Shopify: A Hundred Billion Dollars. One Quarter. One Platform.

Shopify crossed $100 billion in GMV for the first time in a single quarter — a milestone that places it in the company of the world's largest payment networks. Revenue grew 34% to $3.17 billion.

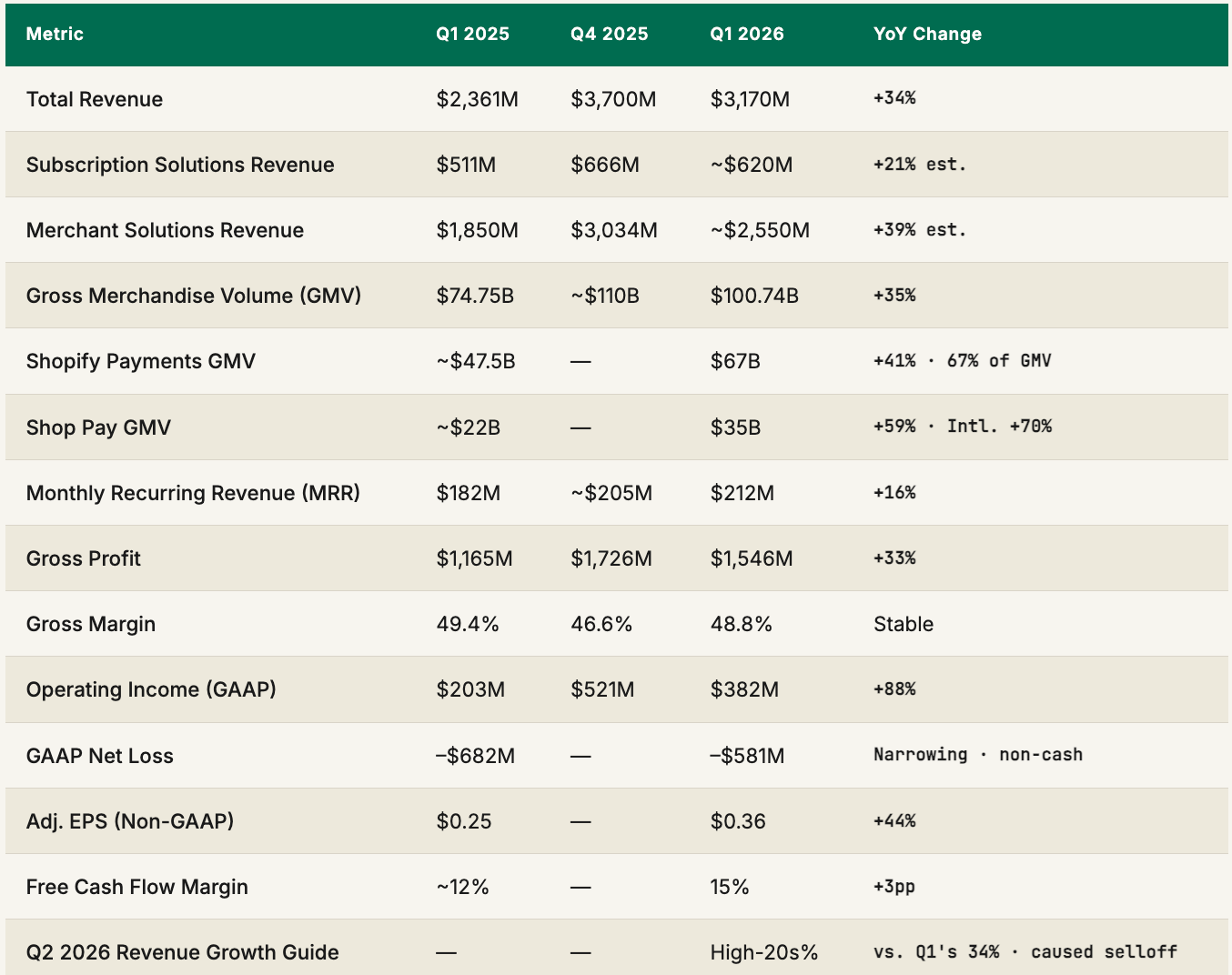

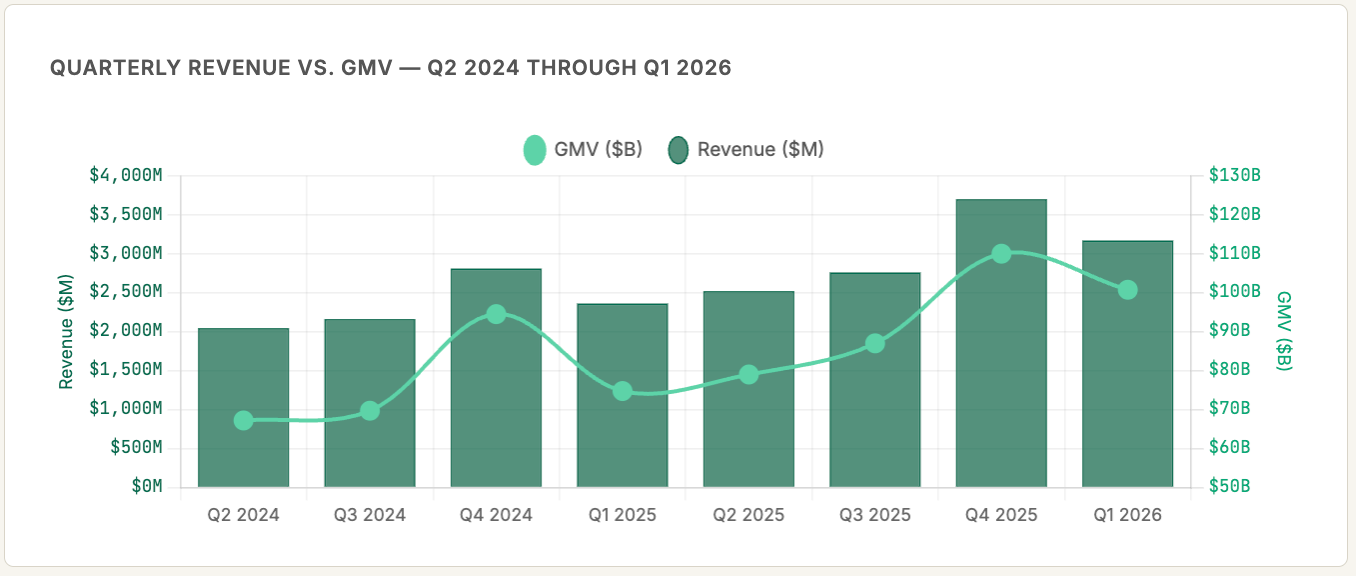

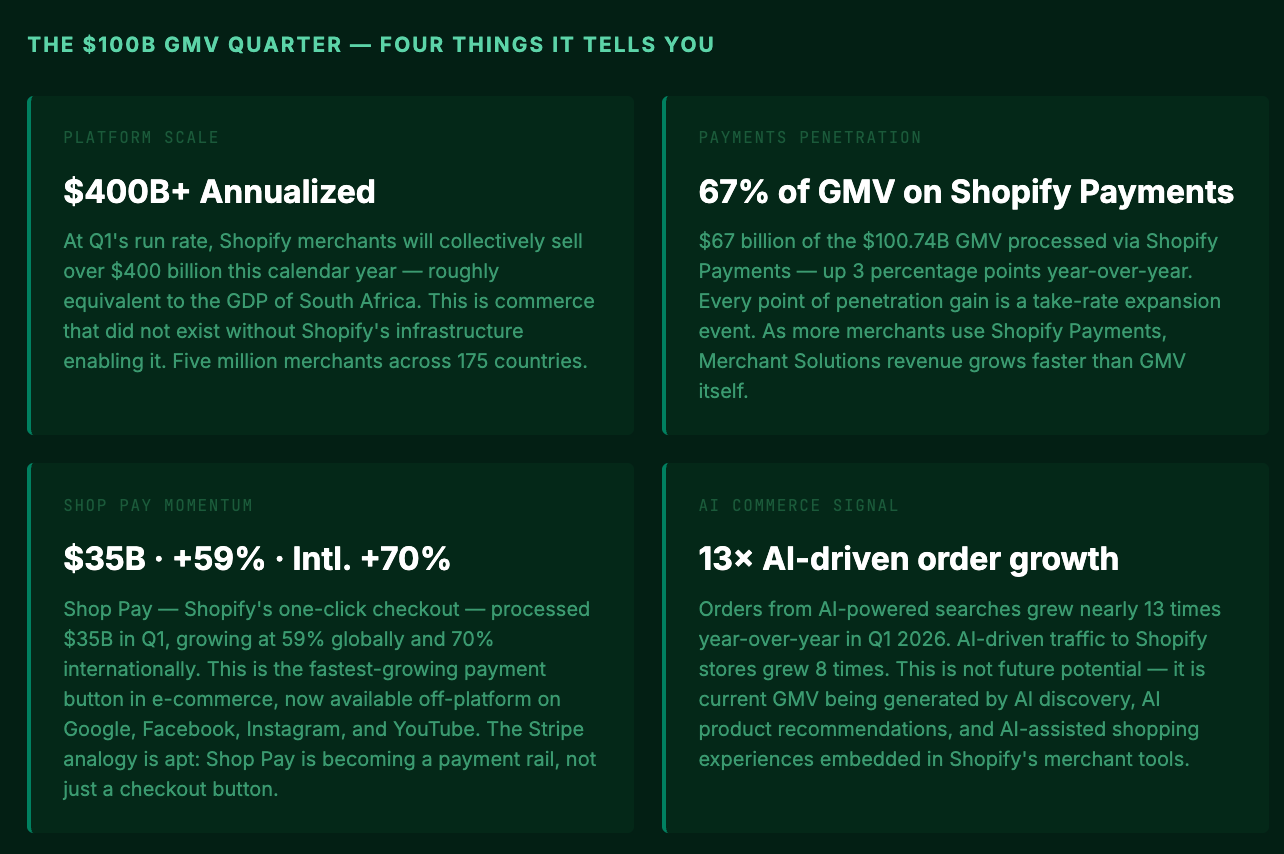

