Rocket Lab: The Quiet Giant Building America's Space Backbone

From garage-scale smallsats to $816M defense contracts — how Peter Beck turned a New Zealand startup into the United States' most important launch company outside SpaceX

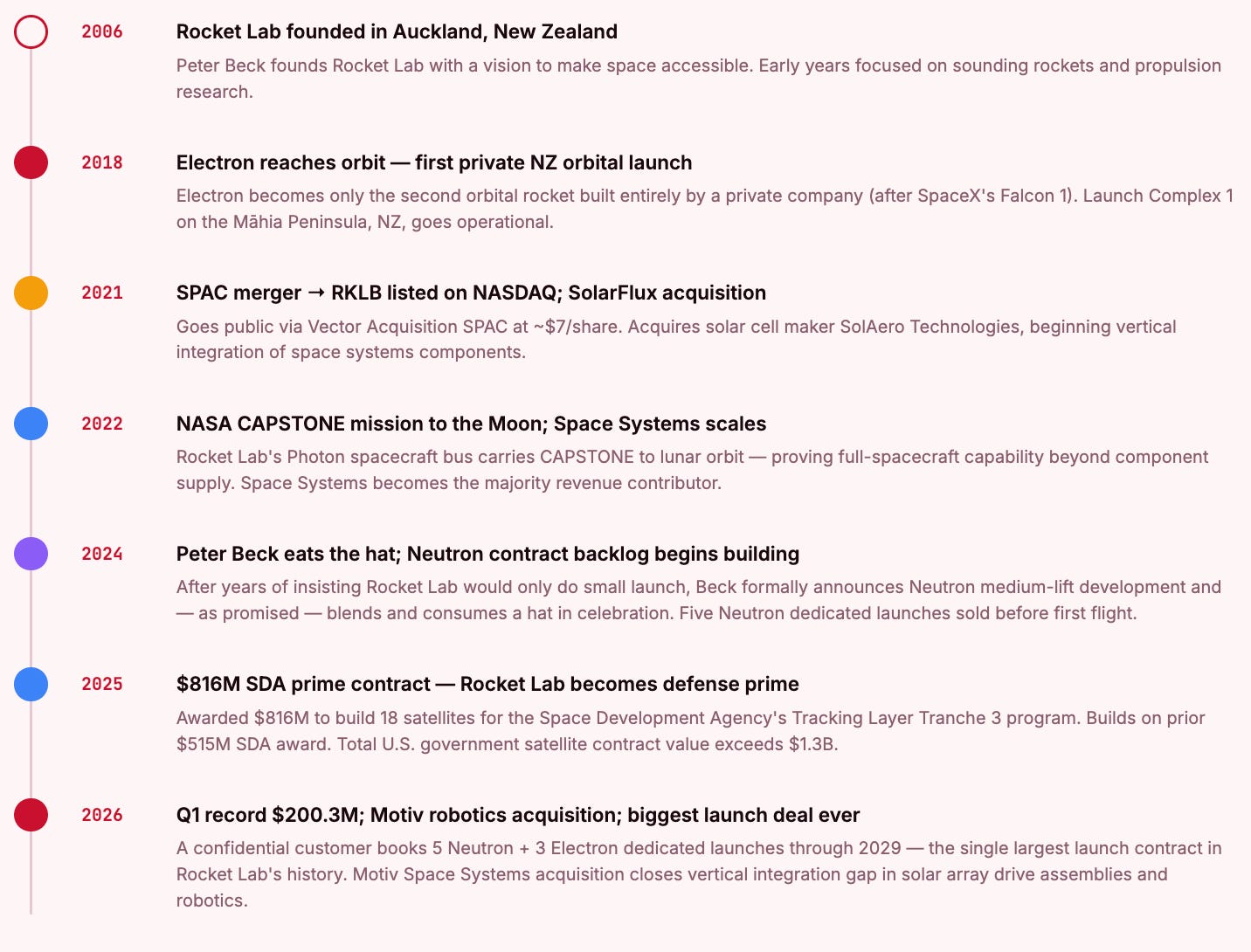

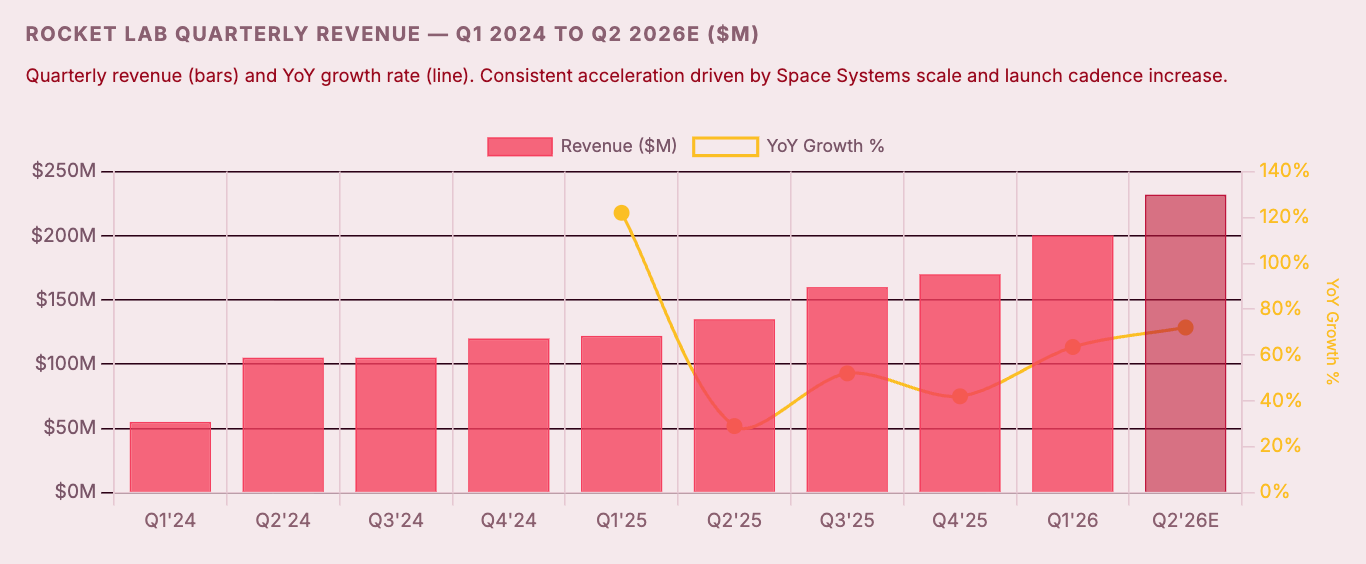

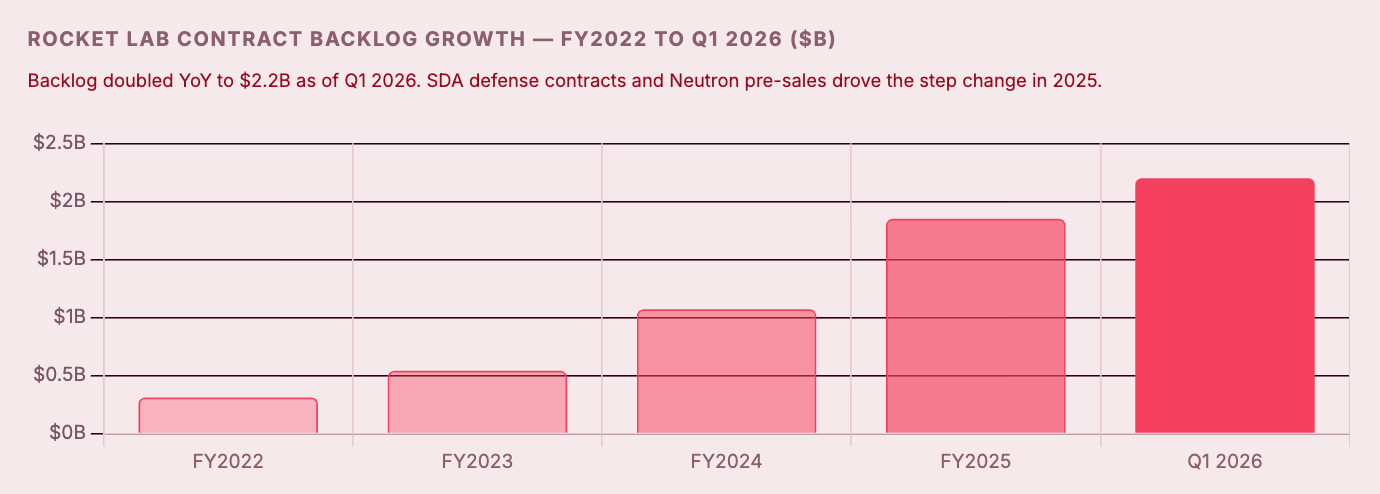

Peter Beck promised he would eat his hat if Rocket Lab ever built a medium-lift rocket. He ate it — literally, in a blended smoothie — and now Neutron is closer to the pad than ever. But the deeper story is not just Neutron. Rocket Lab has quietly assembled something rarer than a great rocket: a vertically integrated space company with recurring defense revenue, a proven smallsat launch monopoly, and a satellite manufacturing division building missile-defense constellations for the U.S. Space Force. Q1 2026 was a record on every metric — $200.3 million in revenue, $2.2 billion in backlog, and more launches sold in a single quarter than in all of 2025. The question is not whether Rocket Lab is a legitimate aerospace prime. It is whether the $42 billion market cap gives enough room for what comes next.

01 — Origin & DNA

From New Zealand Garage to America’s Second Launch Provider

02 — Q1 2026 Earnings

Record Quarter: Every Guidance Metric Surpassed

Three data points from Q1 stood out beyond the headline beat. First, Rocket Lab sold more launches in Q1 2026 alone than in the entirety of FY2025 — an indication that the pipeline is compounding, not just growing linearly. Second, non-GAAP gross margin of 43% is converging toward the long-term 50%+ target management has guided, driven by Space Systems' higher-margin satellite manufacturing work. Third, the Adj. EBITDA loss of -$11.8M is approaching zero — which means the core business is nearly self-funding even as Neutron R&D spending accelerates. The Q2 EBITDA guide of -$20M to -$26M reflects deliberate reinvestment, not fundamental deterioration.

