The European Defense Supercycle

Four Decades of Hollowing Out, One Structural Reversal — Why Europe's Rearmament Is a Capital Cycle Event, Not a Political Story, and What It Means for the Companies, the Supply Chains, and the Invest

Key Takeaways

The European defense supercycle is not a theme. It is a structural capital cycle triggered by four decades of underinvestment, a geopolitical shock that made the underinvestment undeniable, and a fiscal response — led by Germany — of historic magnitude. Capital cycles of this kind typically run for 10–20 years.

Germany’s suspension of its constitutional debt brake and announcement of a €500B+ special infrastructure and defense vehicle is the single most important European fiscal event since the euro was created. It permanently shifts the baseline assumptions for European defense spending.

European defense industrial capacity was not maintained through the post-Cold War “peace dividend” decades. The supply chain cannot ramp instantly. The companies that can actually deliver — Rheinmetall, Leonardo, BAE Systems, Thales, Safran — face years of demand that exceeds their near-term capacity. That is a pricing-power environment of unusual quality.

The US factor — an administration that has explicitly questioned NATO’s value and made European strategic autonomy a political necessity — is an accelerant, not the cause. Even in a world where US commitment to NATO is fully restored, Europe has concluded that sovereign defense capacity is not optional. The spending continues regardless.

The bottlenecks are real and investable: 155mm artillery shell capacity, propellant and explosives chemistry, naval vessel build rates, drone manufacturing, satellite communications, and the skilled labor to operate all of the above. Understanding where the constraint is matters more than buying the most recognizable name.

Executive Summary

In February 2025, Germany’s incoming government announced that it would suspend the constitutionally enshrined Schuldenbremse — the debt brake that had limited German federal borrowing to 0.35% of GDP — to create a €500 billion special fund for infrastructure and defense. The vote passed the Bundestag with a supermajority. In the same week, NATO defense ministers met to discuss raising the alliance’s spending target from 2% to 3% of GDP. Neither event was coincidental. Both were consequences of the same structural realization: Europe had systematically disarmed itself over 35 years, and the cost of that disarmament had become undeniable.

This memo analyzes the European defense supercycle not as a news story but as a capital cycle — because that is what it is. A capital cycle describes the dynamics of investment, capacity, supply-demand imbalance, and pricing power that emerge when a sector has been starved of capital for an extended period and then receives a sudden, large, and sustained demand shock. The defining characteristics of a classic capital cycle setup — multi-decade underinvestment, inelastic near-term supply, sovereign demand with political compulsion, and long lead times for capacity expansion — are all present in European defense, in textbook form. The only question is which companies, segments, and investment structures are best positioned to capture the value created by that imbalance.

We identify the specific bottlenecks in the European defense industrial base, evaluate the key beneficiaries by segment (land systems, naval, aerospace, ammunition, cyber, and space), examine the supply chain constraints that will shape the timing and distribution of earnings growth, assess the US factor as an accelerant rather than the fundamental cause, and build three long-term scenarios with valuation implications. Our conclusion: this is one of the clearest and most structurally supported capital cycle opportunities available to equity investors today, and the market has only partially priced it.

Section I

The Capital Cycle Framework: Why This Is Different from the Last Defense Upcycle

The capital cycle framework, developed most systematically by Edward Chancellor and applied to sectors from shipping to mining to energy, describes a predictable sequence: extended capital scarcity creates supply shortfalls, which create pricing power, which create earnings growth, which attract new capital, which eventually creates overcapacity, which destroys pricing power. The most profitable entry point is early in the recovery phase — after the demand shock has arrived but before new supply has materially entered the market.

