SpaceX Files for the Largest IPO in History: What the S-1 Really Reveals

On May 20, 2026, Elon Musk's Space Exploration Technologies Corp. made public the S-1 registration statement that the investment world has awaited for two decades.

01 — Executive Summary

The Document Two Decades in the Making

SpaceX’s S-1, made public on the evening of May 20, 2026, is not merely a financial filing. It is a strategic manifesto disguised as a prospectus — a document that demands investors decide whether they believe in the commercial colonization of the solar system, and what that belief is worth in present-day dollars.

When Elon Musk founded Space Exploration Technologies Corp. in 2002, he publicly stated the goal was to make life multiplanetary. Few outside his inner circle took the Mars aspiration literally. Twenty-four years later, the S-1 submitted to the SEC under ticker symbol SPCX contains language confirming that the Mars mission is not rhetorical decoration — it is embedded in the company’s stated total addressable market, which the filing pegs at $28.5 trillion. This framing is deliberate and important: it tells investors they are not buying a rocket company, they are buying a civilization-infrastructure platform at the earliest stage of its trajectory.

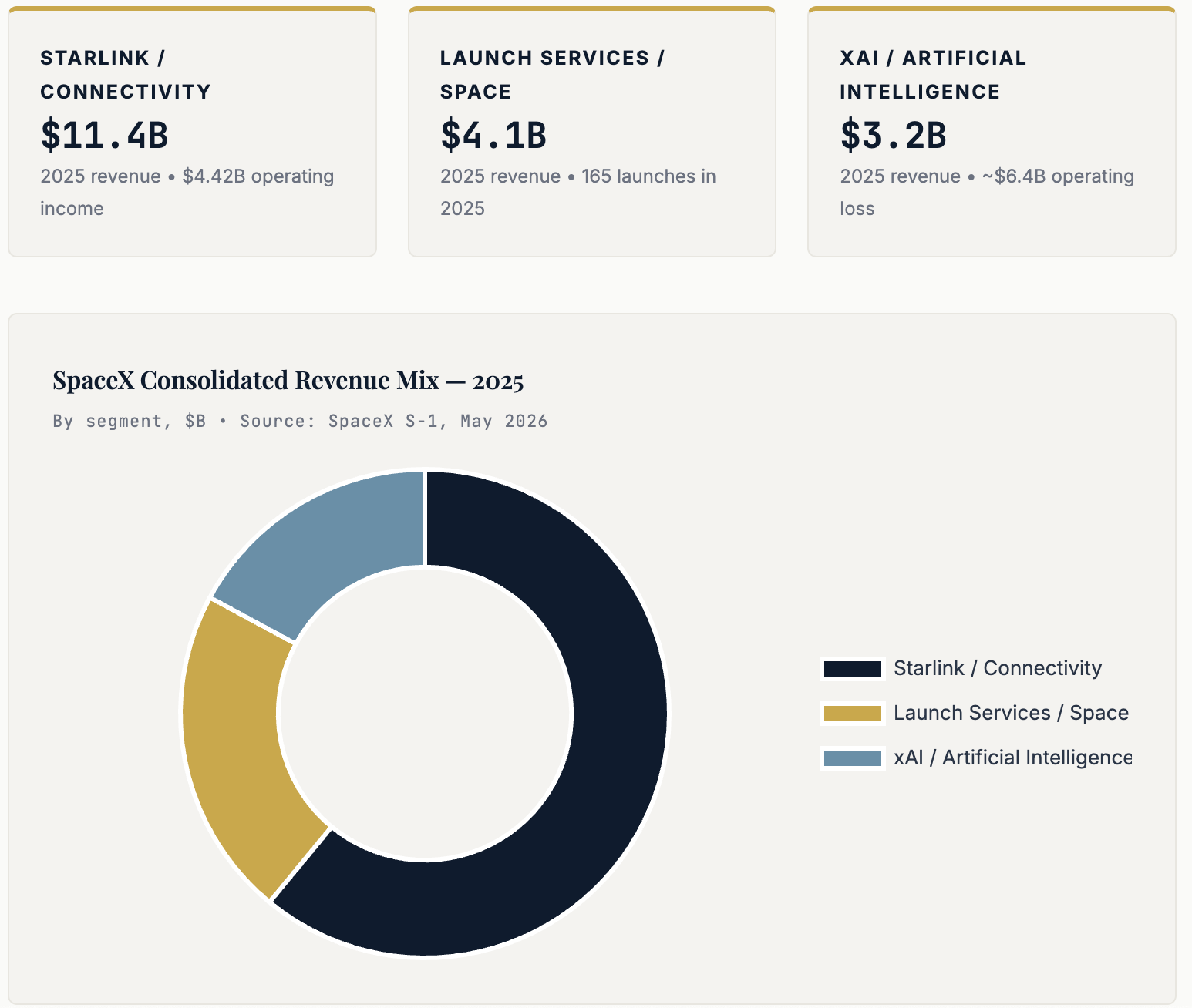

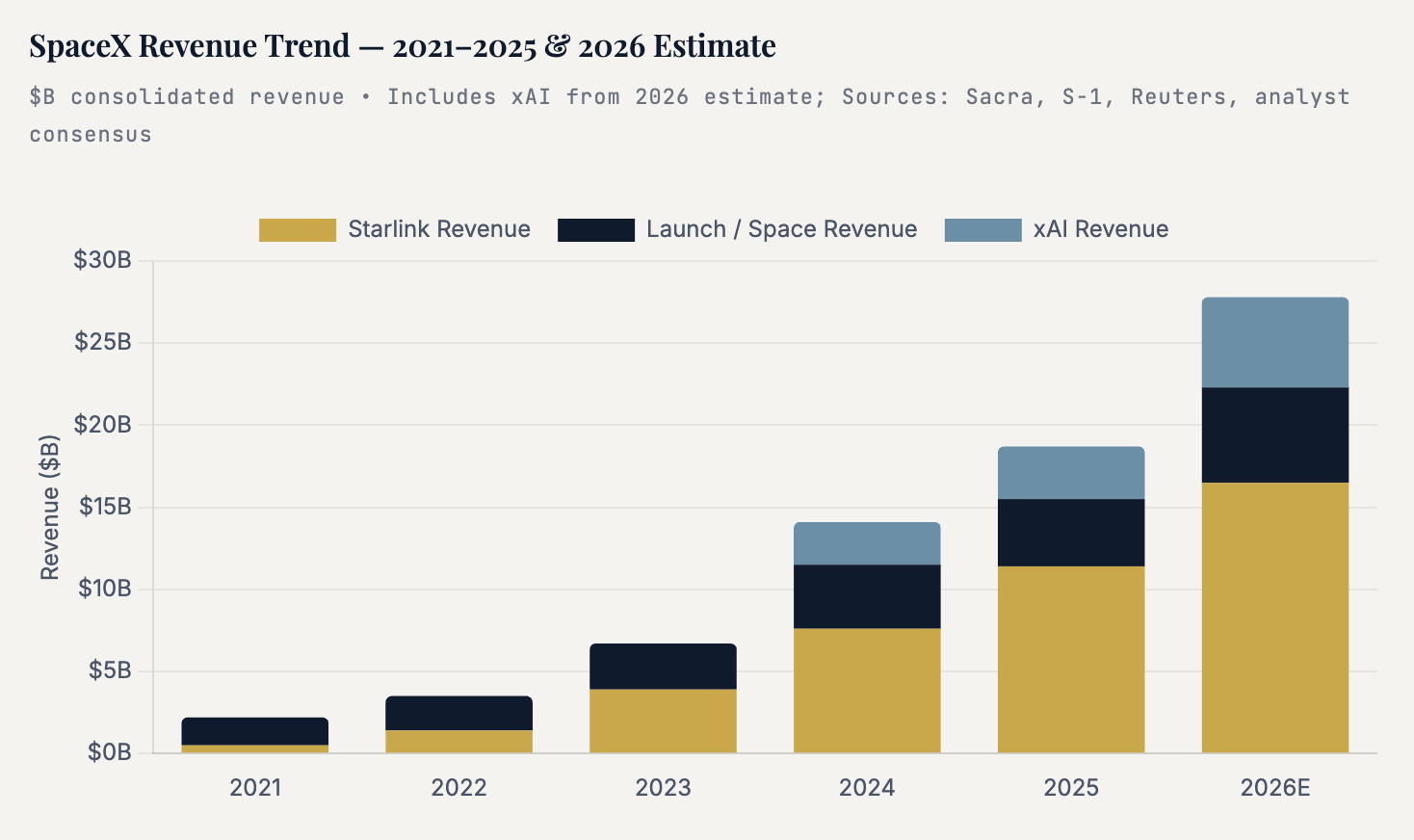

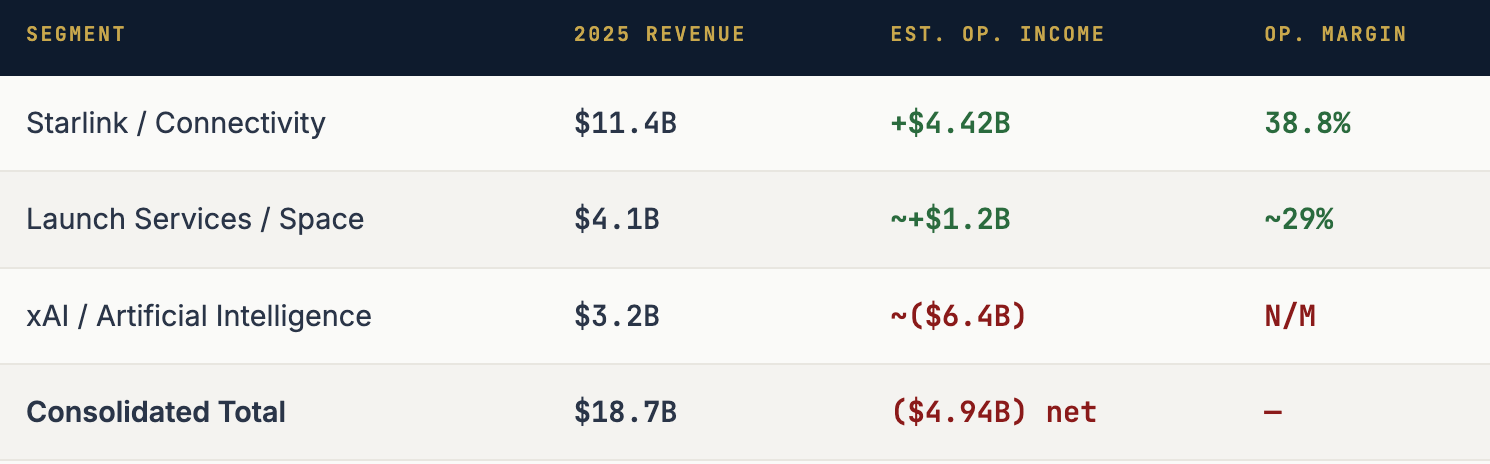

