Seagate Technology: The Last Drive Standing

Seagate Technology and the unexpected resilience of spinning rust in the age of AI

For a company whose core product was supposed to be obsolete by now, Seagate

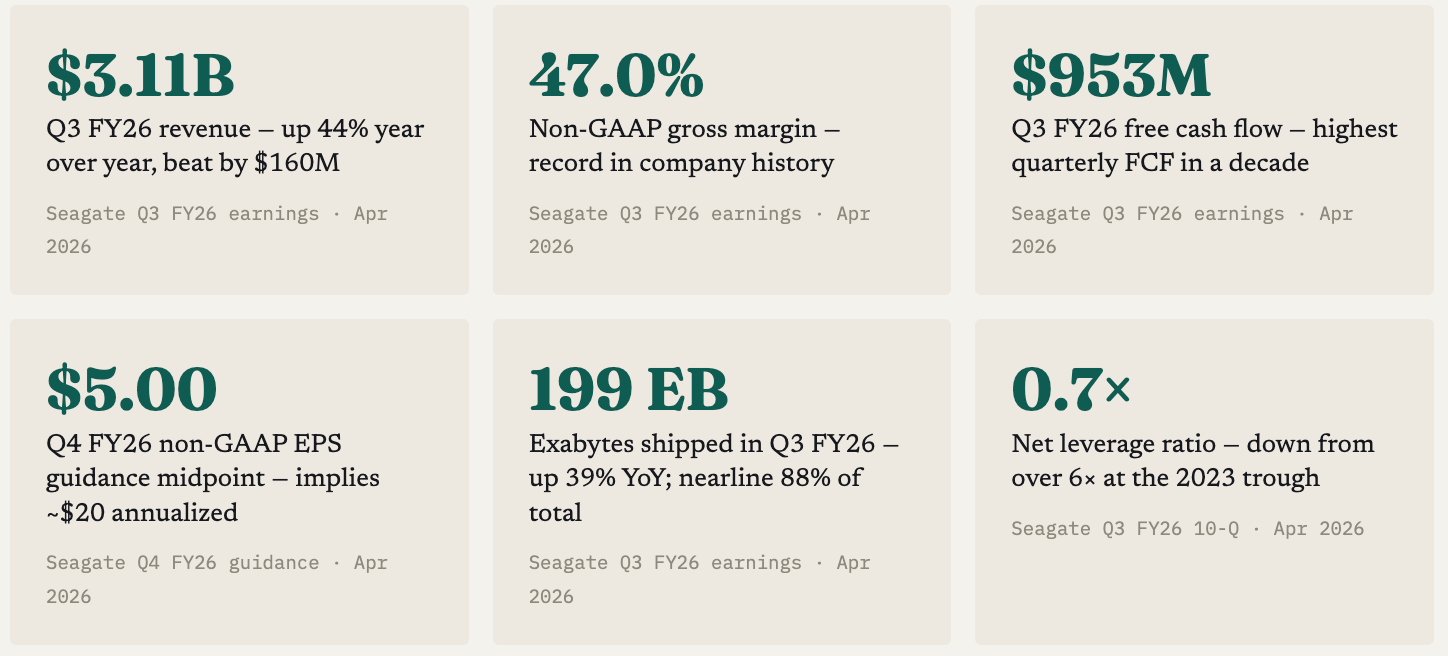

Technology Holdings is having a remarkable year. In its fiscal third quarter of 2026, the hard drive maker reported revenue of $3.11 billion — up 44 percent year over year, more than $150 million ahead of Wall Street consensus — alongside non-GAAP gross margins of 47.0 percent, a record in the company's four-decade history. Free cash flow reached $953 million, the highest quarterly figure in a decade. Management guided for $3.45 billion in revenue and $5.00 in non-GAAP earnings per share for the coming quarter.[1] The stock, which traded below $130 just twelve months ago, has crossed $930. The obituary for the hard disk drive was premature, and understanding why is the key to one of the most consequential turnarounds in the enterprise storage supply chain.

The AI Storage Supercycle

The conventional wisdom about hard disk drives was written sometime around 2015, in the giddy early years of NAND flash price collapse, when storage pundits confidently declared that spinning magnetic media would follow CDs and film cameras into obsolescence. It made intuitive sense. SSDs were getting cheaper every year, faster by orders of magnitude, and the cultural narrative had one direction. The HDD was a dead man walking.

