Rheinmetall AG: Defense Supercycle or Expectations Trap?

Record Backlog, Rising Capacity, and the Economics of a More Militarized World

Disclaimer: This report is for informational purposes only and does not constitute investment advice, a recommendation, or a solicitation to buy or sell any security. All data is sourced from public filings, earnings releases, and third-party research

Executive Summary

Rheinmetall delivered record financial results for fiscal year 2025 — revenue of €9.9 billion (+29%), operating profit of €1.84 billion (+33%), and a backlog that surged 36% to €63.8 billion. Yet the stock fell more than 7% on the day of release. The gap between operational strength and market reaction frames the central question of this analysis: Is Rheinmetall a long-duration defense compounder sitting at the centre of Europe’s structural rearmament, or a company whose stock already prices in too much perfection?

This report examines the latest results, demand visibility, capacity constraints, financial quality, and valuation to answer that question. The conclusion is that the business is fundamentally stronger than the market reaction implies — but investors must carefully distinguish between real industrial value creation and narrative-driven momentum. Rheinmetall is not just a defense stock. It is becoming an industrial bottleneck in Europe’s security infrastructure, and that distinction matters.

01

Record results, record expectations. Revenue and operating profit hit all-time highs, but 2026 guidance of €14.0–14.5B missed consensus near €15B. The stock’s 7% drop was about expectations, not fundamentals.

02

Backlog provides extraordinary visibility. At €63.8B — over six years of current revenue — Rheinmetall has demand visibility most industrials can only dream of. Management expects backlog to approach €135B by end of 2026.

03

Cash conversion is the real debate. Operating free cash flow of €1.2B improved 15% but 2026 guidance of >40% FCF conversion disappointed a market expecting 70–90%. Capacity investment absorbs cash before it generates returns.

04

Europe’s rearmament is structural, not cyclical. Germany alone will add €400B+ in defense spending over the next five years. NATO’s 3.5% GDP target by 2035 creates a multi-decade procurement runway.

05

Rheinmetall is a factory story now. The investment case rests less on order announcements and more on whether new ammunition, vehicle, and naval capacity can convert demand into timely, margin-quality output.

06

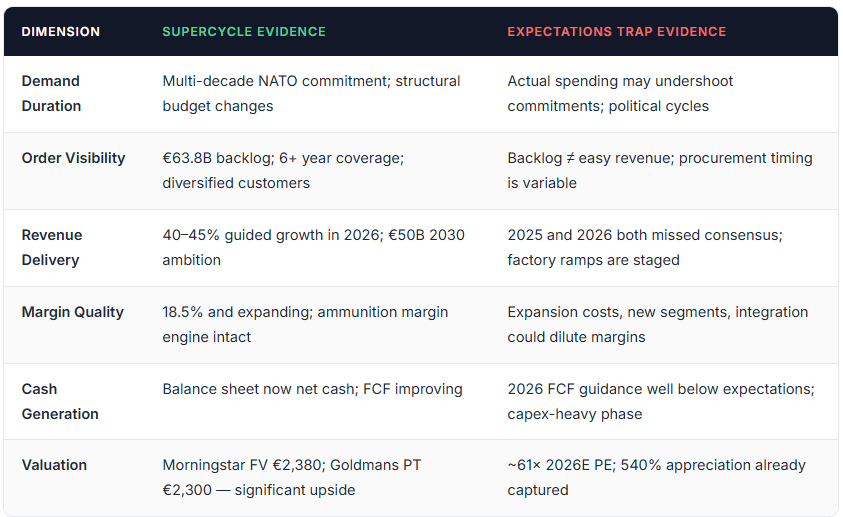

Valuation demands discipline. Trading around 61× forward 2026 earnings, the stock leaves limited room for execution slippage. This is a strong business where the stock requires strong performance just to hold its price.

Section I

Why Rheinmetall Matters Now

For decades, European defense was an afterthought. Governments cashed the “peace dividend,” drew down arsenals, and let industrial defense capacity atrophy. The assumption was that major land warfare in Europe was a historical artefact. Russia’s full-scale invasion of Ukraine in February 2022 destroyed that assumption — and with it, the entire planning framework on which European security had rested for thirty years.