The headline numbers are remarkable for a company that has never traded publicly. Consolidated 2025 revenue reached $18.67 billion, up 33% from $14.1 billion in 2024. Starlink — the satellite internet constellation that SpaceX bootstrapped from its own launch profits — contributed $11.4 billion of that total, generating $4.42 billion in segment operating income in a single year. The launch services business added approximately $4.1 billion. The company’s S-1 also consolidates xAI, Musk’s artificial intelligence venture merged into SpaceX in February 2026, which contributed $3.2 billion in revenue but generated approximately $6.4 billion in operating losses — producing the consolidated net loss of $4.94 billion that would otherwise be a strong profit without the AI division. On a cash basis, xAI spent an additional roughly $14 billion in capital expenditures on data center buildout, representing a separate but equally significant drain on consolidated cash flows.

On the governance side, the S-1 confirms what private market investors have long understood: this is Elon Musk’s company. His Class B shares carry 10 votes per share, giving him approximately 85% of voting power despite holding about 42% of economic equity. Public investors buying into the IPO acquire an economic participation in one of the most extraordinary businesses ever built — but essentially zero ability to influence its direction. That dynamic, unusual but not unprecedented among tech founders (Meta, Alphabet, Snap all used similar structures), will be the defining governance reality for SPCX shareholders for as long as Musk remains at the helm.

The IPO is expected to raise up to $75 billion, more than double Saudi Aramco’s $29 billion record set in 2019 and nearly three times the prior technology IPO record. Morgan Stanley, Bank of America, Citigroup, JPMorgan, and Goldman Sachs are leading an underwriting syndicate of 21 banks. SpaceX has targeted a roadshow launch around June 4, pricing on June 11, and a first day of trading on the Nasdaq on June 12, 2026. What follows in these pages is our attempt to read every layer of this document — the businesses behind the numbers, the risks the boilerplate obscures, the valuation logic, and the civilizational bet at the core of it all.

02 — The Business

What SpaceX Actually Does: Three Revenue Engines

SpaceX is not one business. It is three distinct businesses operating at very different stages of maturity, with radically different economics and growth trajectories — all under one corporate roof and one controlling shareholder. The S-1 breaks these into three reportable segments: Space (launch services), Connectivity (Starlink), and AI (xAI). Understanding them separately is essential to any honest valuation exercise.

