PayPal's Third Act: The Restructuring Gamble at 8× Earnings

CEO #3 in two years, a $1.5B cost campaign, and a branded checkout losing ground to Apple Pay — but Venmo is ripping and the stock is historically cheap

Not financial advice.

All figures sourced from PayPal investor relations, earnings releases, and publicly available research.

Past performance is not indicative of future results. Always conduct your own due diligence.

Executive Summary

PayPal reported a Q1 2026 beat on both revenue ($8.35B, +7%) and non-GAAP EPS ($1.34 vs. $1.27 expected), but the stock sold off nearly 8% because the Q2 guidance told a different story: non-GAAP EPS down ~9% year-over-year and transaction margin dollars compressing again. The underlying mechanics are not subtle — branded checkout TPV grew just 2% as Apple Pay, Google Pay, and Stripe continue chipping away at the premium end of the market, while the two bright spots (Venmo at +14%, BNPL at +23%) are still structurally lower-margin.

The more important story is the leadership rupture. Alex Chriss — the CEO brought in from Intuit just 2.5 years ago to engineer a comeback — was pushed out in February 2026. His replacement, Enrique Lores from HP, took over March 1 and has moved fast: a 20% global headcount reduction, a $1.5B savings target, and a three-unit reorganization. At 8× earnings and a market cap of roughly $41B, PayPal is priced for permanent decline. Whether Lores can prove that wrong — or whether PayPal’s structural issues are deeper than any single CEO can fix — is the only question that matters.

01

From Mafia to Monopoly to Midlife Crisis

The PayPal Mafia isn’t a myth. In 1998, Max Levchin and Peter Thiel built Confinity to beam money between Palm Pilots. They merged with Elon Musk’s X.com, survived a coup that nearly ended the company, and sold the whole enterprise to eBay in 2002 for $1.5 billion. What eBay got was a payments rail so embedded in e-commerce that it became synonymous with online trust — the blue button that told buyers their card number was safe.

The 2002–2015 eBay era was simultaneously a golden cage and a strategic straightjacket. PayPal processed nearly all of eBay’s transactions but was forbidden from partnering aggressively with other merchants. When Carl Icahn forced the spinoff in 2015, the newly independent PayPal exploded into deals — Braintree ($800M, 2013, which came with Venmo), Xoom, iZettle, Honey ($4B, 2019). The stock tripled. Then the pandemic hit and supercharged everything: PayPal added 72 million net new accounts in 2020 alone, peaking at 429 million active users by early 2022, and the stock touched $310.

What followed was one of fintech’s most brutal corrections. Apple Pay was pre-installed on 1.2 billion iPhones. Stripe had quietly captured the developer-first checkout market. Shop Pay was converting Shopify’s 2 million merchants onto a single optimized flow. PayPal’s branded checkout — the core revenue engine — found itself fighting on every front simultaneously. The company cycled through Dan Schulman (retired mid-2023), Alex Chriss (hired July 2023, fired January 2026), and now Enrique Lores (effective March 2026), each arrival trailing a reorganization announcement. The stock has spent four years oscillating between $55 and $90, a $40-billion company that once had a $350 billion market cap, waiting for a thesis that sticks.

02

Q1 2026 by the Numbers

The surface read is reasonable. Revenue of $8.35B came in above the $8.05B consensus, growing 7% year-over-year on a currency-neutral basis. Total payment volume (TPV) of $463.96B grew 11%, its fastest pace in several quarters. Non-GAAP operating income rose to $1.47B, and the company bought back $1.5 billion of stock in the quarter — aggressive capital return for a company in restructuring mode. But the granular breakdown reveals the bifurcation that defines PayPal’s predicament.

The most revealing line is branded checkout TPV at just +2% on a foreign-exchange-neutral basis. This is PayPal’s highest-monetization product — the consumer-facing checkout button with the richest take rate — and it is essentially stagnant. Management called the +1 percentage point sequential acceleration an early positive signal, but a $310-stock-peak company calling 2% growth an “improvement” tells you everything about where the ground shifted.

