Rocket Companies: Generational Demographics will Drive Growth

Rocket Companies: Generational Demographics will Drive Growth

but the Fed will slow down their opportunities

Rocket Companies, perhaps Rocket Mortgage is one of the best positioned companies when it comes to online mortgage generation. Founded in 1985 as Rock Financial it was not until late 90’s that it switched from traditional mortgage lending to mostly online lending. Today they have close to 10% of the mortgage generations in the US, they have continuously grown over the past two decades and recently have had some of their best quarters. Today, with mortgage rates rising rapidly they find themselves in the middle of an industry that will be highly impacted by lower activity for many quarters to come. Inflation has forced the Federal Reserve to hike the Fed funds rate, the ten year yield has responded with a dramatic shift upwards, mortgage rates have reached 7% on the 30 yield fixed rate. Rocket Companies has seen its market share go in the opposite direction just as fast. It has come from a high of close to $40 per share to $6.37 per share today. We will be looking at the company in detail, they will have an impact from higher rates, but as the leader in the market, does it really justify the drop in value that it has seen?

Business Model:

Revenue Streams & Operational Model:

Home Financing

Rocket Mortgage:

Mortgage originator and servicer that provides clients with an end-to-end digital mortgage experience. The nation’s largest mortgage lender. Their digital solution utilizes automated data retrieval and underwriting technology to deliver fast, tailored solutions to a client. Their clients leverage the Rocket Mortgage app to apply for mortgages, interact with their team members, upload documents, e-sign documents, receive statements, and complete monthly payments.

Amrock:

Title insurance services, property valuation and settlement services, leveraging proprietary technology that integrates into the Rocket platform and processes. This provides a digital, experience for their clients from their first interaction with Rocket Mortgage through closing

Lendesk:

Canadian technology services company offering a suite of products to digitize and simplify the Canadian mortgage experience, including a point of sale system for mortgage professionals and a loan origination system for private lenders

These are products focused on brokers mainly and not to the regular individual customer. Their main product is called Finmo which is a digital mortgage platform for mortgage brokers.

Edison Financial (Rocket Mortgage Canada):

Their Windsor, Canada based digital mortgage broker that serves the needs of consumers across Canada by leveraging technology to make the mortgage process efficient, transparent, and comfortable. This is the closest product with similarity to the Rocket Mortgages product in the US, in fact their website now redirects to Rocket Mortgage Canada.

Home Search and Sales

Rocket Homes:

Their home search platform and real estate agent referral network, Rocket Homes provides technology-enabled services to support the home buying and selling experience. The company allows consumers to search for homes, connect with a real estate professional and obtain mortgage approval – through sister company Rocket Mortgage – creating an integrated home buying and selling experience.

This product is essentially a similar product to Zillow, Redfin etc.

For Sale by Owner

It is a platform that allows individuals to list their home bypassing the traditional use of realtors. Rocket Companies offers services to assist on paperwork and process for a fee. This is offered also to a homeowner that already has an offer, and does not need to list but still could need assistance on the closing.

Personal Finance

Truebill (Rocket Money)

Their personal finance app that helps clients manage their financial lives. Truebill offers clients an understanding of their finances and a suite of valuable services that could save them time and money.

The app is free but they charge for some of the services like bill negotiation or their premium account which includes syncing your balance, Premium Chat, Cancellations Concierge, Custom Categories, Unlimited Budgets, Smart Savings, and More.

Rocket Loans

Their online‑based personal loan business that focuses on “high” quality, prime borrowers, by leveraging a user-friendly platform and dedication to client-experience.

These are consumer loans as well as home improvement, debt consolidation, solar loans etc.

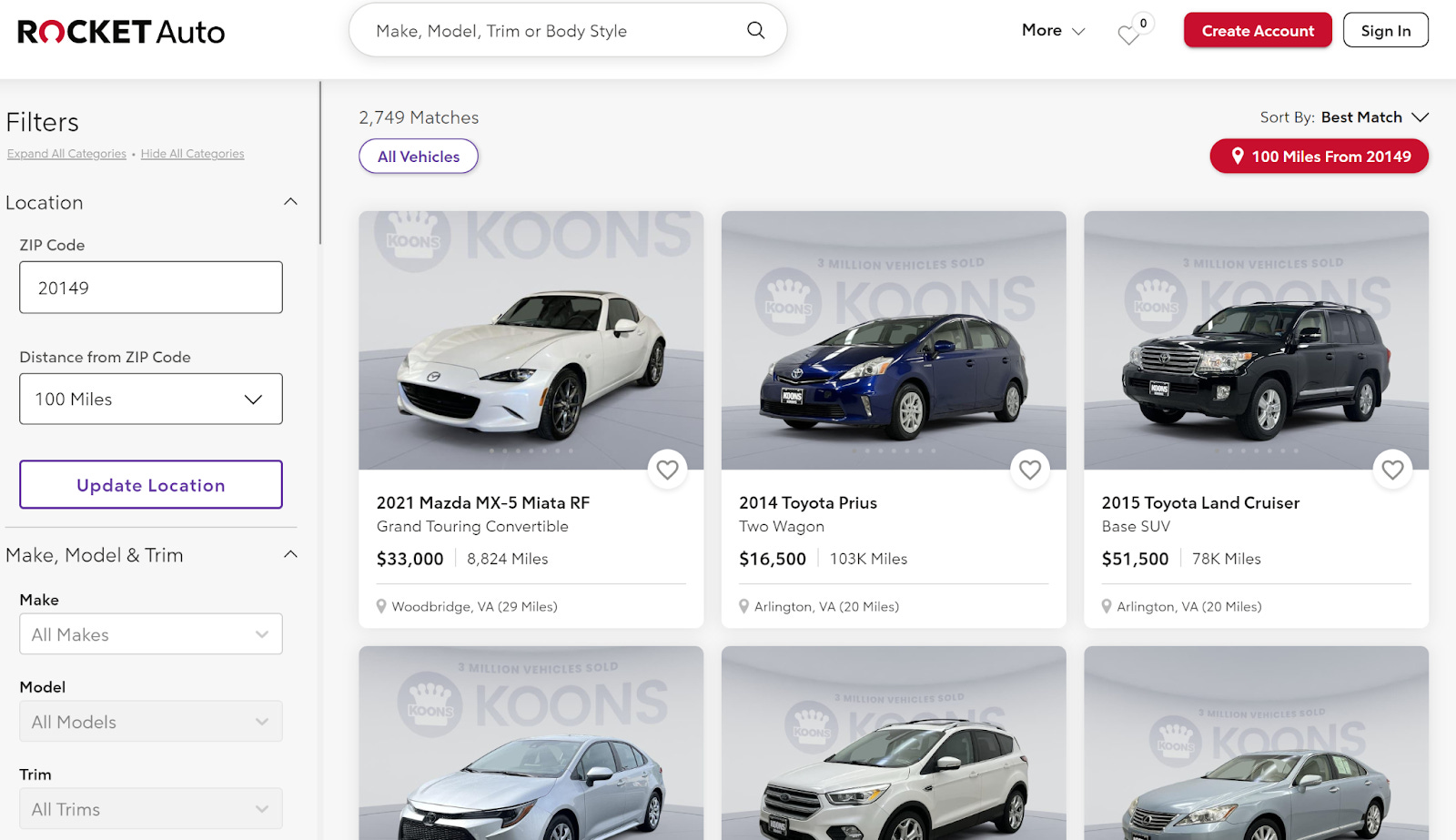

Auto Purchase

Rocket Auto

It is a bit more than just a way to get a car loan. Their website takes the inventory of many car dealers and lists them in the website. The website can be searched by car, make, model etc. When trying to purchase they offer a way to finance the car.

