Paramount Skydance: Streaming Turns Profitable. Now Comes the $110 Billion Bet.

9 months after David Ellison closed his takeover of Paramount, the restructuring thesis is working: streaming is profitable for the 1st time, cost cuts are ahead of schedule, & the core biz is stable

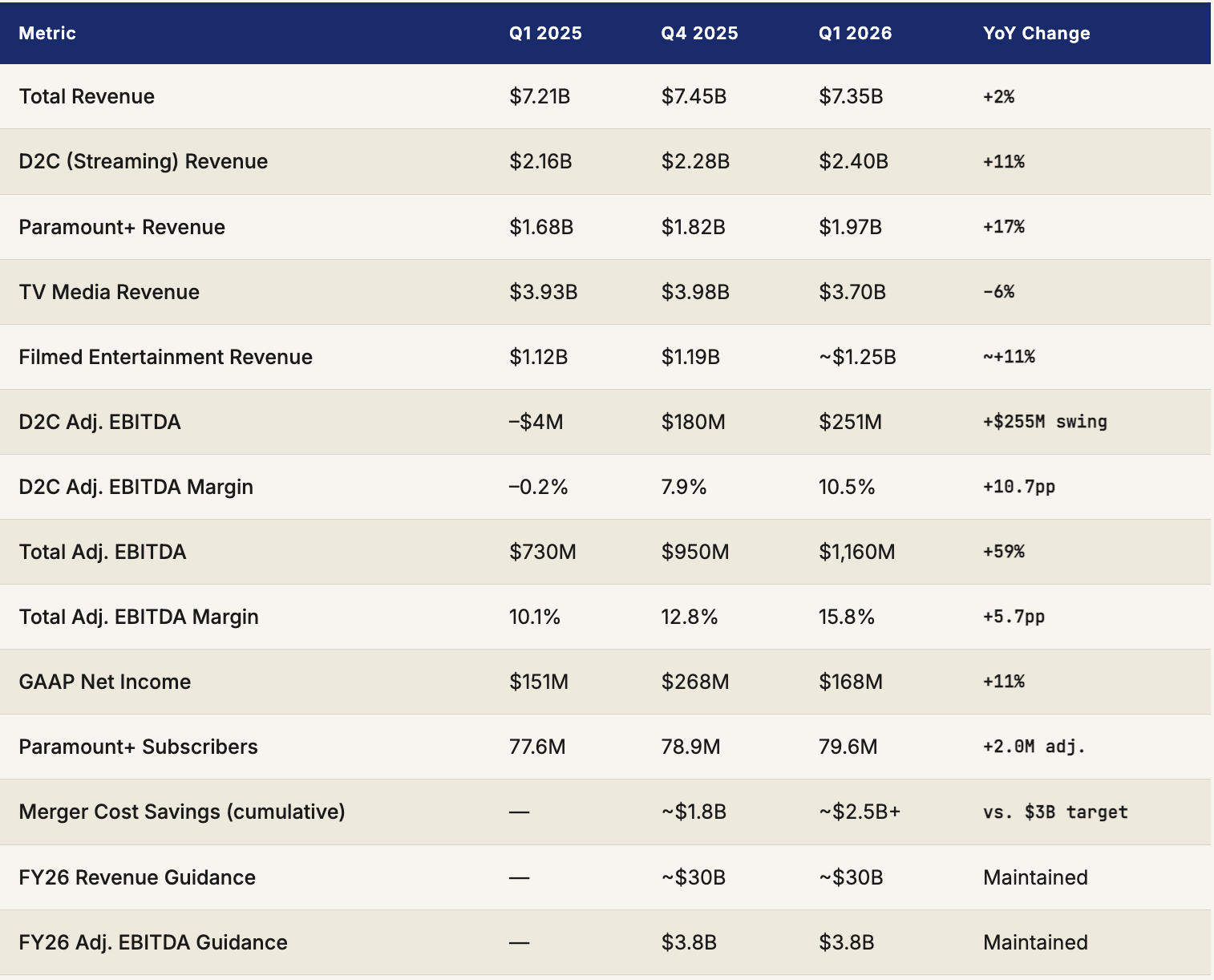

Paramount Skydance posted Q1 2026 revenue of $7.35 billion, up 2% year-over-year, beating consensus estimates on both the top and bottom lines. The headline story was streaming: direct-to-consumer revenue grew 11% to $2.4 billion, with Paramount+ revenue specifically up 17% to $1.97 billion. For the first time in the company’s modern streaming history, the D2C segment generated positive adjusted EBITDA — $251 million, a swing of $255 million from the $4 million loss recorded in Q1 2025. Total adjusted EBITDA grew 59% to $1.16 billion. GAAP net income came in at $168 million.