03

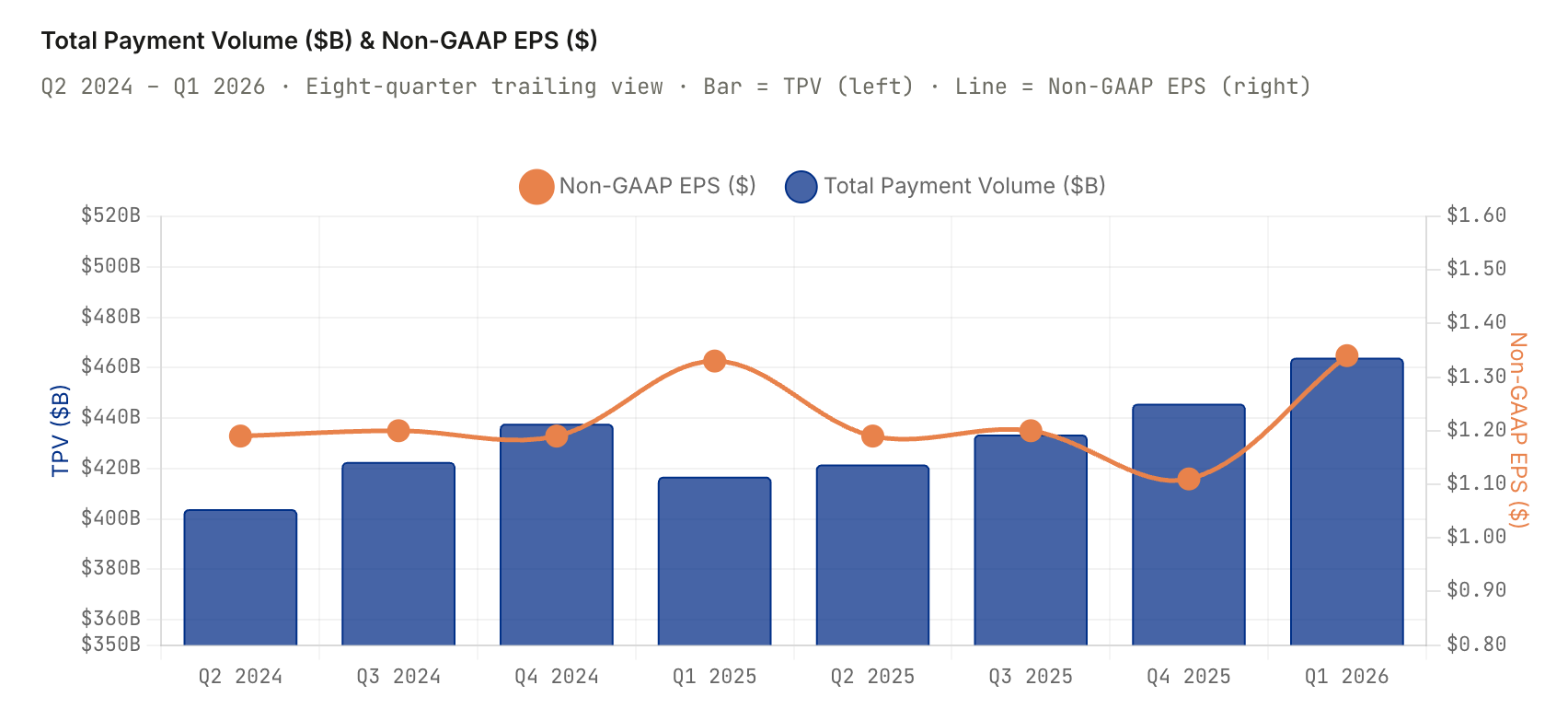

Volume Growth vs. EPS Stagnation

The chart below captures the fundamental tension in PayPal’s story: payment volumes are growing at a healthy clip while earnings per share have barely moved in two years. The divergence between TPV and EPS tells you that while PayPal is moving more money, it’s keeping less of it — a direct consequence of branded checkout mix shift toward lower-margin unbranded processing and rising operating cost structures.

