TeraWulf: The Nuclear-Powered Miner That's Quietly Becoming an AI Infrastructure Company

While the market debated Bitcoin's post-halving economics, TeraWulf was converting its nuclear-powered Lake Mariner campus into one of the most cost-advantaged AI/HPC data center sites in North Americ

")

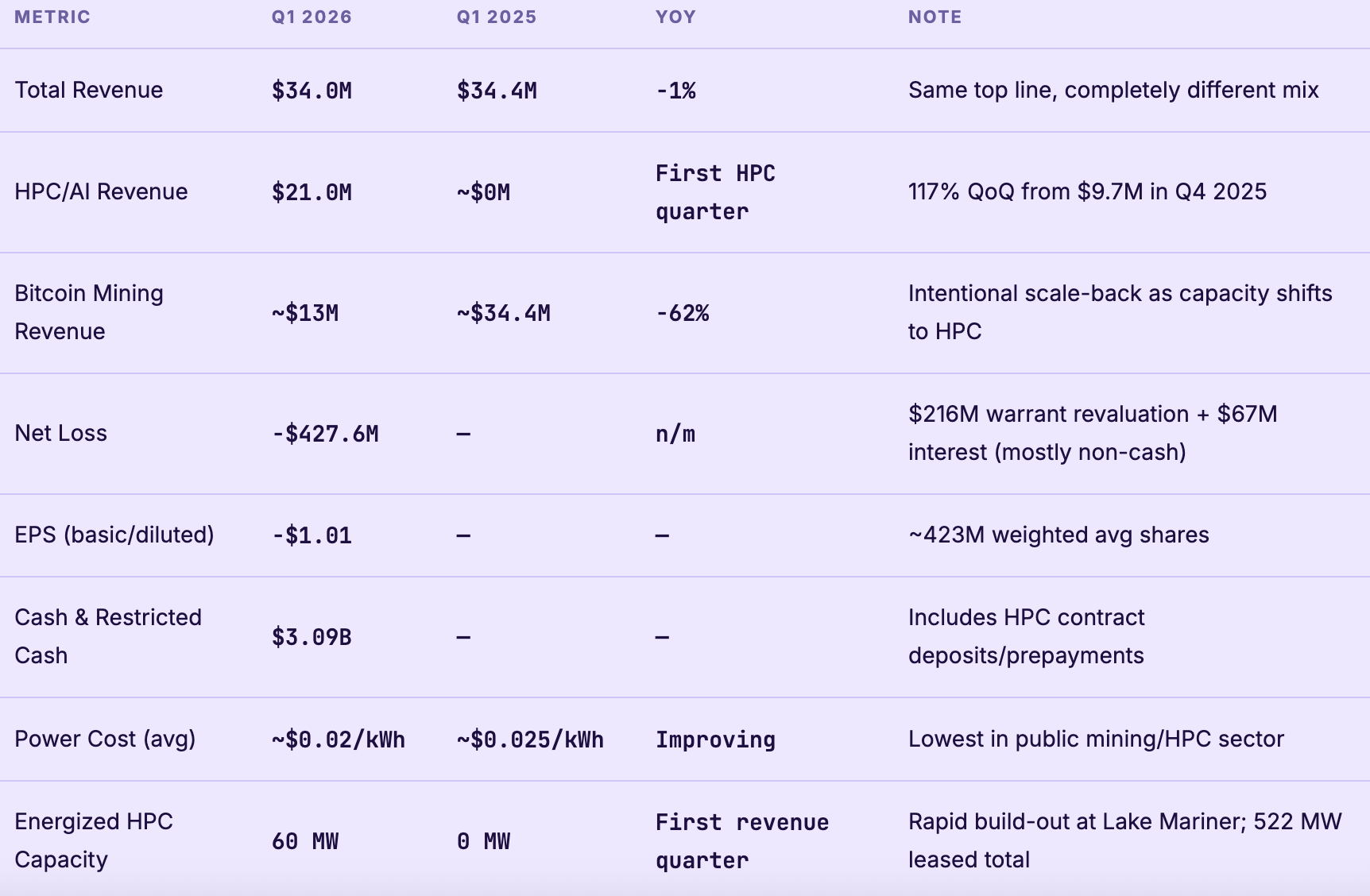

TeraWulf began as a Bitcoin miner with a differentiating premise — use nuclear and hydroelectric power instead of coal and gas, and build on zero-carbon baseload rather than volatile renewable curtailment. That premise was correct. The nuclear power advantage gave TeraWulf the lowest electricity costs in the mining sector at roughly $0.02 per kilowatt-hour. But the more important insight came after the halving: the same nuclear-powered infrastructure that makes Bitcoin mining cheap makes AI/HPC data center co-location extraordinarily attractive. Q1 2026 is the quarter where HPC revenue exceeded Bitcoin mining revenue for the first time — $21M vs $13M, on a base of $34M total. The headline loss of $427.6M ($1.01/share) is large but almost entirely non-cash: $216.3M of warrant revaluation and $67.1M of interest expense. Strip those out, and the operating infrastructure is generating real cash. The transition is not coming — it already happened.

01 — Origin Story

From Clean-Energy Miner to Nuclear-Powered HPC Platform

TeraWulf was founded in 2021 by Paul Prager — who also founded Beowulf Electricity & Data Inc. (the “wulf” in TeraWulf) — and a team of energy infrastructure veterans who saw Bitcoin mining as fundamentally an energy business, not a technology business. The core thesis was simple: mining profitability is determined almost entirely by electricity cost. Companies that secured the cheapest, most reliable power would win; companies paying market rates would be perpetually exposed to Bitcoin price volatility. The team identified nuclear and hydroelectric baseload as the ideal power sources — low cost, extremely stable, and immune to the curtailment issues that plagued wind and solar-dependent mining operations.

