Plug Power: Burning Toward Viability

The turnaround metrics are real. The credibility deficit is not yet healed.

Plug Power has been two years from profitability for a decade. Today — with its first-ever CEO change, a finalized 45V hydrogen tax credit, a $1.66B DOE loan in the bank, and genuine margin improvement — the company finally has what it says it always needed. The question is whether it can survive long enough to collect. Q1 2026 beat estimates and the stock surged 13%. But the accumulated deficit just crossed $8.47 billion, unrestricted cash stands at $223 million, and the company still burns $150 million per quarter in operations. This report does the math the press release doesn't.

Q1 2026 · Full Scorecard

The Quarter: What the Numbers Actually Say

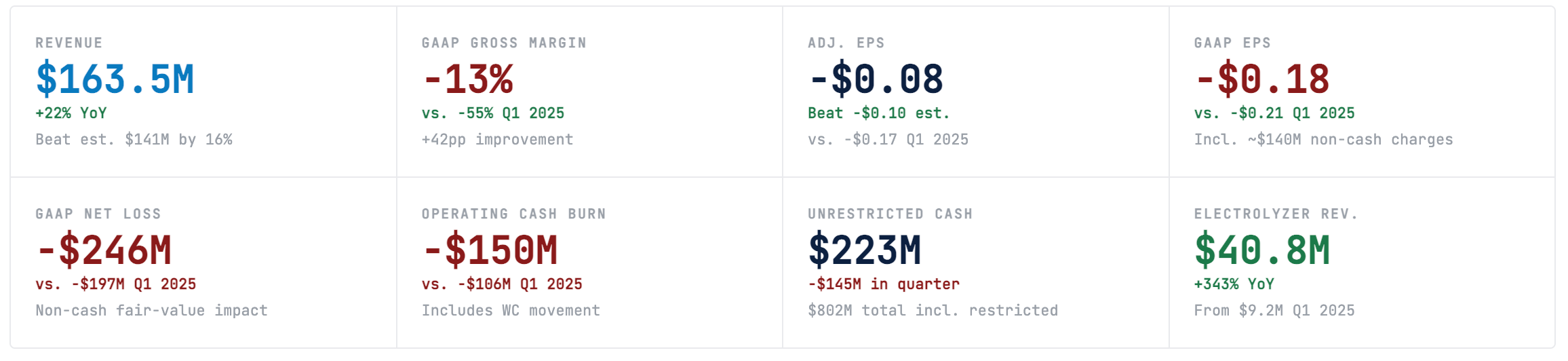

On the surface, Q1 2026 was Plug Power’s cleanest beat in recent memory. Revenue of $163.5 million beat the Street’s $141 million estimate by 16%. Adjusted EPS of -$0.08 beat the -$0.10 consensus. Gross margin improved by 42 percentage points year-over-year — a legitimate structural improvement, not an accounting reclassification. CEO Jose Luis Crespo, making his debut as chief executive after taking over from Andy Marsh in March 2026, called it a “meaningful inflection.” For once, the claim is not entirely without foundation.