04

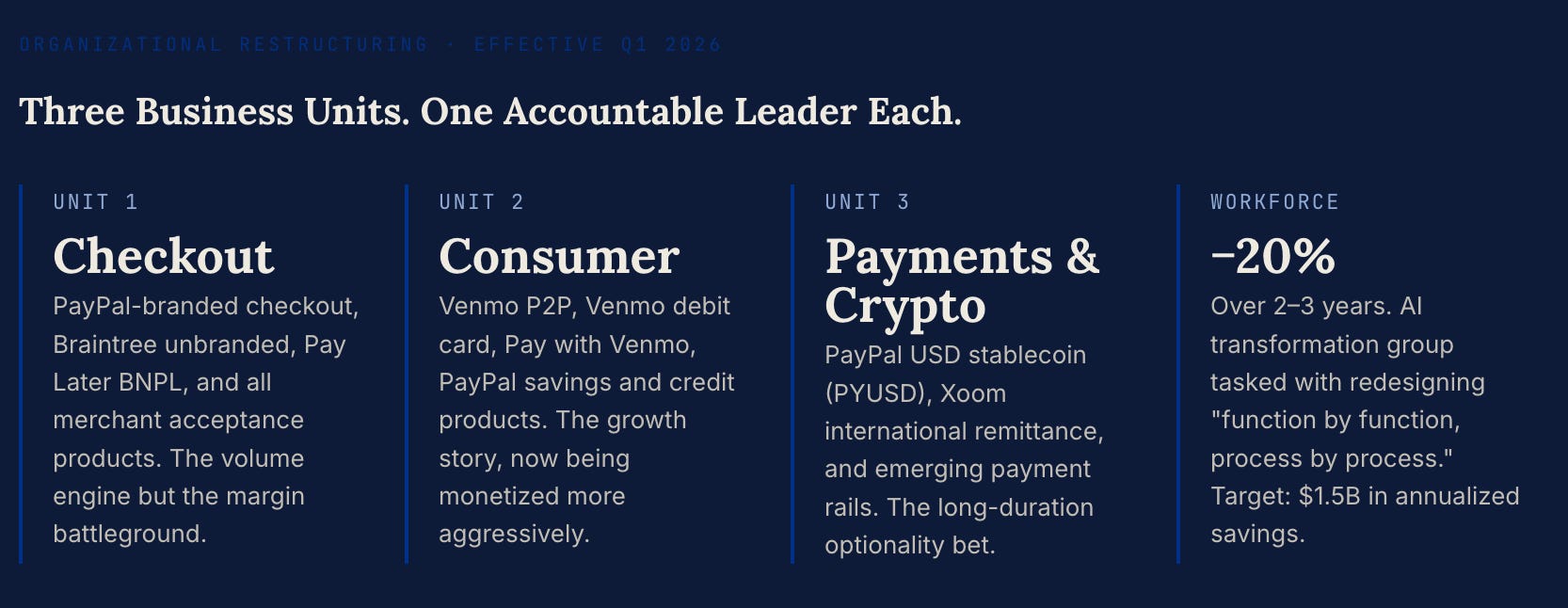

The Three-Unit Gamble

On his first earnings call as CEO, Enrique Lores announced a structural reorganization that will define his tenure. PayPal has been collapsed from a sprawling matrix organization into three distinct business units, each with a single accountable leader. The theory is elegant: Chriss’s PayPal suffered from diffuse ownership, too many initiatives, no clear P&L discipline. Lores is a hardware executive — he ran HP through a cost-cutting and portfolio-refocus era — and he’s applying the same logic to fintech.

The risk with any reorganization of this scale is execution drag. PayPal has 21,000+ employees across 45+ countries, deep regulatory entanglements, and a technology stack built through 20 years of acquisitions that were never fully integrated. HP under Lores took three years to realize its restructuring savings. PayPal’s payments landscape moves faster than enterprise printing cycles. If competitors — particularly Stripe and Apple — accelerate while PayPal is reorganizing, the 2–3 year savings horizon could look like a luxury the company doesn’t have.

