Samsung Electronics: The AI Supercycle Meets Conglomerate Optionality

The world's largest memory maker just posted the most profitable quarter in its history — KRW 57.2 trillion in operating profit in a single quarter, exceeding its entire 2025 full-year total. The HBM catastrophe is over. The memory cycle is vertical. The foundry turnaround is a work in progress. And the stock still trades at a single-digit forward earnings multiple. This is the full picture.

01 · The Investment Thesis

Samsung Electronics is the only investable public entity on earth that offers simultaneous pure-play exposure to three of the most strategically important subsectors of the global technology stack: AI memory (the fuel for every GPU cluster on the planet), advanced semiconductor foundry (the manufacturing base that everything runs on), and premium consumer electronics (the platform through which two billion people experience computing every day). Each of these businesses is, in isolation, a multi-hundred-billion-dollar opportunity. The fact that they cohabit inside a single Korean conglomerate — with a consequent structural valuation discount — is precisely what makes Samsung interesting to the institutional investor with a genuine time horizon.

The investment case has undergone a fundamental re-rating in the first half of 2026. For the better part of two years, the narrative around Samsung was almost uniformly bearish: it missed the first-generation HBM3E qualification window with NVIDIA, ceding meaningful ground to SK Hynix at exactly the moment when high-bandwidth memory became the most valuable semiconductor product in the world; its foundry division continued bleeding red ink against a dominant TSMC; and its mobile business faced margin compression from both ends — Apple’s iPhone at the premium tier and Chinese OEMs relentlessly grinding away at mid-range. That narrative, while largely accurate, failed to account for what a normalized memory cycle — let alone the AI-induced memory supercycle now underway — does to Samsung’s earnings power.

Q1 2026 answered that question definitively. Revenue of KRW 133.9 trillion. Operating profit of KRW 57.2 trillion. An operating margin of 42.7%. A single quarter whose profits exceeded the company’s entire 2025 full-year total. The AI-driven memory cycle is not a quarterly blip — structural demand from hyperscaler AI infrastructure, the proliferation of HBM4 as the standard memory substrate for next-generation AI accelerators, and a DRAM pricing environment that TrendForce is calling the most extreme up-cycle in the industry’s history collectively suggest this run has years, not quarters, of runway. Samsung has now qualified for NVIDIA’s Vera Rubin platform as an HBM4 supplier alongside SK Hynix and Micron, and it has already sold out its entire 2026 HBM production allocation.

The thesis rests on four pillars. First, Samsung is the primary structural beneficiary of the AI memory supercycle — it produces DRAM, NAND, and HBM at a scale no other company can match, and the pricing environment for all three is at historic extremes with no credible relief mechanism before late 2027 at the earliest. Second, the HBM recovery story is now a fact rather than a promise: Samsung has completed the transition from embarrassing NVIDIA qualification failures to being a named supplier on the next-generation Vera Rubin platform. Third, the foundry business, while still challenged, represents a free option on a continued TSMC capacity crunch — as TSMC’s 2nm capacity books out, any Samsung yield improvement becomes immediately monetizable against a captive demand set. Fourth, and most importantly from a valuation standpoint, the market continues to apply a conglomerate discount that values Samsung at roughly 6–9x forward earnings — a fraction of the multiples commanded by pure-play peers like SK Hynix (20x+) and TSMC (25x+).

The Core Tension

Samsung’s structural complexity is simultaneously its greatest competitive advantage and its greatest valuation liability. The same conglomerate architecture that lets it cross-subsidize foundry losses with memory profits and invest KRW 110 trillion in semiconductor R&D and capex in a single year — the largest single-year semiconductor investment in history — is the same structure that makes Western and international institutional investors skeptical about capital allocation discipline, minority shareholder rights, and governance opacity. That tension is the opportunity for investors who can get comfortable with it.

