Snowflake: The CoCo Inflection — When One Product Changes Everything

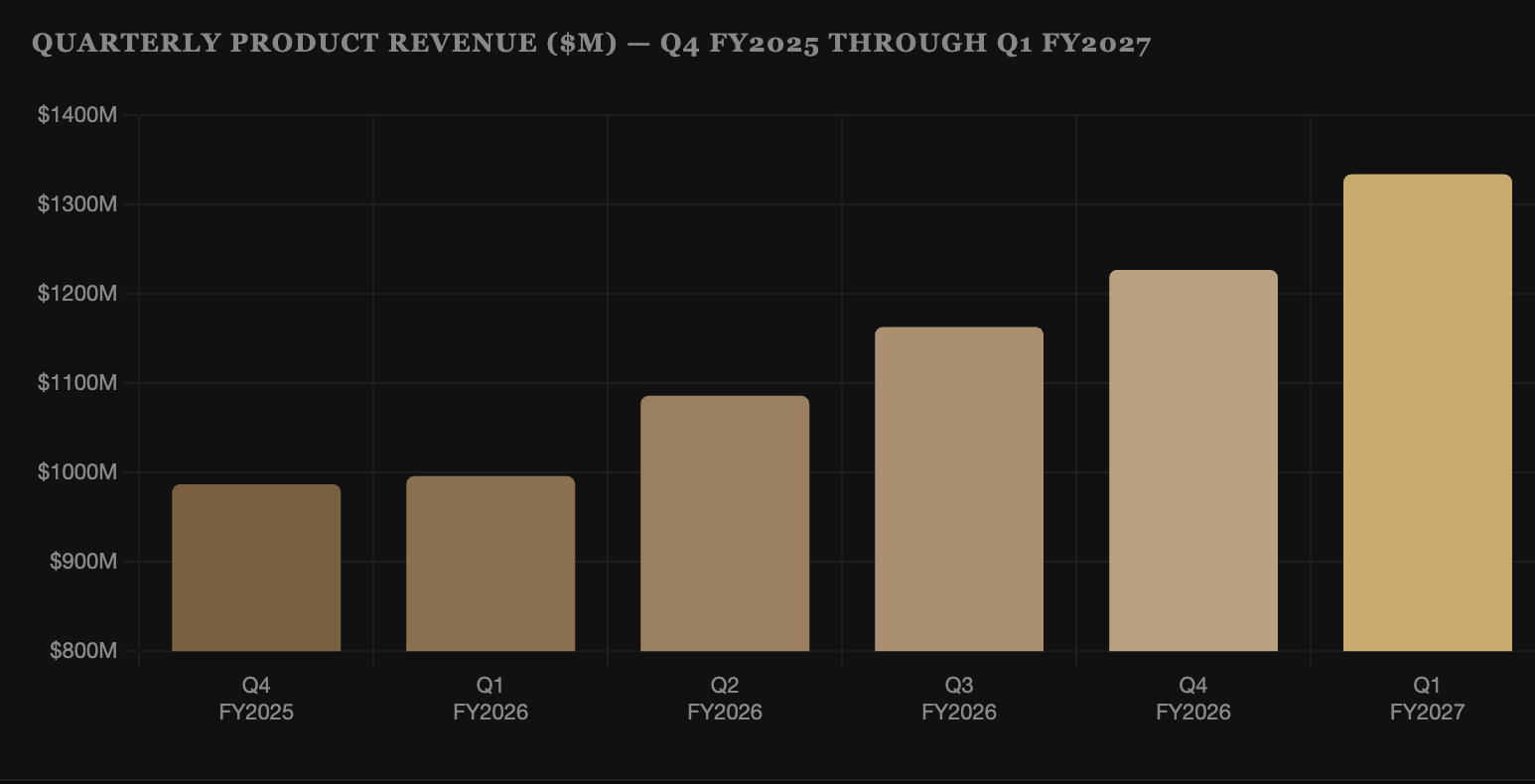

Snowflake’s fiscal first quarter of FY2027, covering the three months ended April 30, 2026, delivered one of the most decisive inflection prints in the company’s public history. Product revenue reached $1.334 billion, up 34% year over year — an acceleration from 30% in Q4 FY2026 and 20% in Q1 FY2026 one year prior. The beat against the company’s own guidance of $1.262 to $1.267 billion was $69 million, equivalent to roughly one-third of a standard quarterly beat from a company this size. That is not a rounding error. That is a product story.