What nobody adequately modeled was artificial intelligence — not the concept, but the physical infrastructure that running AI at planetary scale actually requires. Training a frontier large language model demands ingesting hundreds of petabytes of text, images, video, and code. Running it in production means retaining user interaction histories, query logs, retrieval corpora, model checkpoints, and version archives. Every AI assistant query — and there are billions daily across the major platforms — produces data that must persist somewhere cost-effectively.

The “somewhere” has a name: nearline hard disk drives. These are the high-capacity, high-reliability 3.5-inch drives that populate the racks of hyperscale data centers, occupying the storage tier below NVMe SSDs (used for active computation) and above tape (used for deep archival). They handle what the industry calls cold and warm storage — data that must be accessible on demand but is not being actively processed in real time. In a typical AI data center today, HDDs account for more than 80 percent of total raw storage capacity by volume.[2]

The four major hyperscalers — Amazon, Alphabet, Microsoft, and Meta — have committed extraordinary capital to AI infrastructure. Together, they are expected to spend approximately $725 billion on capital expenditures in 2026, up roughly 77 percent from last year’s already-elevated baseline.[3] Most of that flows to GPUs, networking, and real estate. But storage is not optional. Every AI server cluster needs its data reservoir, and those reservoirs are overwhelmingly hard drives.

“Storage price hikes are the new normal. We are in a demand environment unlike anything we have seen before.”— Ban-Seng Teh, Chief Commercial Officer, Seagate Technology, 2025[4]

The supply side has not kept pace with demand. Seagate’s Chief Commercial Officer, Ban-Seng Teh, said in late 2025 that storage price hikes had become “the new normal,” calling current conditions an “unprecedented supercycle” driven by AI that differs fundamentally from prior storage cycles. The distinction he drew is structural: hyperscalers are not accumulating speculative safety stock — they are building committed, multi-year AI infrastructure with known storage requirements. As evidence: Seagate’s nearline hard drive production is entirely on allocation through calendar year 2027, with purchase orders in hand for 2027 and preliminary supply discussions already underway for 2028 and beyond.[5]

Total HDD exabyte shipments industry-wide surpassed 450 exabytes annually by late 2025, resuming a sustained upward trajectory after the severe 2022–2023 inventory correction.[6] Western Digital’s management has projected a base case of 15 percent CAGR in exabyte demand through the end of the decade, rising to 23 percent with AI uplift. Seagate’s results appear to be tracking the upper end of that forecast.

HAMR: A Decade-Long Bet That Changed the Game

For most of its modern history, Seagate improved storage density by making magnetic domains smaller — a technique called perpendicular magnetic recording (PMR), later enhanced with energy assistance (ePMR). The problem with miniaturizing domains is thermal instability: below a critical size, the magnetic bits can spontaneously flip their polarity, corrupting data. This is the superparamagnetic limit, and it has constrained the HDD industry for two decades.

The solution Seagate committed to — at enormous R&D expense over more than a decade — is heat-assisted magnetic recording, or HAMR. The principle is elegant: by briefly heating a tiny spot on the disk with a near-field laser built directly into the read/write head, you can use magnetic materials with extremely high coercivity (resistance to accidental demagnetization) that would otherwise be unwritable at room temperature. When the spot cools in nanoseconds below the Curie temperature, it freezes in the new magnetic state with exceptional long-term stability.

The engineering challenge involved is nearly incomprehensible in its difficulty. The laser must heat a spot roughly 25 nanometers across — smaller than many viruses — to approximately 450 degrees Celsius, then allow it to cool in nanoseconds, reliably repeating this cycle millions of times per second across the drive’s expected 5-plus-year operational lifetime in a vibrating rack. New magnetic recording media — iron-platinum alloys, or FePt, deposited on a glass platter substrate, with coercivity an order of magnitude higher than conventional cobalt-alloy media — new lubricant chemistry, new thermal management architectures, and years of customer qualification work were all required before a single HAMR unit shipped in volume.