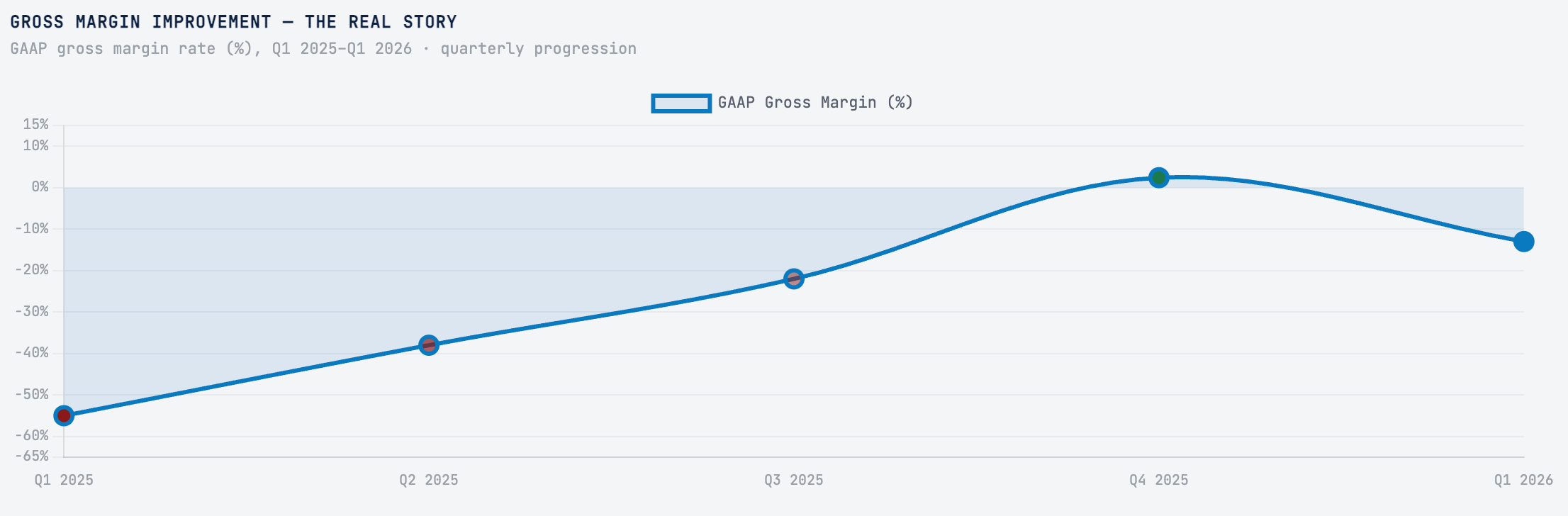

But context is necessary. The GAAP net loss was $246 million — worse than Q1 2025’s $197 million loss, inflated by $70.8M in non-cash convertible debt fair-value charges and $54.6M in warrant liability markups triggered by the stock price rally. Operating cash burn was $150 million, up from $106 million a year ago. Unrestricted cash fell from $368.5M to $223.2M in a single quarter. The business is genuinely improving — gross margin trending from -55% to -13% is not noise — but the runway calculus remains the headline investors must confront.

Leadership Transition · March 2026

The Marsh Era Ends. Crespo’s First Quarter.

Andy Marsh joined Plug Power as CEO in 2008 and led the company for nearly 18 years, becoming one of the hydrogen industry’s most prominent — and most criticized — evangelists. In October 2025, the board named Jose Luis Crespo, Plug’s longtime Chief Revenue Officer and architect of its $8B+ electrolyzer pipeline, as incoming CEO. Crespo took the title officially in March 2026; Marsh became Executive Chair. This is Crespo’s first full quarterly earnings. His message was disciplined: execution over vision, margin improvement over grand proclamations. Whether the style change translates to a credibility recovery with skeptical investors remains the open question.

