Palantir Technologies (PLTR): Worth the Price?

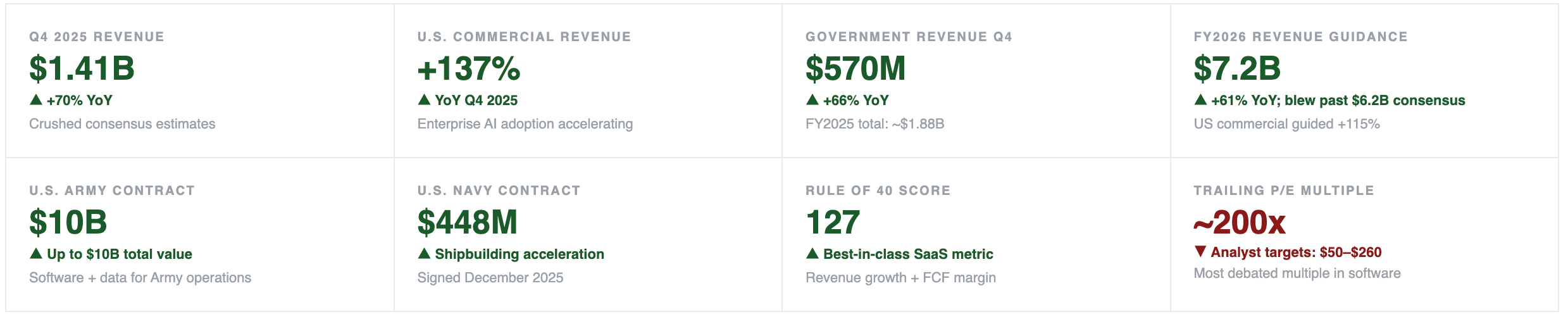

The most debated valuation in the software universe Palantir reported 70% revenue growth in Q4 2025, guided for 61% growth in 2026, and signed a $10 billion U.S. Army contract.

For informational purposes only. Not investment advice. Data sourced from Palantir Q4 2025 earnings release (February 2026) and LongYield research.

Q4 2025 + FY2026 Guidance

The Numbers Are Real

What Palantir Actually Does

The Three Platforms That Drive Revenue

Palantir sells three software platforms that converge around the same core idea: turning large, messy, siloed data into operational decision-making. Gotham was built for government intelligence and military applications — analyzing signals, patterns, and adversary behavior across fragmented data sources. Foundry extended that capability to commercial enterprises, helping manufacturers, hospitals, and financial firms do what governments were doing: see across their data. AIP — the Artificial Intelligence Platform launched in 2023 — connects Palantir’s infrastructure to large language models, letting organizations deploy AI on their own data with guardrails for accuracy and compliance.

The commercial explosion is happening in AIP. The 137% U.S. commercial revenue growth in Q4 2025 is not traditional enterprise software sales. It’s AIP boot camps — intensive 3–5 day sessions where enterprise clients build working AI prototypes on Palantir’s platform — converting to contracts at rates that would be extraordinary in any software business. The remaining deal value for U.S. commercial contracts surged 145% to $4.38 billion, a forward revenue signal that is unusually strong.

THE RULE OF 40 SCORE — 127 — WHAT DOES IT MEAN?

The Rule of 40 is the gold standard for SaaS health: add your revenue growth rate to your free cash flow margin. Anything above 40 is exceptional. Salesforce at its peak was ~50. Snowflake’s best quarter was ~80. Palantir’s score of 127 — combining ~70% growth with ~57% FCF margins — is the highest ever recorded by a public software company. It doesn’t make the stock cheap. But it confirms the underlying business quality is extraordinary.

Government Business

Defense AI — The Original Moat

Palantir’s government business is misunderstood by investors who focus on commercial growth. The government contracts are not cyclical revenue — they are infrastructure contracts for the U.S. military, intelligence community, and allied nations that are essentially irreplaceable once embedded. The switching costs are measured in years of institutional knowledge and classified system integration.

