Tesla Q1 2025: Earnings Under Pressure Amid Tariffs and the “Musk Factor”

Tesla’s first quarter of 2025 saw a notable slowdown in financial performance, driven by lower vehicle deliveries, slimmer margins, and external headwinds. The electric vehicle leader navigated production retooling for its flagship Model Y, faced tariff challenges, and contended with the impact of Elon Musk’s high-profile government role. Below we break down the key financial and operational highlights, the influence of tariffs, Musk’s governmental involvement, and how the market is reacting.

Financial and Operational Performance

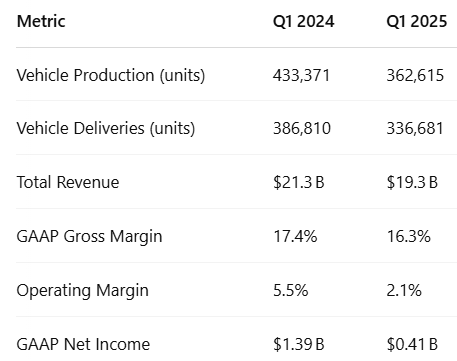

Tesla’s revenue and profit declined sharply in Q1 2025 compared to a year ago. Total revenue fell about 9% year-over-year to $19.3 billion, reflecting lower delivery volumes and reduced vehicle average selling prices. GAAP net income dropped to just $409 million, a steep 71% decline from $1.39 billion a year prior. This drove Tesla’s operating margin down to 2.1% in Q1 2025 (from 5.5% in Q1 2024), as profitability was squeezed by a combination of factors.

The drop in vehicle deliveries was a major factor. Tesla produced ~362,600 vehicles and delivered ~336,700 in the quarter, down 16% and 13% year-over-year, respectively. This dip was partly planned – Tesla temporarily halted production at all four vehicle factories to simultaneously upgrade them for the refreshed Model Y, sacrificing several weeks of output. Indeed, Tesla’s management had signaled that an unprecedented global factory retooling would make Q1 a “tricky” quarter with lost production. The lower volumes meant higher unit costs (less fixed-cost absorption) and, combined with price cuts/incentives on older models, led to thinner automotive gross margins.

Table 1: Key Q1 2025 Metrics vs. Q1 2024

Despite the weakness in automotive, Tesla’s energy division was a bright spot. Energy generation and storage revenue grew 67% YoY to $2.73 billion, and Tesla achieved record gross profit in its energy storage business. This helped offset some automotive decline. Operating expenses rose about 9% as Tesla continued to invest heavily in AI, the Optimus robot, new vehicle development (including the Cybertruck and a future affordable model). Free cash flow did turn positive at about $0.7 billion, aided by a ramp-down in capital spending, and quarter-end cash grew to a robust $37 billion.

In summary, Q1 2025 was a transitional quarter for Tesla. Revenue and deliveries slipped due to planned factory upgrades and some demand headwinds, compressing margins and profits. However, management emphasized this was a temporary setback and pointed to improving output of the new Model Y and strength in the energy segment as reasons for optimism.

Tariff Impacts

Tariffs emerged as a key theme in Tesla’s results and outlook. Tesla has spent years localizing its supply chains, which has made its U.S.-made models about 85% compliant with USMCA (United States-Mexico-Canada Agreement) content rules. This positioning gives Tesla some insulation from trade barriers, but not full immunity. In May 2025, new Section 232 automotive tariffs take effect, extending to parts and vehicles from Canada and Mexico – regions integral to Tesla’s supply chain. Tesla’s finance chief noted that these tariffs will “have an impact on our profitability”, estimating a cost on the order of a “couple of thousand” (dollars) per vehicle. Even for Tesla, which enjoys higher margins than many legacy automakers, such incremental costs are meaningful in the current margin-constrained environment.

The tariff drag is even more pronounced in the energy business. Tesla relies on lithium iron phosphate (LFP) battery cells from China for its Megapack grid storage products, so import tariffs on batteries significantly raise costs. Tesla is responding by fast-tracking domestic cell production – it has begun commissioning equipment to produce LFP cells in the U.S., though that equipment will only cover a fraction of needed capacity initially. The company is also seeking non-Chinese suppliers, but shifting a complex battery supply chain takes time.

