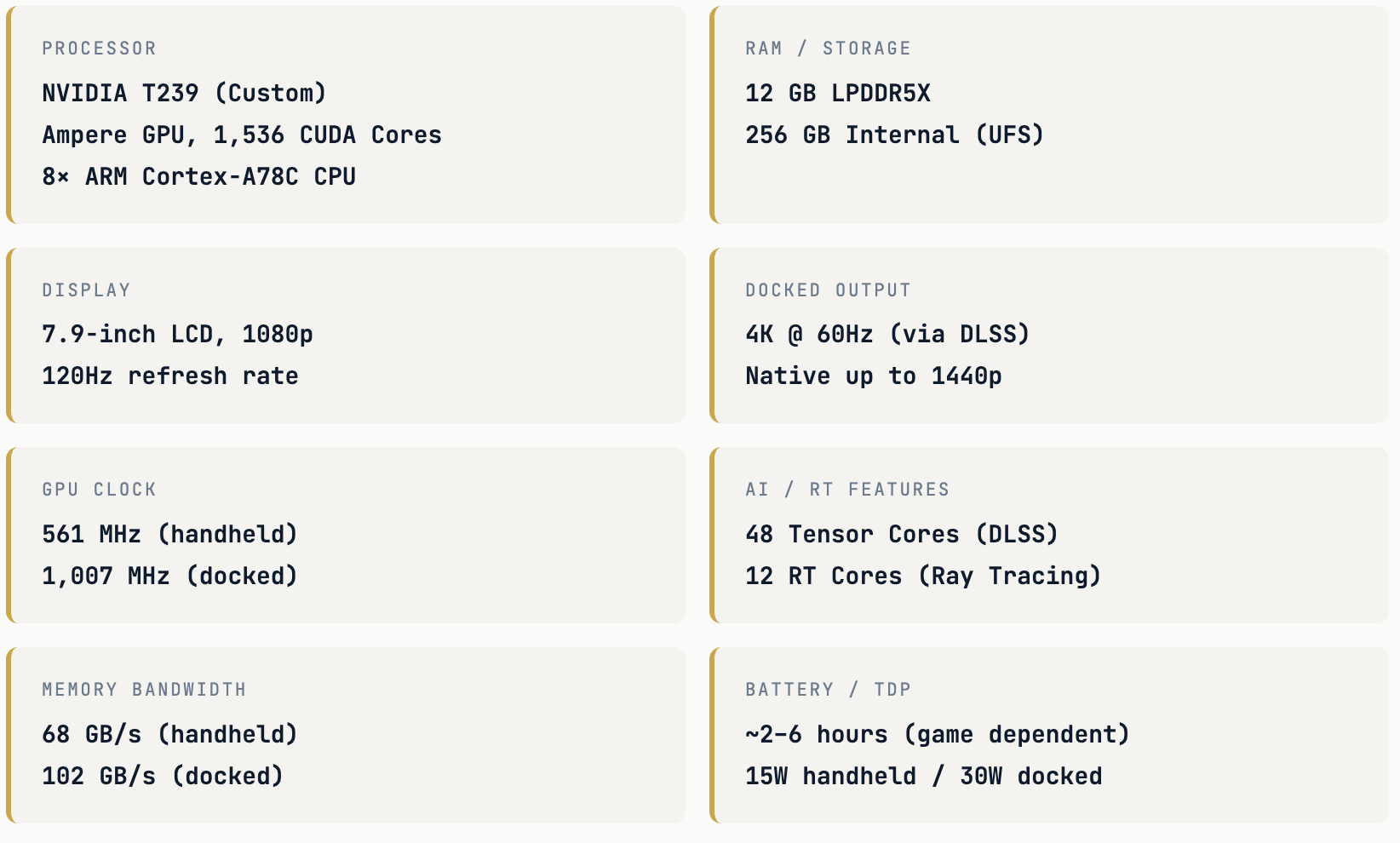

Technical Specifications

The NVIDIA partnership is the defining technical story of the Switch 2. The T239 System-on-Chip brings Ampere-generation GPU architecture to a portable device for the first time, delivering the kind of DLSS-powered upscaling and hardware-accelerated ray tracing that previously existed only on desktop GPUs and Sony’s PlayStation 5. DLSS (Deep Learning Super Sampling) is particularly consequential: by using AI-trained neural networks to reconstruct high-resolution frames from lower-resolution inputs, the Switch 2 can produce 4K output in docked mode from scenes rendered at 1080p or below, dramatically expanding the resolution headroom without proportional power consumption penalties.

The 12 RT cores enable genuine real-time ray tracing on portable hardware — a first for the gaming handheld market segment. While ray tracing on the T239 is not equivalent to what a dedicated desktop RTX card can achieve, its presence signals NVIDIA and Nintendo’s intent to position the Switch 2 as a serious platform for current-generation multi-platform releases, not merely a home for first-party exclusives.

Pricing: From Launch to Price Hike

The Switch 2 launched globally on June 5, 2025, priced at $449.99 in the United States and ¥49,980 in Japan. Both prices were widely seen as appropriately premium — higher than the Switch 1’s $299.99 launch price, but defensible given the hardware generation gap and the persistent inflationary environment in consumer electronics.

By May 2026, however, the pricing chapter had acquired a new and controversial chapter. Nintendo announced a Japan price increase to ¥59,980 effective May 25, 2026 — a ¥10,000 (20%) hike in under a year — citing component cost escalation, tariff impacts on supply chains, and the weaker yen reducing effective overseas revenue repatriation. US and European price increases to $499.99 were subsequently confirmed for September 2026. The market reacted poorly: the prospect of a demand-destroying price increase layered onto already cautious FY2027 hardware unit guidance produced a feedback loop of negative sentiment in the hours following the earnings release.

Pricing Timeline — Switch 2

June 5, 2025: Global launch — $449.99 US / ¥49,980 Japan | May 25, 2026: Japan price rises to ¥59,980 (+20%) | September 2026: US price rises to $499.99 (+11%) and European markets follow. Accessories adjusted at launch — Joy-Con 2 pair raised to $95, Pro Controller to $84.99.

04 — Tariff Headwinds