Salesforce: Agentforce Reaches $1.2B ARR, Record Margins Signal Structural Inflection

Agentforce annual recurring revenue hit $1.2 billion in Q1 FY2027 — a 205% year-over-year surge — as Salesforce reported record non-GAAP operating margin of 34.8%, accelerating revenue growth of 13%,

Section 01

Quarter at a Glance

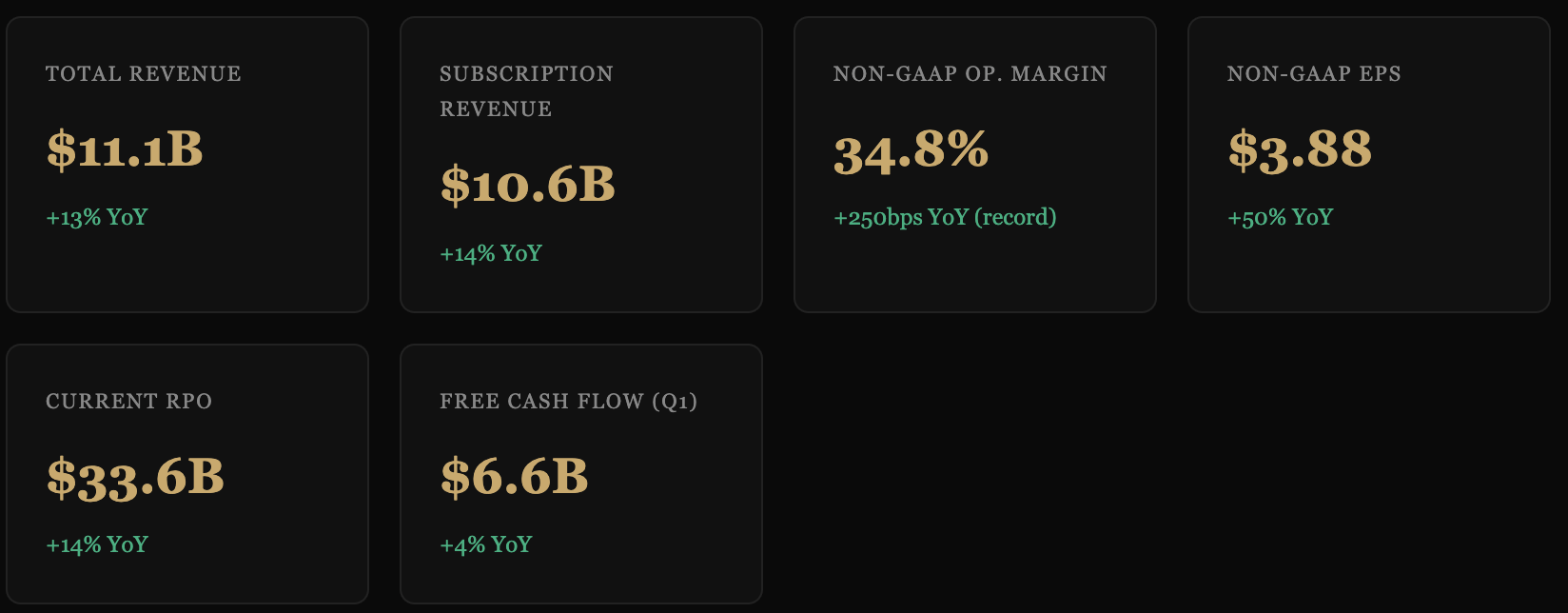

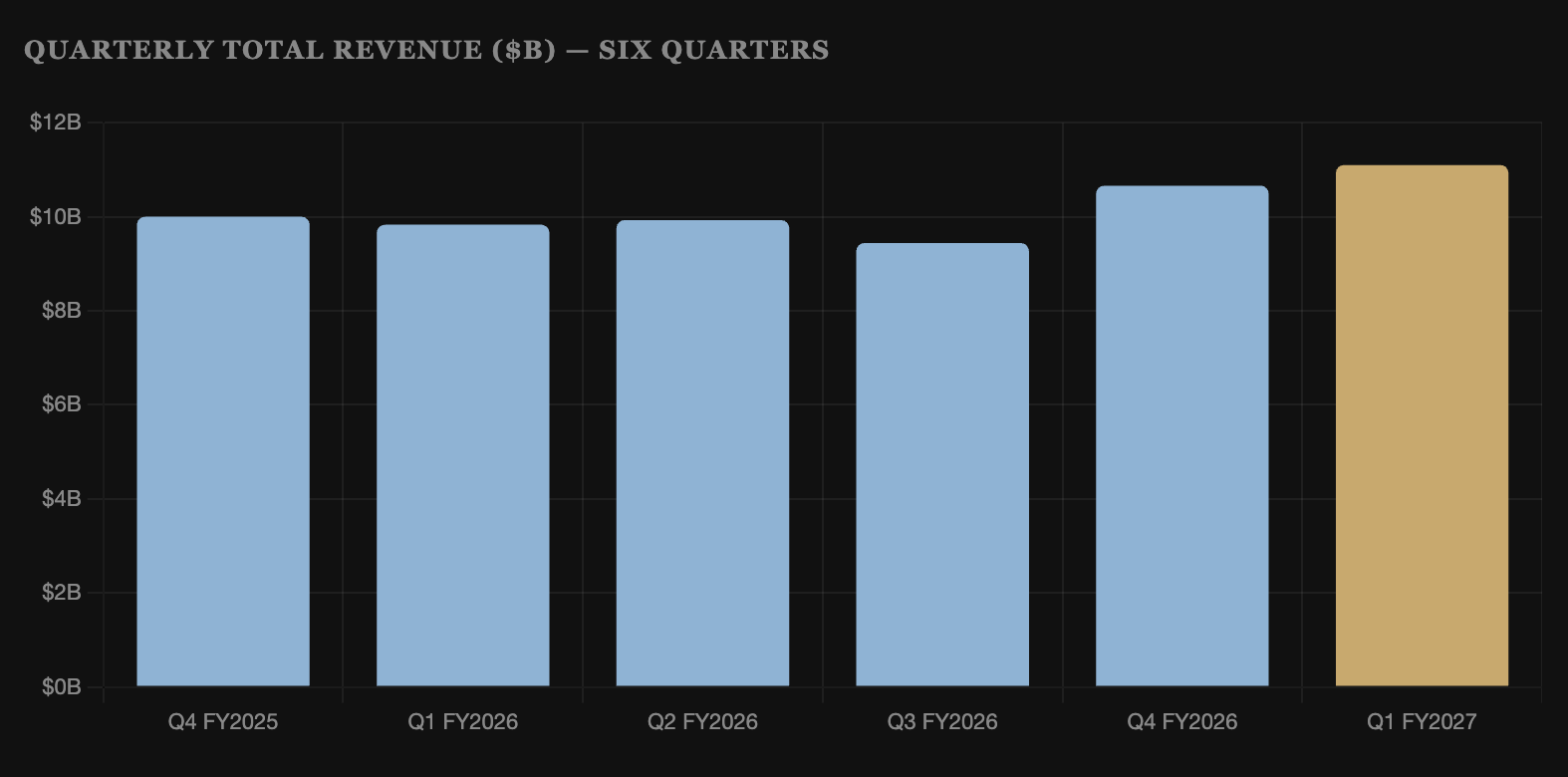

Salesforce’s fiscal Q1 2027 — the three months ended April 30, 2026, reported May 27, 2026 — was not a beat-and-raise quarter in the conventional sense. It was a statement of intent. Total revenue of $11.1 billion grew 13% year over year (12% in constant currency), an acceleration from the 8–9% range the company had been running at for several prior quarters. Subscription and support revenue, which now includes approximately $428 million from the recently closed Informatica acquisition, grew 14% to $10.6 billion. Professional services, increasingly an afterthought as agent-led deployment models reduce consulting dependence, contributed the remainder.

The headline that investors could not ignore: Agentforce annual recurring revenue reached $1.2 billion, representing 205% year-over-year growth. Combined AI and Data ARR — including Data Cloud and related products — surpassed $3.4 billion at a growth rate exceeding 200%. These are not rounding errors or accounting constructs. They are revenue numbers, and they arrived faster than even the optimistic case anticipated when Agentforce launched at Dreamforce in September 2024.