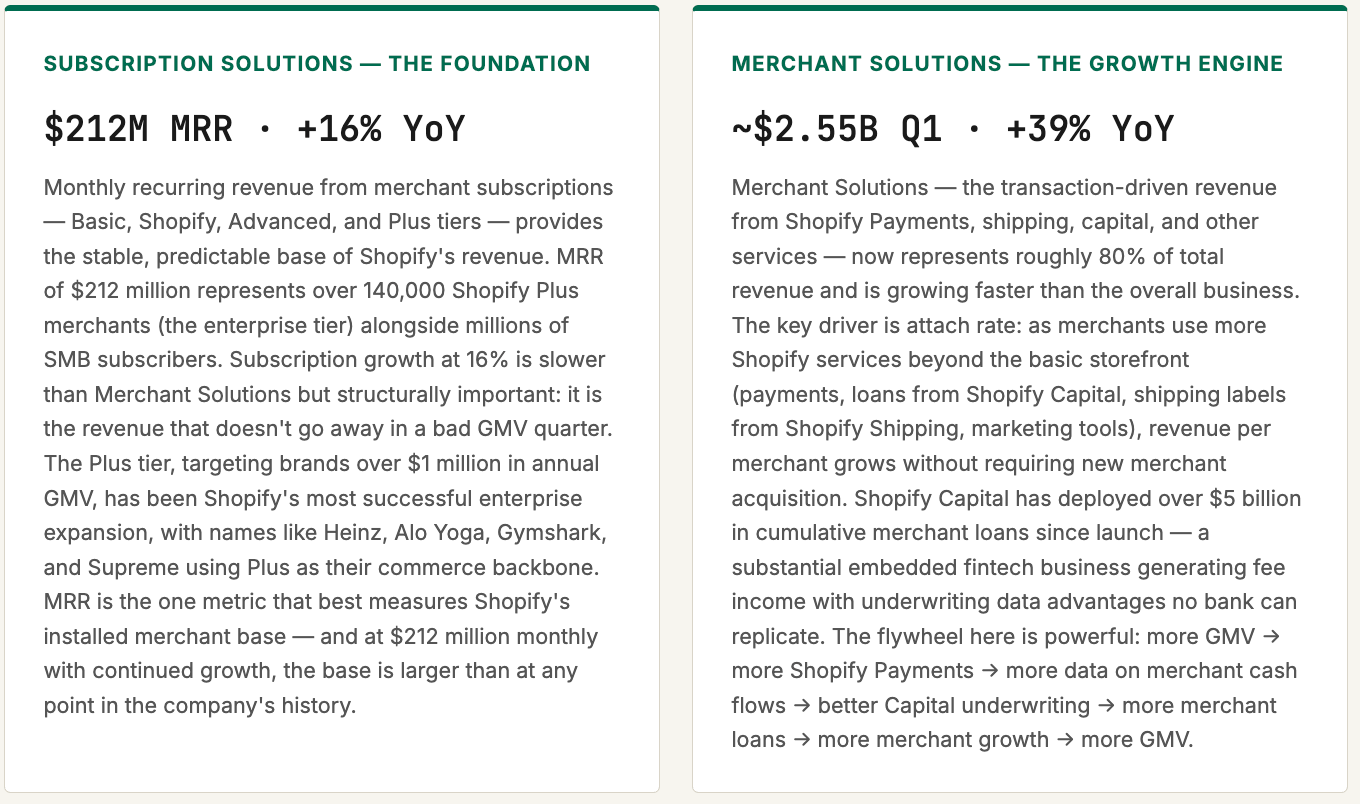

Shopify reported Q1 2026 revenue of $3.17 billion, up 34% year-over-year, beating the $3.09 billion consensus estimate. Gross merchandise volume — the total value of commerce processed through Shopify’s platform — reached $100.74 billion, up 35%, crossing the $100 billion quarterly threshold for the first time in the company’s history. Merchant solutions revenue grew 39%, driven by Shopify Payments processing $67 billion in GMV (67% of total) and Shop Pay hitting $35 billion at 59% growth. Adjusted EPS came in at $0.36 against a $0.24 consensus. Free cash flow margin hit 15%. The GAAP net loss of $581 million is entirely attributable to non-cash investment valuation adjustments and is not reflective of operating performance.