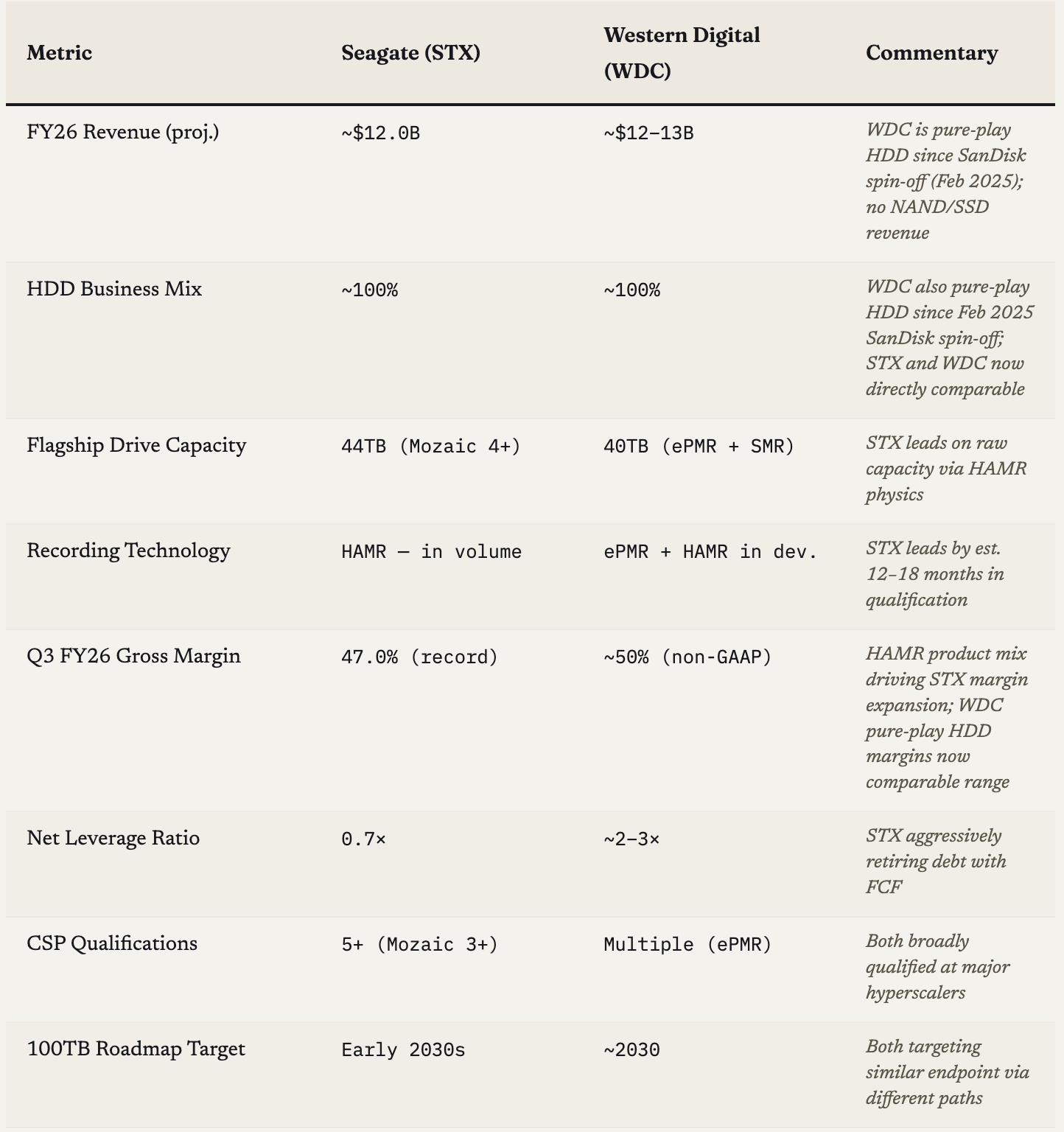

Seagate was first to commercialize this technology. Its Mozaic platform — now in its fourth generation, the Mozaic 4+ — ships at up to 44 terabytes per drive using 10 platters at 4.4 terabytes per disk, making it the highest-capacity shipping HDD on the market as of 2026.[7] Two leading hyperscalers have begun volume procurement of Mozaic 4+ drives, with two more in active qualification ahead of an expected volume ramp in the second half of 2026.[8] Five cloud service providers in total have qualified the prior-generation Mozaic 3+ (up to 36TB), giving Seagate broad footprint across the world’s most important storage buyers. Seagate reports having shipped more than 1.5 million HAMR units to date, with Mozaic 4+ drives achieving an annualized failure rate of 0.35 percent — competitive with conventional drives despite the technological complexity involved.