Sales and Marketing Services

LowerMyBill.com

It is mainly a website that helps individuals to learn from the purchasing or refinancing of homes.

It is basically a marketing platform that generates client leads for Rocket brands and third parties.

Rocket Central

Shared service organization that provides technology, data, marketing, communication and other services across our companies

Business Model:

In general many of their product are driven by the selling of the loans generated

Their mortgage origination business primarily generates revenue and cash flow from the gain on sale of loans, net. The gain on sale of loans, net includes all components related to the origination and sale of mortgage loans, including:

Net gain on sale of loans, which represents the premium received in excess of the loan principal amount and certain fees charged by investors upon sale of loans into the secondary market

Loan origination fees (credits), points and certain costs

Provision for or benefit from investor reserves

The change in fair value of interest rate lock commitments ("IRLCs") and loans held for sale

The gain or loss on forward commitments hedging loans held for sale and IRLCs

The fair value of originated MSRs (Mortgage Servicing Fees) (

Servicing

They also generate income from servicing their clients’ loans. For every mortgage that they service, they receive a contractual set of recurring cash flows for the life of the loan, primarily those which are part of a securitization by the GSEs or Ginnie Mae

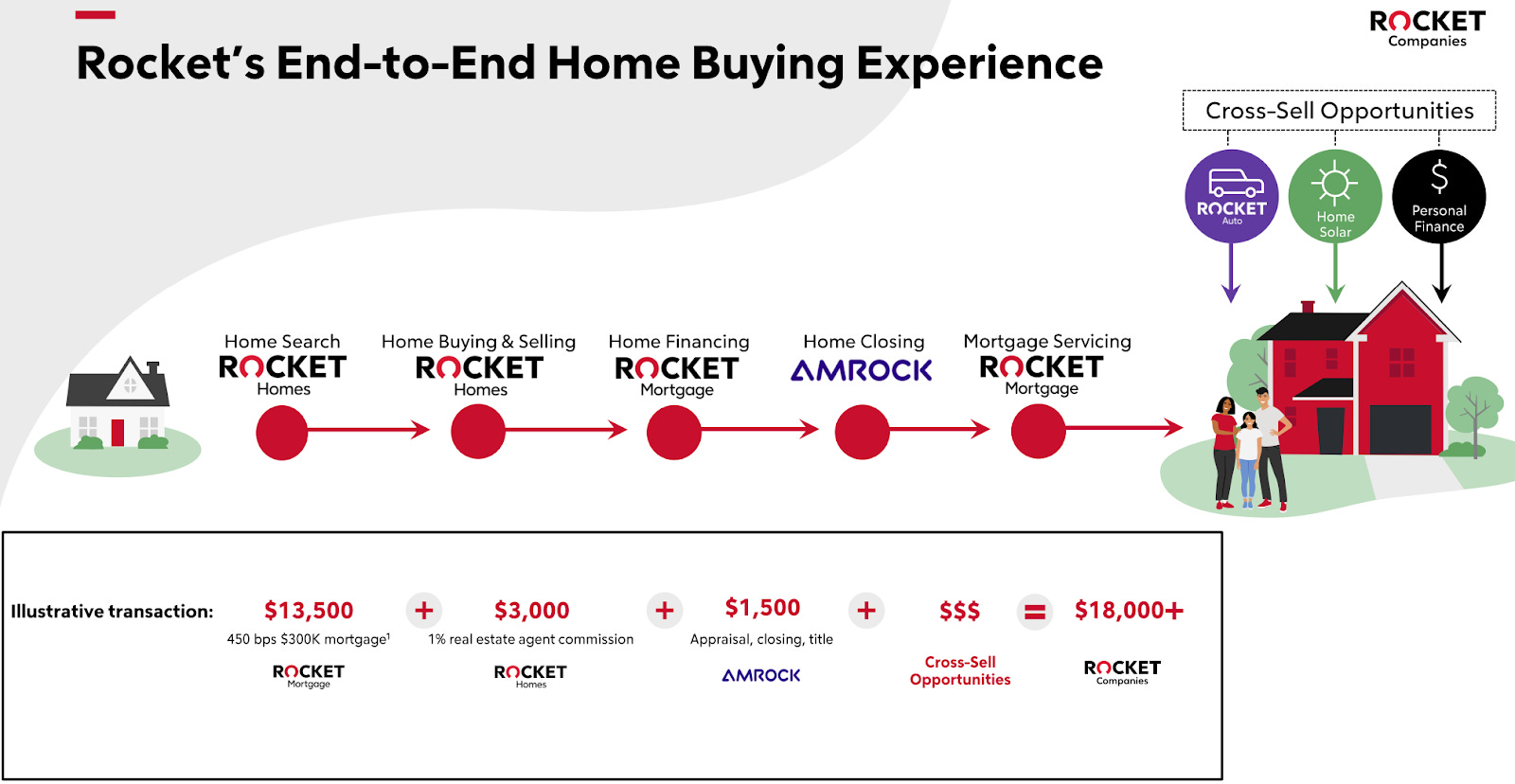

It is now clear that despite the strong branding they have as Rocket Mortgage, they are not only about Mortgage anymore, though mortgage is a very large part of their business.

Below you can see an illustration of all the revenue generation opportunities throughout the home purchasing journey