What followed was not just a political shift but an industrial one. European governments discovered that their ammunition stockpiles could sustain weeks — not months — of high-intensity warfare. Artillery shell production across NATO Europe was measured in the low hundreds of thousands of rounds per year, while Ukraine was consuming that volume in months. Armored vehicle fleets had been thinned to skeleton levels. Air-defense systems were in short supply. And the industrial base that could produce these capabilities had been allowed to shrink to near irrelevance.

This is the context that elevated Rheinmetall from a mid-cap German industrial to one of the most strategically important listed defense companies in Europe. Rheinmetall produces the things Europe most urgently needs: artillery ammunition, armored vehicles, air-defense components, and the industrial capacity to scale them. It is not simply a beneficiary of rising defense budgets — it is a production bottleneck in Europe’s security supply chain.

Germany, the largest economy in Europe, has committed to a constitutional reform of its fiscal rules that will unlock up to €500 billion in additional defense spending over the coming decade. The country’s defense budget is set to rise from €86 billion in 2025 to €108 billion in 2026, with a trajectory toward €162 billion by 2029. Germany accounted for 38% of Rheinmetall’s 2025 sales. NATO has agreed to a new spending target of 3.5% of GDP by 2035, up from the 2% that most allies only recently met. EU member states collectively spent €381 billion on defense in 2025 — a 62% increase from 2020 — and investment spending reached nearly €130 billion.

This is not a one-year story. It is a structural repricing of how much the Western world spends on defense, and Rheinmetall sits at the intersection of where the money must go: ammunition, vehicles, air defense, and electronics.