05

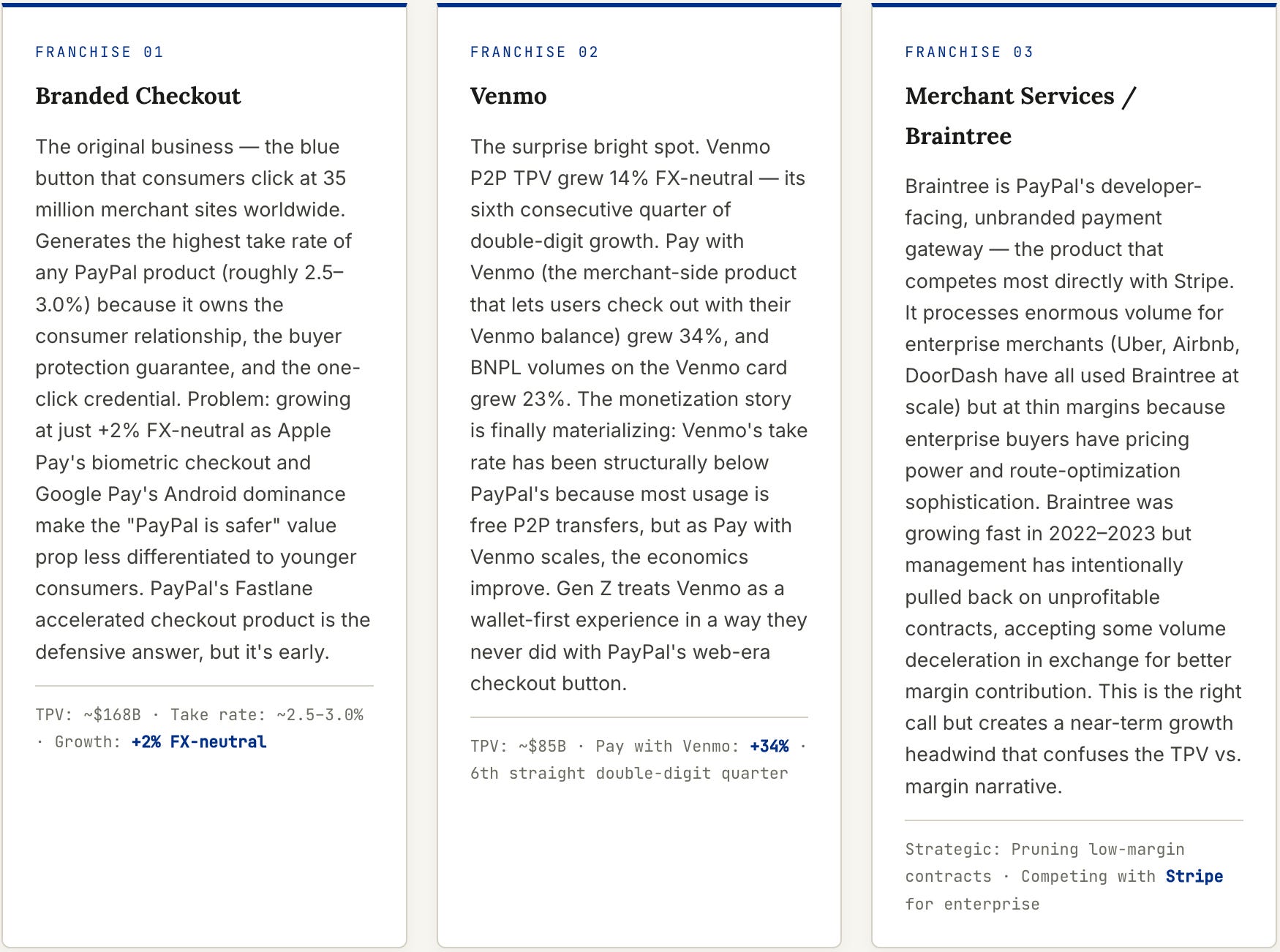

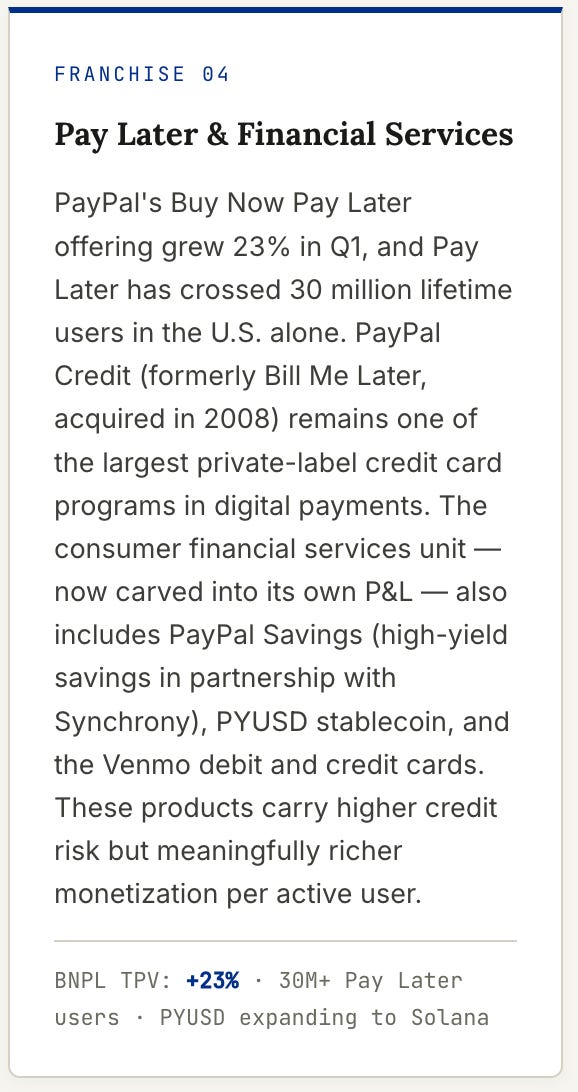

The Four Franchises Inside PYPL

06

What Lores Is Building

Every new CEO at a company in structural transition gets a 100-day grace period to define what they stand for. Enrique Lores has used his to signal four clear priorities: radical cost discipline, Venmo monetization, AI-driven process redesign, and a cautious but real crypto posture. Whether these are the right bets depends almost entirely on whether branded checkout stabilizes — if it does, the cost savings flow directly to EPS and the stock re-rates; if it doesn’t, the savings are just triage.

Strategic Pipeline · 2026–2027 Initiatives

Four Bets on the Turnaround

Cost Program

$1.5B annualized savings via 20% workforce reduction over 2–3 years. AI group redesigning OpEx function by function. HP playbook applied to fintech — Lores executed a similar program at HP to $1B+ in savings.

Venmo Monetization

Expanding Pay with Venmo merchant acceptance, Venmo credit card APR improvements, Venmo debit card rewards. Goal: close the take-rate gap between Venmo and PayPal branded. Still $10–15B GMV monetization unlock available.

Fastlane & AI Checkout

Fastlane accelerated guest checkout — PayPal’s answer to Shop Pay’s one-click conversion advantage. Early merchant beta shows conversion uplift of 40%+. AI-personalized checkout flows using PayPal’s 25+ year transaction graph.

PYUSD & Crypto Rails

PayPal USD stablecoin expanded to Solana; targeting international remittances via Xoom. Not a near-term revenue driver but positions PayPal for any regulatory window on stablecoin payments in U.S. and EU.

07

The Real Risk: Transaction Margin Compression

⚠ Key Risk — Transaction Economics

The Market Isn’t Worried About Revenue. It’s Worried About Margin.