Tariffs also indirectly raise Tesla’s costs to expand: many large manufacturing equipment and tooling must be imported (since U.S. suppliers have limited capacity), which now faces tariffs. Tesla indicated its 2025 capital expenditures will exceed $10 billion even after some optimizations, partly due to tariff-related cost inflation on new factory equipment. In short, trade policies are a near-term headwind for Tesla’s automotive and energy segments. The company’s strategy of localizing production and sourcing is softening the blow, but until new domestic facilities and suppliers come online, tariffs are pressuring margins.

Elon Musk’s Government Role and Brand Perception

One unique factor this quarter was Elon Musk’s involvement with the U.S. government – specifically, his role leading the Department of Government Efficiency (DOGE) under President Trump. Musk spent considerable time in Washington working on cutting federal waste, an effort he views as vital for the country’s fiscal health. However, this unusual CEO side-gig has not come without controversy. Musk acknowledged “blowback” and organized protests targeting him and the DOGE team, suggesting that those benefiting from waste and fraud are pushing back.

This political involvement appears to have spilled over into Tesla’s brand image. Tesla management noted “unwarranted hostility” toward the Tesla brand and employees in certain markets, including vandalism, which negatively impacted sales in those areas. In other words, Musk’s polarizing government role may have hurt consumer sentiment toward Tesla for some customers. This is a rare instance where Tesla’s brand – typically an asset – faced headwinds due to external perceptions. Some investors have been concerned that Musk’s attention is divided and that Tesla could suffer reputationally from association with partisan politics.

Musk sought to reassure stakeholders on the call. He explained that the “heavy lifting” at DOGE is largely done, and starting in May he would “be allocating far more of my time to Tesla” (while devoting only 1–2 days a week to the government project). Musk emphasized that Tesla itself remains on solid footing (“not on the edge of death, not even close” in his words), and he remains “extremely optimistic” about Tesla’s future now that he can refocus on the company’s core mission. Investors will be watching to see if Musk’s reduced presence in D.C. helps mend Tesla’s public image and allows him to drive key initiatives (like vehicle programs and operations) more directly in the coming quarters.

Market Reaction and Outlook

Wall Street and the market have reacted cautiously to Tesla’s Q1 results. The immediate response to the earnings release was one of concern about shrinking margins and earnings. A 13% drop in deliveries and the erosion of automotive profit metrics were not entirely unexpected (given Tesla’s factory upgrades and price cuts), but the magnitude of the net income decline and a mere 2% operating margin raised eyebrows. Tesla’s stock traded lower after the announcement, but recovered later reflecting investor jitters about near-term profitability and the tariff-related cost increases looming in Q2. Many analysts see 2025 as a more challenging year for Tesla’s earnings, a “reset” period where the company is making strategic factory changes and weathering external issues (tariffs and PR challenges) before growth re-accelerates.

At the same time, there are optimistic signals that tempered the market’s negativity. Tesla reiterated that demand remains robust – the company managed to sell through remaining inventory of the outgoing Model Y even amid the quarter’s headwinds. Executives stressed that with factories now retooled, production and delivery volumes should rebound in subsequent quarters, which could restore economies of scale. Additionally, new products and technologies are on the horizon. Tesla confirmed that it is on track to start production of its long-awaited next-generation affordable model in June 2025. This lower-cost model could open up a much larger market and boost volumes. Furthermore, Musk provided updates on Tesla’s autonomy efforts, announcing a pilot robotaxi service in Austin by the end of 2025 and reiterating his bold prediction that by the second half of 2026 Tesla could have “millions” of its cars operating fully autonomously. Such developments in self-driving technology and new vehicle segments represent significant long-term earnings potential.

Analysts and investors are split – in the short term, concerns center on margins, tariffs, and any lingering brand fallout from Musk’s government involvement. In the long term, Tesla’s roadmap of product launches (from the Cybertruck to the new mass-market car) and advancements in AI and energy storage keep the bullish thesis intact. Tesla’s CFO summarized the situation well, noting the company faces “near-term challenges” from tariffs and brand image, but remains focused on its strategy of compelling products at competitive prices and on bringing new models to market.

Overall, Tesla’s Q1 2025 results underscore both the pressures and the promise facing the company. Investors will be watching upcoming quarters to see if Tesla can translate its investments and upgrades into renewed growth – and whether external issues like tariffs and the “Musk factor” subside – thereby steering the company back toward higher margins and robust profits.