The product is Cortex Code — CoCo in Snowflake’s internal shorthand — a code generation and AI developer assistant that went generally available on February 5, 2026, the literal first day of the quarter. CFO Mike Scarpelli was unusually direct on the earnings call: “CoCo had the largest driver to the increase in our forecast.” In a company that almost never singles out individual products as demand drivers, that statement demands analysis. We provide it in Section 5.

Equally notable is the sequential dollar growth in product revenue: from $1.227 billion in Q4 FY2026 to $1.334 billion in Q1 FY2027 — a $107 million sequential increase. Snowflake stated this was the strongest sequential dollar growth in company history, a remarkable achievement given that Q1 is historically a seasonally softer quarter as enterprises reset annual IT budgets. The fact that the strongest sequential dollar gain in Snowflake’s history arrived in a Q1, against a seasonal headwind, underscores the degree to which organic AI demand is reshaping the consumption curve.

Net new customer additions of 616 grew 38% year over year — matching the RPO growth rate almost exactly and suggesting the new logo engine is firing at a pace that will matter for revenue in FY2028. Among those new additions: 13 Global 2000 customers, versus just 4 in the prior year quarter. That 3x increase in premium enterprise logo acquisition is the clearest evidence that Snowflake’s go-to-market is not merely benefiting from existing customer expansion — it is also breaking through in new enterprise accounts at an accelerating rate. Net Revenue Retention rebounded to 126%, reversing a prolonged compression trend and providing the first data point suggesting that AI-driven consumption is genuinely improving the expansion behavior of the installed base.

Section 02

The Consumption Model Explained — Why This Quarter’s Beat Is Different

To understand why the Q1 FY2027 beat is structurally significant rather than merely cosmetically impressive, you must understand what it means to beat guidance inside a consumption model. Snowflake does not recognize revenue when contracts are signed. Revenue flows when customers actually use compute credits — when they run queries, execute pipelines, call AI functions, generate code suggestions, or perform inference operations. Guidance is therefore a forward estimate of usage behavior, not of contract signings. Beating guidance in a consumption model means customers consumed more than Snowflake expected them to.

This is harder to manufacture than a traditional SaaS beat. In subscription SaaS, guidance upside can come from deals closing earlier in the quarter than expected, pushing committed revenue into the current period. In Snowflake’s model, there is no such mechanism. The $69 million beat above the high end of guidance reflects one thing: enterprise customers ran significantly more compute workloads inside Snowflake than historical patterns predicted. CoCo drove secondary consumption of the core platform — every code suggestion called, every code generation query executed, every developer workflow orchestrated through Cortex Code generated incremental credit consumption that management had not fully anticipated when they issued Q1 guidance in March.

This creates a compounding dynamic that is genuinely new for Snowflake. Previous AI features — Cortex functions, Cortex Search, Cortex Analyst — added workloads incrementally. CoCo appears to have triggered a step-change in developer engagement with the platform, and developer workloads tend to be stickier than analytics workloads: they get embedded into build pipelines, CI/CD workflows, and daily developer routines in ways that are extremely difficult to dislodge. A developer team that has routed its code generation through CoCo for 90 days has built a workflow dependency that survives most budget review conversations.

“CoCo had the largest driver to the increase in our forecast.”

— Mike Scarpelli, Snowflake CFO, Q1 FY2027 earnings call, May 27, 2026

The RPO growth rate of 38% year over year — accelerating from 34% in Q1 FY2026 — corroborates the consumption story from the contract side. Enterprises are not just using more Snowflake today; they are committing to materially higher spend over the next one to three years. That combination — consumption beating guidance and RPO growth accelerating simultaneously — is the strongest possible configuration of forward signals in Snowflake’s reporting structure. It suggests the demand impulse is not a one-quarter event.

The second-order implication is for guidance credibility. Snowflake’s Q2 FY2027 guidance of $1.415 to $1.420 billion implies approximately 30% year-over-year growth. Given that Q1 actual results arrived 34% higher than Q1 FY2026, the 30% guidance for Q2 looks conservative by historical norms — particularly if CoCo, which is now in over 7,100 accounts after just one quarter of GA, continues to scale. The full-year raise from $5.66 billion to $5.84 billion — a $180 million increase — represents guidance issued in the early days of a new product adoption curve. The question for investors is not whether FY2027 guidance will be met. It is whether the beat-and-raise cadence has structurally reset to a new level.