Revenue Analysis

Revenue Trend & Segment Breakdown

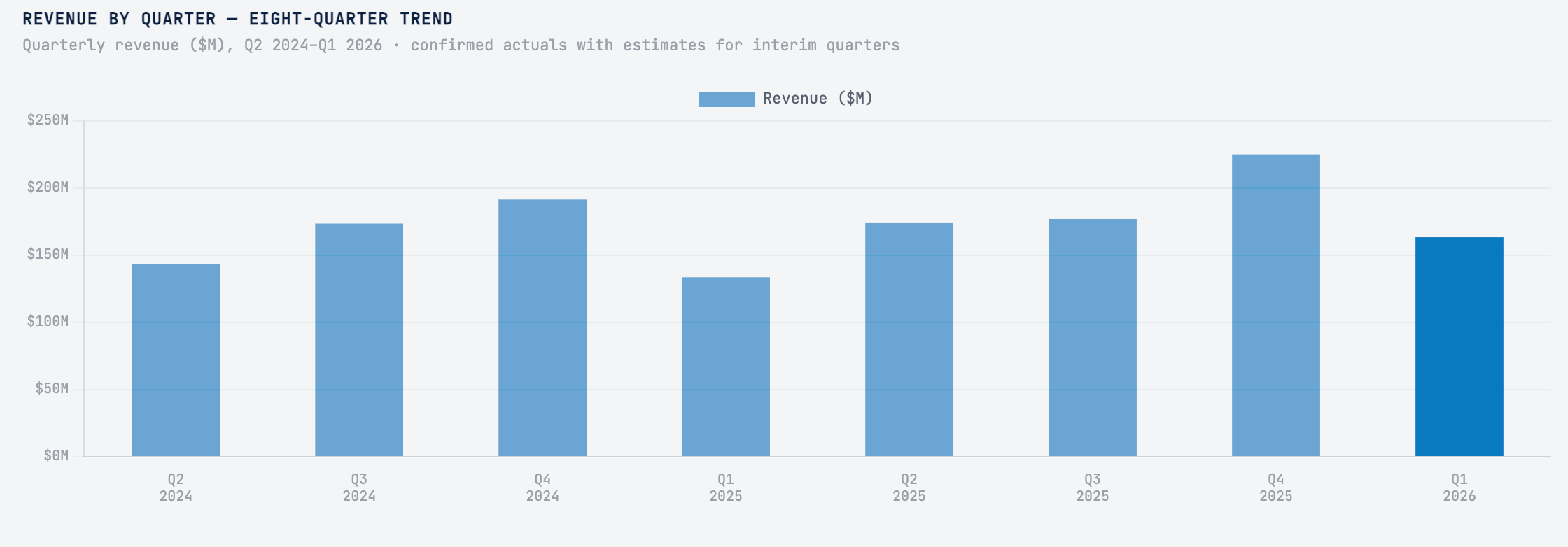

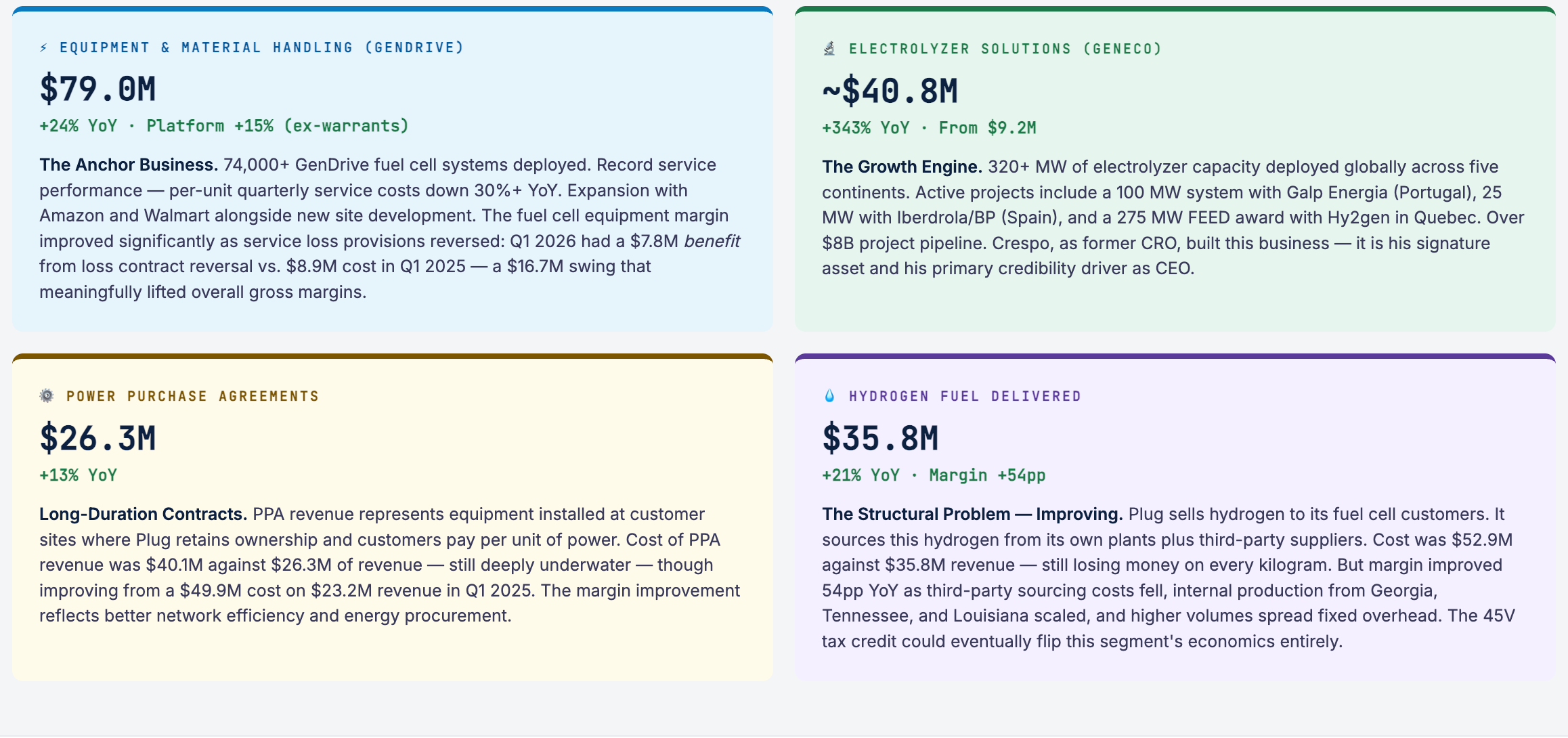

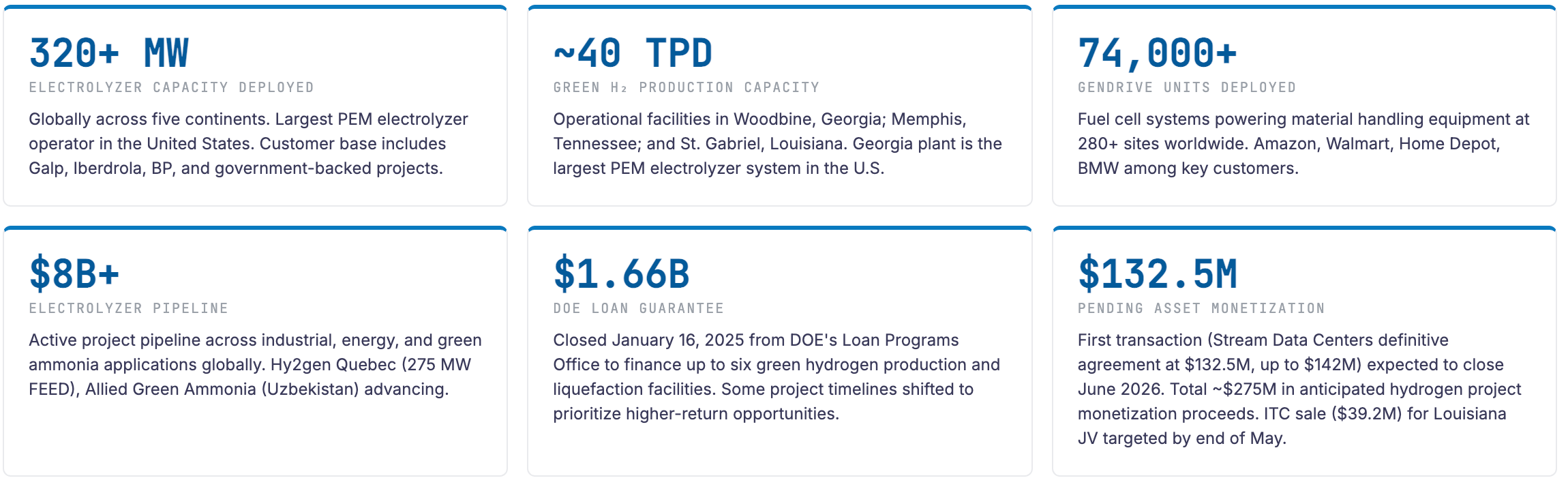

Plug’s revenue trajectory tells a story of genuine — if lumpy — growth. The business has more than tripled from its 2020 levels, though it has done so in fits and starts: a brutal Q1 2025 dip following a massive Q4 2024 write-down cycle, followed by a recovery that accelerated through 2025 and now into 2026. The Q1 2026 result of $163.5M is the highest Q1 in company history, driven by the electrolyzer business erupting to over $40M from single-digit levels a year ago.

Plug now operates three distinct revenue platforms. The material handling business (GenDrive fuel cells powering forklift fleets at Amazon, Walmart, Home Depot) remains the backbone — stable, growing 15% YoY, and now generating improved per-unit margins after 30%+ reduction in quarterly service costs per GenDrive unit. The electrolyzer business (GenEco) is the growth engine, exploding 343% as megawatt-scale projects with global energy majors begin to recognize revenue. The hydrogen fuel business is the structural challenge — Plug sells hydrogen at a loss because its production cost is still above market, though the margin improved 54 percentage points as network utilization increases.

Infrastructure · Production Network

What Plug Is Actually Building

Strip away the quarterly EPS noise, and Plug Power is fundamentally an infrastructure buildout story. The company is attempting to construct the first vertically integrated green hydrogen ecosystem in North America — owning the electrolyzers that split water, the plants that liquify and store the hydrogen, the trucks that deliver it, and the fuel cells that consume it. No company has ever done this at scale. The question is whether Plug can afford to finish what it started

The DOE Loan: A Lifeline With Strings

The $1.66B DOE loan guarantee, closed in January 2025, was supposed to fund up to six hydrogen production plants. In late 2025, Plug suspended work on several of those plants, describing the decision as “reallocating capital to higher-return opportunities.” This is a meaningful pivot: the DOE loan is government money with government strings — delays and project changes require DOE approval. Plug is now pursuing what it calls “asset monetization,” selling completed or in-progress infrastructure to data centers and industrial partners who need reliable green energy. The Stream Data Centers deal ($132.5M definitive, up to $142M) is the first proof of concept. If successful, this strategy turns CAPEX into cash — but it also means Plug does not fully control its own production network.