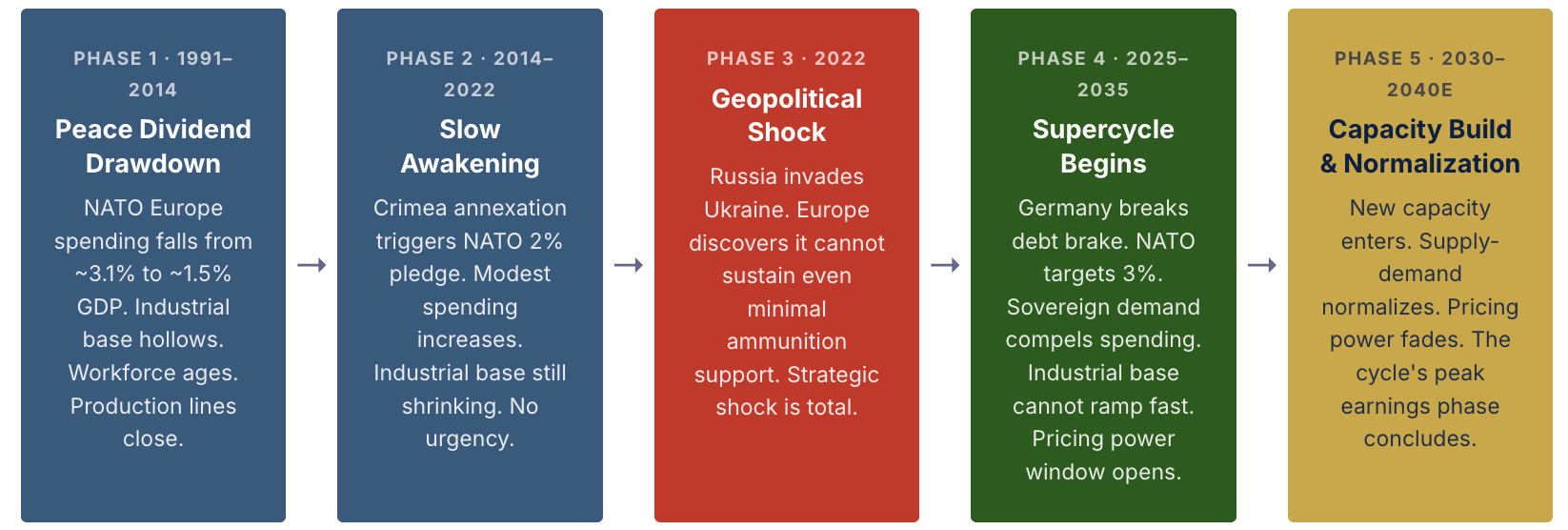

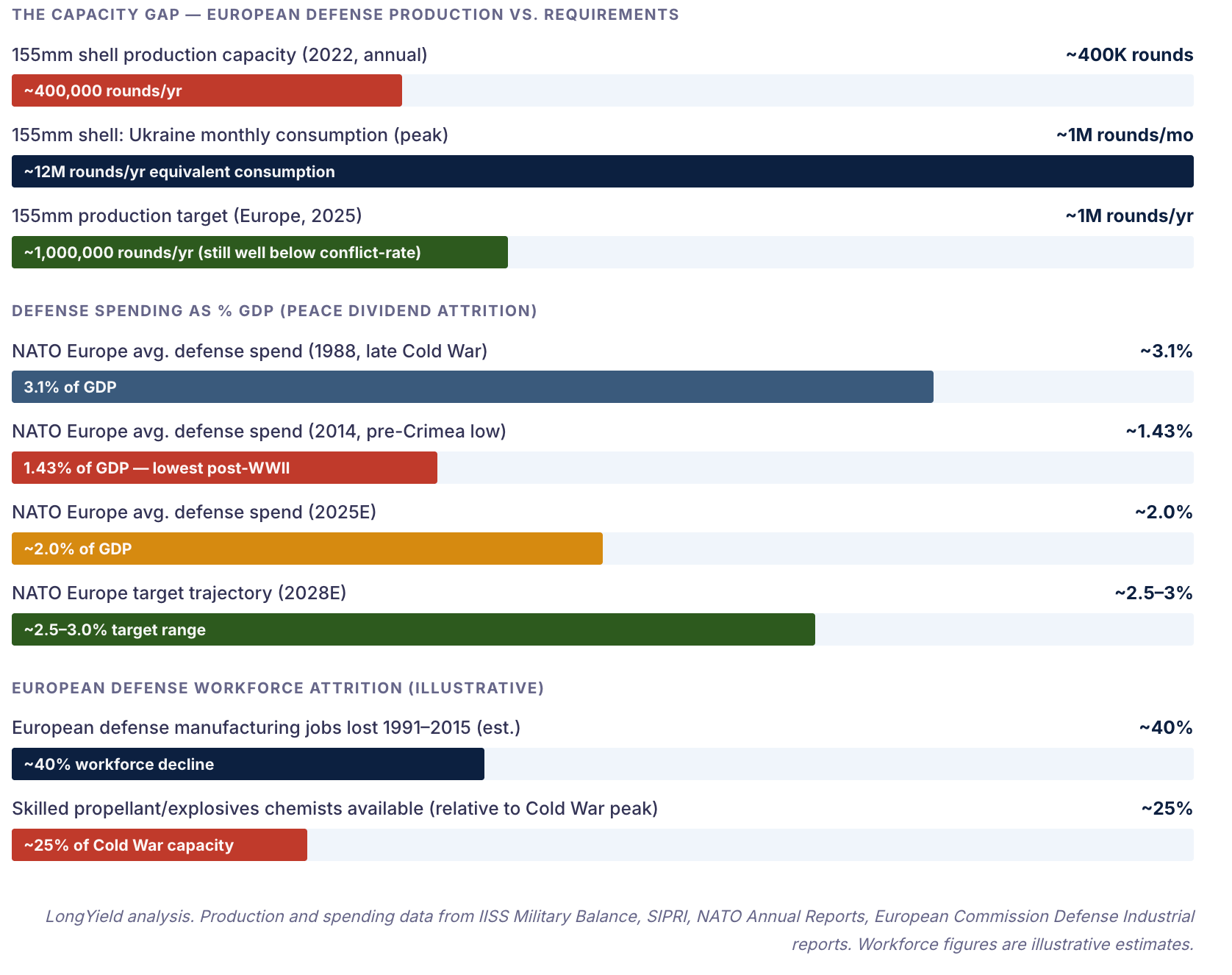

European defense is in the early recovery phase of one of the longest capital cycle drawdowns on record. The “peace dividend” — the reduction in Western defense spending following the Cold War’s end in 1991 — was not a one-year adjustment. It was a 30-year sustained withdrawal of capital from the defense industrial base. NATO’s European members collectively reduced defense spending from an average of approximately 3.1% of GDP in the late Cold War period to approximately 1.5% of GDP by the mid-2010s. Several major members fell below 1.2%.

The consequences for the industrial base were severe and largely invisible during the years they accumulated. Defense contractors consolidated, shrank their workforces, reduced R&D investment, and allowed production lines to atrophy or close entirely. The skilled artisan workforce — the welders, machinists, propellant chemists, naval architects, and systems integrators who build complex weapons systems — aged out without being replaced. Supply chains for defense-specific components became single-sourced, fragile, and geographically concentrated in ways that were acceptable in peacetime but are structurally inadequate in a remilitarizing world.

The current cycle differs from prior post-Cold War defense spending bumps in one decisive way: the political compulsion is durable. Post-9/11 defense spending surged and then normalized as the sense of crisis faded. The European rearmament of 2025–2035 is different because the threat is permanent and geographically proximate. Russia has demonstrated both the will and the capacity to conduct large-scale conventional warfare on European soil. That reality does not go away if a ceasefire is reached in Ukraine. It shapes European security planning for a generation.

The additional accelerant — the Trump administration’s explicit skepticism about NATO’s value and its public pressure on European countries to provide for their own defense — is not the cause of the supercycle but has removed the final political obstacle to spending. European governments that might have slowed their rearmament in the absence of US pressure have instead accelerated, because the political cost of under-investing in defense has become higher than the political cost of borrowing to pay for it.

“Europe did not merely spend less on defense after the Cold War. It systematically dismantled the industrial, human, and organizational capacity to defend itself — and then spent 30 years pretending that the infrastructure of the peace was also the infrastructure of the future. It was not. Rebuilding what was lost will take at least as long as it took to lose it.”