Key Metrics / Performance

Revenue and Key KPIs

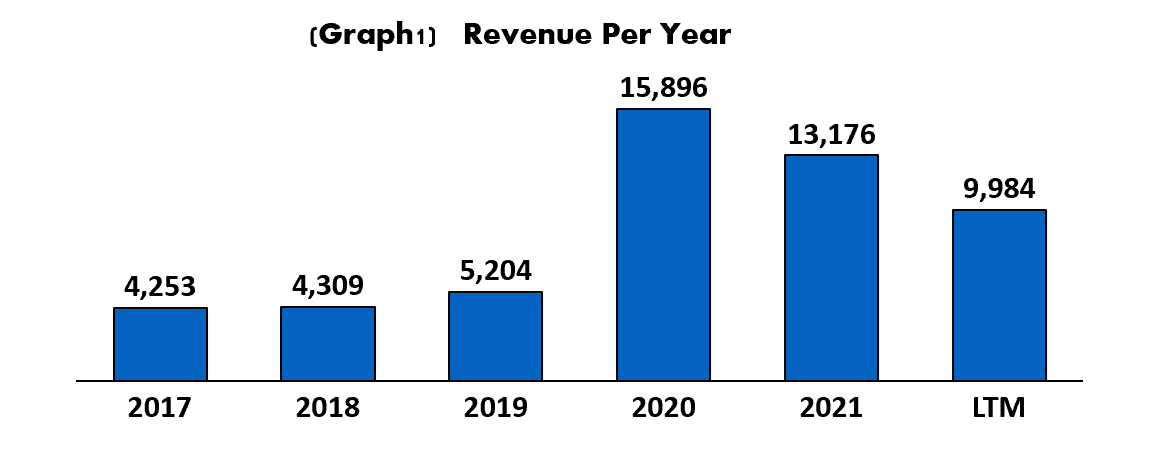

First thing we can see when starting to look at the financial statement from Rocket Companies is that they had a terrific performance during 2020 and also 2021. This came from the great buying spree that the American population took advantage during these Covid years. As a response to the likely economic depression that could have come, the Fed took the rate down dramatically close to zero. The Fed as well took part in buying more than a trillion dollars in mortgage backed securities, this was basically a green light for mortgage originators to produce mortgages, since there was definitely a buyer on the secondary market. This low rate environment plus the sudden change in behavior where the population started buying homes somewhere less crowded, or getting a bigger place to have office space, helped companies like Rocket Companies to originate more mortgages that they could have ever had on normal conditions. From 2019 to 2020 their total revenue grew by 205%, over the last 12 months this revenue is still 92% higher than what they had in 2019

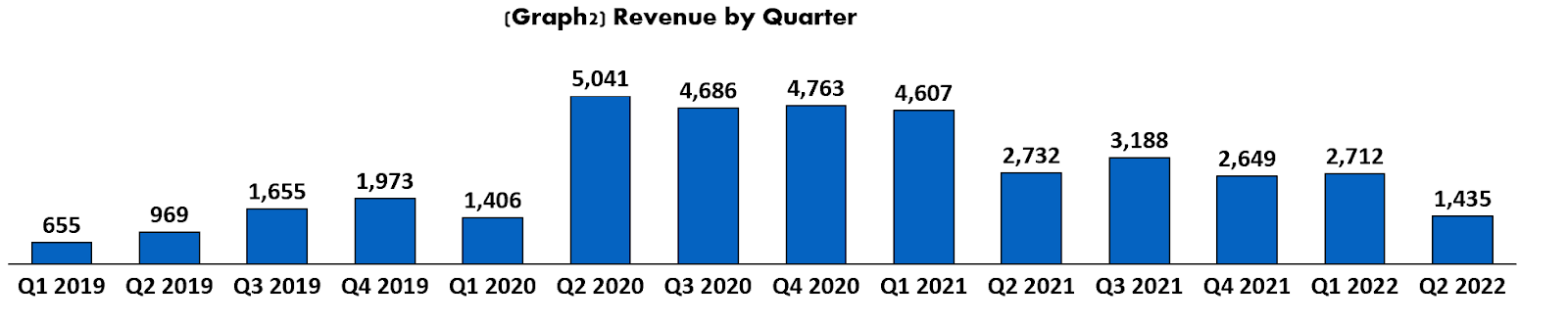

Recently though the story, for obvious reasons, (Fed hiking rates, no longer buying mortgage backed securities, ten year yield in decades highs and mortgage rates as well in decades high) it is very different. Revenue for the second quarter of 2022 was just $1.4 billion, 28% of the total revenue they had during Q2 2020, the best during the pandemic. $1.4 billion for the second quarter was still higher than Q2 2019 but very close to the third and fourth quarter in 2019. In addition the trend is clear and expected to continue to be impacted on the mortgage front until the Fed slows down hikes or even pivots.

The jump in revenue is directly related with the jump in mortgage money originated, the big increase is seen in 2020 and 2021. Most of the revenue increase is explained by this though a little comes as well from the rise in market share (but mostly comes from more generations in the overall market)

The trend though, as expected is coming down fast. Run Rate today if we take Q2 2022 would be $138b about a third of the high in 2021. This is not 100% accurate since there is some seasonality throughout the year.

On their title insurance side of the business, the trend is very similar. Amrock closing units have fallen as well to levels below quarters in 2019. This number gives a little more detail on how units are considerably lower than 2019. The number in originations is increased by the fact that loan values now are higher than in 2019, since the average price of a single family home has increased considerably. It is the amount that they are having in closing units with Amrock that is clear of a heavily impacted market due to high interest rates

Similar trend was seen in Rocket Auto sales, though it was still high, it has started to trend down. Last quarter this number was not reported by Rocket.