Section II

What the Latest Results Actually Show

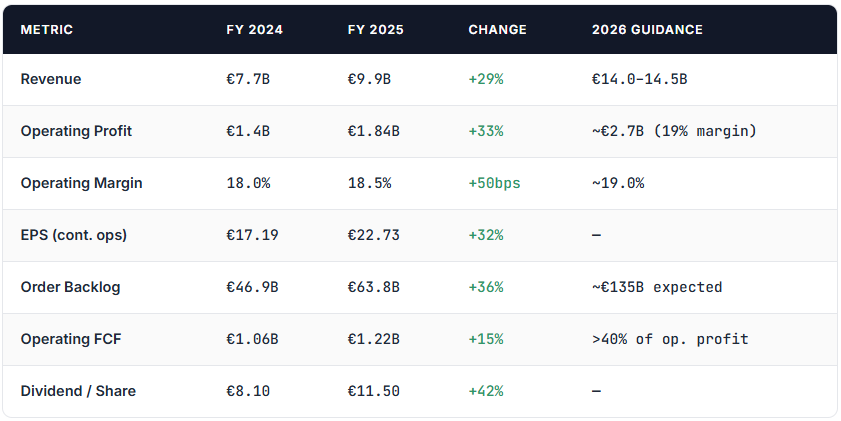

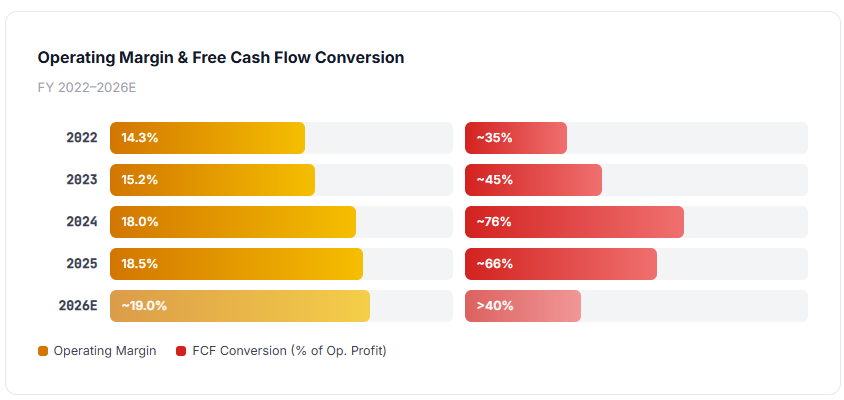

Rheinmetall’s FY 2025 annual results, reported on March 11, 2026, were by any absolute measure the strongest in the company’s history. Revenue grew 29% to €9.935 billion. Operating profit rose 33% to €1.841 billion. The operating margin expanded 50 basis points to 18.5%. Earnings per share from continuing operations climbed to €22.73 from €17.19. The dividend was raised 42% to €11.50, with a payout ratio of 45.5%.

And yet, the stock dropped more than 7% on the release, closing at €1,519. Why?

The answer lies entirely in relative expectations. FY 2025 revenue of €9.9 billion missed LSEG consensus of €10.5 billion. The fourth quarter specifically generated €2.42 billion, roughly 7% below Jefferies’ estimate. More importantly, the 2026 revenue guidance of €14.0–14.5 billion — representing 40–45% growth — fell short of consensus near €15 billion. The margin outlook of approximately 19% was below the 19.6% the market had pencilled in. And the free cash flow conversion guidance of greater than 40% of operating profit landed well below market expectations of 70–90%.

This is a critical distinction: the business did not disappoint. The stock did. The underlying operational trajectory — record sales, record margins, record backlog, healthy dividend growth — would be enviable for any industrial company. The reaction reflects a market that has priced Rheinmetall for perfection and punishes anything short of it.

Key Insight

The guidance miss was largely attributable to German procurement approvals slowing during the federal election period and a multibillion-euro artillery contract being sent back for procedural review — timing issues rather than demand shortfalls. Goldman Sachs, JPMorgan, and Morningstar all maintained or raised their positive assessments following the results.

Section III

Backlog, Guidance, and Demand Visibility

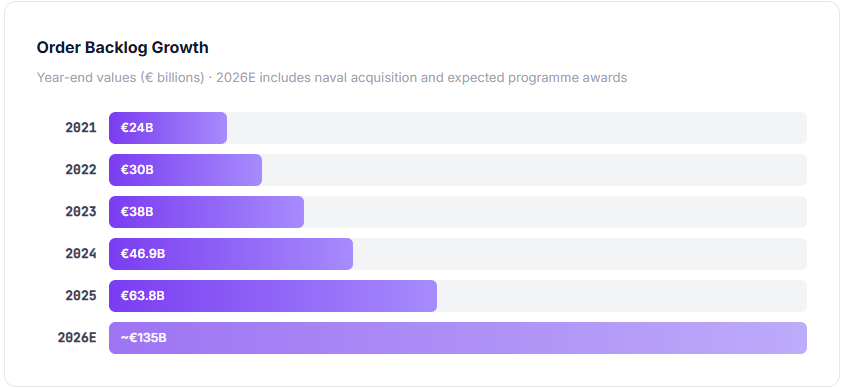

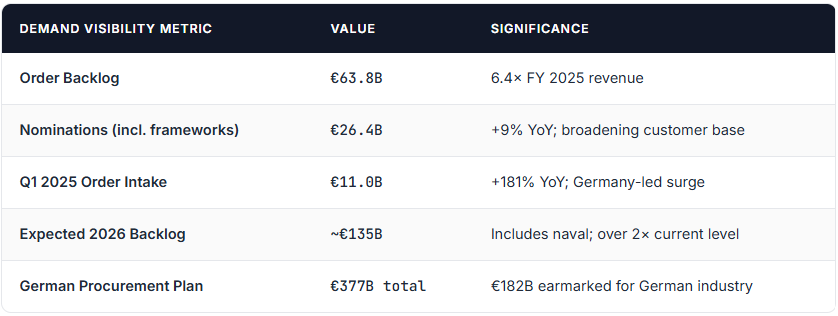

Rheinmetall’s order backlog reached €63.8 billion at year-end 2025, up 36% from €46.9 billion a year earlier. This represents more than six years of current annual revenue — an extraordinary level of demand visibility for any industrial company. Nominations (which include framework agreements alongside firm orders) rose 9% to €26.4 billion. In Q1 2025 alone, order intake surged 181% to €11.0 billion, propelling the backlog above €62 billion as early as March 2025.