The competitive moat that HAMR creates is real and time-bounded: it took Seagate more than a decade and billions in cumulative R&D to get here. Western Digital, the only other supplier that matters at hyperscale, is pursuing a dual-track strategy — extending its own ePMR technology while gradually ramping a separate HAMR program. WDC’s 40TB drive, in hyperscaler certification in 2026 with volume shipments targeted for H2 2026, reaches its capacity through ePMR combined with UltraSMR shingled recording, which writes overlapping tracks to achieve density at the cost of sequential-write performance penalties.[9] Seagate’s HAMR approach delivers comparable capacity without shingling compromises. Independent market commentary consistently puts WDC 12 to 18 months behind Seagate in HAMR qualification and volume production.

Toshiba, the third HDD manufacturer with approximately 30 percent of global unit shipments, has not announced a competitive advanced recording technology program with the same near-term commercialization timeline.[10] At 24TB CMR and 28TB SMR capacities — Toshiba’s current nearline flagship products — the cost-per-terabyte disadvantage versus Seagate’s 36–44TB drives in large-scale deployments is substantial. In the segment that matters most for near-term financials — nearline for hyperscale — Seagate and Western Digital have effectively a bilateral supplier relationship with the world’s most important storage buyers.

The Mozaic roadmap extends significantly beyond the current 44TB milestone. Seagate targets qualification samples of its Mozaic 5 platform — aiming for 50 terabytes per drive — in late 2027, with volume production in 2028. The path to 60TB by 2029-2030 and 100TB in the early 2030s relies on pushing areal density toward 10 terabytes per disk, a target management believes HAMR’s underlying physics can support.[11] Each density generation amplifies the same margin dynamics: more storage per unit, same assembly complexity, higher average selling price.

The economics of HAMR compound in one direction: more bytes per dollar of assembly, higher ASP per drive, same cost structure. Seagate is not at the ceiling of this curve — it is still climbing the ramp.