Section II

The Scale of the Fiscal Commitment: Germany Changes Everything

To understand the magnitude of what has happened, it is worth dwelling on Germany’s fiscal shift in specific terms — because its scale and institutional significance exceed most investor’s mental model of a “spending increase.”

Germany’s Schuldenbremse, enshrined in Article 109 of the Basic Law, limited structural federal borrowing to 0.35% of GDP annually — the strictest constitutional debt constraint of any major economy in the world. It was passed in 2009 in response to the financial crisis and reflected a deep cultural consensus in Germany around fiscal rectitude. The constraint was not merely a policy preference. It was constitutional law, requiring a supermajority of the Bundestag to modify.

When the incoming German government in early 2025 passed a constitutional amendment creating a €500 billion special fund (Sondervermögen) for infrastructure, defense, and climate investment — exempt from the debt brake — it was not a routine budget decision. It was a seismic institutional shift, equivalent in German political terms to the US suspending the debt ceiling permanently and creating a multi-trillion dollar off-balance-sheet vehicle for specific investment priorities. The vote required and received a two-thirds supermajority. Germany had collectively decided that security trumped austerity.

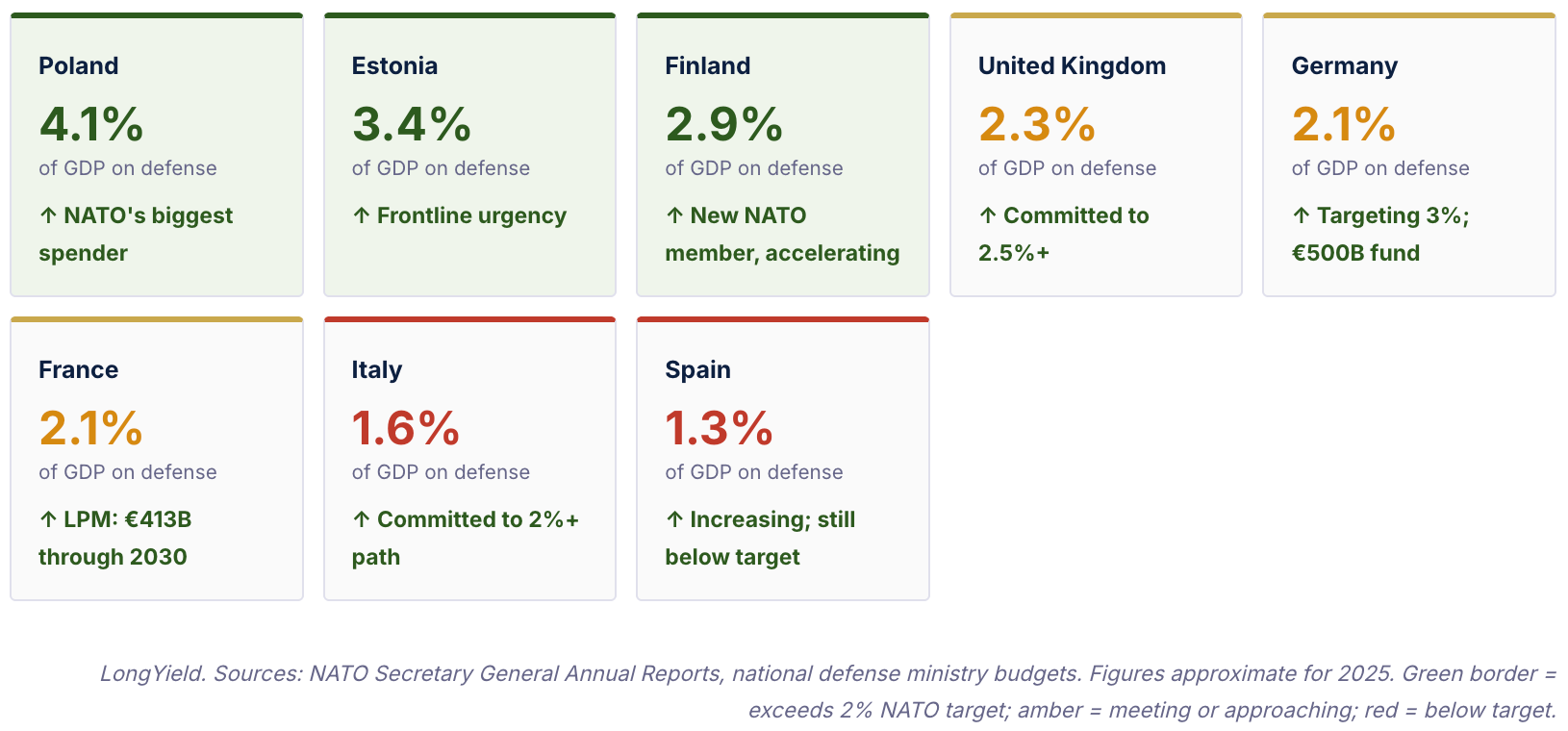

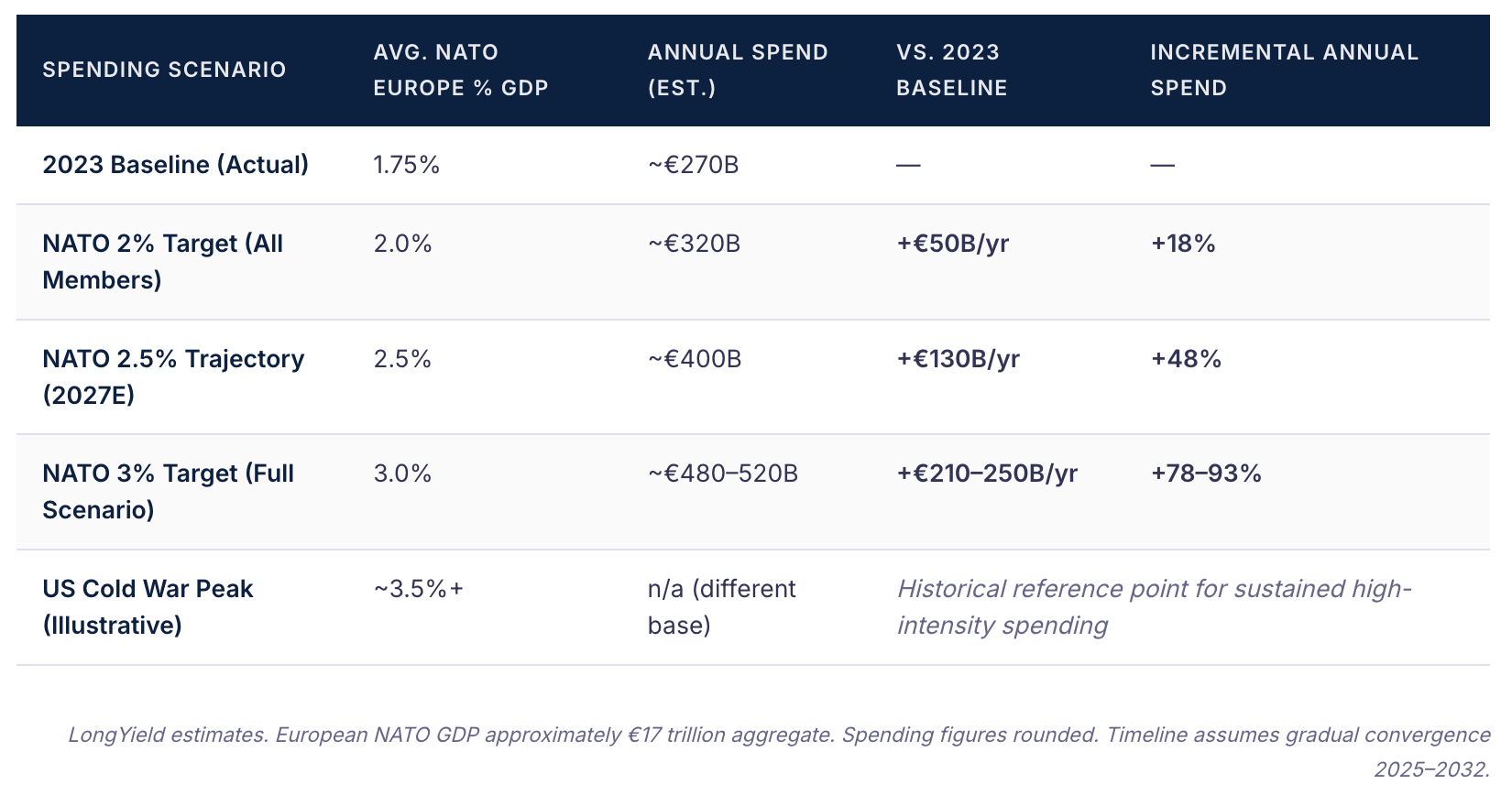

Of the €500 billion package, approximately €100 billion is specifically earmarked for defense over the coming years — in addition to Germany’s base defense budget, which is separately being raised toward 3% of GDP. Combined, Germany alone will spend approximately €85–100 billion per year on defense within the next few years, up from roughly €52 billion in 2023. That is an annual increase of approximately €35–50 billion — from a single country. The ripple effects across the European defense industrial complex are extraordinary.

The aggregate numbers across NATO's European members are striking. If all European NATO members reach 3% of GDP defense spending — now the emerging baseline expectation rather than an aspirational target — total annual European defense spending increases from approximately €270 billion in 2023 to approximately €520 billion per year. That is an incremental €250 billion per year of sovereign defense demand, sustained over a decade or more. For context, the entire annual revenue of Europe's top five defense contractors combined is approximately €120 billion. The demand pipeline is structurally larger than the current industrial base can serve.

Section III

The Industrial Gap: What Four Decades of Disinvestment Actually Destroyed

The gap between what Europe needs and what its defense industrial base can currently produce is not a management problem or a procurement problem. It is a structural consequence of four decades of systematic disinvestment, and it cannot be closed by writing larger checks alone. Understanding what was lost — and how long it takes to rebuild — is the most important input to timing the investment thesis and understanding which companies face the most attractive supply-demand dynamics.

The Ukraine conflict served as the most brutal stress test of European defense industrial capacity in the post-Cold War era. When European governments committed to providing 155mm artillery ammunition to Ukraine — a commitment that seemed straightforward in political terms — they discovered that the entire European defense industrial base could produce approximately 300,000–400,000 rounds per year. Ukraine was consuming approximately one million rounds per month. The gap was not a rounding error. It was a fundamental mismatch between the demand of a high-intensity conventional conflict and the residual capacity of an industrial base designed for the peace dividend era.

The shell shortage was the most visible symptom of a much deeper problem. European navies have fewer vessels than their strategic requirements suggest, and the shipyards that could build more have reduced capacity and skilled workforce. European air forces operate aging fleets in need of replacement, and the manufacturing capacity for fighter aircraft is constrained by bottlenecks in engines, avionics, and composites. European ground forces have tank parks that are smaller than their Cold War predecessors, with readiness rates that reflect years of reduced maintenance budgets.

Why the Gap Cannot Be Closed Quickly: Building a propellant chemistry facility takes 3–5 years from decision to production. Training a skilled naval architect or munitions engineer takes 5–10 years. Qualifying a new supplier in the defense supply chain — particularly for safety-critical components — involves testing and certification cycles measured in years. The institutional knowledge that was allowed to atrophy over 30 years cannot be recreated by adding budget lines. This is precisely the condition that makes the early phase of a capital cycle so valuable to investors: the pricing power window is open while new supply cannot yet enter. For European defense, that window is measured in years, not quarters.