Launch Services: The Foundation

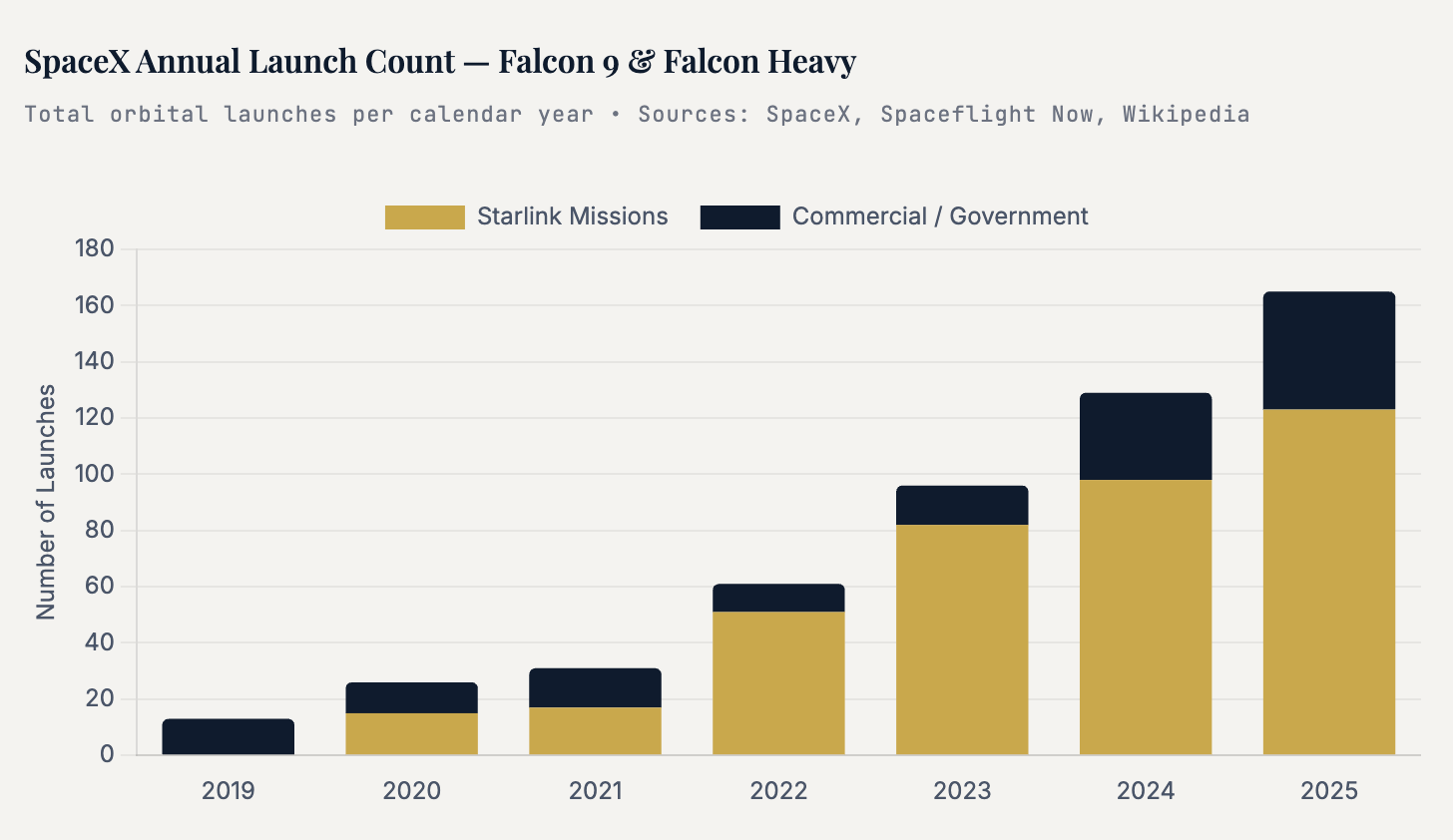

SpaceX’s launch business is the original engine that made everything else possible. Without the reliable, reusable Falcon 9 generating consistent cash flow, Starlink could never have been funded. In 2025, SpaceX conducted 165 Falcon family launches — roughly one every 2.2 days — at a pace no rocket company in history has approached. Of those, 123 were Starlink missions, with the remaining 42 serving commercial, government, and institutional customers at list prices ranging from $74 million to over $150 million for Falcon Heavy.

The economics of the launch business are driven by reusability in a way that no financial model from 2010 could have predicted. SpaceX has demonstrated Falcon 9 booster recovery and reuse through over 34 flights on a single core (booster B1067 set the record on March 31, 2026). Refurbishment between flights costs roughly $250,000 on the booster alone versus tens of millions to manufacture a new one. This creates a deepening cost advantage with every flight cycle: the more a booster flies, the cheaper each launch becomes. At a list price of approximately $74 million per flight and an estimated marginal cost of under $28 million for mature refurbished boosters, the launch business runs gross margins that rival software companies — and those margins expand as cadence increases.

Starlink: The Compounding Machine

Starlink is the business that transformed SpaceX from a remarkable aerospace company into a potential multi-trillion-dollar enterprise. A global satellite internet constellation generating subscription revenue at scale represents a fundamentally different business model than selling rocket rides — it is recurring, geographically unconfined, and improves with density as latency and throughput increase when more satellites fill the orbital shell.

xAI: The Complicating Factor

The February 2026 merger of xAI into SpaceX is perhaps the most analytically vexing element of this S-1. xAI contributed $3.2 billion in revenue while posting approximately $6.4 billion in operating losses, burning cash at a pace that consumed the entirety of Starlink’s profitability and pushed the consolidated entity to a net loss. The strategic rationale — orbital AI data centers powered by Starship, Grok integrated into Starlink terminals — is imaginative. The financial reality is that investors must decide whether the xAI attachment is a synergistic amplifier or a combination of $6.4 billion in annual operating losses and $14 billion in capital expenditures that obscures the underlying SpaceX profitability story.