Non-GAAP EPS of $3.88 grew 50% year over year — a remarkably steep acceleration for a $40-billion-plus revenue company. GAAP EPS of $2.42 grew 52% YoY, narrowing the gap between GAAP and non-GAAP as Salesforce’s stock-based compensation as a percentage of revenue moderates at scale. Operating cash flow hit $6.7 billion for the quarter, with free cash flow of $6.6 billion after capital expenditures. Salesforce has announced a $25 billion accelerated share repurchase authorization and disclosed that it returned $27.5 billion to shareholders in the trailing period — a figure that would have seemed inconceivable five years ago from a company once synonymous with serial acquisitions and ignored buybacks.

Q2 FY2027 guidance calls for revenue of $11.27–$11.35 billion, implying 10–11% growth. Full-year FY2027 guidance was raised to $45.9–$46.2 billion (+11%), with non-GAAP operating margin guided at 34.3% — slightly below the Q1 record print as the company invests through the year, but still above the FY2026 exit rate.

Section 02

Agentforce — $1.2B ARR and the Consumption Flywheel

When Marc Benioff described Agentforce at Dreamforce 2024 as the most significant platform shift in Salesforce’s history — more consequential than the move to cloud, more transformative than the mobile era — the appropriate response was measured skepticism. Salesforce has a history of ambitious product proclamations. What has made Q1 FY2027 different is that the numbers have arrived to support the narrative.

Agentforce is Salesforce’s suite of autonomous AI agents designed to independently handle customer service interactions, qualify and advance sales opportunities, execute marketing workflows, and complete complex, multi-step enterprise tasks — without requiring a human in the loop for each decision. The architecture is fundamentally different from earlier AI copilot products, which were sophisticated autocomplete tools. Agentforce agents close the loop: receive an incoming support case, query the customer’s unified profile from Data Cloud, retrieve the relevant policy from a connected knowledge base, take action, and resolve the interaction — with human escalation only when the agent determines it is necessary or required.

“We delivered 3.8 billion Agentic Work Units this quarter and have processed 28.6 trillion tokens to date. The speed at which enterprises are deploying Agentforce agents in production workflows is unlike anything we have seen in the history of this company.”

— Marc Benioff, Chair and CEO, Salesforce, Q1 FY2027 Earnings Call, May 27, 2026 (paraphrased)

The scale metrics are instructive. 3.8 billion Agentic Work Units delivered in a single quarter, and 28.6 trillion tokens processed cumulatively, are not marketing statistics — they are consumption infrastructure metrics that imply meaningful enterprise adoption at production scale. These are not pilot deployments or sandboxed experiments. Enterprises are running Agentforce agents on live customer interactions in volume.

The pricing architecture is structurally important for the revenue model. Agentforce starts at $2 per conversation for standard interactions, with enterprise deals carrying custom consumption-based pricing. This decouples Salesforce’s revenue from customer headcount in ways that fundamentally change the company’s growth ceiling. A company deploying Agentforce to handle 15 million customer service interactions annually — a realistic number for a mid-to-large enterprise — is paying $30 million per year for that product alone, regardless of seat count. The revenue potential per customer expands dramatically relative to the traditional seat-based model, which plateaued as enterprises stopped hiring new salespeople and service agents at historical rates.

One striking leading indicator of platform momentum: Slack MCP (Model Context Protocol) surpassed one million active users within six weeks of launch — a viral adoption curve that underscores how deeply Slack’s AI-agentic integration has penetrated the existing user base. Slack is no longer simply a communication tool competing with Microsoft Teams on feature parity. It has become the conversational interface through which enterprises interact with Agentforce agents, query Data Cloud, and orchestrate agentic workflows — a positioning that substantially raises its strategic value within the Salesforce platform stack.

Public Sector Cloud ARR surpassed $2 billion and grew 23% year over year, suggesting that Agentforce’s penetration into government and regulated-sector enterprises is materially ahead of what the market had anticipated. Government agencies deploying AI agents for constituent services, permitting workflows, and case management represent a large and historically underpenetrated market for consumption-based AI.