By the Numbers: A Financial Inflection Nobody Forecast

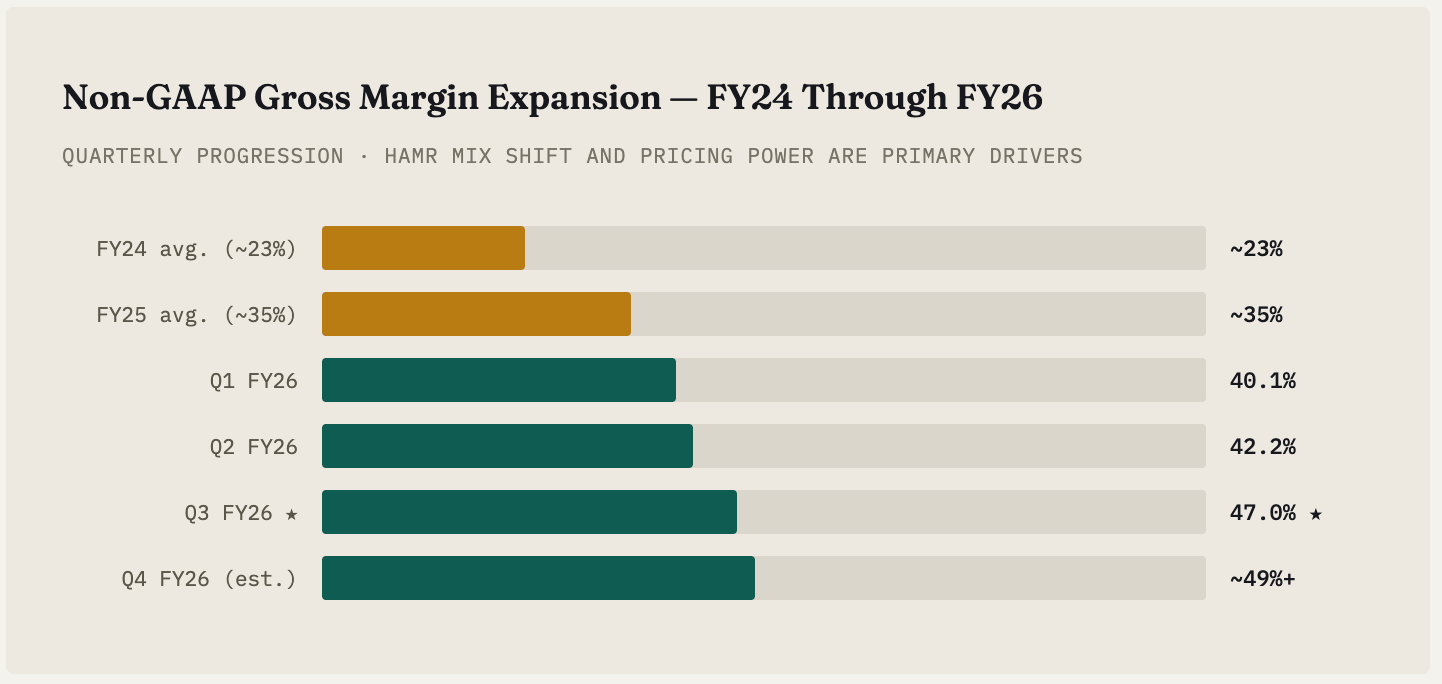

The financial progression at Seagate over the past three fiscal years is unusual in both speed and magnitude. Coming out of the 2022–2023 memory and storage downcycle — during which non-GAAP gross margins troughed at approximately 18–19 percent and the company consumed free cash rather than generating it — the recovery has been steeper and more durable than even management’s own prior forecasts suggested.

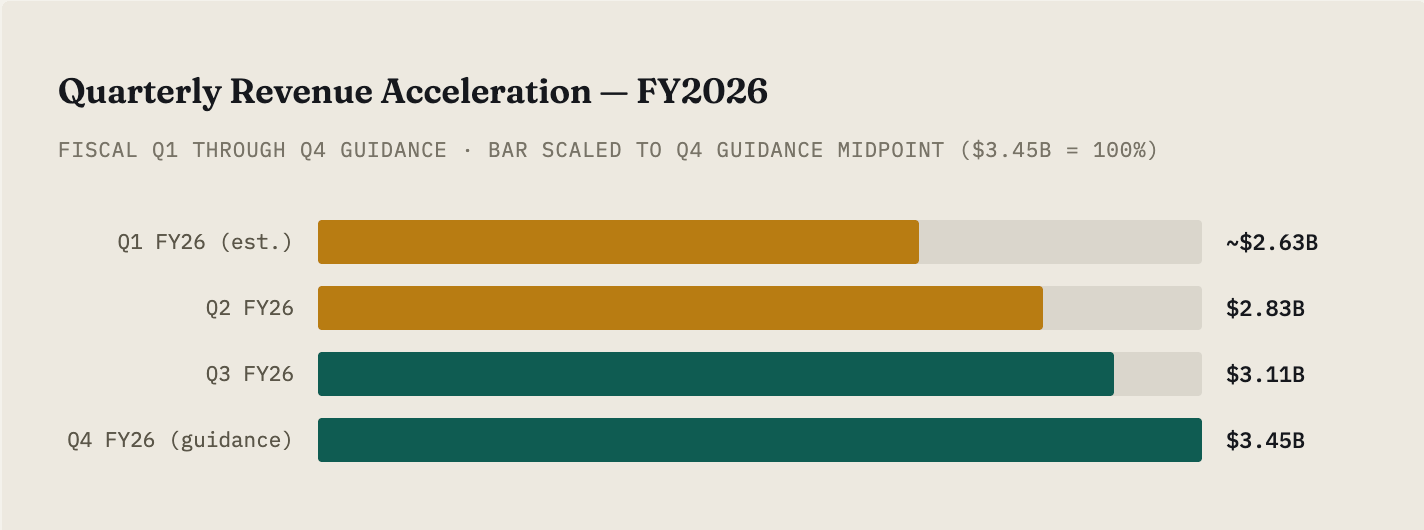

For fiscal year 2025 (ended June 2025), Seagate reported full-year revenue of $9.10 billion, up 39 percent year over year, with non-GAAP diluted EPS of $8.10 and free cash flow of $818 million for the year.[12] For fiscal year 2026, combining three reported quarters with Q4 guidance, the full-year revenue is tracking toward approximately $12.0 billion — another 32 percent year-over-year increase that would represent the most powerful consecutive-year revenue growth in the company’s recent history.

The EPS trajectory is particularly striking. Non-GAAP EPS moved from $2.61 in Q1 FY26 to $3.11 in Q2 to $4.10 in Q3, an increase of 57 percent in two quarters.[13] The Q4 FY26 guidance midpoint of $5.00 implies a run-rate of roughly $20 in annual earnings power — and there is no consensus yet that this represents the cycle peak. The $4.10 Q3 actual exceeded Wall Street’s $3.50 consensus by 17 percent. A company that beat estimates by that margin while generating nearly a billion dollars of free cash flow in a single quarter has not finished surprising the market.