03 — Starlink

The Crown Jewel: A Global ISP in Low Earth Orbit

No other company in the world has built a global internet provider from scratch using its own launch vehicles. Starlink is, at its core, a vertically integrated telecommunications infrastructure business that happens to be operated from space — and the economics of that integration are unlike anything in the history of the internet.

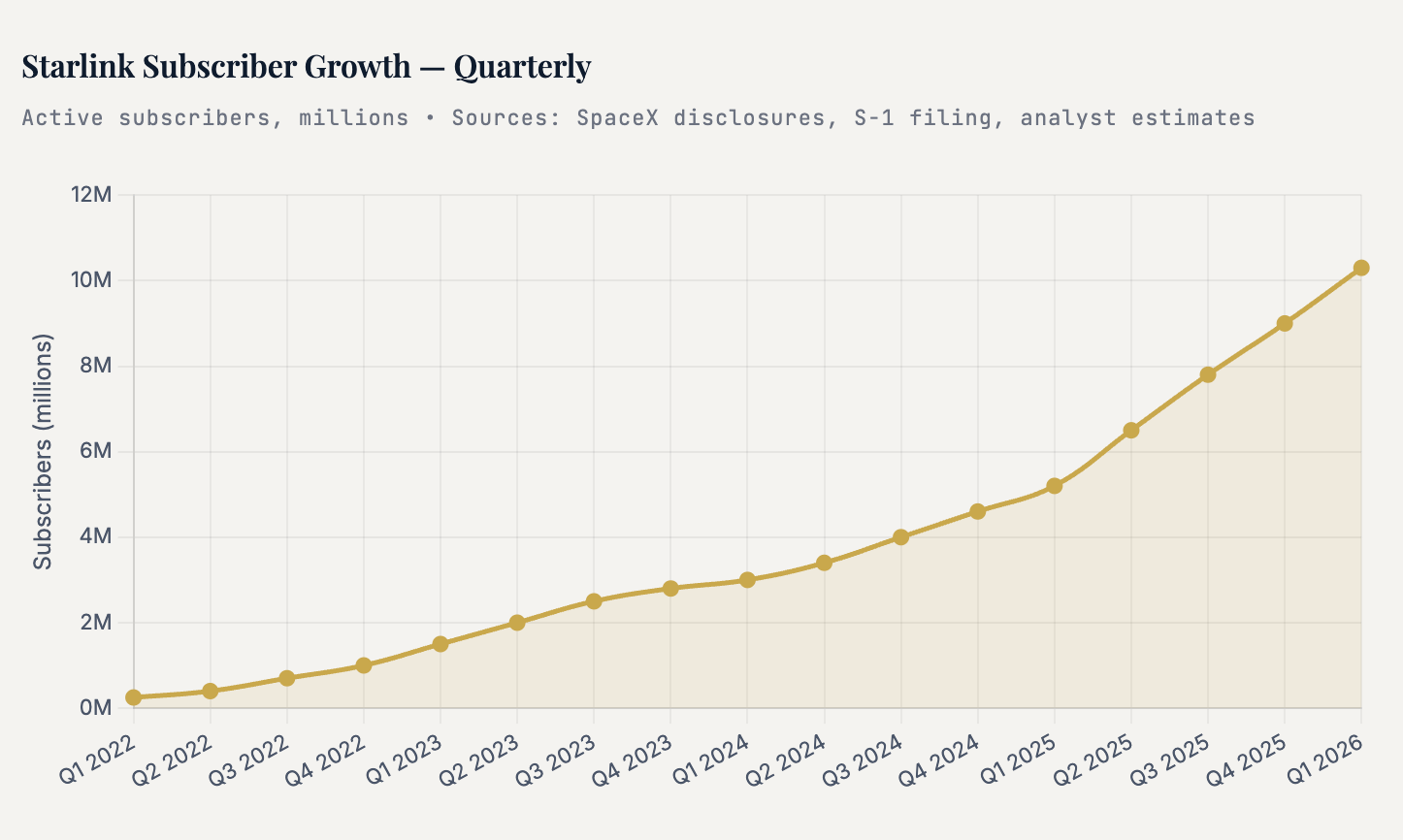

As of March 31, 2026, Starlink had 10.3 million active subscribers across 164 countries and territories, supported by approximately 10,300 satellites in low Earth orbit — the largest constellation in history by a factor of more than three. The growth trajectory has been extraordinary: SpaceX added approximately 4.4 million net new customers in 2025 alone, nearly doubling the subscriber base from roughly 4.6 million at year-start to approximately 9 million at year-end. By early 2026, the service was crossing the 10 million threshold, a milestone that anchors the subscription revenue base at a level that makes Starlink one of the larger ISPs in the world by subscriber count, behind only the largest wireline and mobile providers in major individual markets.