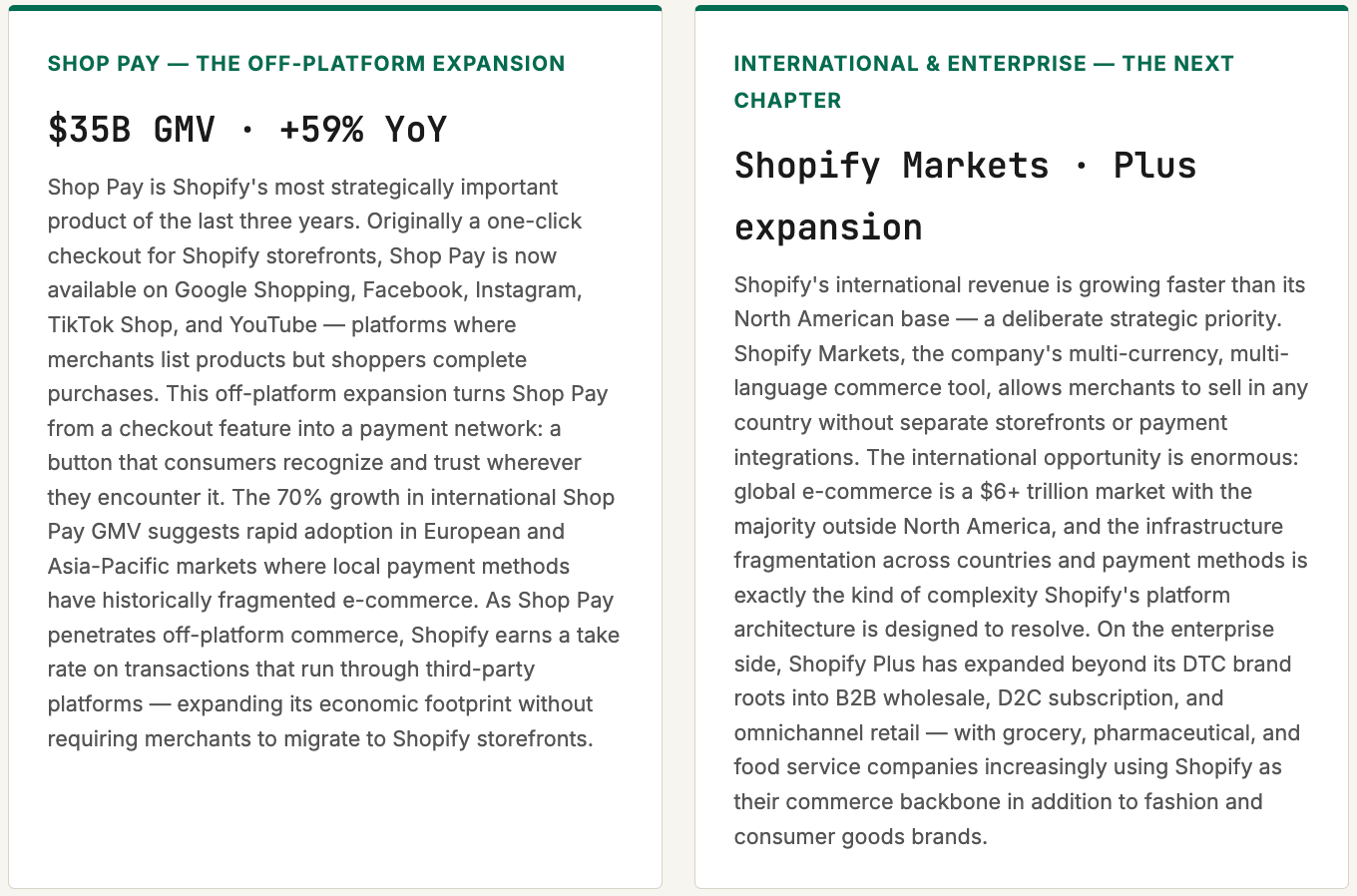

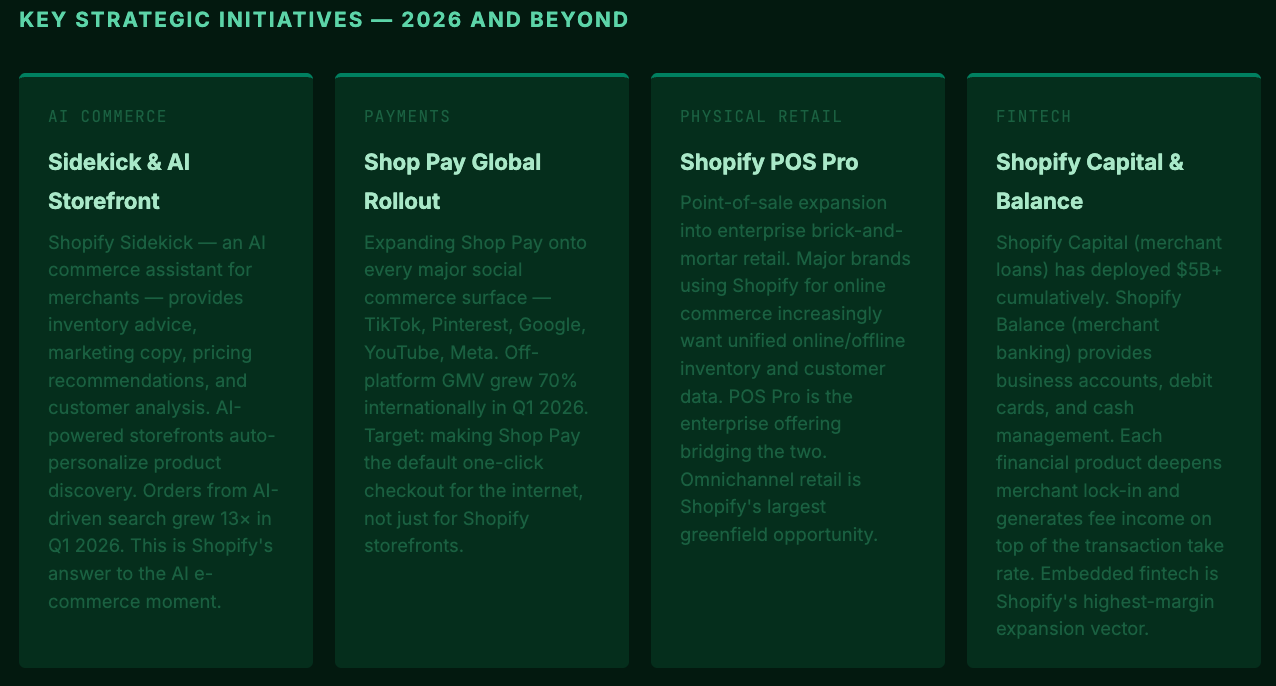

The revenue beat was unambiguous. The reaction was negative anyway, because Q2 2026 guidance of “high-twenties percent” revenue growth implies a deceleration from Q1’s 34% pace — and the market, conditioned to Shopify’s above-expectation performance, is sensitive to any signal of slowdown. The deceleration reflects a combination of tougher year-over-year comparisons, macro uncertainty from U.S.-China tariff escalation affecting cross-border merchants, and the natural base effect of a platform that now processes over $400 billion in annualized GMV. Underneath the guide, the operating data — AI-driven orders up 13 times, Shop Pay international up 70%, merchant solutions growing 39% — points to a business still firing on every cylinder. The tension between the operating reality and the guidance math is the entire Shopify investment debate in May 2026.

01

Tobi’s Original Idea — The Merchant First, Always

Shopify’s origin story is one of the most purely accidental in technology. In 2004, Tobias Lütke — a German-born software engineer who had moved to Ottawa to be with his girlfriend, later wife, Fiona McKean — wanted to sell snowboards online. He looked at the available e-commerce software and found it uniformly terrible: expensive, inflexible, designed for the vendor rather than the seller, and almost impossible to customize without deep technical knowledge. So he built his own. The snowboard company, Snowdevil, was a modest business. The software underneath it was remarkable — clean, fast, extensible, and built around the premise that the merchant’s needs were paramount. His friends started asking if they could use the software for their own businesses. In 2006, Lütke and his co-founders launched Shopify as a product. By 2015, it had gone public on the New York Stock Exchange at $17 per share.