Understanding the Corporate Structure

Samsung Electronics is a publicly listed subsidiary within the broader Samsung Group conglomerate — a fact that matters for governance analysis but less for financial modeling, since Samsung Electronics is itself a near-complete ecosystem. Within Samsung Electronics, there are four primary reporting divisions: the DS (Device Solutions) Division, which encompasses memory, System LSI, and Samsung Foundry; the DX (Device eXperience) Division, which includes the MX (Mobile eXperience) and VD/DA (Visual Display and Digital Appliances) businesses; Samsung Display Corporation (SDC), which manufactures OLED panels primarily for Samsung’s own devices and Apple; and Harman International, the separately operated subsidiary acquired in 2017 for $8 billion that produces premium audio equipment, automotive infotainment systems, and connected car technology.

DS Division

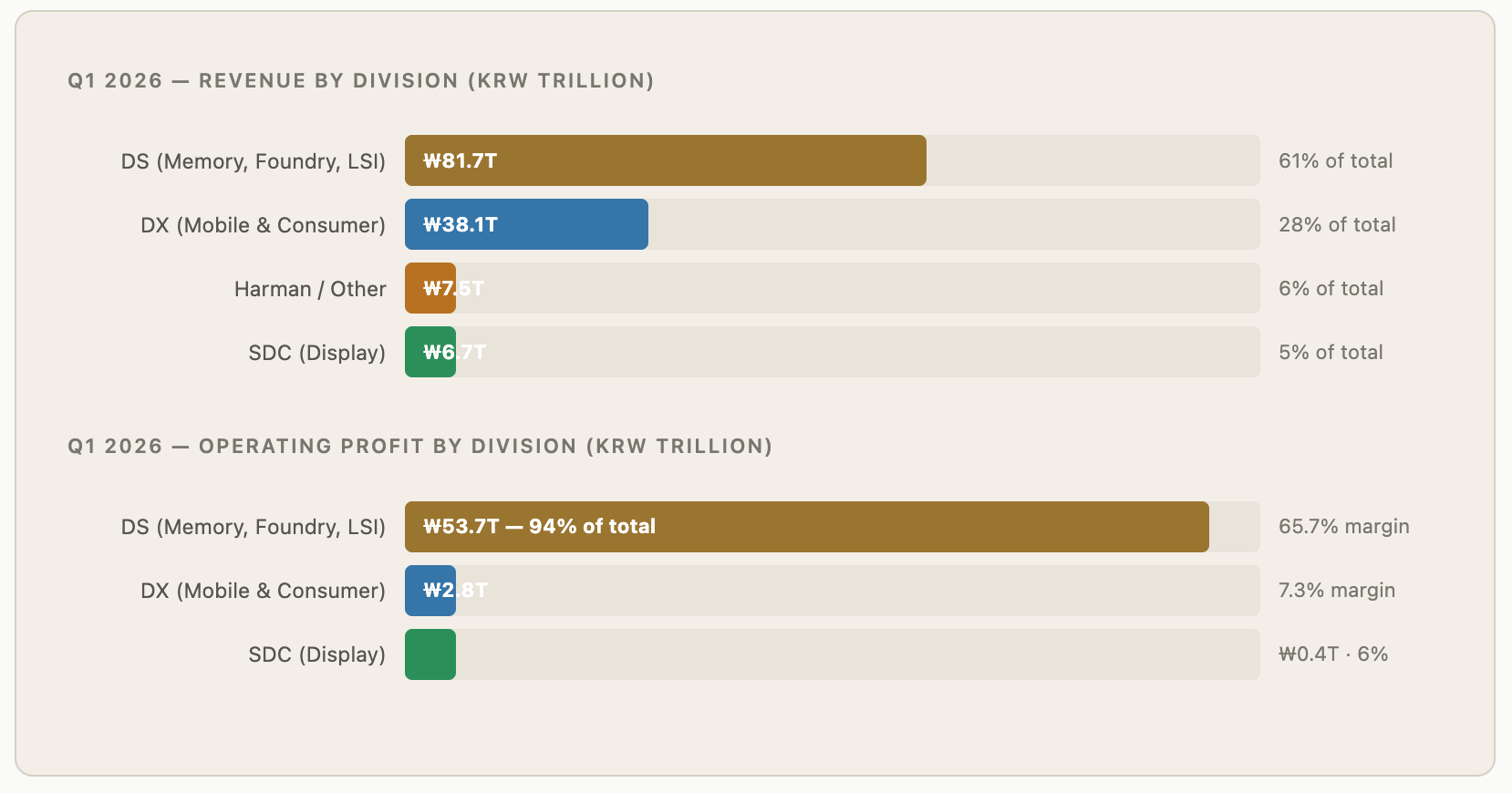

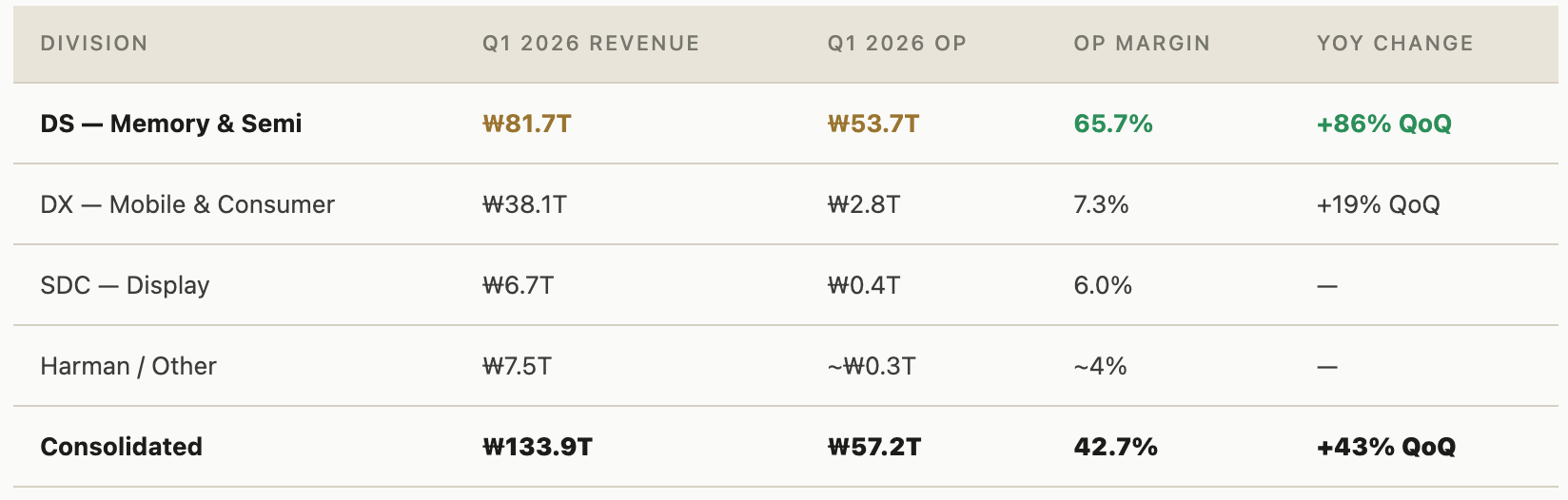

Device Solutions — Memory (DRAM, NAND, HBM), System LSI (Exynos, image sensors), and Samsung Foundry. The profit engine. Generated 94% of total Q1 2026 operating profit.

DX Division

Device eXperience — Smartphones, tablets, wearables (MX), plus TVs and home appliances (VD/DA). Revenue-heavy but margin-thin at ~7%. Faces pressure from Apple above and Chinese OEMs below.

SDC

Samsung Display Corporation — Makes OLED panels for Galaxy devices and supplies Apple iPhone displays. Structural oligopoly position. Margins compressed recently but stable cash flow.

Harman

$11.4B/year consumer and automotive audio and connected-car technology business. JBL, Harman Kardon, AKG brands. Acquiring ZF’s ADAS unit for €1.5B, positioning for automotive AI.