ARPU: The Trade-Off SpaceX Made

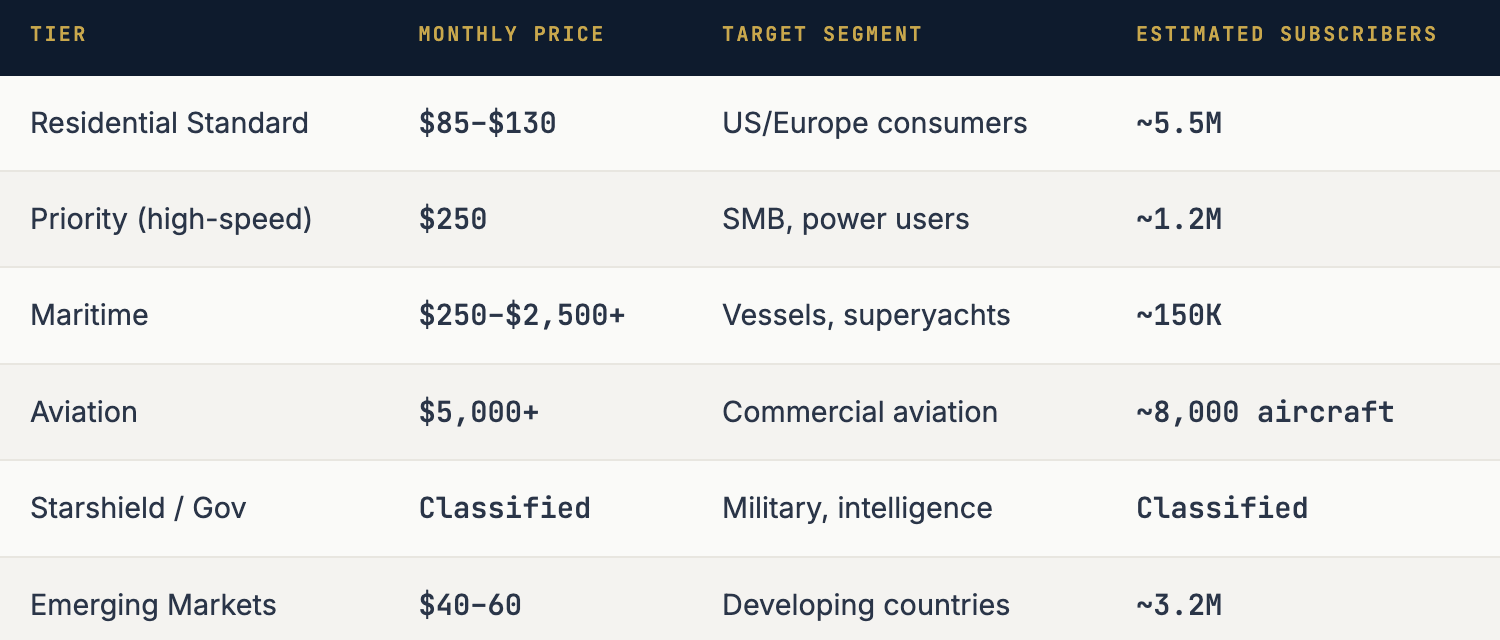

The S-1 reveals a significant ARPU compression story that demands attention. Average revenue per subscriber has fallen approximately 18% from 2023 to 2025, declining from around $99 per month globally to approximately $81 per month worldwide. The blended global ARPU implied by the S-1 financials works out to approximately $92 per month ($11.4B annual revenue divided across 10.3M subscribers), which is higher than the individual subscriber average because the mix includes high-ARPU maritime, aviation, enterprise, and government tiers alongside lower-priced residential and emerging market plans. The declining trend reflects the deliberate international expansion strategy of offering lower price points in emerging markets — India, Brazil, Indonesia, sub-Saharan Africa — in exchange for volume, a trade SpaceX has explicitly embraced.

The ARPU picture is more nuanced than the headline average suggests. SpaceX operates multiple pricing tiers that reflect the underlying economics of different customer segments:

The math that drives the revenue line is straightforward in structure but complex in implication. The $11.4 billion in 2025 Starlink revenue across 10.3 million subscribers implies a blended ARPU of approximately $92 per month — a figure that is boosted by high-value maritime, aviation, enterprise, and government accounts on top of the residential subscriber base. The critical question is what happens at 30 million subscribers — a figure several sell-side models place SpaceX at by 2028 — where the economics of a near-fixed-cost satellite constellation generate enormous incremental margins on each additional subscriber.

Profitability: Starlink Already Turned the Corner

The S-1 confirms that the Starlink segment itself is profitable, generating $4.42 billion in operating income in 2025 — a roughly 39% segment operating margin. This is a watershed number. In 2021, Starlink was burning hundreds of millions of dollars annually on constellation buildout. By 2023, it had reached breakeven at the operating level. By 2025, it was generating nearly $4.5 billion in operating income — enough to fund the entire SpaceX launch business, most of the Starship development program, and still leave substantial cash flow.