Section 03

Revenue Composition and Informatica Integration

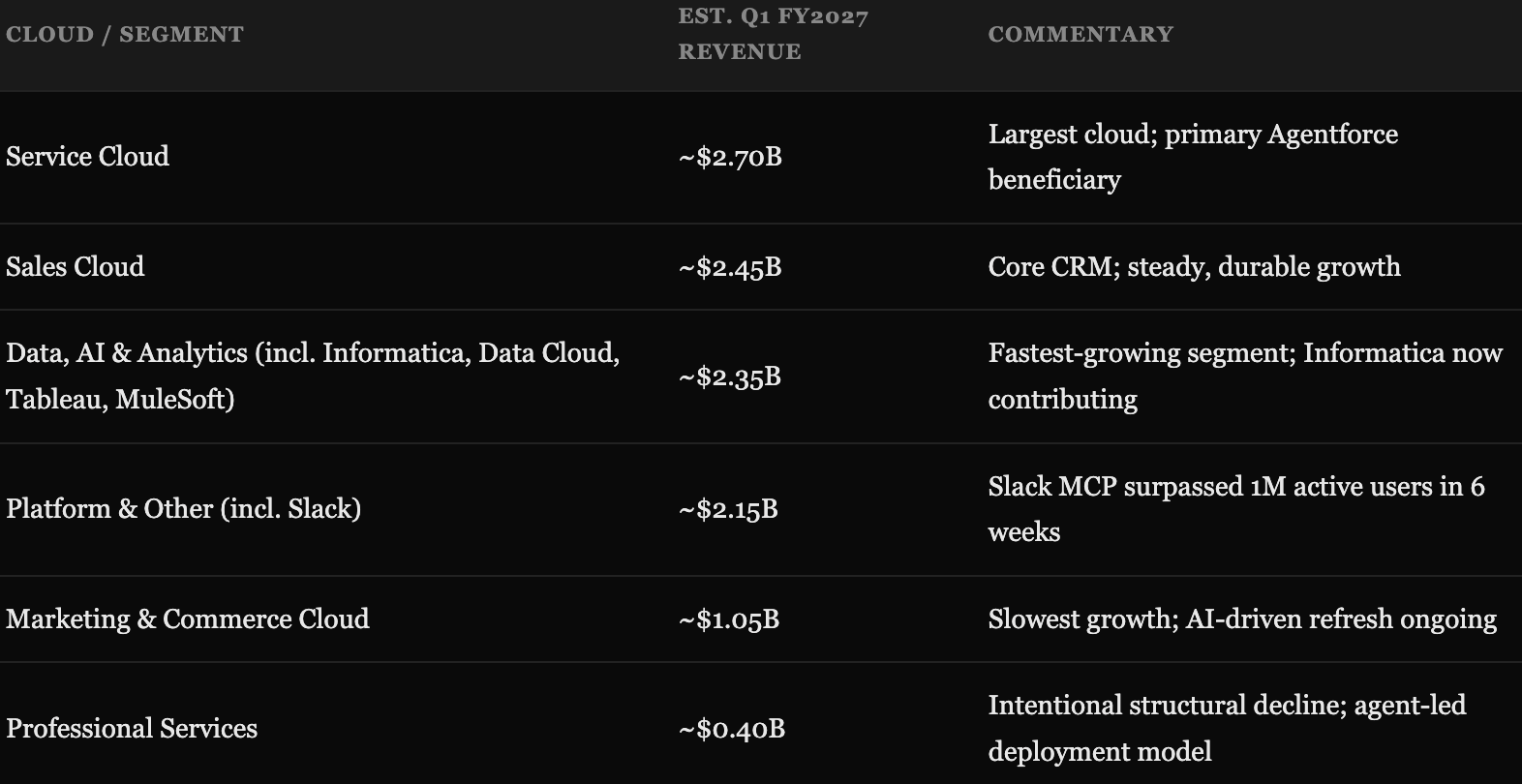

Salesforce’s Q1 FY2027 revenue of $11.1 billion reflects the first full quarter of Informatica contributing to results following the closing of that acquisition. Informatica contributed approximately $444 million to total revenue in Q1 FY2027, with approximately $428 million falling within subscription and support. This means organic revenue growth — excluding Informatica — ran at roughly 8–9%, consistent with recent trends, while the reported 13% reflects acquisition contribution plus incremental Agentforce and Data Cloud momentum layered on top.