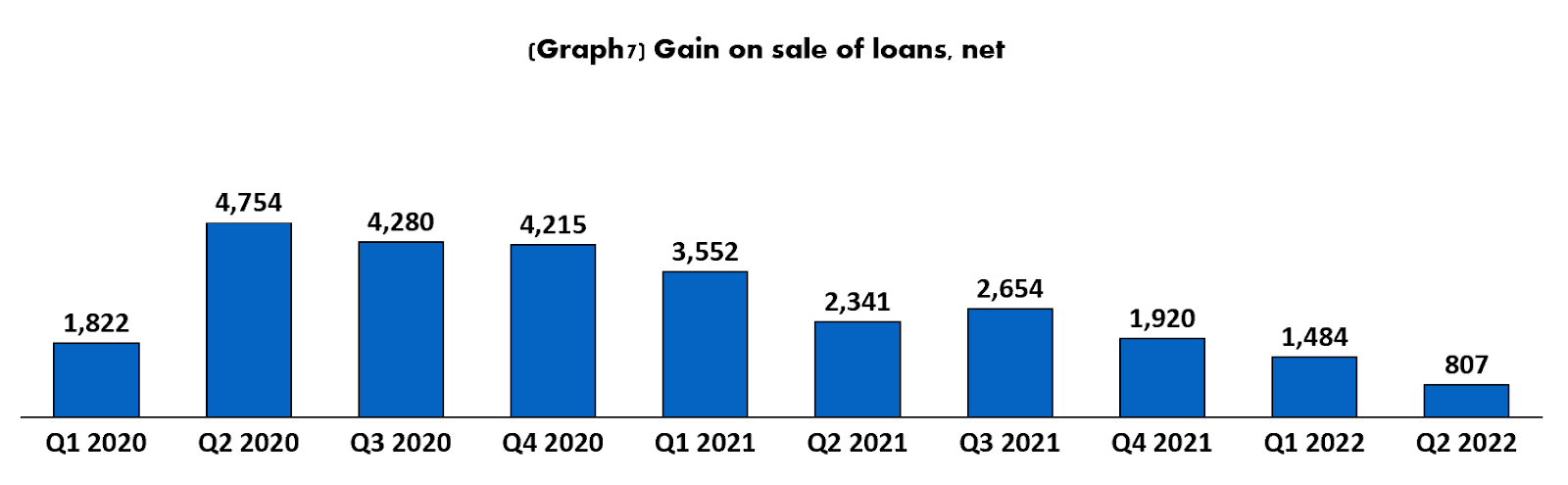

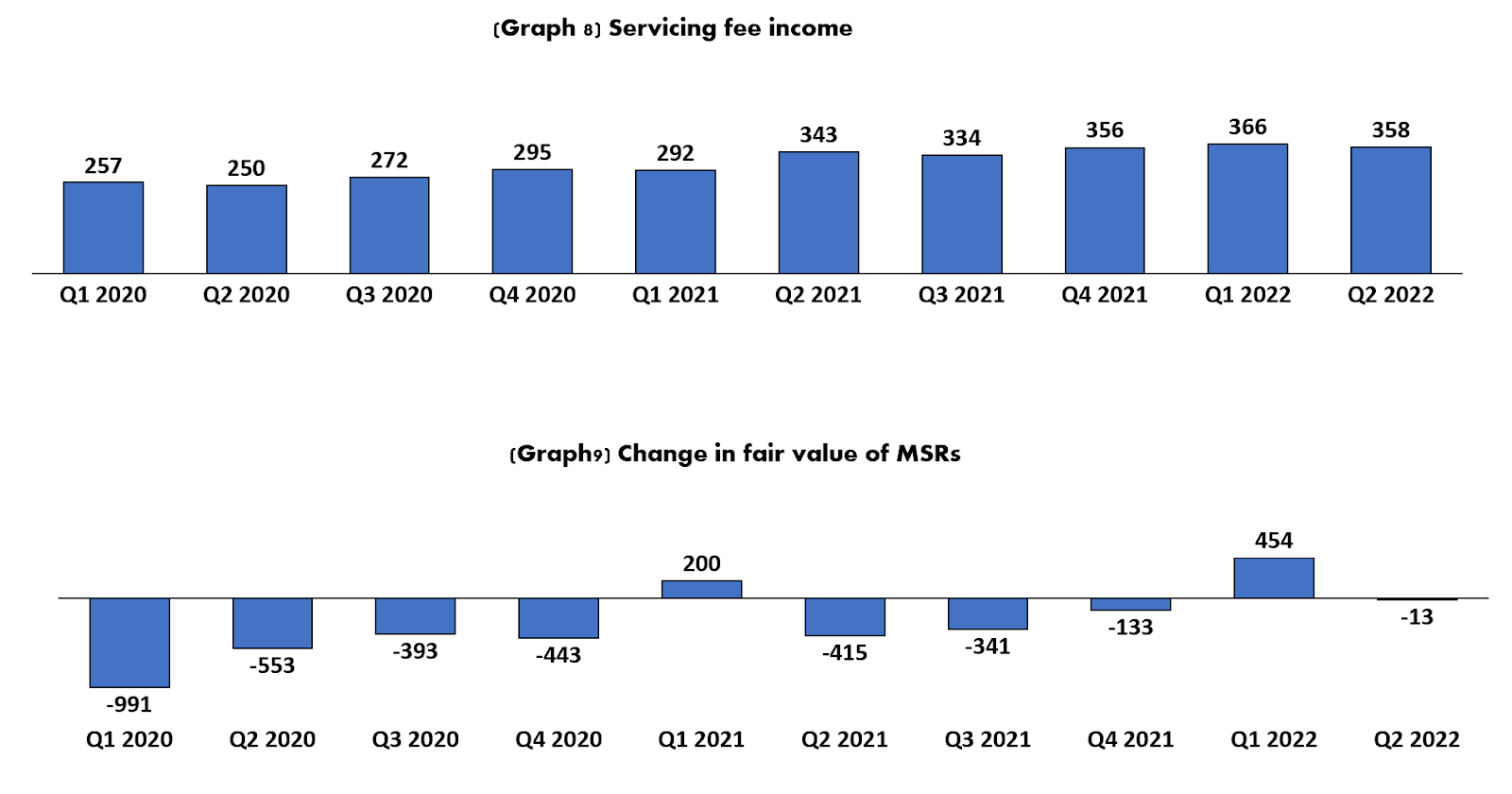

Looking at the revenue in more detail, Gain on sale of loans is the one heavily hurt by the drop in rates, but servicing revenues are stable and keep growing, this will likely keep growing but at a slower pace since less homes are being sold so less homes will be added to the servicing base. Change in fair value of MSR had been recently negative but has started to turn positive since less prepayments are expected now that the rates are so high and refinancing very unlikely.

On graph 10 we see that the number of MSRs being serviced has been flat recently. MSRs at fair value continue to rise at a faster rate than the change in total MSRs, this means that these are gaining in value due to what we mentioned previously, the fact that less prepayment comes when interest rates rise. When it comes to Unpaid Principal Balance of MSRs it goes hand by hand with the unit amount (Graph 10,11,12)

Costs and Expenses

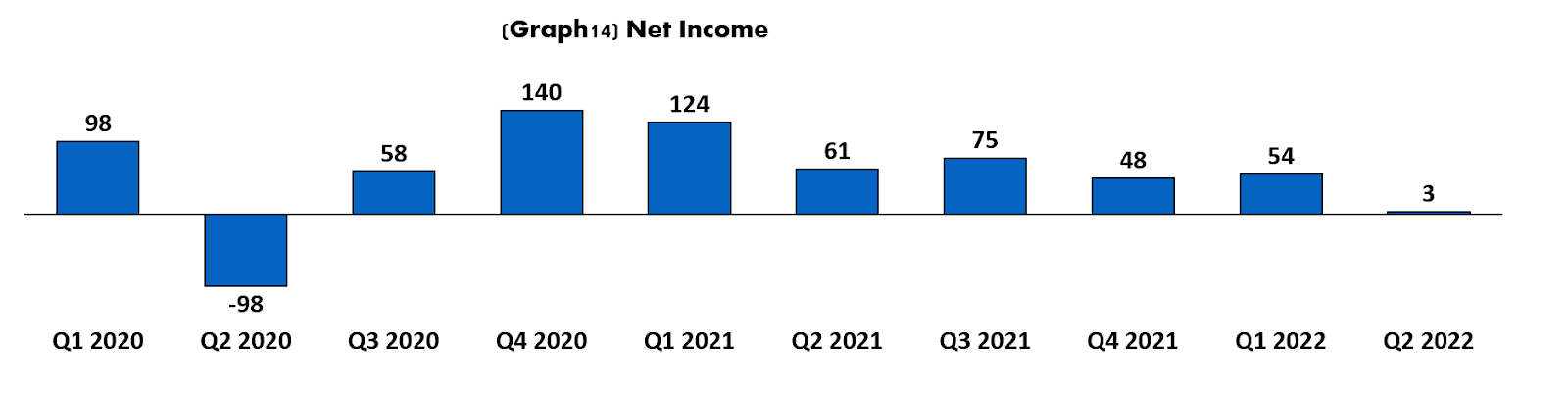

Since the start of the year Rocket Companies has emphasized in their call that they are focusing on cost reductions. They indicated that they would have close to $200m in reductions in Q2, by the time they came for the Q2 call they got a higher number closer to $300 m. They have reduced items like marketing, which makes sense, since there is a lot less interest now in both new mortgages and refinancing. You see a drop in expenses of $293 million comparing Q1 2022 and Q2 2022, but as a percentage of revenue this shoots up considerably since revenue came down faster.

Despite the dramatic change in revenues the net income, thanks in part to these cuts, has remained positive so far, yet it is flirting with the negative side.