Section 03

Product Revenue Trajectory — Reaccelerating Off a Larger Base

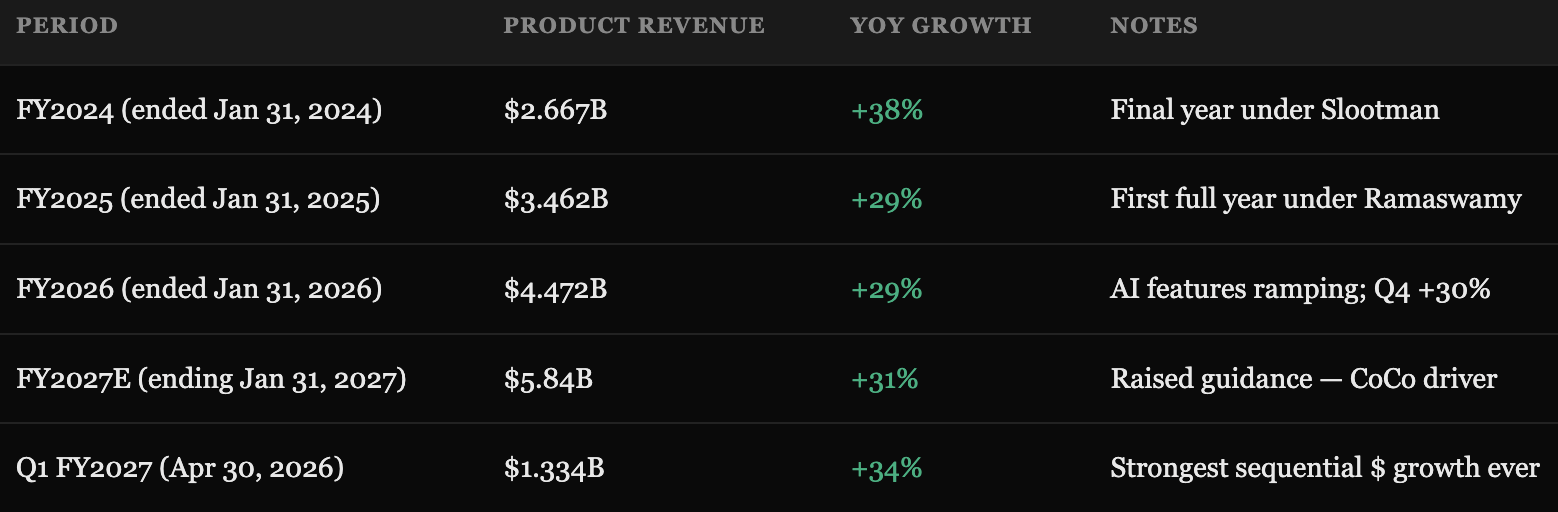

The table above requires careful reading, because the pattern it reveals is counterintuitive. Enterprise software at scale almost universally decelerates as the law of large numbers takes hold. Snowflake at $4.472 billion in FY2026 product revenue is not a small company; it is one of the largest standalone pure-play data infrastructure businesses in the world. The expectation embedded in most financial models entering 2026 was that 29% growth would gradually settle toward 24-25% as the platform matured and competitive pressure intensified. Instead, Q1 FY2027 delivered 34% growth — the highest rate since Q3 FY2025 — and full-year guidance implies 31% for FY2027 in aggregate.

Reacceleration at scale is exceedingly rare. The short list of enterprise software companies that have managed it includes Salesforce in the early CRM buildout, ServiceNow during its workflow platform expansion, and more recently Palantir as government AI adoption accelerated. In each case, the reacceleration was driven by a new workload category that attached to an existing installed base rather than requiring net new customer acquisition. CoCo fits precisely this template: it is a new product running inside accounts that already have Snowflake data infrastructure, converting developers who were previously passive Snowflake users into active credit consumers.

The FY2027 guidance raise to $5.84 billion is itself notable for what it implies about the cadence of the year. If Q1 came in at $1.334 billion and Q2 is guided at $1.415 to $1.420 billion, then H2 FY2027 is implicitly guided at approximately $3.09 billion — a pace that requires modest sequential growth as the year progresses. Given the historical pattern of Snowflake’s guidance conservatism and the early stage of CoCo adoption, H2 estimates appear beatable. The operating margin raise — from 12.5% to 13.5% for the full year — provides further evidence that management is gaining confidence in the revenue trajectory: you do not raise margin guidance alongside revenue guidance unless you believe the revenue will arrive.

For historical context: FY2024 growth of 38% was achieved on a base of roughly $1.93 billion. The 34% growth in Q1 FY2027 was achieved on a base of $996 million for Q1 FY2026 — roughly half as large. The absolute dollar growth in Q1 FY2027 ($338 million year over year) is vastly larger than the FY2024 era. Snowflake is adding more revenue per quarter in absolute terms than it was during its highest growth-rate periods. This is the math of compounding operating at scale, and it matters for long-duration capital allocation decisions.

Section 04