Management’s most striking forward-looking statement was that backlog could more than double to approximately €135 billion by the end of 2026, driven by European rearmament programmes, the newly acquired naval systems business (which adds €5–6 billion immediately), and Germany’s planned procurement programme valued at €377 billion, of which €182 billion is earmarked for German companies.

The Electronic Solutions segment saw the most dramatic booking surge: total bookings, including framework agreements, reached €14.2 billion — more than double the prior year. Nordic NATO members — Denmark, Finland, Norway, and Sweden — were among the most active buyers. The breadth of order sources provides diversification beyond any single programme or government.

Backlog Is Not the Same as Easy Revenue

A €63.8 billion backlog is impressive on paper, but investors must resist the temptation to treat it as guaranteed revenue. Defense backlogs are not like consumer subscriptions. They are subject to government procurement timelines — which can shift with elections, budget reviews, and bureaucratic procedure. The guidance miss itself was partly caused by a German artillery contract being returned for procedural review, illustrating how administrative process can delay even committed demand.

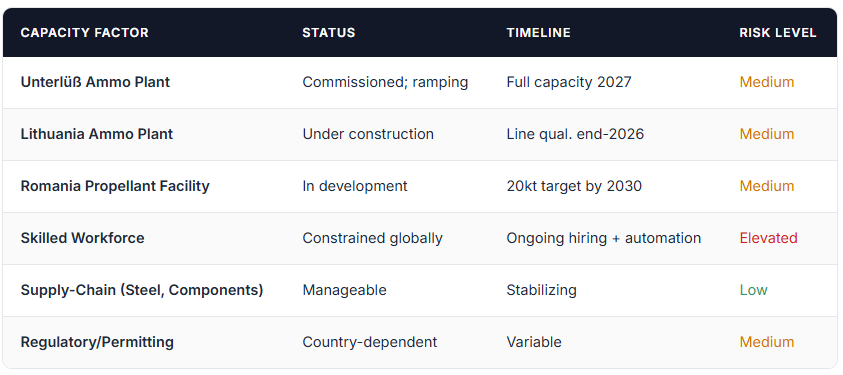

Furthermore, converting backlog into revenue requires production capacity. Rheinmetall is investing heavily to expand, but factory ramp-ups take time. The Unterlüß ammunition plant, Europe’s largest, was commissioned in mid-2025, but its ramp profile is staged: approximately 25,000 rounds in 2025, 140,000 in 2026, and full capacity of 350,000 by 2027. The gap between orders received and orders fulfilled is where execution risk lives. Backlog provides exceptional visibility into demand. It does not provide certainty of delivery timing or margin quality.

Section IV

How Rheinmetall Fits the New Defense Era

The rearmament underway in Europe is not a reaction to a single conflict. It is a repricing of the cost of security across the Western world. NATO’s new 3.5%-of-GDP target, agreed at The Hague in June 2025, effectively doubled the previous spending commitment. Germany’s constitutional reform to exempt defense from its debt brake represents the most significant fiscal-policy shift in modern German history. EU defense investment spending is projected to reach €130 billion in 2025 alone — a 42% increase over the prior year.

What makes Rheinmetall’s position distinctive is the breadth of its exposure to the categories of spending that matter most. Europe does not primarily need stealth fighters or aircraft carriers. It needs the industrial sinew of ground-based deterrence: artillery ammunition in volumes that can sustain high-intensity operations, modern armored vehicles to replace Cold War-era fleets, integrated air-defense systems to protect critical infrastructure, and the sensors, electronics, and command systems that connect them.

Rheinmetall produces all of these — and in several categories, it is the only European manufacturer operating at the necessary scale. This is not a company riding a broad defense-spending tide. It is a company that makes the specific products that Europe’s military shortfalls demand most urgently.

