Starbucks: The Long Walk Back

Brian Niccol's first year: what's working, what isn't, and what it will take

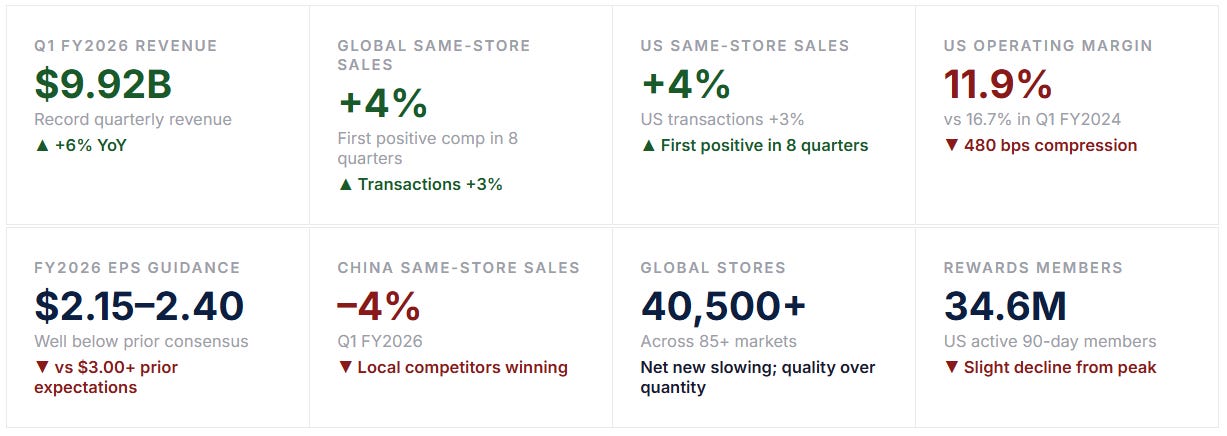

Starbucks hit a record $9.92 billion in quarterly revenue and saw its first positive US transaction growth in eight quarters. The "Back to Starbucks" plan is showing early signs of working. But US operating margin sits at 11.9% — nearly 5 points below where it was two years ago — and China remains deeply challenged. The recovery story is real, but it's going to take longer than the market initially hoped.

Snapshot

Q1 FY2026 — The First Signs of Life

Leadership

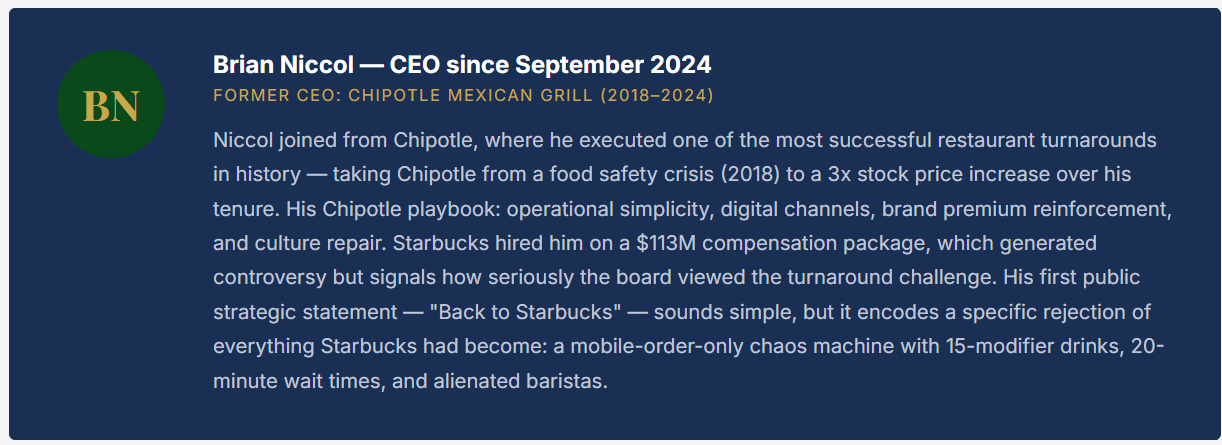

Why the Niccol Hire Was Extraordinary

The Niccol hire matters for one reason above all others: he has done this before. Restaurant turnarounds from operational complexity creep are a specific, well-understood problem, and Niccol’s record at Chipotle is the closest comparable in modern restaurant history. The bear case on Starbucks isn’t that Niccol is wrong about the diagnosis — virtually everyone agrees the operational complexity issue is real. The bear case is that Starbucks’s structural position is weaker than Chipotle’s was in 2018, and the fix will take longer and cost more.