HBM

High-Bandwidth Memory — a stacked DRAM architecture that delivers 10–15x the data throughput of conventional DRAM at the cost of much higher ASPs. The dominant memory substrate for AI GPU accelerators.

DRAM Cycle

Memory semiconductors are acutely cyclical — supply expands, prices collapse, capacity exits, then demand recovers. AI demand has structurally altered the cycle’s amplitude and duration dynamics.

02 · Most Recent Results — Q1 2026 in Detail

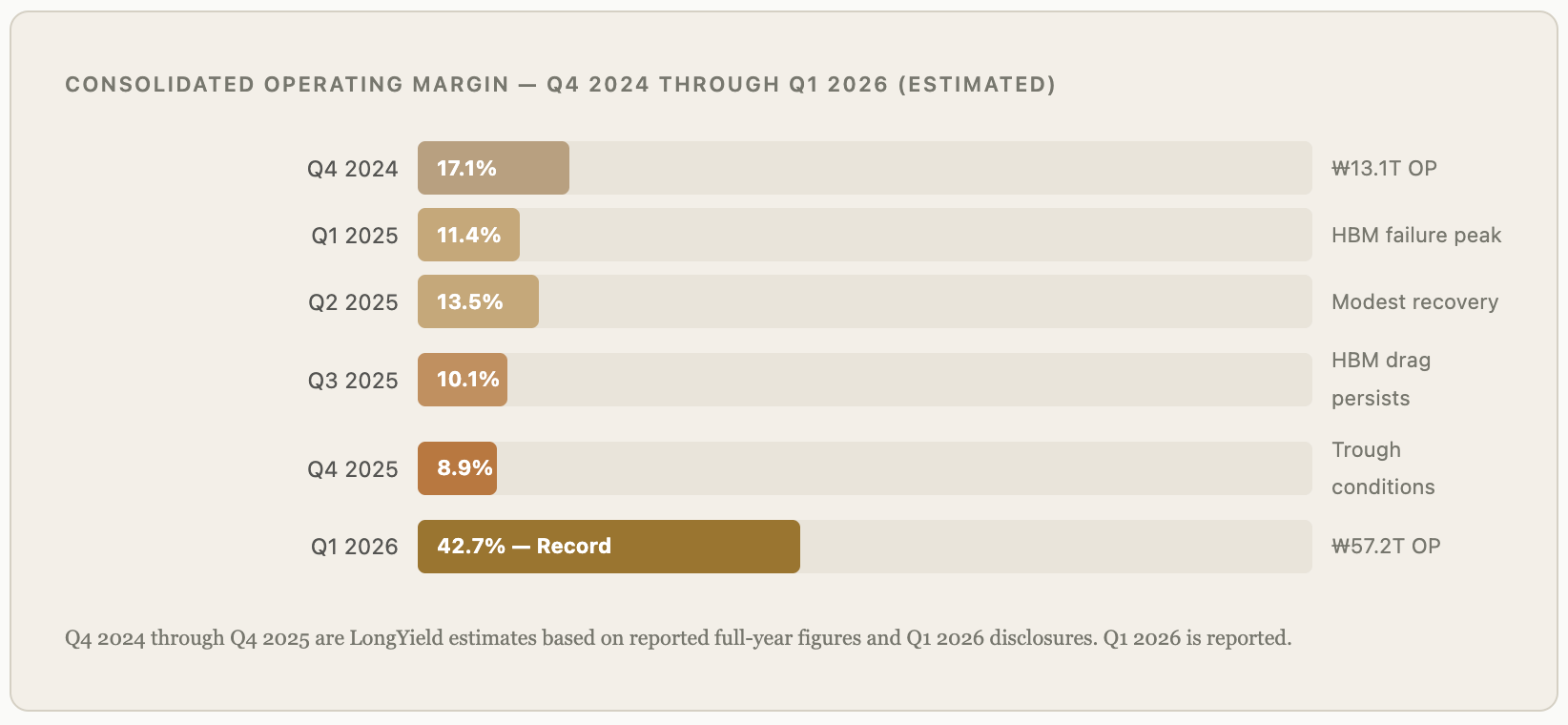

Samsung Electronics reported its first-quarter 2026 results in late April, and the numbers were categorically unlike anything in the company’s 50-year history. Consolidated revenue hit KRW 133.9 trillion, a 43% sequential increase and an all-time record for a single quarter. Operating profit reached KRW 57.2 trillion — also a record — representing an operating margin of 42.7%. To put the magnitude in perspective: Samsung’s Q1 2026 operating profit alone exceeded the company’s entire fiscal year 2025 aggregate operating income. At prevailing exchange rates, Samsung generated roughly $41.5 billion in operating profit in a single quarter, placing it among the most profitable three-month periods of any industrial company anywhere, in any industry.

The engine is almost entirely the DS division and, within it, almost entirely the memory business. The Device Solutions division reported KRW 81.7 trillion in revenue (61% of consolidated total) and KRW 53.7 trillion in operating profit — a 65.7% divisional operating margin that reflects the extraordinary pricing power of a memory supplier in a structural undersupply environment. Memory operating profit was described in Samsung’s earnings presentation as up “nearly 50-fold” year-over-year, a figure that, while arithmetically extreme, accurately reflects the depth of the 2025 memory trough from which prices have now rebounded. The Memory Business set all-time high quarterly records for both revenue and operating profit.

The DX division was the contrasting story — one that requires careful reading. Revenue of KRW 38.1 trillion was respectable on an absolute basis, supported by the launch of the Galaxy S26 series in early 2026 and the continued rollout of the Galaxy Z Fold and Z Flip foldable lineup. But operating profit of KRW 2.8 trillion on that revenue base implies a 7.3% margin — thin by any global technology hardware standard, and reflecting the structural pressure on smartphone economics when Apple commands premium margins at the