The flagship site is Lake Mariner in Barker, New York — a former coal plant on the shores of Lake Ontario that was converted into a large-scale digital infrastructure campus. The site is co-located with the Nine Mile Point Nuclear Generating Station, one of the largest nuclear power plants in the United States, giving TeraWulf access to nuclear baseload power at rates unavailable to almost any other industrial consumer in America. A second site, Nautilus, was TeraWulf’s joint venture in Pennsylvania co-located with the 2.5 GW Susquehanna nuclear station — the country’s first fully nuclear-powered Bitcoin mining facility. In 2024, TeraWulf sold its 25% Nautilus stake back to partner Talen Energy for $85M cash plus equipment, a 3.4x return on invested capital. All future campus development is now concentrated at Lake Mariner and new acquisitions in Kentucky, Maryland, and Texas (the Abernathy JV with FluidStack).

The HPC pivot was not originally in the business plan. But as the April 2024 Bitcoin halving approached — cutting block rewards from 6.25 BTC to 3.125 BTC and halving the per-unit economics of mining — TeraWulf’s leadership recognized that their nuclear-powered campuses had an attribute far more valuable than cheap mining: extreme power density, reliability, and cost structure that AI/GPU workloads require. The decision to convert mining infrastructure to HPC co-location was made before the halving hit. By Q1 2026, it is producing results.

02 — Q1 2026 Earnings

The Crossover Quarter: HPC Surpasses Bitcoin for the First Time

Q1 2026 is a landmark for TeraWulf. For the first time in the company’s history, HPC/AI co-location revenue exceeded Bitcoin mining revenue in a single quarter — $21M vs $13M, on total revenue of $34.0M. The top-line number looks flat year-over-year ($34.0M vs $34.4M in Q1 2025), but that obscures a complete business model transformation: in Q1 2025, TeraWulf generated essentially all its revenue from Bitcoin mining; in Q1 2026, HPC leases are 62% of the total. The Q1 2026 net loss of $427.6M ($1.01/share) looks alarming but is overwhelmingly non-cash — $216.3M of warrant revaluation losses and $67.1M of interest expense. Operationally, the infrastructure is generating real cash against a $3.09B liquidity position that reflects contracted HPC deposits and prepayments.

The gross margin profile is transforming rapidly. HPC leases are structured as long-term contracts with fixed monthly payments — more akin to data center REITs than volatile mining economics. The take-or-pay nature of HPC contracts means TeraWulf receives revenue whether or not the tenant's GPU clusters are running at capacity. Bitcoin mining revenue, by contrast, fluctuates daily with BTC price, network hashrate difficulty, and power costs. The shift toward HPC is a deliberate margin quality upgrade, not just a revenue growth story.

03 — The Nuclear Advantage

~$0.02/kWh: A Moat That Most Competitors Can’t Replicate

The Lake Mariner site’s power cost advantage is the single most important fact in the TeraWulf investment thesis. At roughly $0.02 per kilowatt-hour — compared to the $0.05–0.08/kWh that most commercial AI data centers pay for grid power — TeraWulf’s HPC tenants receive a subsidy that is impossible to replicate without nuclear co-location. Major hyperscalers are desperately signing nuclear power purchase agreements (Microsoft with Constellation Energy at Three Mile Island, Google with Kairos Power) precisely because they understand that AI compute’s insatiable power demand requires firm, dispatchable baseload — and nuclear is the only proven source at scale.

TeraWulf has this advantage already secured, already built, already operating. New nuclear plants take 10–15 years to permit and construct. The existing co-location agreement at Lake Mariner is not easily replicated by a competitor starting today. This creates a durable infrastructure moat that is fundamentally different from most technology competitive advantages — it’s physical, not intellectual, and it gets more valuable as AI power demand grows.

04 — The HPC/AI Pivot

Converting Mining Racks to GPU Clusters: The Economics of the Pivot

TeraWulf’s HPC model is elegantly simple: build out power infrastructure and data hall space at Lake Mariner, sign multi-year take-or-pay leases with AI/HPC tenants at rates of approximately $12–15M per year per 10 MW of capacity, and collect predictable cash flows. The tenants bring their own GPU hardware (Nvidia H100/H200/B200 clusters); TeraWulf provides the power, cooling, connectivity, and physical security. This “bare metal” or “colocation” model is lower margin than running the GPU workloads directly, but it is also lower capital intensity — TeraWulf doesn’t need to buy $50K+ Nvidia GPUs to monetize its nuclear power advantage.

The known HPC tenants include Core42 (a UAE-based AI infrastructure company backed by G42, the Abu Dhabi AI conglomerate with Microsoft as a strategic partner), FluidStack (a GPU cloud marketplace serving AI startups with Google providing credit enhancement on FluidStack agreements commencing in 2026), and future tenants through the Abernathy JV — a majority-owned 84 MW campus in Texas being developed alongside FluidStack, targeted for Q4 2026 delivery. Google’s credit enhancement is the most consequential tenant development in recent months: it transforms FluidStack contracts from startup credit risk to effectively investment-grade, dramatically de-risking the $12.8B backlog.

05 — Bitcoin Mining Economics

Post-Halving: Why WULF’s Mining Segment Still Makes Money