The Georgia plant — Plug’s flagship — was supposed to be producing 15 metric tons per day of liquid hydrogen by early 2024. It is now part of a combined ~40 TPD network across three states. That production capacity is critical for two reasons: it directly serves the company’s material handling customers (who need hydrogen to run their forklift fleets), and it is the primary asset that benefits from the 45V production tax credit. Higher utilization means lower cost per kilogram. Lower cost per kilogram means the fuel segment’s chronic losses shrink. At scale — something Plug hasn’t reached yet — the economics theoretically flip to profitable.

Policy · The Make-or-Break Regulation

The 45V Tax Credit: The Reason Plug Is Still in This Game

The clean hydrogen production tax credit, Section 45V of the Internal Revenue Code, is arguably the single most important external variable in Plug Power’s investment thesis. Finalized by the Treasury Department on January 10, 2025, it creates a 10-year production incentive of up to $3.00 per kilogram of clean hydrogen — for producers that generate hydrogen at the lowest carbon intensity levels using clean electricity.

The math is transformational if — and only if — Plug can produce hydrogen at sufficient scale and carbon purity to qualify for the top credit tier. Green hydrogen produced via PEM electrolysis powered by renewable electricity can qualify for the $3/kg credit. At 40 tons per day of production, a $3/kg credit translates to roughly $44 million per year in tax credit value at full utilization. Scale that to 200 TPD — Plug’s aspirational network target — and the credit alone would generate over $200 million annually in economic benefit.

What the Final Rule Actually Says

The finalized 45V rule establishes annual temporal matching through 2029 — meaning clean electricity and hydrogen production must match within the same calendar year. Starting in 2030, matching becomes hourly, which is a significantly more demanding standard that requires either dedicated renewable capacity or sophisticated grid accounting. For 2026, Plug qualifies under the more lenient annual standard. The final rule also restricts the “book and claim” accounting system until after 2026, requiring direct pipeline connections for some hydrogen credit types in the near term. Plug’s owned production infrastructure — its actual plants — positions it better than pure electrolyzer sellers to capture these credits.

The 45V Political Risk: Not Yet Safe

The 45V credit was finalized under the Biden administration in January 2025. While it is now law, the current political environment has not been uniformly friendly to clean energy subsidies. The IRA’s clean energy provisions have faced scrutiny, and implementation challenges around the additionality and temporal matching requirements create ongoing uncertainty. Additionally, Plug must actually generate the qualifying hydrogen to capture the credits — which requires its production plants to operate efficiently and at scale. A hydrogen plant running at 40% utilization collecting Tier 4 credits is very different from a plant running at 85%. The credit is real; the execution of collecting it is the next test.

The current cost of green hydrogen production — without any subsidy — is roughly $5–$8 per kilogram, versus $1–$2 for conventional gray hydrogen made from natural gas. The 45V credit, at its maximum, closes most of that gap. This is why the credit’s finalization was so significant for Plug: for the first time, green hydrogen has a credible path to cost parity with the incumbent. Plug has positioned itself to be the primary American beneficiary of that parity shift — if it can stay solvent long enough for the policy to deliver.