The core insight that has compounded through twenty years of Shopify’s development is deceptively simple: e-commerce infrastructure is a platform business, not a product business. Rather than building the best storefront or the best shopping cart, Shopify built the best system for anyone else to build their own best storefront and shopping cart — and then collected a slice of every transaction that ran through it. This platform model creates network effects that are invisible until they become overwhelming. Every merchant on Shopify contributes data on what sells, when, to whom, and at what price point. That data improves Shopify’s AI recommendations, its fraud detection, its inventory management tools, and its marketing products. The more merchants join, the better the platform gets. The better the platform gets, the more merchants join. By 2026, more than five million merchants in 175 countries sell through Shopify — from solo entrepreneurs selling handmade ceramics on Etsy-alternative storefronts to enterprise brands like Alo Yoga, Gymshark, Allbirds, and Heinz.

Lütke has spent the last three years positioning Shopify explicitly as an AI company. His January 2025 internal memo — widely quoted after it leaked — told Shopify employees that before requesting new headcount, teams must demonstrate that AI cannot do the job. “Reflexive AI usage” and “AI as a first responder to problems” have become organizational mandates. In Q1 2026, AI-driven traffic to Shopify stores grew eight times year-over-year. Orders from AI-powered searches grew thirteen times. These are not marketing claims about AI integration — they are GMV-generating events that show up directly in the company’s financial results.