“Starlink generated $4.42 billion of operating income in 2025 — a ~39% segment operating margin. This is what a subscription business looks like when the infrastructure is already in orbit and every new subscriber is nearly pure margin at the increment.”

LongYield Research Desk, SpaceX S-1 Analysis

Competitive Landscape: Is Starlink’s Moat Real?

The most important competitive question for Starlink is not who can match it today — no one can — but who might credibly challenge it in five years. Amazon’s Project Kuiper completed its first batch of constellation satellites in late 2025 and is expected to begin consumer service in 2026. OneWeb (now part of Eutelsat) operates a smaller LEO constellation but serves primarily enterprise and government. Traditional ISPs are largely irrelevant in Starlink’s core underserved rural market; in urban areas, fiber and 5G pose genuine substitution risk.

The Kuiper threat deserves the most analytical weight. Amazon has committed billions to the program, has its own launch infrastructure relationships (ULA, Blue Origin), and possesses the AWS cloud integration capability to create an enterprise internet offering more integrated than anything Starlink currently sells. However, Amazon is also running years behind SpaceX’s constellation development timeline — Starlink was effectively launched on the backs of 165 Falcon 9 missions per year, a deployment rate that Kuiper cannot match with current launch capacity. SpaceX’s ability to self-launch Starlink satellites at marginal cost is perhaps its deepest competitive moat: each Starlink satellite ride costs approximately $1,000 per kilogram internally, versus $6,000+ per kilogram for the closest competitor’s launch pricing.

04 — Launch Services

The Factory in the Sky: Falcon 9’s Industrial Revolution

The launch services segment is not SpaceX’s fastest-growing business, but it is arguably the most important strategically, because it is the capability that enables everything else. The Falcon 9’s reusability has not simply lowered launch prices — it has transformed the orbital economy in a way that no analysis written before 2017 could have modeled. When a technology reduces cost by 70-80%, it does not just grow the existing market. It creates entirely new markets that were previously uneconomical.

The Economics of Reusability

A new Falcon 9 first stage costs approximately $30-35 million to manufacture. Refurbishing a recovered booster for the next flight costs roughly $250,000 in direct materials. Even accounting for additional inspection, labor, and propellant costs — bringing the total refurbishment bill to perhaps $1-2 million per re-flight — the economics are transformative. A booster flying 20 times amortizes its manufacturing cost across 20 missions at roughly $1.5-1.75 million per flight in capital cost, compared to $30 million for a single expendable competitor rocket.

The Falcon 9’s all-in cost per launch, including booster amortization, propellant, upper stage, fairing, and operations, is estimated at approximately $28-32 million for mature refurbished configurations. Against a list price of $74 million, this implies gross margins of 56-63% on external commercial launches — margins that would be the envy of any aerospace company. The government launch pricing, under National Security Space Launch (NSSL) contracts, tends to be higher and thus even more profitable.

The Manifest: Who’s Flying on Falcon?

Of SpaceX’s 165 launches in 2025, approximately 74.5% were Starlink constellation-building missions. The remaining 25.5% — roughly 42 commercial and government flights — carried institutional payloads for NASA, the Department of Defense, the NRO, commercial satellite operators, and international customers. This ratio reveals something important: SpaceX is primarily its own customer for launch services. The “launch services revenue” reported in the Space segment ($4.1 billion) represents a mix of external customer revenue and internal transfer pricing for Starlink satellite deployment.

The implications of this vertical integration cannot be overstated. SpaceX does not pay the launch tax that every competitor satellite operator faces. A OneWeb or Amazon Kuiper satellite costs $3,000-8,000 per kilogram to orbit. SpaceX’s Starlink satellites ride for an estimated $1,000 per kilogram at internal cost. Over a constellation of more than 10,000 satellites averaging approximately 280 kilograms each, this represents a structural cost advantage in the billions of dollars.

Starship: The Potential Discontinuity

SpaceX has invested over $15 billion in Starship development as of the S-1 filing, with $3 billion in R&D spending in 2025 alone devoted to the program. As of May 2026, SpaceX has conducted 11 Starship integrated flight tests, with the V3 variant and upgraded Raptor 3 engines entering testing. Commercial Starlink V3 satellite deployments using Starship are expected to begin in the second half of 2026.

The financial significance of a fully reusable Starship at scale is not incremental — it is potentially transformative. At 50+ flight reuse of both stages, SpaceX projects a cost per kilogram to low Earth orbit below $20. At that price, the entire launch market re-prices, every competitor becomes economically unviable, and entirely new applications — orbital manufacturing, space-based solar power, Moon and Mars transit — become commercially viable for the first time. Starship is not just a larger rocket. It is the precondition for a space economy an order of magnitude larger than the one that exists today.

05 — The Financials

Reading Between the Lines: Revenue, Margins, and the xAI Distortion

SpaceX’s S-1 financials are simultaneously impressive and deliberately complex. The consolidation of xAI into the filing created a headline net loss of $4.94 billion on $18.67 billion in revenue — a figure that masks a fundamentally profitable underlying space and connectivity business. Understanding the true financial architecture of SpaceX requires stripping out the xAI distortion and examining each segment on its own terms.