Against those genuine operational wins, management maintained its full-year 2026 guidance of approximately $30 billion in revenue and $3.8 billion in adjusted EBITDA — a 15% margin target that would represent the healthiest profitability profile in the company’s modern history. The cost savings from the Skydance merger are tracking ahead of schedule: more than $2.5 billion of the $3 billion target is expected to be eliminated by year-end 2026. Television Media, the legacy cash cow, declined 6% as cord-cutting accelerated and advertising softened. But the larger shadow over all of it is the pending Warner Bros. Discovery merger — a $110 billion transaction that WBD shareholders approved on April 23, 2026, and that now awaits regulatory review in the U.S. and Europe. If it closes, David Ellison will be running the second-largest streaming platform on earth. If it doesn’t, or if the integration goes wrong, the downside scenario is severe.

01

From Sumner Redstone’s Empire to Ellison’s Bet — The Long Road to PSKY

Paramount’s story is one of the great American media sagas — a company that defined the golden age of Hollywood, built CBS into a broadcast dynasty, and then spent the better part of a decade trying to navigate the streaming revolution while carrying the debts of its past. Sumner Redstone built Viacom and CBS into twin pillars of American media through a combination of acquisition aggression and sheer force of personality. He bought Paramount Pictures in 1994. He bought CBS in 1999. He reunited them in 2019. When he died in August 2020, he left behind a sprawling media empire that was simultaneously indispensable and financially fragile — rich in content libraries and broadcast infrastructure, poor in the kind of technology investment and subscriber-first discipline that streaming competitors were building from scratch.

The years under CEO Bob Bakish were characterized by genuine effort and insufficient capital. Paramount+ launched in March 2021 as a rebranding of CBS All Access, carrying the weight of legacy infrastructure and the underinvestment of years. It grew — to 56 million, then 67 million, then approaching 80 million subscribers — but it never grew fast enough, profitably enough, to satisfy a market that had decided streaming was a winner-take-most game. The stock, which traded under the ticker PARA, declined steadily as the market discounted the linear TV business and questioned whether Paramount could fund the streaming buildout without diluting equity or loading debt.

The Skydance bid arrived in the context of a balance sheet that offered limited options. David Ellison — 42 years old, son of Oracle’s Larry Ellison, founder of Skydance Media (Top Gun: Maverick, Mission: Impossible, several Marvel co-productions) — had spent fifteen years producing films with Paramount and had developed a specific conviction: that the studio’s core content franchise was undermonetized, that its cost structure was bloated by legacy overhead, and that a $3 billion restructuring could transform the economics without destroying the brand. National Amusements, the Redstone family holding company, sold a controlling interest to Skydance after a competitive process that involved several other bidders. The transaction closed August 7, 2025. Paramount Global was renamed Paramount Skydance. Ticker became PSKY. David Ellison became chairman and CEO.

Q1 2026 is the first full quarter reflecting the combined company’s restructured cost profile, and the numbers are — on the streaming side at least — a validation of Ellison’s thesis. The question now is whether he can replicate the logic at ten times the scale with the Warner Bros. Discovery deal.