Cash Flow

Net income for the company was close to zero, when looking at the actual cash from operations. The variation in loans originated/sold moves the needle in terms of how much cash is needed during a quarter. During Q2 2022 this had a negative impact of $871m, an additional impact of $617m came from the change in other net operating activities. All together, from operating activities the company consumed $2.1b. This moves a lot from quarter to quarter, last quarter was a lot different, the company generated $9 billion, mostly came from the same, the variation from loans originated to loans sold. Also these cash movements if we have a look at their historic value it has to do a lot with the seasonality during the year. Q4 and Q1 usually bring the highest amount of cash flows and Q2 and Q3 lower (when usually selling season in real estate happens)

During the quarter the company also paid a dividend for $1.8 billion at the same time they got an almost equal amount in financing. Overall during the quarter the company net cash change was $1.4 billion, over the past 12 months they used $ 1 billion.

Balance Sheet

Rocket Companies ended the quarter with $1.2 billion in cash, they also ended the quarter with $12.4 billion in loans held for sale. Debt moves close to the loans held for sale, they have a total of $14.6 billion in debt at the close of Q2 2022

Housing Market

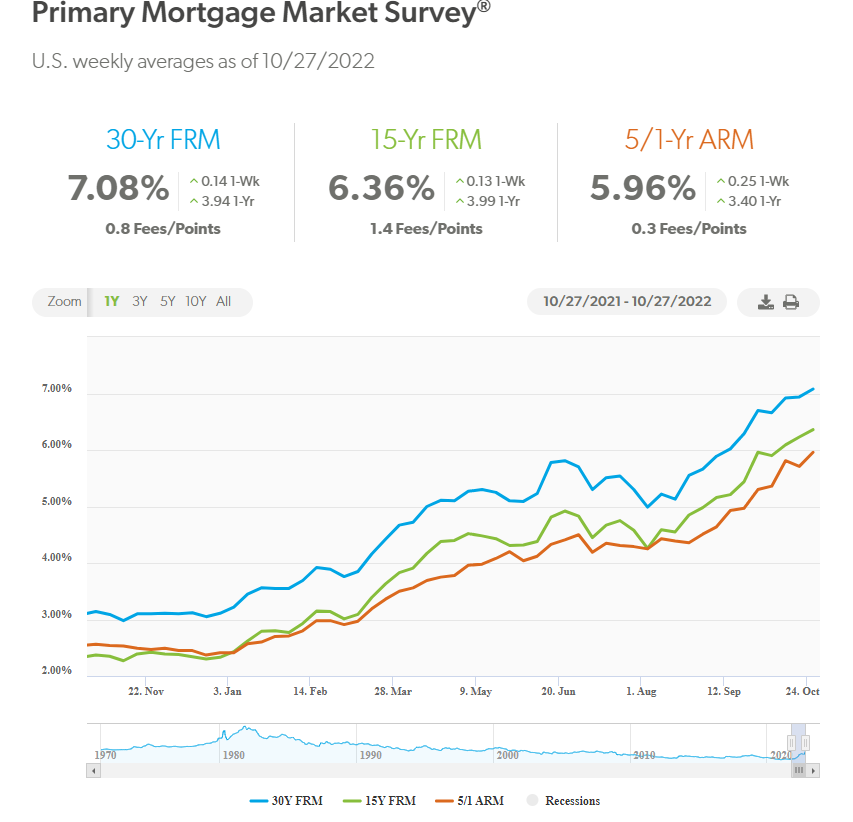

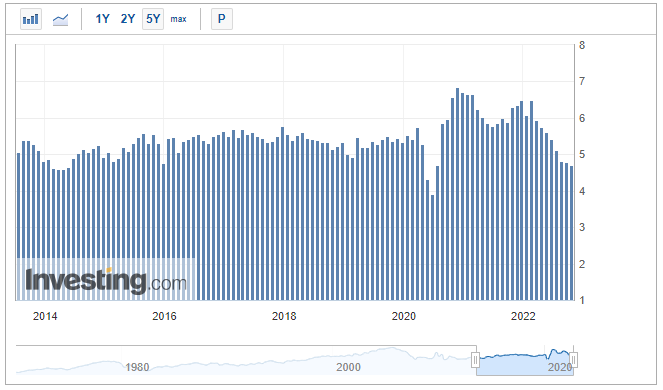

Rocket companies' short term future will be directly dependent on how the real estate market moves and the real estate market will be highly dependent on how the Fed keeps moving. Already the Fed has done a lot of damage. Mortgage rates have come from 3.11% on December 30th 2021, to 7.08% this week.

High mortgage rates have impacted housing affordability dramatically. In the most recent report by the National Realtors Association we can see that housing affordability is at decades lows. The index by August was at 104, it needed $84,000 to qualify for the typical 20% down mortgage. In 2019, before the pandemic, the index was at 160 and it was needed to have $51,000 in income. The rise in income needed has nearly doubled in just 3 years.