02

Q1 2026 by the Numbers

A note on the GAAP net loss: Shopify holds equity stakes in several companies through its investment portfolio, including Affirm, Global-E Online, and other fintech and e-commerce businesses. These positions are marked to market every quarter. When those equity values decline — even temporarily — the accounting loss flows through to GAAP net income and produces the headline losses that dominate news coverage. The $581 million GAAP loss in Q1 2026 bears no relationship to Shopify’s operating performance: operating income was $382 million, and free cash flow margin was 15%. Investors who track GAAP net income as Shopify’s primary profitability metric are reading the wrong number.

03

The $100 Billion Quarter — What That Number Actually Means

The $100 billion GMV milestone is not a vanity metric. It positions Shopify alongside the world’s largest payment processing networks in terms of commerce facilitated. For reference: Visa processes approximately $3.8 trillion in payment volume annually, or roughly $950 billion per quarter. Shopify at $100 billion per quarter represents about 10% of Visa’s volume — but Shopify is not a payment network. It is the infrastructure on which that commerce is built, managed, and shipped. The GMV figure captures every transaction that runs through a Shopify-powered storefront, regardless of whether Shopify Payments processed the underlying payment. It is the best single measure of Shopify’s economic footprint in global commerce.

04

Four Revenue Streams, One Commerce Operating System

05

Product Pipeline — AI, Offline Commerce, and the Global Checkout

06