top of the market and Xiaomi, OPPO, and Vivo squeeze aggressively through the mid-range. The DX division generated 28% of Samsung's consolidated revenue but only 5% of its operating profit. That asymmetry is the defining financial characteristic of Samsung's conglomerate structure: a high-volume, low-margin consumer business sitting alongside the most profitable per-unit product in the semiconductor industry.

Operating Margin — Six-Quarter Trend

The margin trajectory is the most compelling single chart in Samsung’s financial history. For most of 2025, Samsung operated with consolidated operating margins in the high single digits to low teens — weak by any historical standard, reflecting HBM qualification failures in the DS division, the associated opportunity cost versus SK Hynix, and a still-depressed NAND pricing environment. The Q1 2026 inflection is not gradual; it is vertical, driven by the simultaneous re-rating of memory ASPs, the ramp of HBM volumes to Nvidia, and the beginning of the broader AI memory supercycle.

Guidance and Forward Commentary

Samsung guided for continued strong demand across the DS division heading into Q2 and beyond, citing sustained AI infrastructure buildout from hyperscalers and the ramp of new AI accelerator platforms. Samsung’s own management commentary included what is, for a conservative Korean conglomerate, an unusually direct warning: memory supply tightness is expected to persist into 2027, and the company is warning customers to secure long-term supply agreements now. That is not a company hedging its cycle outlook — it is a company telling the market that the structural undersupply has years of duration.

03 · The Memory Business — The Engine of Everything

Memory semiconductors are, in the context of the global AI infrastructure buildout, among the scarcest and most strategically critical manufactured goods on earth. Every GPU cluster requires vast quantities of DRAM to store model weights and activations during inference and training. HBM — a specialized, stacked form of DRAM — is the substrate that attaches directly to NVIDIA’s H100, H200, and now Blackwell and Vera Rubin GPUs, delivering the data bandwidth that the GPU’s compute engines require. Without sufficient HBM, NVIDIA cannot ship GPUs. Without sufficient conventional DRAM, AI servers cannot operate at scale. And without sufficient NAND, the storage infrastructure that underpins cloud AI deployment cannot expand. Samsung is the world’s largest producer of all three.