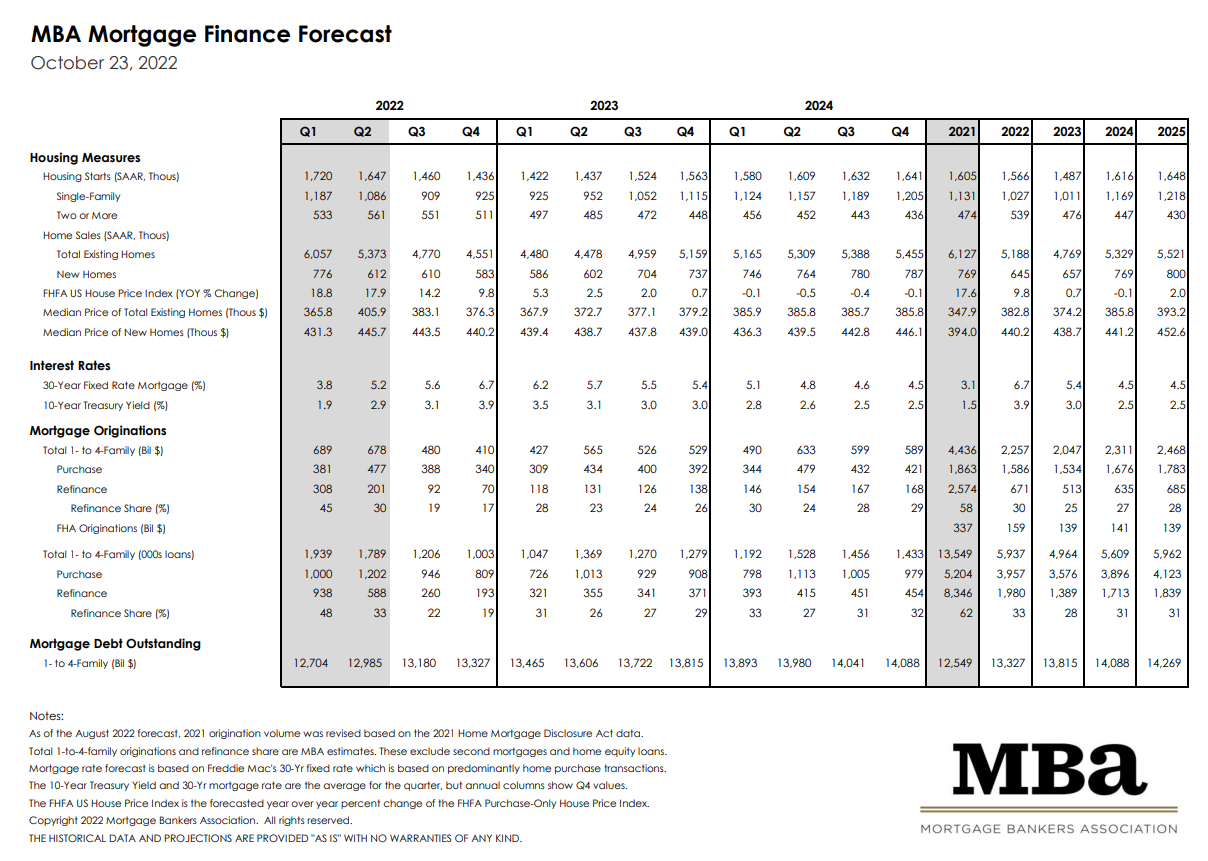

The impact that this has had in the mortgage industry is also dramatic. From the data reported by the Mortgage Banker Association, 2022 will have only $2,200 billion in mortgage originations. That is 51% of the total mortgage the US had in 2021. In terms of units, the number crashed to 5.9 million purchase and refinance transactions, or 43% of the amount originated in 2021. The expectation for 2023, 2024 looks very similar to what we have in 2022 so, the MBA expects that not a lot will change for years to come.

The number of originations was considerably higher for two years, but even 2019 was higher than what the MBA is forecasting for the next three years.

Existing home sales have dropped considerably as well, it is currently moving at one of the lowest levels in a few years and way below the average of these years as well. 4.7 million existing homes have been sold for the past 12 months. Excluding the pandemic these levels had not been seen since November 2015, then was different, the number was hit briefly and quickly rebounded above 5 million homes per year.

Prices have started to crack as well, they are still higher year on year, but many cities are starting to show drops month over month. Cities like San Francisco (-4.3%), Seattle (-3.9%) and San Diego (-2.8%). The S&P CoreLogic Case-Shiller 20-City Composite Home Price NSA Index saw a decrease of 1.63% over the last reported month and 2.2% over the last 3 months.

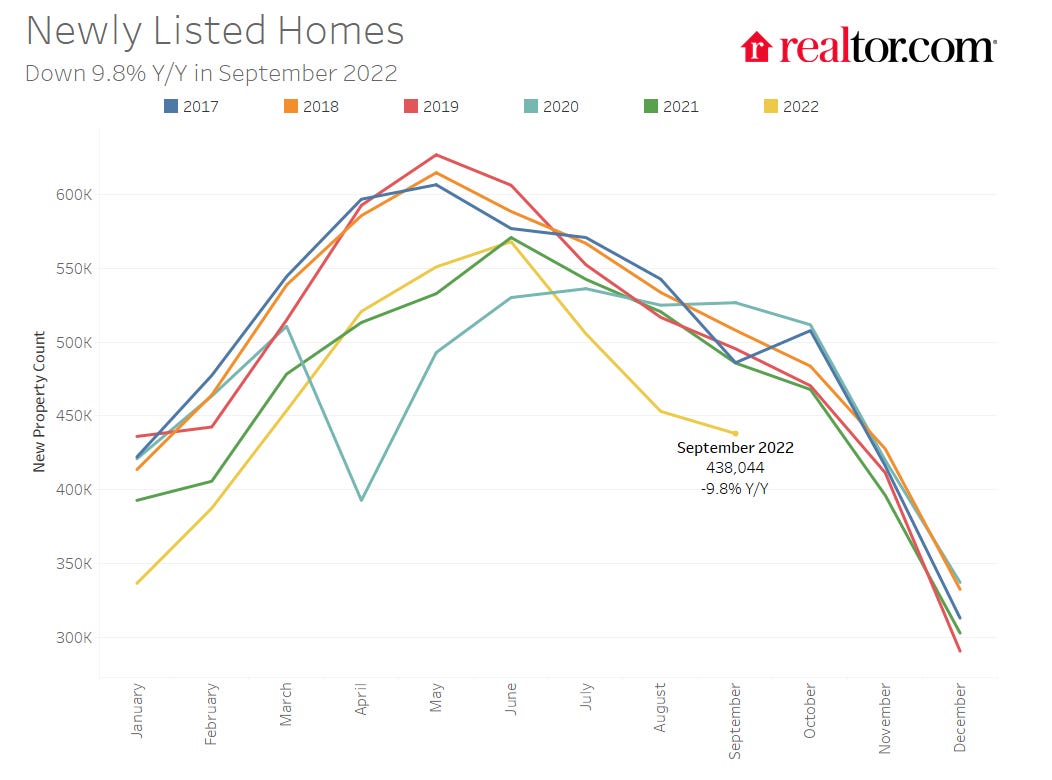

The housing market has turned the corner. The number of homes being sold is lower, the number of mortgages is lower, affordability is terrible and the Fed has still not shown signs of stopping. The housing market will not improve until the Fed pivots, and actually housing might or will be the thing that will force the Fed to pivot. This is the most important asset for US households. The home is usually the American household's biggest asset; the Fed cannot afford to have a huge drop here. The Fed has only one thing in their favor, 65% of mortgages in the United States are under 4%, 24% are 3% or lower, 285K people have mortgages below 2%, 4.7 million people have mortgages between 2.0% and 2.5% and 13.1 million have 2.5% and 3% mortgages. These people with ultra low mortgage rates will not let go of their homes unless they are forced to sell. That impact is reflected in the inventory, the inventory is rising, specially because houses are taking longer to sell, but the overall number is not even at pre pandemic levels yet, and pre pandemic it was not a buyers market either, housing inventory has to rise a lot for the market to have huge prices decreases. That will only happen if the Fed breaks the job market, that market is a lagging market, but for now, it is still holding strong with more open positions than people looking for employment. For now it has not happened, and newly listed homes are the lowers in years (from the data from Realtor.com)