The Chipotle Comparison — Why It’s Both Inspiring and Cautionary

Chipotle’s problem in 2018 was primarily a brand/trust problem stemming from a specific food safety incident. The unit economics were fundamentally sound. Starbucks’s problem is different: it’s an operational complexity problem compounded by competitive pressure from independent cafes and fast-casual chains, plus a secular shift in how younger consumers value third-place experiences. The Chipotle playbook (simplify menu, focus on throughput, invest in digital) is directionally correct for Starbucks, but Starbucks has more structural challenges to address simultaneously — including a labor relations problem and a China competitive crisis that have no Chipotle parallel.

Root Cause Analysis

How Starbucks Lost the Plot

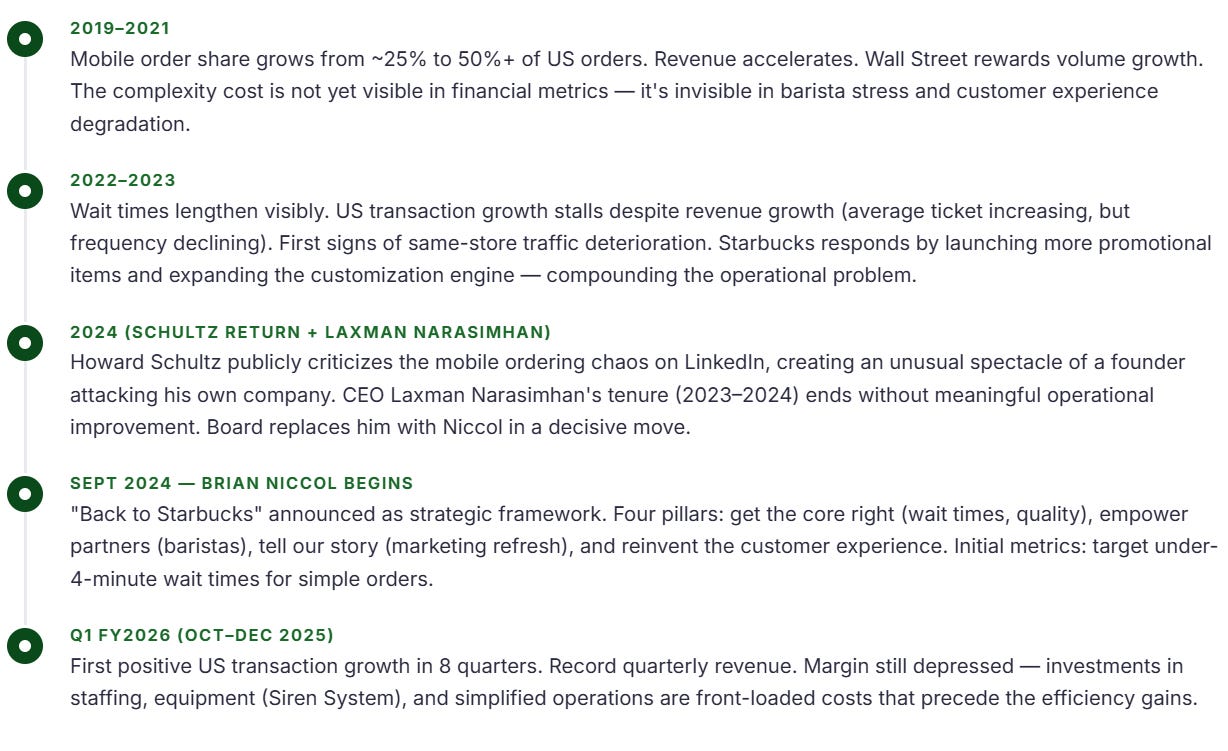

Starbucks went through a period between 2020 and 2023 where growth strategy prioritized mobile order volume above all else. Mobile ordering is efficient and profitable — it drives ticket size and eliminates the friction of queuing. But Starbucks optimized for mobile ordering without adequately investing in the operational capacity to fulfill it. The result was a catastrophic degradation of the in-store experience.