The persistence of the demand signal matters. Even if the war in Ukraine were to end tomorrow, the stockpile replenishment requirement alone would sustain years of ammunition production. The armored vehicle replacement cycle across Germany, the Nordics, and Eastern Europe is a decade-long programme. Air-defense demand is only accelerating as drone warfare makes point-defense systems essential. Rheinmetall benefits not just from one conflict, but from a broad shift toward sustained military readiness and domestic defense industrial self-sufficiency.

Section V

The Industrial Reality: Capacity, Supply Chains, and Execution

If the last three years were about orders, the next three are about factories. Rheinmetall’s investment case has shifted from demand validation to production execution. The market no longer asks whether the orders exist; it asks whether Rheinmetall can build fast enough, at sufficient quality, without destroying margins.

The centrepiece of the capacity expansion is the Unterlüß ammunition facility, built in just 15 months and opened in August 2025. It is now Europe’s largest artillery ammunition plant, with a target capacity of 350,000 155mm rounds per year at maturity in 2027. But the ramp is staged: 25,000 rounds during commissioning in 2025, 140,000 in 2026, and full output only in 2027. This is realistic, but it means revenue conversion from ammunition orders will be backloaded.

Beyond Unterlüß, Rheinmetall is expanding production in Lithuania, Latvia, Estonia, Denmark, and soon Ukraine. A new propellant-powder facility in Romania addresses what management describes as a strategic bottleneck — propellant supply — with a target of 20,000 tonnes of annual capacity by 2030. Capital expenditure ran at 7.8% of sales in 2025, and management expects elevated levels to continue before normalizing to 5–6% as major projects complete.

The workforce dimension is frequently underestimated. Rapid scale-up requires qualified engineers, technicians, and manufacturing operators. Automation helps, but integration of new production technology still demands skilled staff. Regulatory approvals for ammunition production add further lead time. These are not dramatic risks — they are the normal industrial friction of scaling a complex manufacturing business at speed.

Why Rheinmetall Is a Factory Story

Defense is now an industrial delivery challenge, not just an order-book story. The market has already priced in the demand. What will differentiate Rheinmetall’s shareholder returns from here is the pace, quality, and margin discipline of production conversion. Investors should monitor factory milestones at least as closely as new contract announcements.