02

Q1 2026 by the Numbers

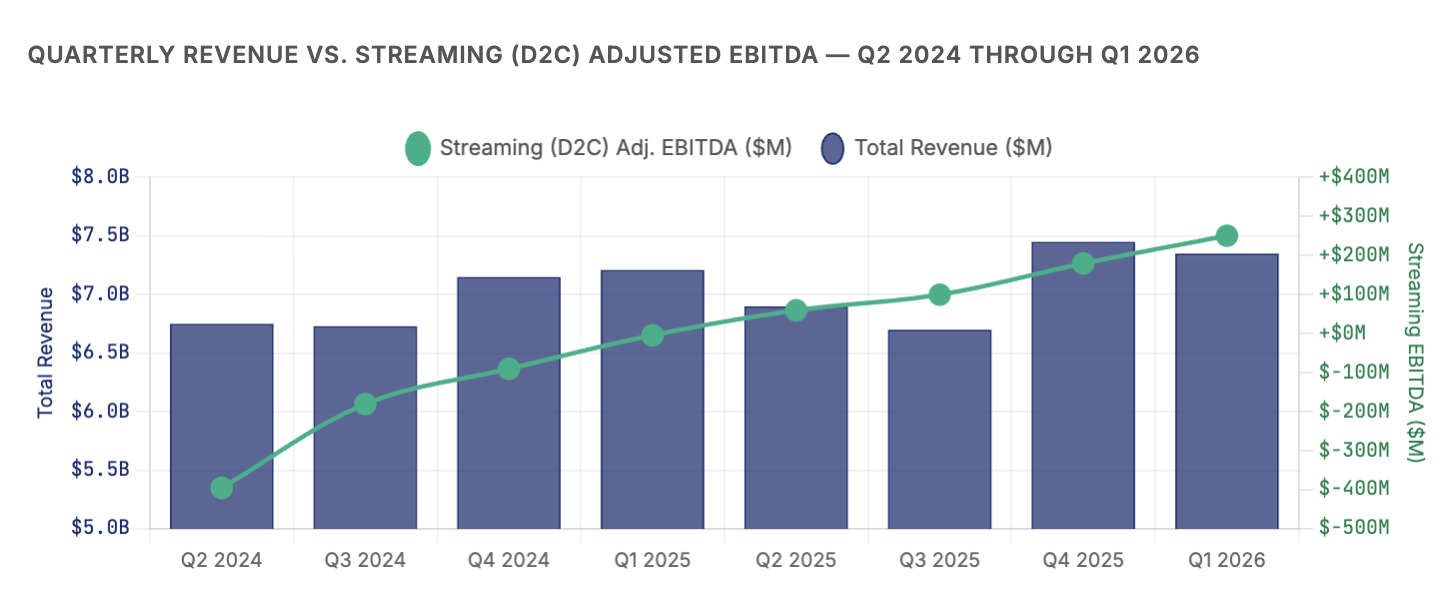

The chart above tells the core restructuring story better than any single data point: total revenue has been essentially flat for two years while streaming profitability has gone from deep losses to a meaningful positive contributor. This is the playbook that Netflix executed, that Disney+ executed, that Warner Bros. Discovery executed — the transition from “spend to grow” to “grow profitably.” Paramount’s version is happening later and on a more compressed timeline than its peers, but Q1 2026 marks the moment the math genuinely changed. A 10.5% EBITDA margin on $2.4 billion in streaming revenue is not a rounding error. It is a business.

03

The $110 Billion Gamble — Warner Bros. Discovery

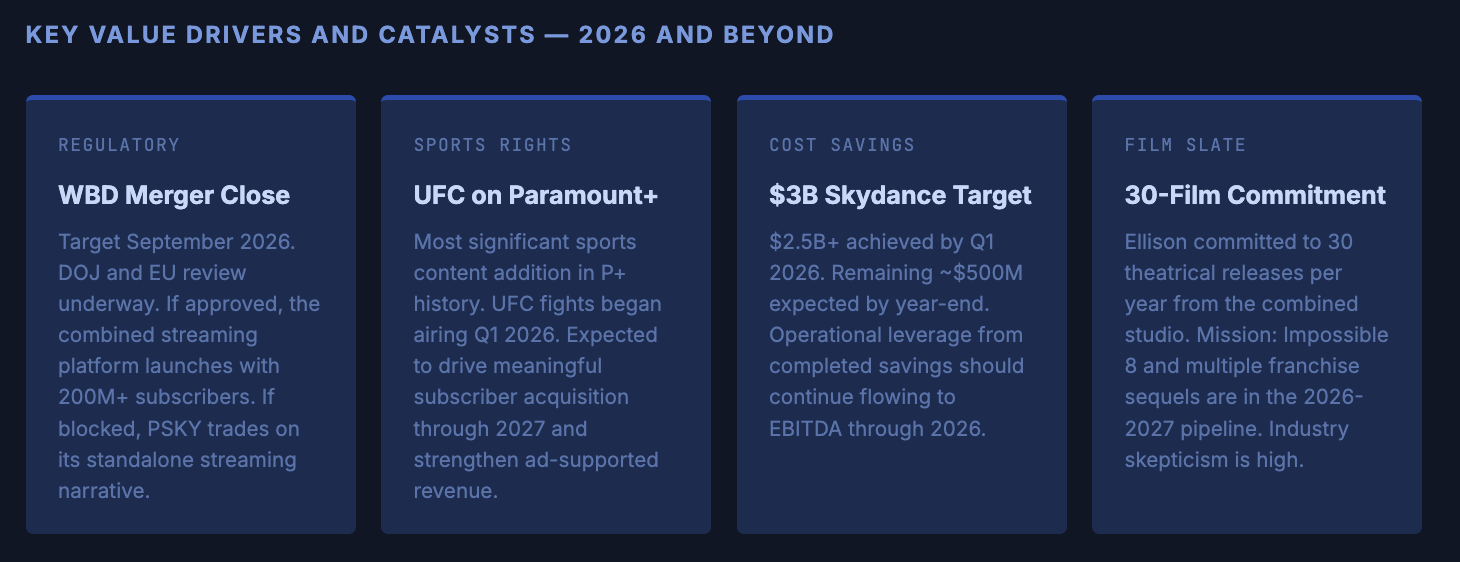

Before the streaming profitability story could fully mature into a re-rating thesis, David Ellison announced the next move: a merger with Warner Bros. Discovery that would combine Paramount+, Max, HBO, CNN, Cartoon Network, Discovery, Nickelodeon, MTV, BET, Pluto TV, and the Paramount and Warner Bros. film studios under a single corporate structure. Warner Bros. Discovery shareholders approved the transaction on April 23, 2026. The deal is valued at approximately $110 billion including debt. Regulatory review in the U.S. and Europe is underway; the target close is September 2026.