By 2023–2024, the average Starbucks mobile order wait time had increased to 8–12 minutes in busy urban locations. Baristas were simultaneously managing: complex customization requests with 15+ modifiers per drink, competing queues (mobile vs. in-person vs. drive-through), a menu that had expanded to hundreds of items, and new promotional “secret menu” items generating huge social media volume but requiring unique preparation.

Strategic Plan

“Back to Starbucks” — What It Actually Means

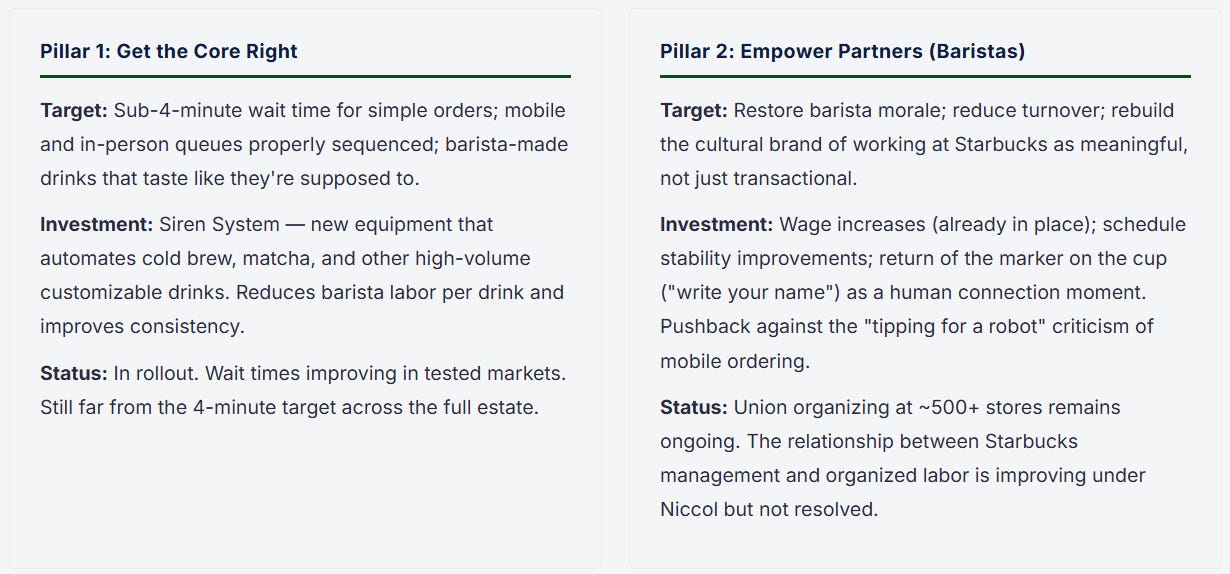

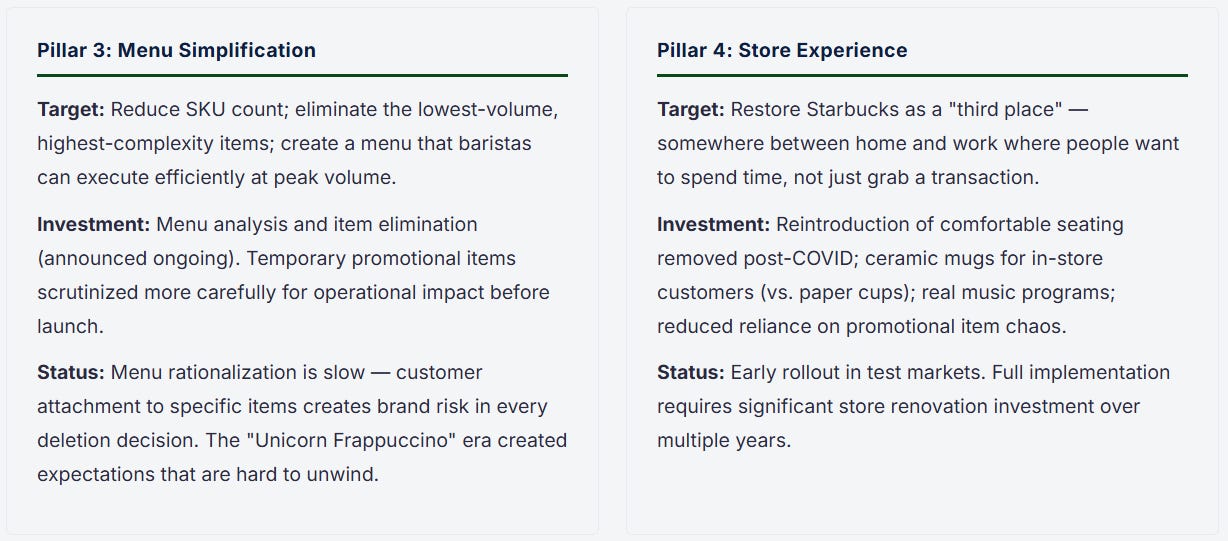

Niccol’s “Back to Starbucks” framework is not nostalgia. It’s an operational restructuring philosophy: return to the things that made Starbucks the world’s most dominant coffee chain, and stop doing the things that diluted that position in the pursuit of mobile order volume. The four pillars are straightforward, but each has significant cost implications.

⚠ The Margin Recovery Will Take Longer Than Hoped

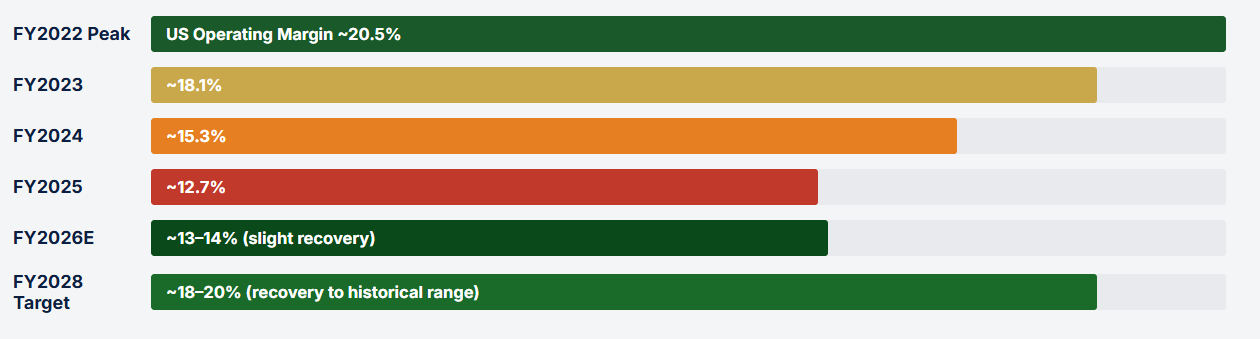

Niccol’s plan is front-loaded with costs: new equipment (Siren System), wage increases, additional barista hours, and store renovation investment. The efficiency gains come later — once throughput improves and labor per drink decreases. This creates a J-curve financial profile where margins compress further before recovering. Management’s FY2026 operating margin guidance implies minimal improvement from FY2025 levels. The margin recovery to 20%+ US operating margin — where Starbucks traded historically — is likely a FY2027–2028 story at the earliest, not a FY2026 story.