03 — Business Model

Two Engines, One Flywheel

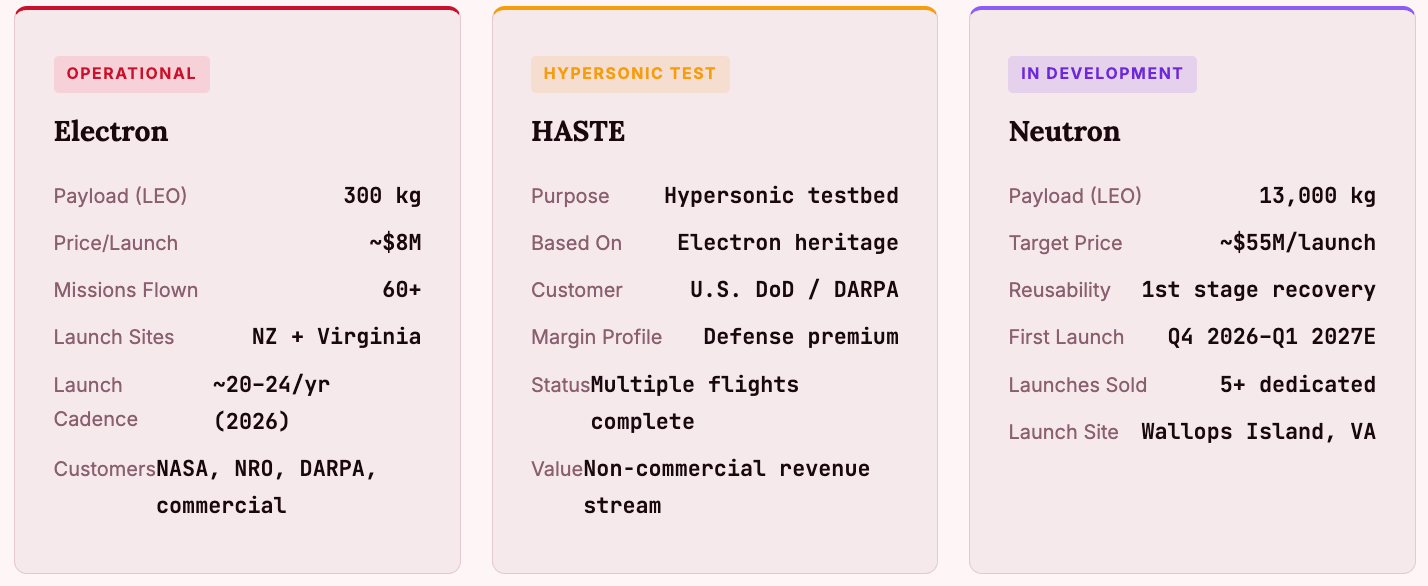

Rocket Lab’s business model is best understood as two interlocking engines that reinforce each other. The first engine is Launch Services — the Electron rocket for small satellites, the HASTE hypersonic testbed, and the in-development Neutron for medium-lift. The second engine is Space Systems — spacecraft components (solar cells, reaction wheels, separation systems, radios), full satellite buses (Photon), and now complete constellation manufacturing under SDA prime contracts.

The flywheel works like this: Electron launches make Rocket Lab the most reliable path to orbit for small satellites, which earns the trust of government and commercial customers. That trust earns Rocket Lab the right to compete for spacecraft and satellite manufacturing contracts. Those contracts scale the Space Systems margin profile and fund Neutron R&D. Neutron, once operational, unlocks the medium-lift market and constellation deployment economics that neither Electron nor SpaceX’s rideshare program efficiently serves. Each orbit reinforces the other.