The Warner Bros. Discovery Deal — What It Means

Combined Streaming Subscribers

200M+

Paramount+ (~80M) plus Max (~105M) creates the second-largest global streaming platform after Netflix (~330M). The combined service would be available in 200+ countries.

Combined Deal Value (incl. debt)

~$110B

WBD shareholders approved at $30/share. The deal triggers a new round of integration complexity on top of the still-unfinished Skydance restructuring.

Ellison’s 30-Film Annual Slate

30 films/yr

Ellison has committed to releasing 30 theatrical films per year from the combined studio — nearly double current Paramount output. Industry executives and theater operators are publicly skeptical. No studio has sustained this pace with consistent quality.

Opposition & Regulatory Risk

4,000+ signatories

More than 4,000 Hollywood directors, writers, and actors signed an open letter opposing the merger. California AG Rob Bonta is investigating antitrust implications. EU review adds a second regulatory front.

The strategic logic for the WBD deal is not hard to articulate: Netflix has 330 million subscribers and dominant market position. Disney has Marvel, Star Wars, ESPN, and 150 million subscribers. Amazon has Prime Video bundled with the world’s largest commerce platform. Apple TV+ has iPhone distribution. In that competitive landscape, a standalone Paramount+ at 80 million subscribers with a recovering balance sheet and a shrinking linear TV business is a viable but ultimately mid-table player. A combined Paramount-WBD at 200 million subscribers, with HBO’s prestige brand, CNN’s news infrastructure, Warner Bros.’ film library, and the combined cable network portfolio, is a genuine contender — the only realistic challenger to Netflix at scale.

The execution risk, however, is substantial. The Skydance cost-cutting playbook is still running — $2.5 billion of $3 billion achieved, with the last tranche being the hardest. Adding a second, larger integration on top of a first integration that is not yet complete is an organizational challenge of a kind that has historically destroyed value in media M&A. AOL-Time Warner remains the cautionary tale. Comcast-NBCUniversal took a decade to fully integrate. Discovery’s takeover of WarnerMedia under David Zaslav is still regarded as unfinished. Ellison, at 42, is betting that his Silicon Valley-trained operator mindset and his streaming conviction can succeed where every prior generation of media consolidators has struggled.

04

Four Businesses Inside One Stock

Streaming (D2C) — The Thesis Validator

$2.4B Rev · $251M EBITDA

Paramount+, Pluto TV (ad-supported), and BET+ combined to deliver the company’s first consistently profitable streaming quarter. Paramount+ revenue grew 17%, driven by both subscription growth and advertising. The UFC rights deal, which took effect in Q1 2026, is the most significant sports content investment in the platform’s history and is expected to drive subscriber acquisition through 2027. The 10.5% EBITDA margin is competitive with where Disney+ and Max were after two to three years of profitability — achieved here in roughly one year of Skydance-led discipline.

TV Media — The Declining Engine

$3.7B Rev · –6% YoY

CBS, MTV, BET, Comedy Central, Nickelodeon, and the full cable portfolio remain profitable and generate substantial cash flow — but the structural decline is accelerating. Advertising revenue fell 6% as the traditional TV upfront market continues to shrink. Affiliate revenue fell another 6% as MVPD subscribers cut the cord. The TV Media segment remains the company’s largest revenue contributor but its cash flows are declining at a rate that makes every year’s patience more expensive. Ellison has explicitly said these assets become more valuable as content supply for streaming than as standalone linear networks.

Filmed Entertainment — Cyclical but Strategic

~$1.25B Rev · Volatile

The Paramount Pictures film studio returned to modest profitability in Q1 on the back of a solid theatrical slate, though management guided for “significantly lower” theatrical revenue for the full year of 2026 as the release calendar is lighter. The studio’s strategic value is not its quarterly P&L but its role as a content factory for Paramount+ and, post-merger, for the combined streaming platform. Top Gun, Mission: Impossible, Transformers, Sonic the Hedgehog, A Quiet Place, and the Star Trek franchise are the IP pillars that Ellison is betting can sustain a 30-film annual slate.

International — Underdeveloped Upside

Incl. in D2C · Growth Mode

Paramount+ has a meaningful international presence — particularly in Latin America, Australia, and select European markets — but has historically underinvested relative to Netflix and Disney. The combined WBD entity would dramatically expand international scale, with Max’s European and Latin American footprint complementing Paramount+’s existing subscriber base. International streaming is the segment where the merger math is most compelling: shared content costs across a larger subscriber base creates a unit-economics improvement that is difficult to achieve organically.

05

The Pipeline — Four Catalysts, Uncertain Timing

06