PayPal’s Q2 2026 guidance calls for transaction margin dollars down approximately 3% year-over-year. This is the number that drove the -7.86% post-earnings selloff — not the revenue miss (there was none), not the EPS miss (there was none). Transaction margin dollars are the profit PayPal extracts from each dollar of payment volume it processes, and that number declining while volume grows 11% is the definition of a business getting less efficient at monetizing growth.

The mechanics: as Braintree enterprise contracts run at lower margins, and as branded checkout (the high-monetization product) grows at 2% while Venmo (lower monetization) grows at 14%, the weighted-average take rate falls. PayPal’s “interest on customer balances” line — which benefited from higher interest rates — is also becoming a headwind as rates soften. The company is managing this with share buybacks ($1.5B/quarter at ~$50–55 means ~6% of float retired annually), but buybacks are financial engineering, not operational improvement.

The structural fix requires either branded checkout reacceleration, Venmo take-rate convergence, or enough cost savings to overpower the margin compression. Management’s FY2026 EPS reiteration (low-single-digit decline to flat vs. $5.31) implies they believe cost cuts will offset margin compression. The Q2 guide of -9% EPS suggests the back half of the year needs to do significant heavy lifting to get there.

08

The Moat — What PayPal Actually Has Left

Four years of negative narrative have obscured a real set of assets that PayPal still possesses. The question is whether those assets are sufficient moat or simply legacy infrastructure that competitors are working around.

🌐

Two-Sided Network at Scale

434 million active accounts and 35 million merchant locations. The two-sided network creates a cold-start problem for any pure challenger — you need both buyers and sellers simultaneously. PayPal already has them. Venmo’s 90M+ user base is the consumer on-ramp; PayPal’s merchant API coverage is the acceptance layer. No pure fintech challenger has cracked this combination at PayPal’s scale.

🛡

25 Years of Transaction Risk Intelligence

PayPal has processed over $13 trillion in lifetime payment volume. The fraud-detection models trained on that dataset are genuinely proprietary — not because the algorithms are secret, but because the labeled data required to train them took two decades and billions of transactions to accumulate. PayPal’s chargeback and dispute rates are meaningfully below industry averages, which is a quantifiable merchant value proposition that survives CEO transitions.

⚖️

Regulatory Licenses & Global Payments Rails

PayPal holds payment licenses in 200+ markets. The EU’s PSD2 compliance infrastructure, its e-money institution licenses across Europe, its APAC partnerships — these represent hundreds of millions of dollars of regulatory investment that cannot be replicated quickly. Stripe has been building this capability for a decade and still doesn’t have PayPal’s geographic reach. For any merchant doing cross-border payments, PayPal’s Xoom and international rails remain competitively relevant.

The honest moat assessment: PayPal’s advantages are real but defensive. They explain why the company won’t collapse, not why it will grow. The branded checkout erosion is happening at the margin — PayPal isn’t losing merchants wholesale, it’s losing checkout share within existing merchant sites as Apple Pay becomes default. That’s a slow bleed rather than a cliff, which is both more manageable and more insidious, because it’s easy to miss in quarterly numbers until the cumulative damage is severe.

09

The Bull/Bear Debate

🐂 Bull Case

“8× Earnings Is Already Pricing Permanent Decline — The Reset Creates the Opportunity”

Historically cheap: PYPL at 8.4× non-GAAP P/E against a peer average of ~30.7× prices in zero reacceleration. If Lores delivers even $0.50 in incremental EPS, the stock has 30–40% upside at current multiples without needing multiple expansion.

Buyback math is compounding: $1.5B per quarter at $50/share retires 30M shares/year against ~1.1B diluted shares. That’s 2.7% annual float reduction — before any earnings growth. EPS can rise even if net income is flat.

Venmo monetization gap is enormous: Venmo’s take rate is a fraction of branded PayPal’s. Even modest Pay-with-Venmo scale at checkout — which is growing 34% — closes the gap significantly. $10B+ of incremental transaction margin dollars is plausibly unlock-able over 3 years without needing new products.

Fastlane is the real branded checkout answer: Guest checkout converts 50–60% below logged-in checkout. Fastlane’s 40%+ conversion lift in beta means PayPal doesn’t need to “win” checkout share — it can insert itself into merchant checkout flows that previously went to Stripe, even without a PayPal login.