Section VI

Financial Quality: Margins, Cash Flow, and Balance Sheet

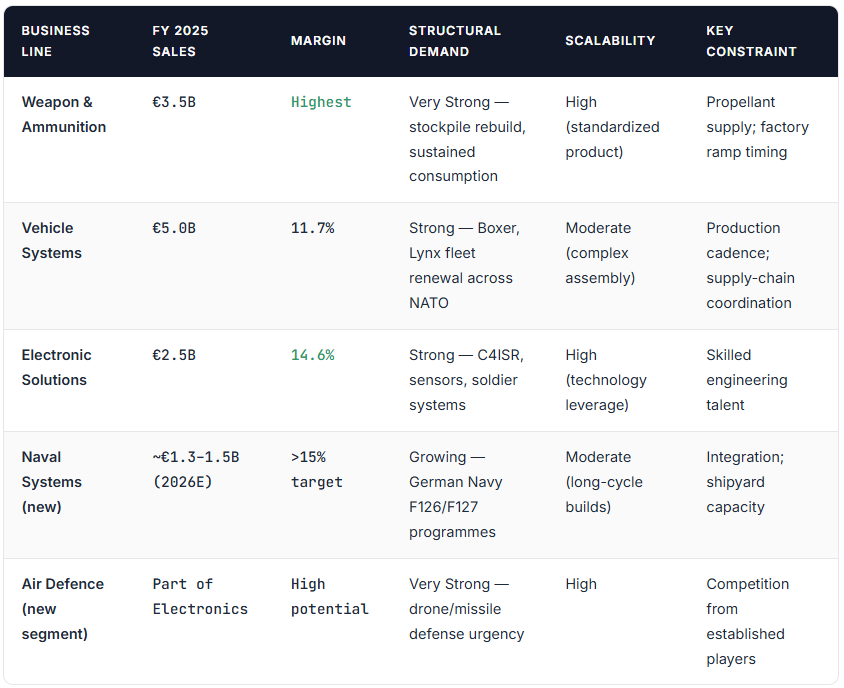

Rheinmetall’s margin trajectory is genuinely impressive. Operating margin expanded to 18.5% in 2025 from 18.0% in 2024, with guidance pointing to approximately 19% for 2026. The ammunition division remains the margin engine, benefiting from high-volume production of standardized rounds, while Electronics Solutions margins expanded sharply from 12.6% to 14.6%. Vehicle Systems margins improved modestly to 11.7%.

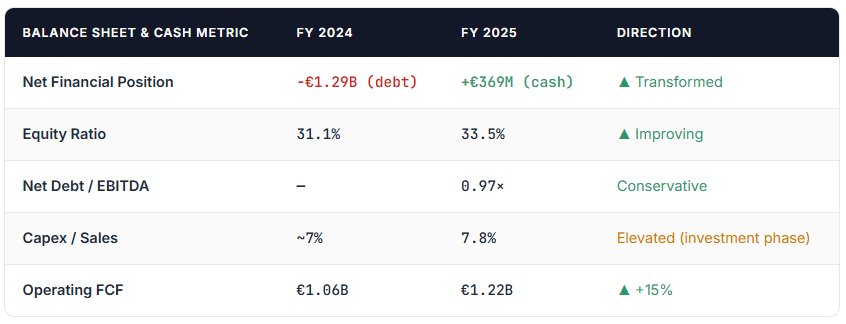

The balance sheet underwent a material transformation. Rheinmetall moved from a net debt position of €1.29 billion at year-end 2024 to a net financial positive of €369 million by year-end 2025. The equity ratio improved to 33.5%, and the net debt-to-EBITDA ratio of 0.97× provides comfortable headroom for M&A — relevant given the naval acquisition now being integrated.

Operating free cash flow reached €1.22 billion, improving 15% year-on-year. This was aided by higher-than-expected customer prepayments. But the 2026 guidance of greater than 40% FCF conversion of operating profit is where market disappointment was sharpest, as consensus had expected 70–90%.

Why Strong Defense Demand Does Not Automatically Mean Strong Free Cash Flow

This is the section that matters most for serious investors. Rheinmetall is in an investment-intensive phase. New factories must be built before they generate revenue. Inventory must be accumulated ahead of production. Working capital swings in defense manufacturing can be significant — governments order in large tranches, payments can be lumpy, and inventory cycles for ammunition and vehicles are measured in months or years, not weeks.

Capex ran at 7.8% of sales in 2025 and was even higher at 8.9% in Q3. The first nine months of 2025 actually showed negative operating free cash flow, driven by plant construction, inventory build-up, and delayed German procurement. The full-year improvement was partly a catch-up effect from late customer payments. Investors should expect continued cash-flow lumpiness as capacity investments proceed.

Section VII

Strategic Positioning by Business Line

Effective January 2026, Rheinmetall reorganized into an expanded divisional structure, adding Air Defence, Digital Systems, and Naval Systems segments alongside its existing Vehicle Systems and Weapon and Ammunition divisions. The civilian Power Systems segment has been designated a discontinued operation and is being divested, completing the transformation into a pure-play defense company.

Ammunition is the margin engine and the most scalable business: demand is consumption-driven (rounds are used, not returned), production is relatively standardized, and pricing power is strong given limited European capacity. Vehicle Systems is the largest division by revenue but carries lower margins due to programme complexity and supply-chain coordination requirements. Electronic Solutions has the fastest growth trajectory and strong margin expansion potential. Naval is the newest addition — management targets €5 billion in annual naval sales by 2030 at margins exceeding 15%, though integration execution will be watched closely.