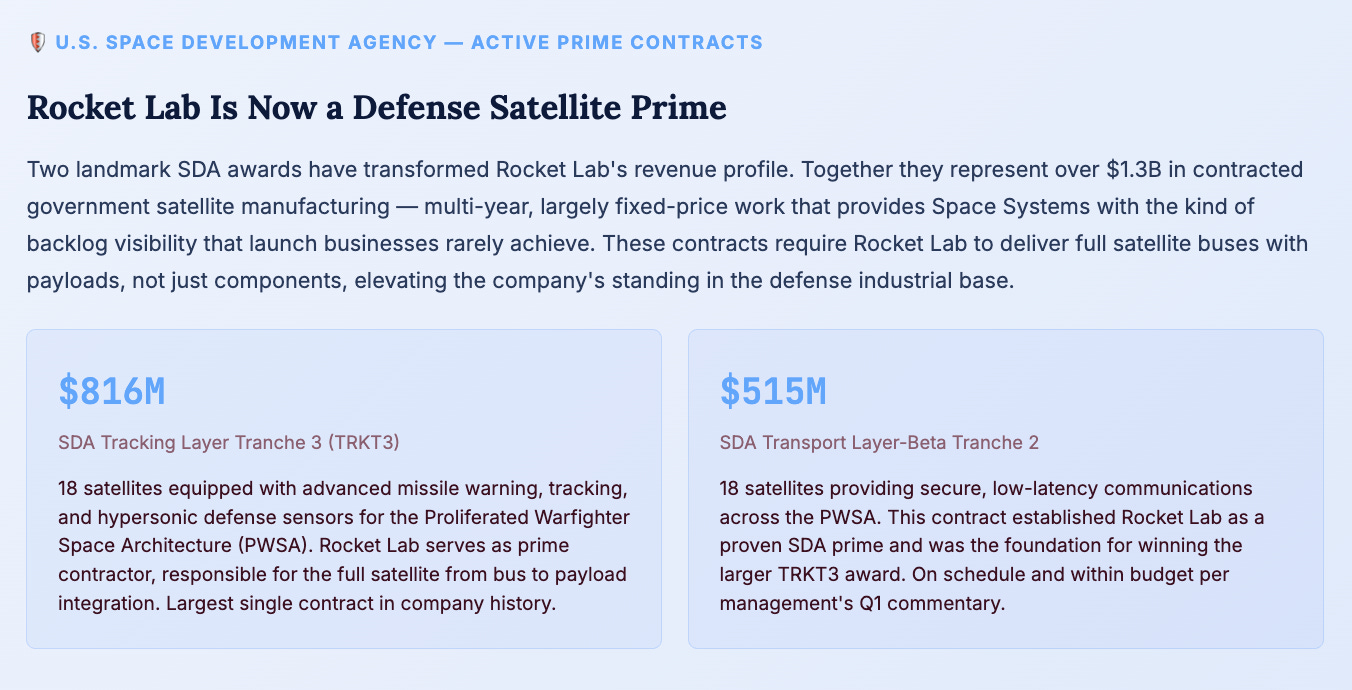

In Q1 2026, Space Systems represents approximately 60-65% of total revenue — the larger segment, and the higher-margin one. This is a notable structural shift from Rocket Lab’s early identity as “just” a launch company. The $1.3 billion-plus in active SDA satellite manufacturing contracts means Space Systems has multi-year revenue visibility that Launch Services has historically lacked.

04 — Electron: The Proven Machine

60+ Launches, One Clear Market Leader in Small Lift

Electron’s position in the market is structurally stronger than most investors appreciate. There are effectively no credible competitors at the dedicated small-lift price point. RocketX, Astra, and a dozen other small launch startups either failed or remain pre-revenue. ABL Space Systems shut down. Virgin Orbit went bankrupt. Relativity Space pivoted away from Terran 1. The result is that Electron has a near-monopoly on dedicated small-lift launches — a market that the proliferation of LEO constellations (Starlink, OneWeb, Planet Labs, Spire, and hundreds of national security satellites) continues to grow.

Electron is also progressing toward partial reusability. Rocket Lab has successfully recovered the first stage from the ocean multiple times and is working toward re-flight — which would meaningfully improve unit economics on the vehicle. At approximately 20-24 launches per year in 2026 at ~$8M average price, Electron generates roughly $160-190M in annual launch revenue. That alone does not justify a $42B market cap. But Electron is the foundation of trust that gets Rocket Lab into every other contract.