China

The China Problem Has No Easy Solution

China is Starbucks’s second-largest market by store count and was supposed to be a primary growth engine for the next decade. The original thesis: as China’s middle class expanded, premium coffee culture would follow the same trajectory seen in Japan, South Korea, and Taiwan. Starbucks would be positioned to capture that growth through its 7,000+ store network and established brand.

That thesis has run into two problems: Luckin Coffee and a changed economic environment. Luckin, the domestic Chinese coffee chain that famously imploded in a 2020 accounting fraud scandal, came back stronger after restructuring. By 2024, Luckin had more locations in China than Starbucks — approximately 18,000 stores vs. Starbucks’s 7,000 — and a price point roughly 40–50% lower. Luckin’s app-only, mobile-first model and aggressive promotional pricing have structurally captured the everyday coffee purchase occasion that Starbucks relied on for transaction volume.

Starbucks’s China same-store sales have been negative for multiple consecutive quarters. The company is facing a structural pricing disadvantage (Luckin’s average ticket is ~$3–4 vs. Starbucks’s ~$7–8), a location disadvantage (Luckin is in more tier-2 and tier-3 cities), and a consumer sentiment headwind as some Chinese consumers increasingly prefer domestic brands over Western ones amid ongoing geopolitical tensions.

⚠ China: Sale, JV, or Long Decline?