Segment-Level Profitability

Before xAI entered the picture, SpaceX was tracking toward approximately $791 million in net income in 2024, with internal Sacra and Reuters estimates suggesting the standalone space/connectivity business generated approximately $8 billion in EBITDA-level profits in 2025. Starlink’s $4.42 billion in operating income, combined with the launch segment’s estimated 50%+ gross margins on external launches, creates a genuinely profitable business at the core. The consolidated loss is an accounting artifact of the xAI merger, not a reflection of operational failure in space and connectivity.

Capital Intensity: The Starship Bill

The S-1 is unusually transparent about Starship capital consumption. The company has spent over $15 billion on Starship development over its history, with 2025 alone contributing $3 billion in R&D (all attributed to Starship). This is a higher annual development spend than the entire annual revenue of most commercial aerospace companies. The question for investors is not whether this spending is worthwhile — the potential return on a successful Starship is almost unbounded — but rather who bears the cost of failure.

The filing reveals that SpaceX has structured some Starship development costs as reimbursable under the NASA Artemis Human Landing System contract — a $4+ billion arrangement that transfers a portion of the development risk to the US taxpayer. The remaining cost is borne by SpaceX shareholders and, increasingly, by Starlink’s cash flow. This creates a fascinating capital structure: Starlink subscribers in rural Montana and rural Kenya are, in aggregate, financing humanity’s first crewed Mars vehicle.

Working Capital and Contract Structure

Launch services revenue is typically contracted 12-36 months in advance with significant deposits. This creates a working capital advantage: SpaceX collects cash from customers before incurring the variable costs of a mission. Government contracts under firm-fixed-price structures provide revenue visibility but limit upside. The Starlink business, by contrast, is month-to-month subscription revenue with very low churn in established markets (estimated at under 1.5% per month), creating an extremely stable, growing recurring revenue base.

The key insight: Strip out xAI, and SpaceX’s space and connectivity operations generated approximately $5.6 billion in combined operating income in 2025 on $15.5 billion in revenue — a blended operating margin of roughly 36%. That is not an aerospace company. That is a subscription software business that happens to operate the world’s most capable rocket fleet.

06 — Government Risk

The Government Dependence Question: 30% of Revenue, 100% of Existential Leverage

SpaceX holds $22 billion in cumulative federal contracts across NASA, the Department of Defense, the National Reconnaissance Office, and the Space Development Agency. With 52 active federal contracts worth $11.8 billion in remaining value, government and defense customers account for an estimated 30-40% of SpaceX’s total revenue in 2025 — and while that share is falling as Starlink scales, the absolute dollar value of government revenue is rising, driven by Starshield, NSSL launch contracts, and the Artemis lunar program.

This concentration creates a risk that the S-1 addresses explicitly: government revenue behaves fundamentally differently from consumer subscription revenue. Starlink subscribers are sticky; government contracts can be rerouted with a signature. The political dimension of this risk has become acutely relevant in the post-DOGE environment. Elon Musk’s leadership of the Department of Government Efficiency in 2025, his subsequent public falling-out with elements of the Trump administration, and ongoing congressional scrutiny of the relationship between government contracting and SpaceX’s competitive positioning have all introduced political uncertainty into what were previously treated as durable revenue streams.

The Starshield Wild Card

Starshield represents both SpaceX’s most lucrative government relationship and its most analytically opaque business line. The classified satellite internet system, purpose-built for military and intelligence community use under a 2021 NRO contract initially valued at $1.8 billion, has since expanded substantially. Over 200 Starshield satellites have been deployed as of mid-2026, with the NRO confirming it reached that milestone within two years of beginning its proliferated architecture program. By 2026, Starshield revenue is projected at approximately $3.2 billion annually — but because the program is classified, the S-1 provides limited public disclosure, meaning investors in SPCX must essentially trust that this revenue stream is as robust as the redacted portions of the filing suggest.

NASA Artemis: A Crown Jewel Relationship

SpaceX’s relationship with NASA on the Artemis human lunar landing program has evolved from a single $2.89 billion contract in 2021 to a total relationship worth over $4 billion in direct funding, with SpaceX’s Starship serving as the exclusive Human Landing System for initial Artemis lunar surface missions. In March 2026, NASA further restructured the Artemis program, reducing Boeing’s role and increasing dependence on SpaceX’s Starship as the primary surface descent and ascent vehicle — a development that concentrated both the upside and the political risk of the lunar program more heavily in SpaceX’s direction.

“Canceling SpaceX contracts would cripple the DoD launch program. There is no credible alternative at scale. That dependency is SpaceX’s greatest government revenue protection and its greatest political vulnerability simultaneously.”

Breaking Defense, June 2025

07 — Risk Factors