05 — Neutron: The Moonshot

The Big Bet That Could Double the Addressable Market

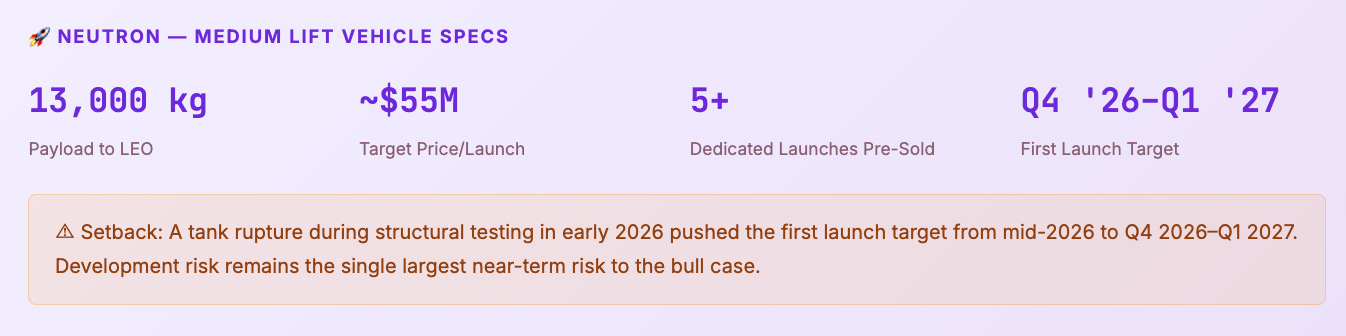

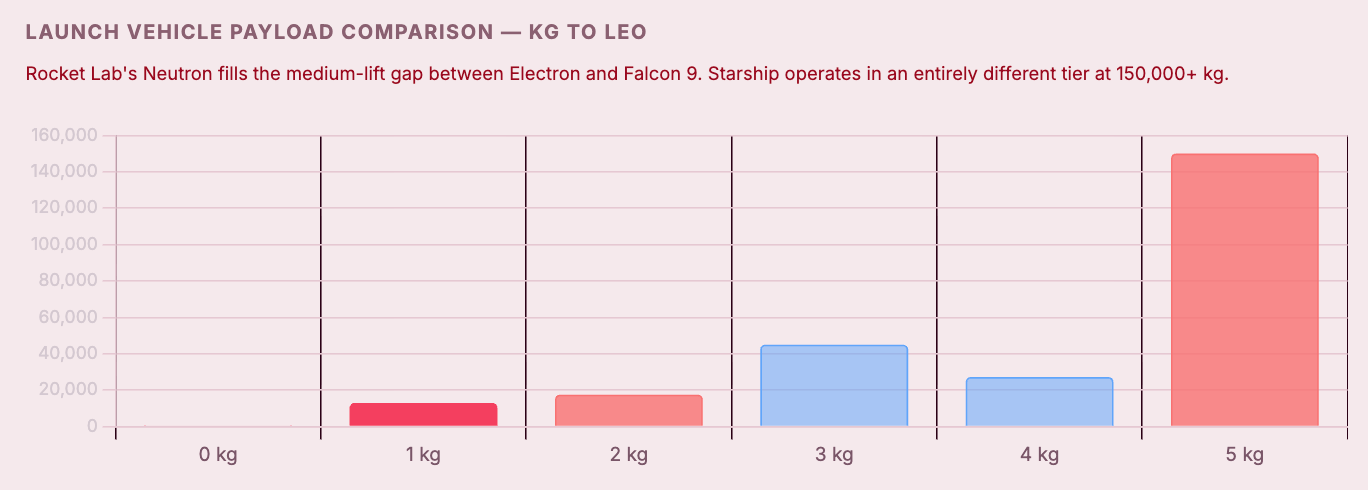

Neutron is Rocket Lab’s most important asset and most significant risk. At 13,000 kg to LEO with first-stage reusability and a $55M target launch price, it slots neatly into the gap between Falcon 9 (17,500 kg, ~$67-70M) and the small-lift market. Neutron is specifically designed for constellation deployment — launching 20-40 satellites per mission — which is the single fastest-growing segment of the launch market as both commercial operators and the Space Development Agency’s PWSA architecture demand thousands of LEO spacecraft.

The bullish read on Neutron is straightforward: there is genuine demand at $55M per launch for a reliable, reusable medium-lift vehicle that is not SpaceX. The U.S. government actively wants a second sovereign launch provider. The five dedicated Neutron launches already contracted — before the rocket has flown once — validate that demand is real and that customers are willing to pay for optionality away from SpaceX dependence. The biggest launch deal in Rocket Lab’s history, announced on the same day as Q1 earnings, included five Neutron flights through 2029 alongside three Electron missions.

The bearish read is harder to dismiss. SpaceX can price Falcon 9 at or below $55M if Neutron begins gaining commercial traction — its internal production cost is estimated at ~$15M per mission, giving enormous room to compete on price. Neutron’s 13,000 kg payload is meaningfully smaller than Falcon 9’s 17,500 kg, which matters for heavier government payloads. And the tank rupture setback is a reminder that rocket development is unforgiving: one more major delay could push first flight into 2027 or beyond, during which time SpaceX’s Starship will have demonstrated full reusability at orders of magnitude higher payload capacity.