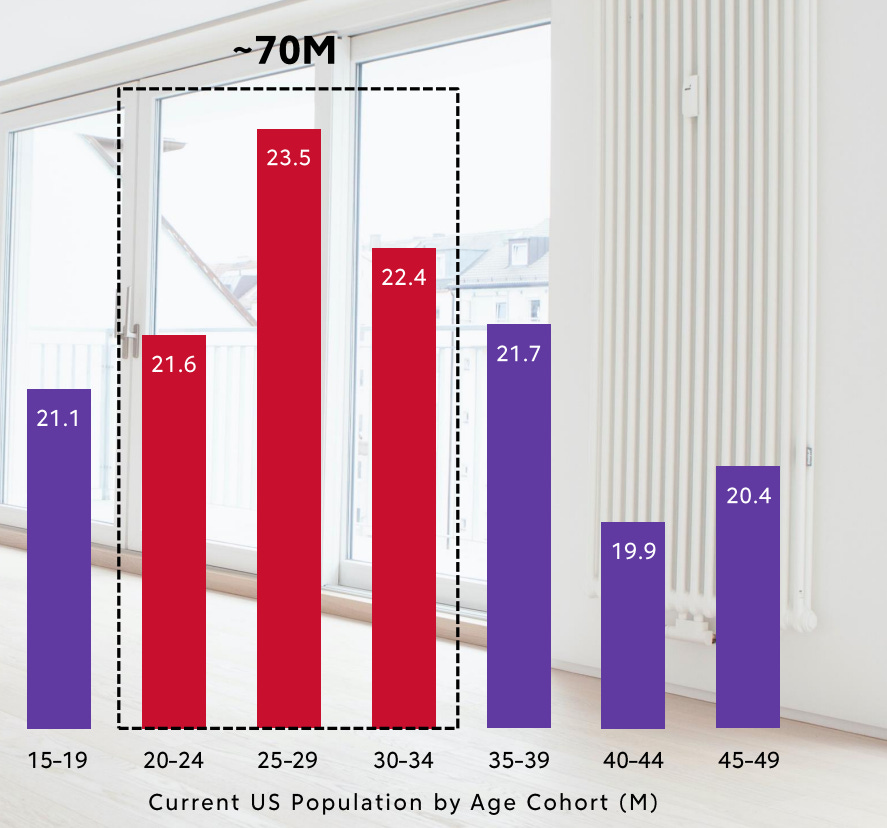

Last but not least, Millennials represent now the largest cohort of home buyers, this generation is considerably bigger to the previous generation looking for a home (Gen X) this means that the low level of inventory for them would even be worse than what the GenXs saw when they were entering their homeownership years