Lores is a cost executor, not a visionary: The market has been burned by visionary PayPal CEOs. An operator who focuses on margin discipline and capital return may be exactly what a 434-million-user commodity-risk business actually needs at this stage.

🐻 Bear Case

“Cheap for a Reason — The Core Business Is in Structural Decline and No CEO Can Fix Structural”

Branded checkout is not a “turnaround” business, it’s a secularly declining one: Apple Pay is pre-installed on 1.2B phones and grows by default with iPhone upgrades. Google Pay dominates Android. Shop Pay has merchant lock-in on Shopify’s 2M+ merchants. PayPal is fighting on three fronts simultaneously and winning on none of them.

Transaction margin compression is structural, not cyclical: Mix shift toward lower-margin Braintree/unbranded and lower-take-rate Venmo doesn’t reverse without branded checkout reacceleration. The Q2 guide of -3% transaction margin YoY is the fourth consecutive quarter of pressure.

CEO #3 in 2.5 years signals board dysfunction, not leadership pipeline: The securities class action filed in February 2026 alleges that management made misleading statements about the pace of the turnaround. The board replacing a 2.5-year CEO with an HP hardware executive suggests strategic uncertainty, not strategic clarity.

$1.5B in savings takes 2–3 years to materialize: During that window, Stripe could reach $1T in annualized TPV (it’s at ~$1.4T now), Apple Pay expands into credit, and Google Pay deepens merchant integrations. Restructuring organizations while competing against well-capitalized attackers is a historically difficult combination.

The 8× multiple may not be cheap if EPS goes to $4: If FY2026 EPS comes in at $5.00 (the low end of guidance) and FY2027 slips to $4.50 on continued margin compression, the current stock implies 11× — not actually cheap for a business with declining earnings power.