Service Cloud at an estimated $2.7 billion remains the single largest revenue contributor and is the most direct commercial beneficiary of Agentforce. Contact center automation is the clearest near-term AI use case for autonomous agents — the ROI is quantifiable, the workflows are well-defined, and Salesforce holds home-field advantage through its installed base of existing Service Cloud data. The combination of Agentforce agents handling routine case resolution while human agents handle escalations is producing measurable cost-per-contact improvements for early adopters, which is driving deal expansion in existing accounts.

The Data, AI & Analytics segment — which now bundles Informatica’s enterprise data management capabilities alongside Data Cloud, Tableau, and MuleSoft — is strategically the most important segment to monitor over the next several years. Informatica brings enterprise data governance, data cataloging, and master data management capabilities that deepen Salesforce’s position as an end-to-end enterprise data infrastructure provider. The combination of Informatica’s data management heritage with Data Cloud’s real-time AI unification layer is a meaningful technical stack, though integration complexity should not be underestimated. Salesforce is assembling the plumbing that makes enterprise AI reliable and compliant — arguably more valuable, if less glamorous, than the agent interface layer itself.

Professional services revenue declining to an estimated $400 million represents a deliberate and structurally positive mix shift. As Agentforce enables faster, lower-touch deployment of new capabilities — with agents handling configuration, onboarding guidance, and workflow optimization tasks that previously required consultants — the labor-intensive services revenue profile becomes less relevant. The margin implications are favorable: professional services carries below-average margins, and its intentional contraction improves the overall revenue quality of the Salesforce income statement.