Competitive Landscape

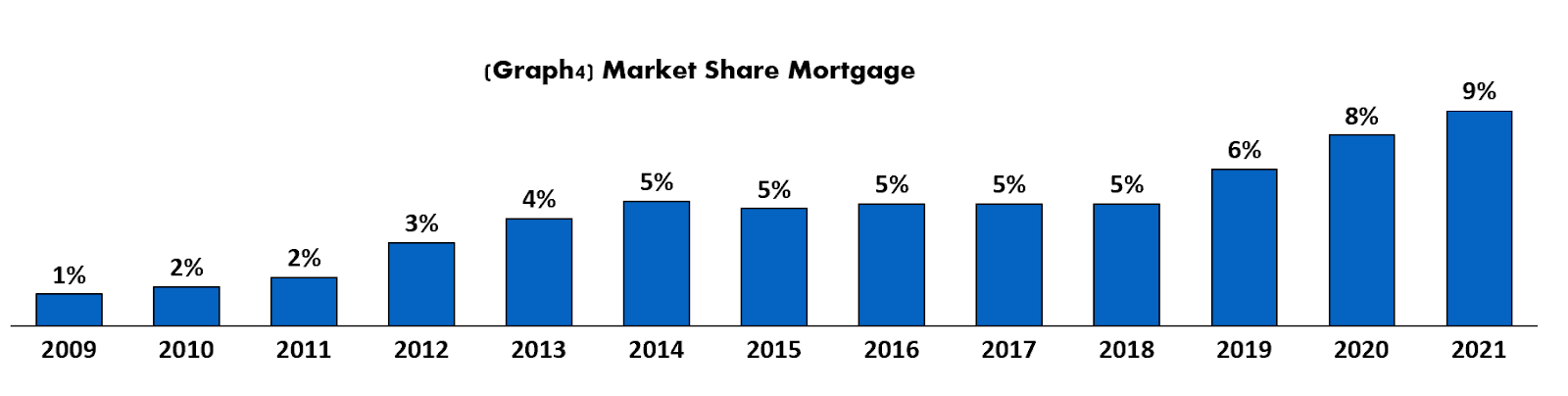

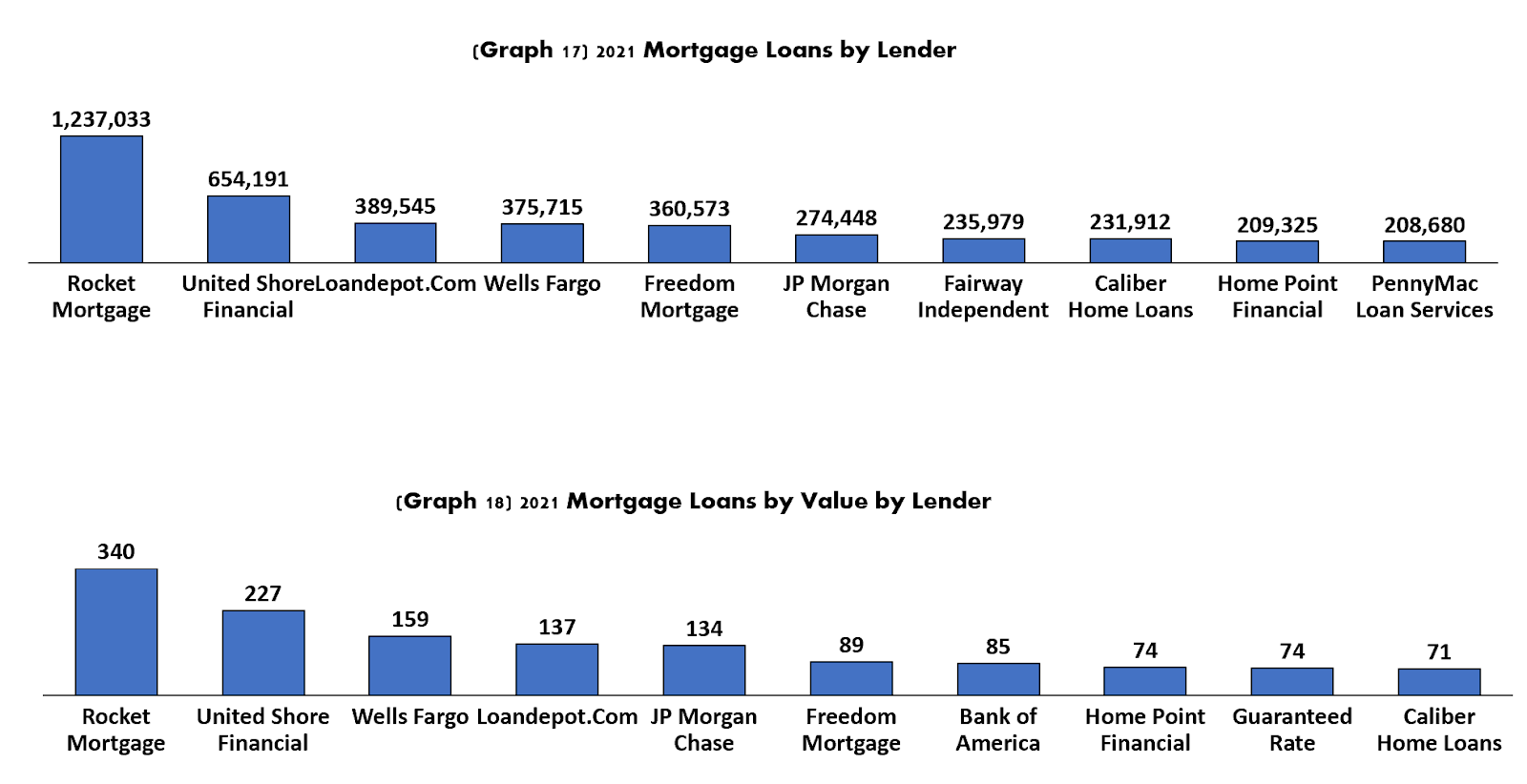

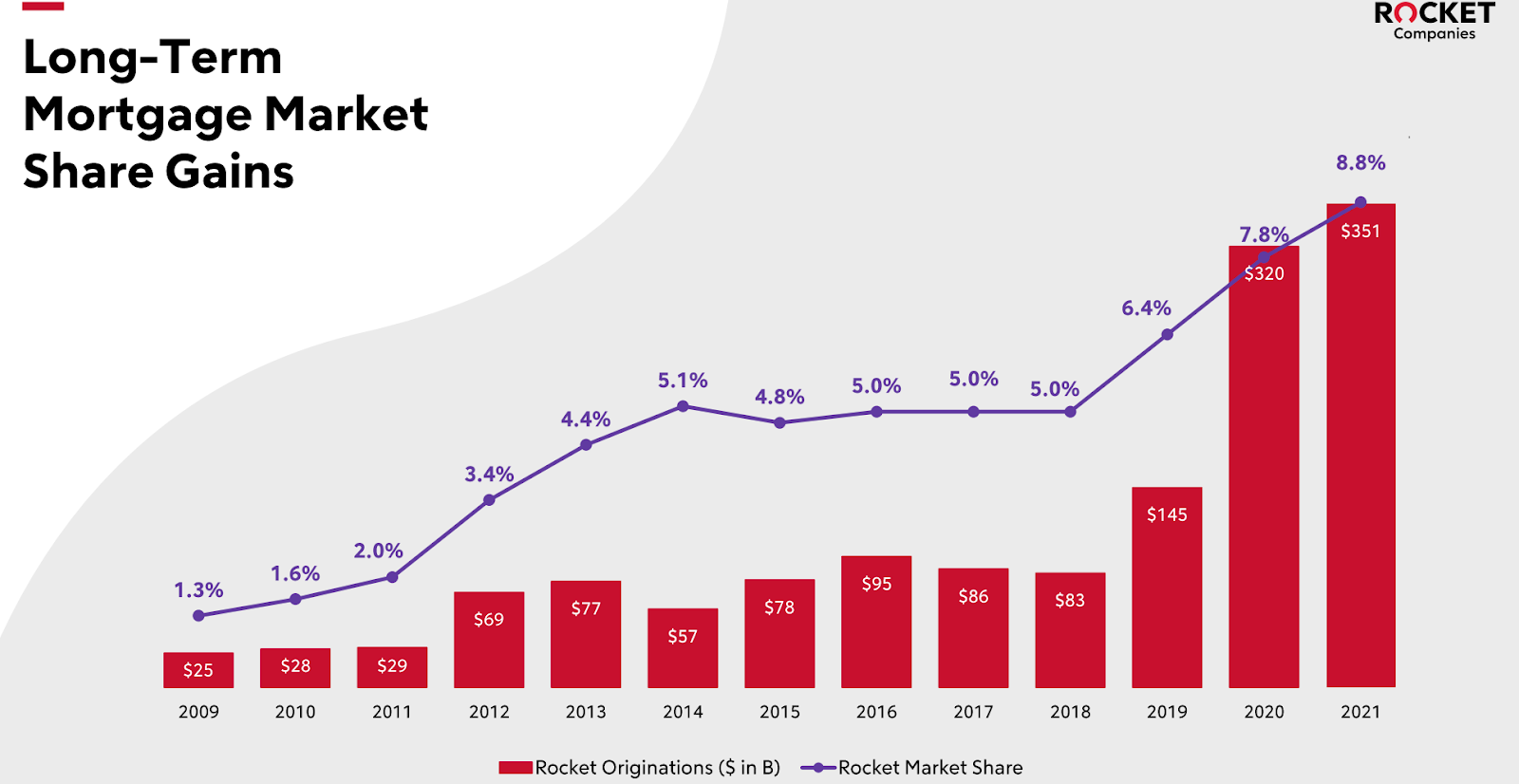

The mortgage lending industry has changed considerably over the past 2 decades. It has gone from a very local, very analog process, to a digital experience in which you don't have to even set foot in a bank’s branch. Rocket Mortgage has driven most of these changes, they have led the transition so far and with that they have managed to climb and become the biggest mortgage lender in the US. As seen in the graphs below they are leading both in number of total loans and loans by value.

Market share has approached 10% and it is expected to surpass the level in 2022. Their market share has accelerated very rapidly over the last 4 years after hitting a wall from 2014 to 2018. With the millennial generation now the main generation looking for a home it is just a matter of time that most of the loan originations are done digitally and companies like Rocket Mortgage could gain more market share and companies like Wells Fargo and JP Morgan could lose more.

Some of the possible risks for the company are:

There are some short term risks from high mortgage rates. As long as the Fed keeps rising rates and homes are less and less affordable the market for mortgages will continue to shrink. This will impact their revenue negatively since originations will continue at very low levels. (The same applies for all debt generation, Auto, solar, etc.) At current levels they are barely profitable, if market is further reduced they might start losing money

Disruption: As Online mortgage origination came to disrupt the mortgage market in the US the same could happen with the new up and coming ibuyer industry, if the industry is successful, many of the homes purchased via these companies might already include the mortgage as well.

Traditional banking might catch up: These banks have the resources to become a serious competition in the online mortgage market. It is all a no brainer for them, Millennials won’t go to branch for a mortgage and also there are a lot potential cost efficiencies on going mainly online

What could be the case for Rocket Companies being a good opportunity for the next 10 years?

Millennials and GenZs: These generations will only do online mortgage applications and the millennial generation specially is the biggest generation in the US and it is now in their prime household formation years. It would be expected that over the next few years not only the number of online mortgages could rise by the mere adoption of the technology but also by demographics. This is a big opportunity for Rocket Mortgages to continue gaining market share.

Strong branding and strong positioning. They are the top of mind brand for everyone in term of online mortgages. As long as they don’t ruin their NPS they are well positioned to capture the coming market growth.

Valuation

Rocket Companies was another company that had a huge bull run during 2021, the company reached almost $40 per share, today is trading at $6.7 per share. You could say that it was expected since the huge drop in the amount of mortgages in the industry, and the very mild market expected for the next 2 years. We have calculated again 3 different scenarios conservative, base case and optimistic case.

For our Base case we have assumed that 2023 is a very slow year and the recovery starting in the back of 2024 with more refinancing expected from that year onwards as well. This is a difficult estimate considering that it will depend directly on what the Fed does, with these assumptions our base model values RKT at $7 per share a bit above their current value.

Our conservative base is basically a bit more pessimistic on the recovery of the mortgage market, it would take a little over a year longer. With this model the valuation is quite lower at $2.3 per share.

Our last model, our optimistic case, where the market recovers faster with an early Fed pivot, the valuation of the company is at $19.6 per share.

Rocket Companies are in a very good position to gain market share yet their revenue will likely won’t be close to what they had in 2020 and 2021 anytime soon. They must solidify their position as the leading mortgage broker; they cannot allow the traditional banks any space to catch up on the digital landscape, they must continue to innovate during these calmer years. The company will likely continue to operate and grow for many years to come, but the valuation it had for a few months in 2021 was mostly a bubble and not the real value of the company.