Risk · Liquidity Analysis

The Cash Problem: $8.47 Billion in Losses and Counting

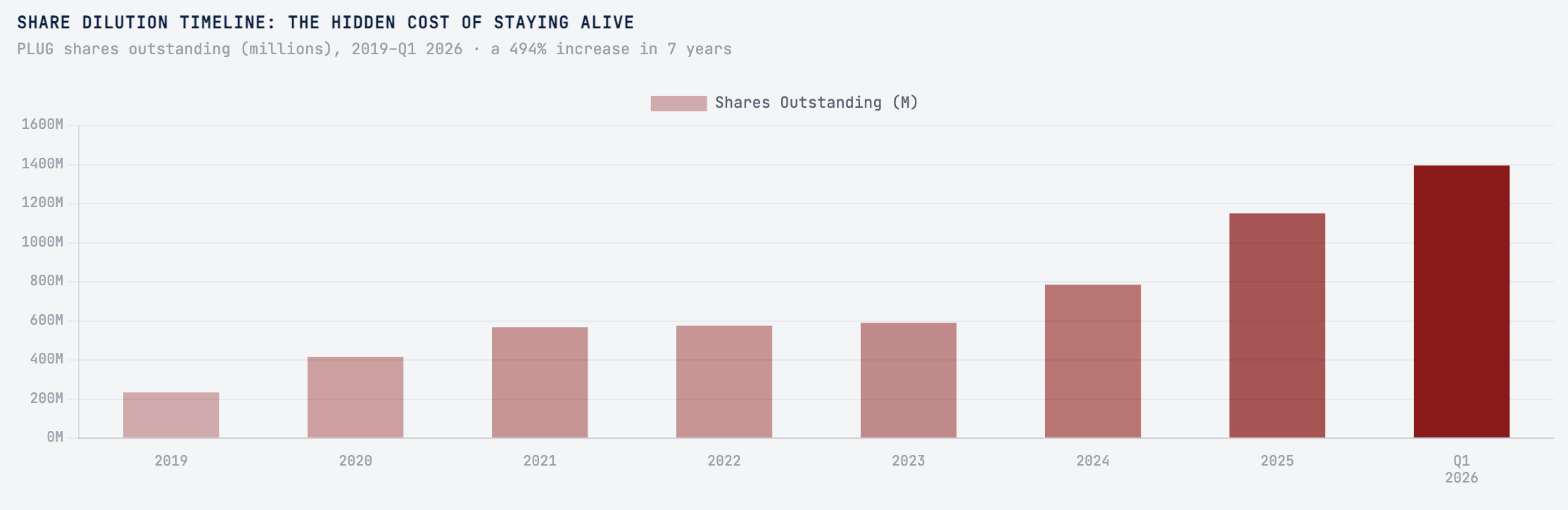

Plug Power has now accumulated $8.47 billion in net losses since inception. Its shares outstanding have grown from 234 million in March 2019 to 1.39 billion as of Q1 2026 — an increase of 494% in seven years, with the most dramatic dilution occurring in 2024–2025 as the company raised emergency capital to avoid insolvency. The going-concern warning issued in November 2023 — formally acknowledging that the company’s survival was not guaranteed — was eventually resolved through the DOE loan closing and equity raises in 2025. But the underlying dynamic has not fundamentally changed: Plug continues to consume more cash than it generates.

Going Concern: Formally Resolved, But Not Forgotten

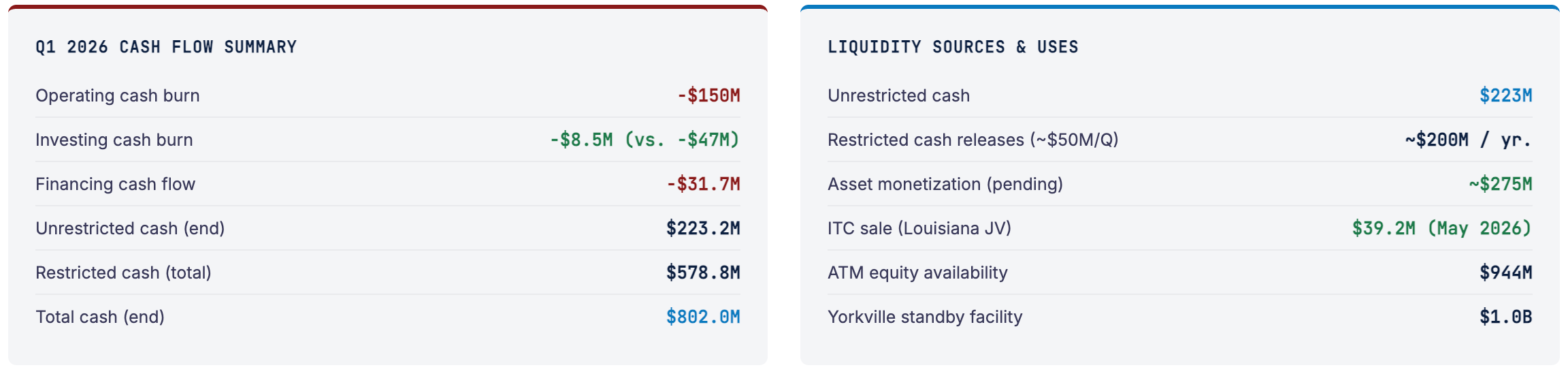

In November 2023, Plug Power disclosed substantial doubt about its ability to continue as a going concern — a devastating acknowledgment for any public company. The warning was triggered by accelerating cash burn, missed revenue targets, hydrogen supply disruptions, and an inability to raise capital on favorable terms. The company survived through a combination of the $1.66B DOE loan guarantee (conditional at first, closed January 2025), a $431M convertible note offering (November 2025), a $276M equity raise (Q1 2025), and the ATM equity program. The going-concern language has been removed. But the structural issues it reflected — negative gross margins, heavy cash burn, reliance on external capital — have only partially improved. The company still has $944M in ATM equity availability and a $1B Yorkville standby facility. That firepower exists for a reason: management expects to need it.