06 — Space Systems & Defense

The Hidden Revenue Engine: $1.3B+ in Active Government Contracts

Beyond the SDA contracts, Space Systems manufactures components that appear in spacecraft across the industry — solar cells, reaction wheels (attitude control), separation systems, radios, and star trackers. These components are sold to third-party satellite builders, creating a diversified revenue stream that is not dependent on Rocket Lab winning prime contracts. With the Motiv acquisition adding solar array drive assemblies (SADAs) — one of the most constrained components in the supply chain — the Space Systems component business becomes more deeply embedded in the broader satellite manufacturing ecosystem.

The strategic logic of Space Systems is that it makes Rocket Lab harder to displace than a pure-play launch company. If SpaceX undercuts Neutron on price, Rocket Lab still captures revenue on the spacecraft and components being launched on Falcon 9. If SDA expands its PWSA architecture (and all indications from the Pentagon suggest it will), Rocket Lab is already positioned as a trusted satellite prime with delivery track record on the Transport Layer contract.

07 — Motiv Acquisition

Closing the Last Gap in Vertical Integration

Rocket Lab to Acquire Motiv Space Systems — Closes Q2 2026

Motiv Space Systems is a California-based company specializing in space robotics, motion control systems, and precision mechanisms. Its technology is Mars-proven — Motiv built the robotic arm on the Perseverance rover and has hardware operating on the lunar surface. The acquisition serves two strategic objectives: it brings in-house the solar array drive assemblies (SADAs) and other precision mechanisms that are currently costly to procure externally, and it adds deep planetary and national security robotics capability that positions Rocket Lab for beyond-Earth-orbit missions.

SADAs — Solar Array Drive AssembliesRobotic Arms & MechanismsMotion Control SystemsMars Heritage (Perseverance)Vertical Integration — Final Gap ClosedPlanetary & National Security Missions

SADAs are the motorized joints that rotate solar panels to track the sun as a spacecraft orbits. They are one of the most constrained and expensive components in satellite manufacturing — with lead times that can stretch 18-24 months from external suppliers. By bringing SADA production in-house, Rocket Lab gains both a supply chain advantage and a margin improvement on every satellite it manufactures. For the SDA constellations — 36 satellites across two programs — the cost savings compound significantly.

08 — Competitive Landscape

SpaceX Dominates, But the Market Is Bigger Than One Player

The competitive reality is nuanced. In the small-lift segment where Electron operates, Rocket Lab has no credible U.S. competitor — the graveyard of failed small launch startups (ABL, Astra, Virgin Orbit, Relativity Terran 1) has paradoxically strengthened Rocket Lab’s position. New entrants face enormous capital requirements and execution risk that has proven fatal even for well-funded teams.

In the medium-lift segment where Neutron will compete, SpaceX is the unavoidable benchmark. Falcon 9 is the world’s most reliable orbital rocket, and SpaceX has explicitly stated it can price competitively to prevent market share loss. However, two structural dynamics favor Neutron: first, U.S. national security customers are mandated to maintain multi-source launch capability and actively fund alternatives to SpaceX dependence. Second, Starship’s eventual dominance may actually cannibalize Falcon 9 rideshare economics, creating an opening for a dedicated medium-lift provider in the intermediate period.

The Starship question deserves its own paragraph. If Starship achieves full, rapid reusability at the scale SpaceX projects, the economics of the entire launch industry transform. Per-kilogram costs could fall below any current vehicle’s floor. The honest answer is that if Starship fully delivers on its promise in the 2027-2030 timeframe, it threatens the entire launch industry including Neutron. Rocket Lab’s hedge against this is Space Systems — manufacturing and components businesses that generate revenue regardless of which rocket performs the launches.

09 — Valuation

$42 Billion Is a Lot of Trust in Rockets Not Yet Flown