The U.S. Army contract worth up to $10 billion is the largest software contract in Army history. The Navy shipbuilding contract reflects a different application: Palantir’s software is being used to accelerate the production logistics of warships — directly relevant to the strategic competition with China’s naval buildup. Both contracts have the geopolitical tailwind of a U.S. defense posture that is investing in AI-enabled decision systems at an accelerating pace.

The Debate

200x P/E — Justified or Irrational?

At approximately 200x trailing earnings, Palantir is one of the most expensive stocks in the software universe. Analyst price targets range from $50 to $260 — a $210 spread that reflects genuine disagreement about whether this is a legitimate premium franchise or a speculative momentum trade. Both camps have real arguments.

⚠ THE DOGE RISK — GOVERNMENT REVENUE IS NOT GUARANTEED

The Department of Government Efficiency (DOGE) has been auditing and cutting federal software contracts. Palantir’s government contracts are largely mission-critical and embedded — but the political environment creates headline risk even if the actual contract base is secure. An unexpected contract review or cancellation would hit a stock priced for perfection very hard.

Valuation Context

Where Palantir Sits in the Software Universe

At 80x earnings — still a premium multiple — Palantir would need to grow into its valuation by sustaining 50%+ revenue growth for 4–5 consecutive years while maintaining margins. The FY2026 guidance suggests Year 1 is on track. Year 3 and Year 5 are the unknowns that justify the valuation debate.

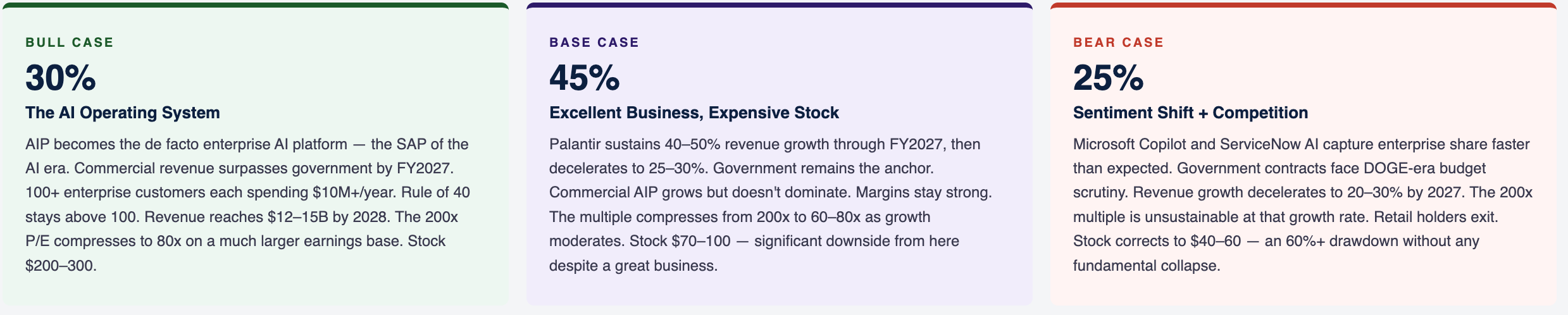

Forward Scenarios

Three Ways the Valuation Debate Resolves

LongYield Signal Dashboard

8-Factor Assessment — Palantir (PLTR)

LongYield View

The Verdict

Palantir is one of the best software businesses ever built. The Rule of 40 score of 127 is not a typo. The government moat is real, deep, and widening as AI becomes central to defense decision-making. The AIP commercial traction is genuine — not hype, not pipeline — evidenced by 137% U.S. commercial growth and $4.38 billion in remaining deal value. If you own zero Palantir and you’re building a concentrated technology portfolio, the business quality argument for owning some is strong.

The valuation is the honest constraint. At 200x earnings, you need the company to execute at the highest level in software history for five consecutive years without a major miss, a government contract setback, or a competitive disruption from Microsoft, Google, or ServiceNow. Those are not impossible conditions. They are simply conditions that have never been met, which is why the 200x multiple has always been a number reserved for companies that are either shortly to be proven right — or proved extremely wrong.