The restricted cash figure — $578.8 million — deserves explanation. This is cash pledged as collateral for various debt and financing obligations. It is Plug’s money, but Plug cannot spend it freely. It releases at roughly $50 million per quarter as underlying obligations roll off. This creates a mechanical liquidity improvement as quarters pass — but it also means the “headline” $802M cash figure is misleading. The spendable cash is $223 million. At a $150M quarterly operating burn rate (and much of that can’t be immediately reduced without cutting the business), the company has less than two quarters of unrestricted liquidity before needing to tap the asset monetization proceeds, the ATM, or additional financing.

The Dilution Math: Shares as a Financing Mechanism

As of March 31, 2026, Plug Power has 1.395 billion shares outstanding — up from 945 million a year ago. Shareholders approved doubling authorized common stock to 3 billion shares in February 2026, explicitly to create room for future capital raises. The company still has $944 million available under its ATM program. The convertible notes due 2033, if fully converted, would add another ~125 million shares. Every dollar of capital raised via equity at current prices (~$2.90/share) represents meaningful dilution to existing holders. The accumulated deficit of $8.47 billion means that even in a successful scenario, equity holders have collectively funded nearly a decade of losses — and more funding is coming.

Track Record · Guidance vs. Reality

The Credibility Problem: A Decade of Promised Tomorrows

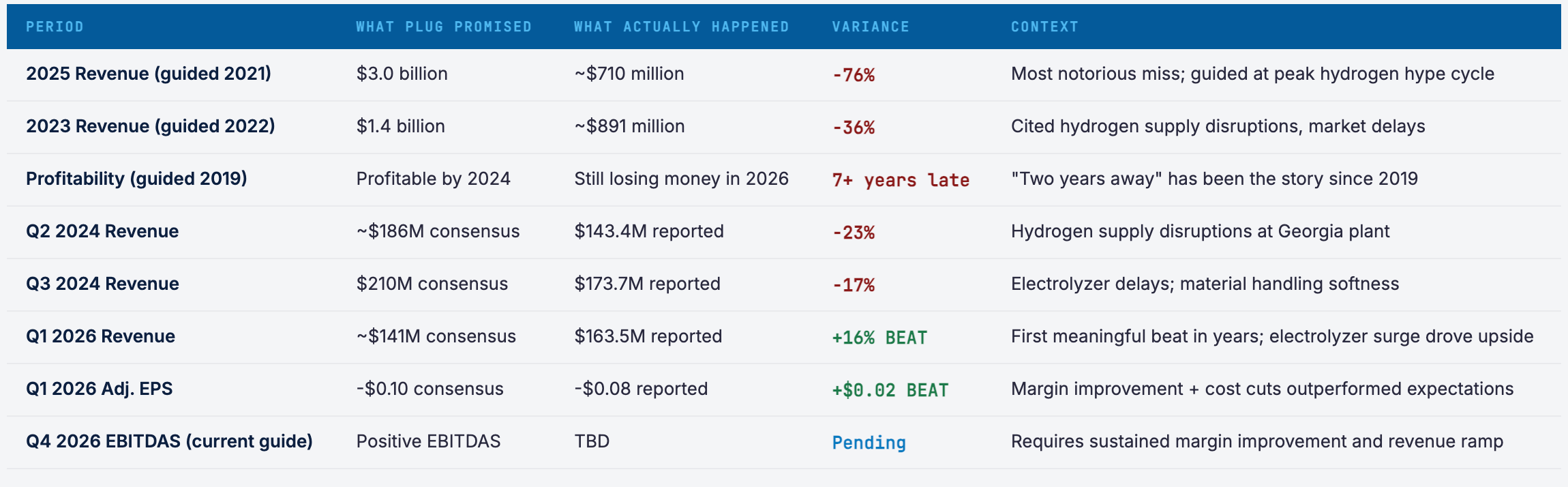

No analysis of Plug Power is complete without confronting its guidance history. The company has, in 16 of 17 recent quarters, reported GAAP EPS worse than analyst expectations — and analysts were already expecting losses. More damning are the long-range targets: in October 2021, Plug guided Wall Street to $3 billion in annual revenue by 2025. The actual 2025 revenue was $710 million — a 76% miss. In 2022, it guided for $1.4 billion in 2023 revenue; actual was roughly $891 million. The pattern is consistent: ambitious targets, enthusiastic capital raises, missed execution, revised targets.