Starbucks has publicly stated it is exploring “strategic alternatives” for its China business — including a potential sale or joint venture partnership. This is significant. A full or partial sale would likely be at a depressed valuation (Chinese tea-coffee chains trade at much lower multiples than US consumer companies), but it would eliminate a structural earnings headwind and allow Niccol to focus entirely on the North America turnaround. Any deal announcement would likely be read as a catalyst — getting the drag off the P&L — even if the economics of the deal itself are modest. China remains the single biggest overhang on Starbucks stock today.

Financial Deep Dive

The Margin Story: Fall, Floor, and Recovery

Understanding Starbucks’s investment case requires understanding the margin trajectory. At its peak, the US segment ran approximately 20–21% operating margins, reflecting the extraordinary unit economics of a premium brand running dense urban locations with high ticket sizes and strong digital order attachment. That margin has been systematically compressed over three years.

The margin compression came from three places: wage inflation (barista wages up 20%+ since 2021), the cost of more barista labor hours required to manage complex drink preparation, and deleverage of fixed costs as transaction volumes declined. The recovery requires same-store transactions to grow (covering fixed costs), the Siren System to improve labor productivity, and menu simplification to reduce per-drink preparation time.

The Rewards Program: 34 Million Reasons for Cautious Optimism

Starbucks Rewards members (34.6M active 90-day US members) represent an extraordinary loyalty and data asset. These members account for approximately 57% of US company-operated revenue — they visit more frequently, spend more per visit, and are significantly more resilient to price increases than non-member customers. The slight decline from the program’s peak reflects disengagement during the operational chaos period. Re-engaging lapsed members through improved experience is likely easier than acquiring new customers — and re-engagement marketing campaigns can be precisely targeted through the app. If the transaction recovery holds and lapsed members return, the rewards data could accelerate the comp improvement significantly.

Competition

The Coffee Competitive Landscape Has Changed

Starbucks built its position in the 1990s and 2000s largely in the absence of direct competitive alternatives at scale. The premium coffee shop market was thin, independent coffee culture was small, and McDonald’s McCafé and Dunkin’ were clearly differentiated down-market products. That competitive environment no longer exists.

Dutch Bros is the most interesting competitive threat to watch. With ~900 US locations in 2025, growing at 150+ stores per year, Dutch Bros has built a service culture and brand identity — primarily with Gen Z and millennial customers — that is explicitly positioned as the “anti-Starbucks.” Their average service time (drive-thru focused model) is faster, their prices are slightly lower on comparable items, and their staff culture is genuinely differentiated. If Dutch Bros reaches 2,000+ locations by 2028, it will be directly competing with Starbucks in Sunbelt and Mountain West markets that are currently Starbucks strongholds.

Scenario Analysis

Three Paths Over the Next Two Years

LongYield Perspective

The Verdict

Starbucks’s Q1 FY2026 — the first positive US transaction growth in eight quarters — is genuinely encouraging, not just noise. The operational problems that drove two years of deteriorating same-store sales are well understood, the new CEO has a specific and credible plan to address them, and there are real early signs that plan is working. That’s the bull case in miniature: a recoverable problem, a competent fixer, early green shoots.

The counterarguments are real. The margin recovery timeline is longer than investors initially hoped when Niccol was hired. China is not a turnaround story — it’s a structural competitive loss that may require an exit from the pure-ownership model. The labor relations environment (500+ unionized stores) adds friction to every operational initiative Niccol wants to implement. And the macro backdrop — consumer discretionary spending pressure, particularly on premiumized everyday luxuries — is not favorable going into 2026.

The honest framing: Starbucks at current prices is a bet on Niccol executing the turnaround over 24–36 months. It is not a bet on a quick recovery. If you have that time horizon, the risk/reward is reasonable — the brand durability is genuine, the digital/loyalty infrastructure is exceptional, and the US unit economics at full health are among the best in quick-service restaurants. If you need the recovery to be visible in the next two quarters to justify the position, the uncertainty is too high.

The One Number That Will Define the Next 12 Months

US same-store transactions. Not revenue, not EPS, not margin — transactions. If Starbucks can sustain positive transaction growth for three consecutive quarters in the US, it means the operational fixes are actually driving repeat customer behavior, not just ticket inflation. Three quarters of positive transactions would validate the turnaround thesis and likely trigger significant institutional re-rating. Two quarters of positive transactions followed by a reversal would confirm that Q1 FY2026 was a one-time setup effect, and the thesis would need reassessment. Watch Q2 FY2026 (reporting ~April/May 2026) very closely.