Section VIII

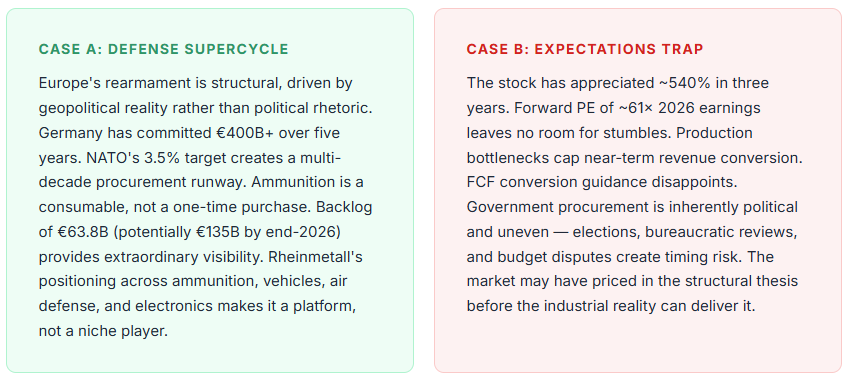

Is This a Defense Supercycle or an Expectations Trap?

This is the question that separates conviction from momentum. Both sides of the argument are real, and serious investors must weigh them honestly.

The honest assessment is that elements of both narratives are true simultaneously. The demand signal is real and structural — this is not a flash of war-driven excitement. But the stock’s valuation assumes excellent execution over multiple years. Rheinmetall’s business is stronger than the stock reaction suggests. But the stock price demands that the business remain strong, grow fast, and convert growth into cash — all at the same time. That is a high bar, even for a company this well-positioned.

Section IX

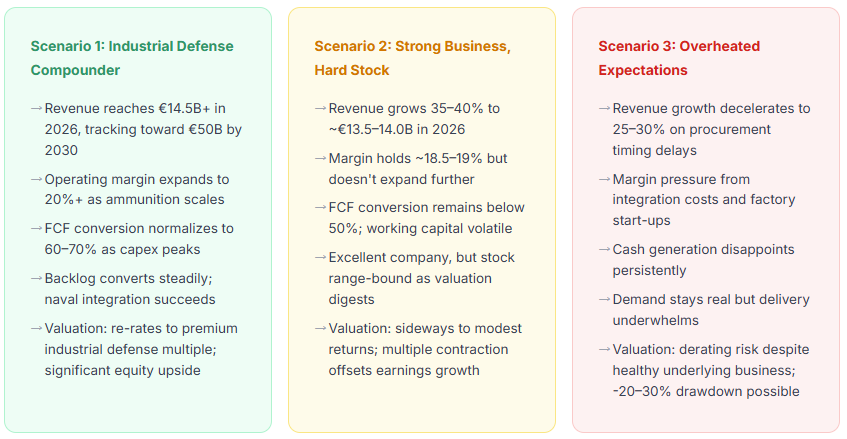

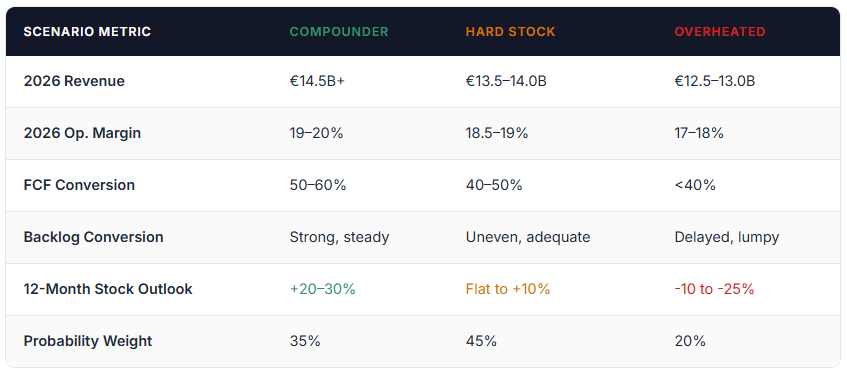

Valuation and Scenario Analysis

Section X