Q1 2026 is the first time in recent memory that Plug actually beat revenue estimates meaningfully. Whether this represents a genuine inflection or simply better-calibrated expectations from a Wall Street that has learned to set the bar low is the key interpretive question.

The new CEO Crespo has, notably, avoided the grandiose long-range promises that defined the Marsh era. His Q1 2026 commentary focused on near-term metrics: margin improvement, cash flow reduction, Q4 EBITDAS target. This is a more defensible posture — but it also means the bull case is now built on quarterly execution rather than transformational vision. That is progress, but it is also a lower bar than what investors were once asked to believe in.

“Our first quarter results reflect strong commercial execution and continued progress improving the underlying economics of the business and positions us to achieve our EBITDAS positive target in Q4 2026.”

— Jose Luis Crespo, CEO, Plug Power · Q1 2026 Earnings Release · May 11, 2026

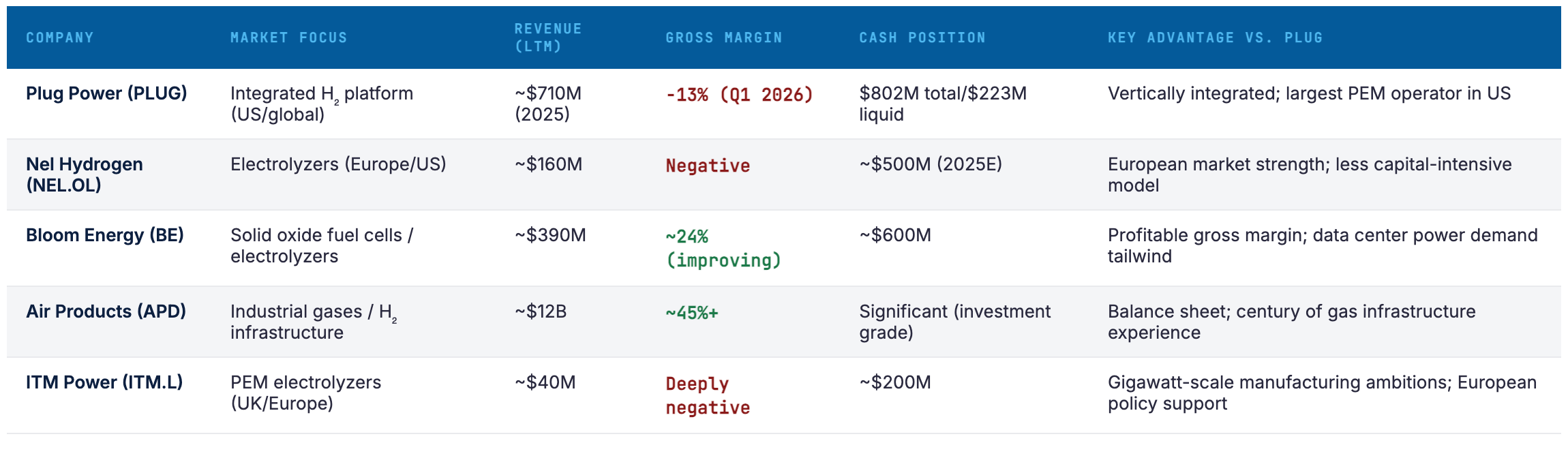

Competitive Context

Where Plug Stands in the Hydrogen Ecosystem

Plug Power occupies a unique position: it is the only company attempting to be simultaneously an electrolyzer manufacturer, a hydrogen producer, a fuel delivery network, and a fuel cell end-use deployer. Competitors tend to specialize. Understanding how Plug stacks up requires separating the electrolyzer business (where it competes with Nel, ITM, and increasingly traditional industrial gas players) from the integrated hydrogen platform (which has no direct comparables).

The most important competitive dynamic is the emergence of traditional energy companies — Air Products, BP, Shell, TotalEnergies — as hydrogen infrastructure players with far larger balance sheets than Plug. These companies can fund hydrogen plants without DOE loans and can absorb startup losses that would threaten Plug’s solvency. The bull case for Plug is that its technological and deployment head start — 320+ MW already in the field, 74,000+ fuel cell units running, 40 TPD of production — creates a moat that slower-moving incumbents cannot quickly close. The bear case is that once hydrogen becomes commercially viable (aided by 45V), those same incumbents use their capital advantages to commoditize the business Plug built.

Investment Analysis

Bull Case vs. Bear Case: The Argument in Full