10

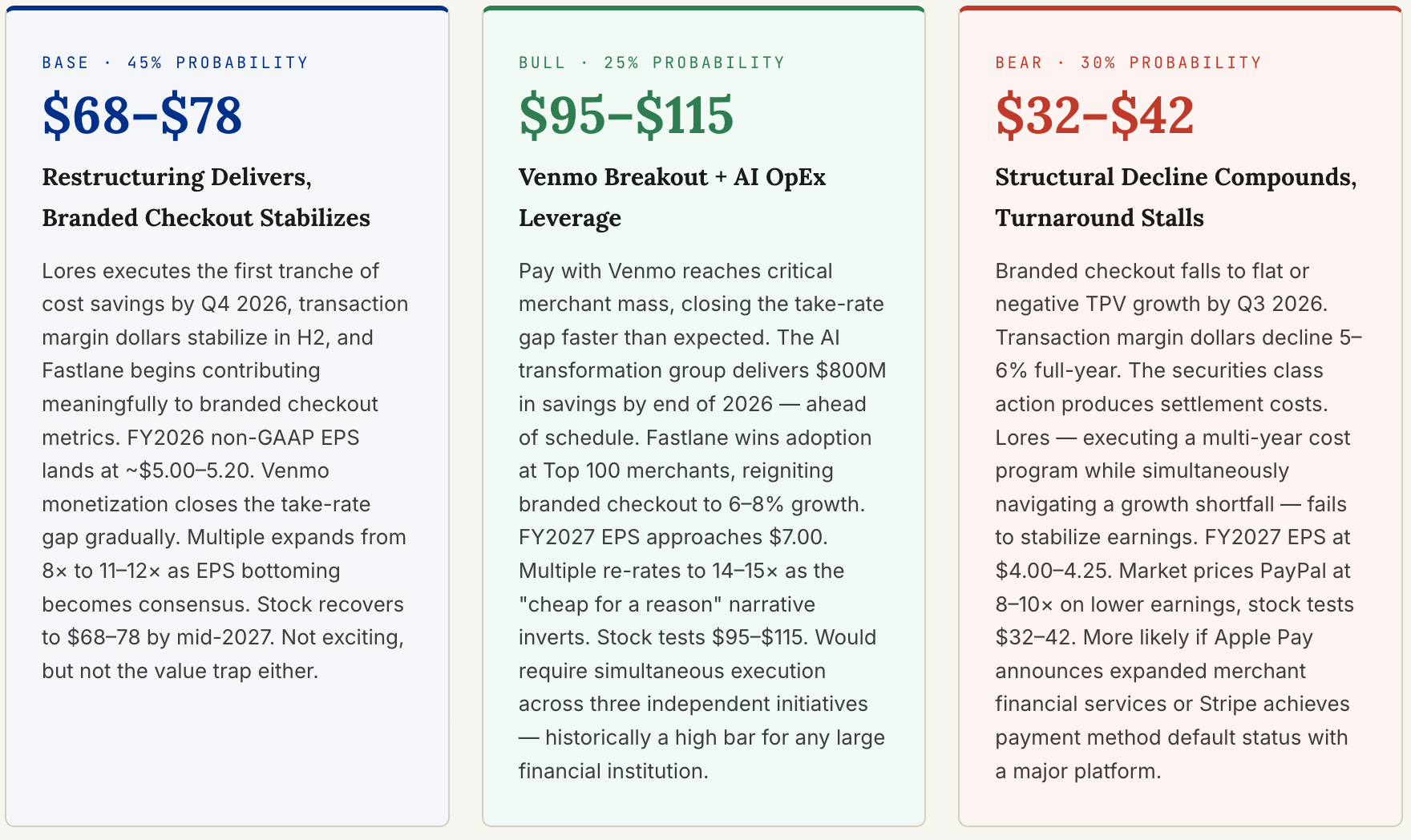

Three Scenarios Over 18 Months

The bear probability is deliberately elevated at 30%, higher than our base case for a company at this valuation. The reason: PayPal’s structural issues — the Apple Pay dynamic, the Braintree margin pressure, the CEO instability — are not fixable by balance sheet discipline alone. The bull case requires operational execution that the company has not demonstrated in four years of trying. The base case requires that Lores is indeed a different kind of leader than Schulman or Chriss. That’s a judgment call the market is currently making at an 8× earnings price, which is either the most obvious contrarian opportunity in fintech or the most obvious value trap.

The Bottom Line

The Most Interesting Uninteresting Stock in Payments

PayPal is the kind of company that makes smart investors argue at dinner. The bull case is obvious: 8× earnings, $6B in annual buybacks, 434 million users, a Venmo franchise growing at double digits, and a new CEO who has executed exactly this playbook before at a different kind of company. The bear case is equally obvious: secular checkout share loss, transaction margins declining for the fourth straight quarter, CEO #3 in 2.5 years, and a securities class action suggesting the prior management team misled the market on the pace of the recovery.

What makes it genuinely interesting is the asymmetry of information. The bull case is entirely priced out — zero premium for Venmo monetization, zero premium for Fastlane, zero premium for the buyback math. If Lores delivers even 60% of his targets, the stock has substantial upside from $50. The bear case requires that the structural decline is faster and deeper than what’s visible in current numbers, which is possible but requires believing that Apple Pay and Stripe can erode an asset as large as PayPal’s two-sided network on a 3-year timeline. That’s a bolder claim than it sounds.

The most likely outcome — and the reason this goes into the base case at 45% — is that PayPal becomes a capital-return story rather than a growth story. Buybacks at this price are genuinely value-accretive in a way that buybacks at $200+ never were. A flat-to-slightly-growing EPS base with 6–7% annual float reduction produces respectable shareholder returns even without multiple expansion. The question is whether the market is patient enough to let that play out — or whether each successive quarter of branded checkout deceleration pushes the stock to new lows before the turnaround has time to work.

Enrique Lores has three months of data and a $41 billion company to prove that the answer is neither. That’s a hard job. But at 8× earnings, you’re not being asked to believe he’ll make PayPal great again — just that he’ll stop making it worse.