Section 04

The Margin Inflection: 34.8% Non-GAAP and a New Ceiling

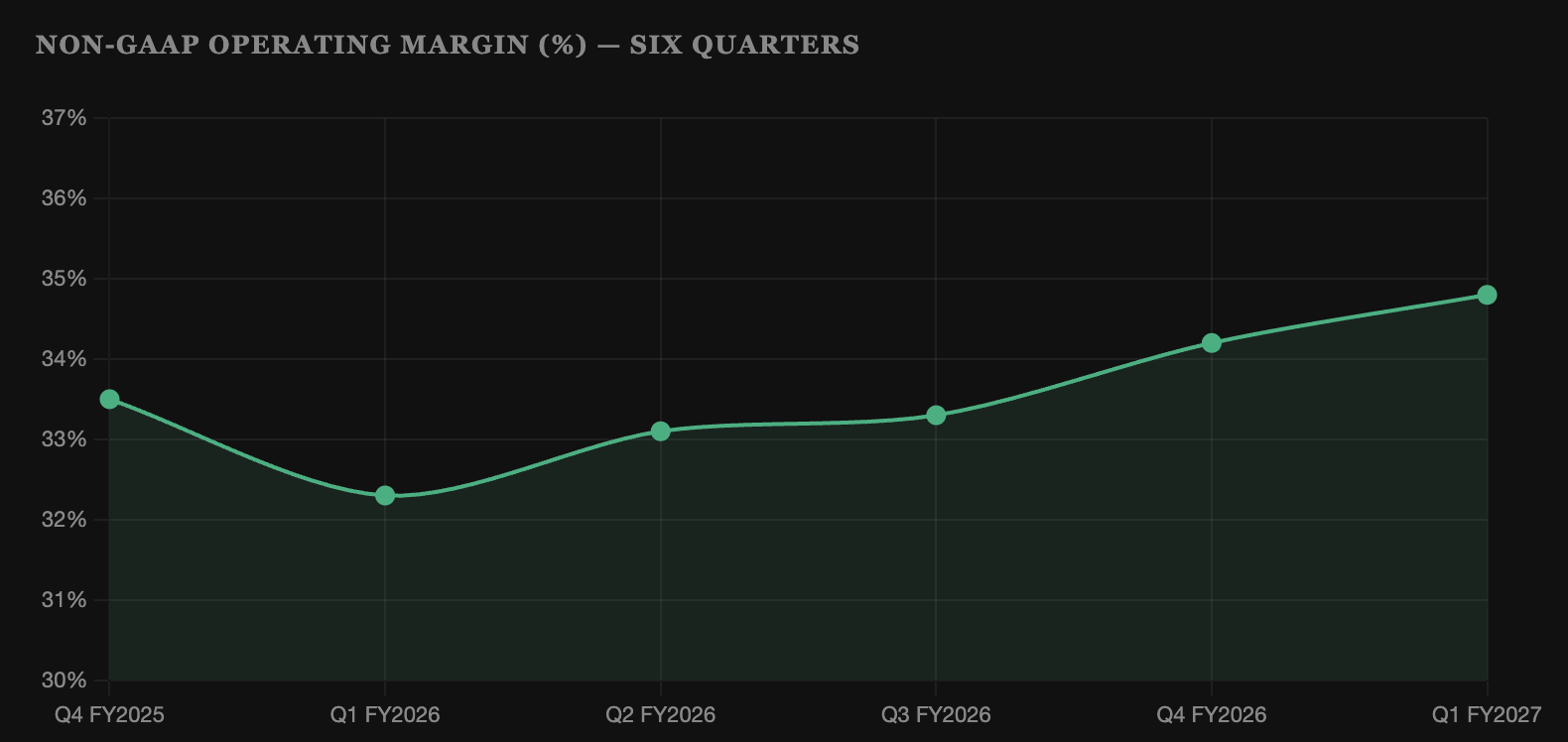

Non-GAAP operating margin of 34.8% in Q1 FY2027 is a record for Salesforce, arriving approximately 1,250 basis points above the 22.5% reported in FY2023 — an expansion that has been among the most dramatic in large-cap enterprise software history. The question the market is now wrestling with is whether 34–35% represents the ceiling, or whether the agentic AI flywheel will create a new margin expansion chapter on top of the structural reset already achieved.

The structural drivers of the margin story are well-documented. The 2023 restructuring — which included reducing the global workforce by approximately 10%, cutting real estate footprint substantially, and ending the era of transformative M&A — reset the cost base in ways that have proven durable. Headcount efficiency has improved meaningfully: Salesforce is generating materially more revenue per employee than at its peak headcount. G&A leverage continues to compound at scale. And the mix shift away from professional services toward high-margin subscription and consumption revenue improves the blended margin profile each quarter.

Non-GAAP EPS of $3.88 grew 50% year over year — a pace that reflects not just margin discipline but the compounding interaction between operating leverage and buyback-driven share count reduction, producing earnings growth roughly four times the rate of revenue growth.

— LongYield Analysis, Q1 FY2027 Results

GAAP operating margin of 21.1% remains substantially below the non-GAAP figure, primarily because of stock-based compensation running at approximately 8–9% of revenue. This is structurally lower than the 12–14% SBC ratios Salesforce carried during its hypergrowth years, reflecting both deliberate compensation governance improvement and the denominator effect of a larger revenue base. The buyback program — $27.5 billion returned to shareholders in the trailing period, with a new $25 billion ASR authorization — provides meaningful offset to ongoing dilution. GAAP EPS of $2.42, up 52% year over year, reflects real economic progress even on the fully-loaded measure.

The forward margin question is genuinely uncertain. The bull case argues that Agentforce is a software product with near-zero marginal cost of delivery per conversation, and that as consumption volumes scale, the incremental margin profile should be exceptional — similar to how cloud infrastructure businesses saw strong incremental margins as workloads compounded. The bear case argues that sustained AI infrastructure investment — model training, Data Cloud compute, Informatica integration, and R&D against competitors building their own agentic platforms — will cap margin expansion at current levels. Management’s full-year FY2027 non-GAAP operating margin guidance of 34.3% implies modest conservatism from the Q1 record, but the company has consistently guided below its eventual delivery over the past several years. A full-year print at or above 35% is the bull scenario to watch.

One important clarification for investors: free cash flow is probably the cleanest margin proxy for this business. Q1 FY2027 FCF of $6.6 billion on $11.1 billion in revenue represents an approximately 60% FCF margin for the quarter — an extraordinary number, though Q1 is seasonally the strongest quarter for Salesforce due to elevated cash collections from annual enterprise subscriptions billed at fiscal year-end (January 31, the end of Q4). On a full-year basis, Salesforce has consistently generated FCF margins in the 30–35% range, which remains among the highest in large-cap enterprise software.

Section 05