Section IV

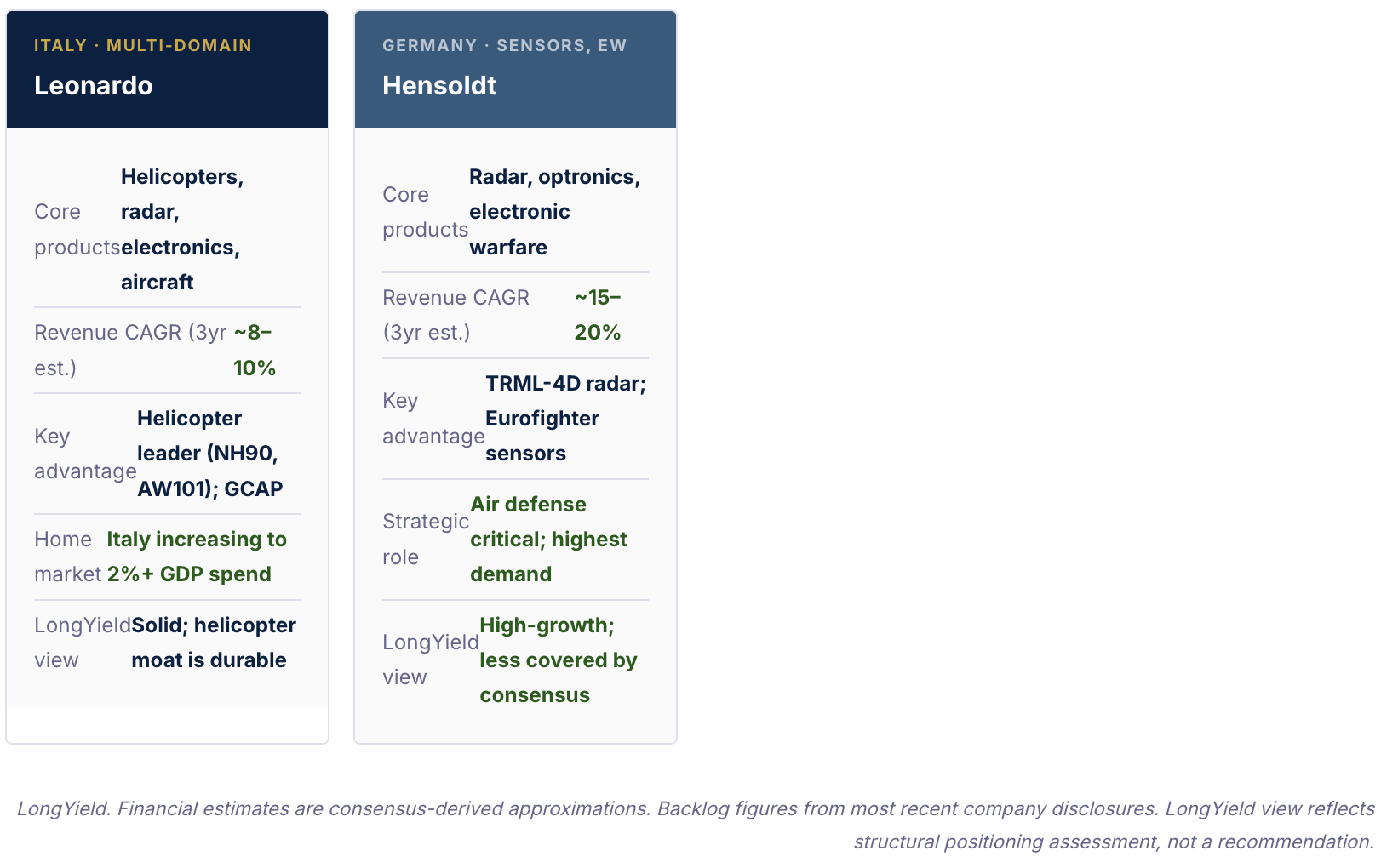

The Beneficiaries: Mapping the European Defense Industrial Complex

European defense is not a monolithic sector. Understanding which companies benefit, in which segments, and over what timeline requires mapping the industrial structure carefully. We organize the beneficiaries by segment, identifying the key players, their current positioning, and the specific demand tailwinds they face.

Section V

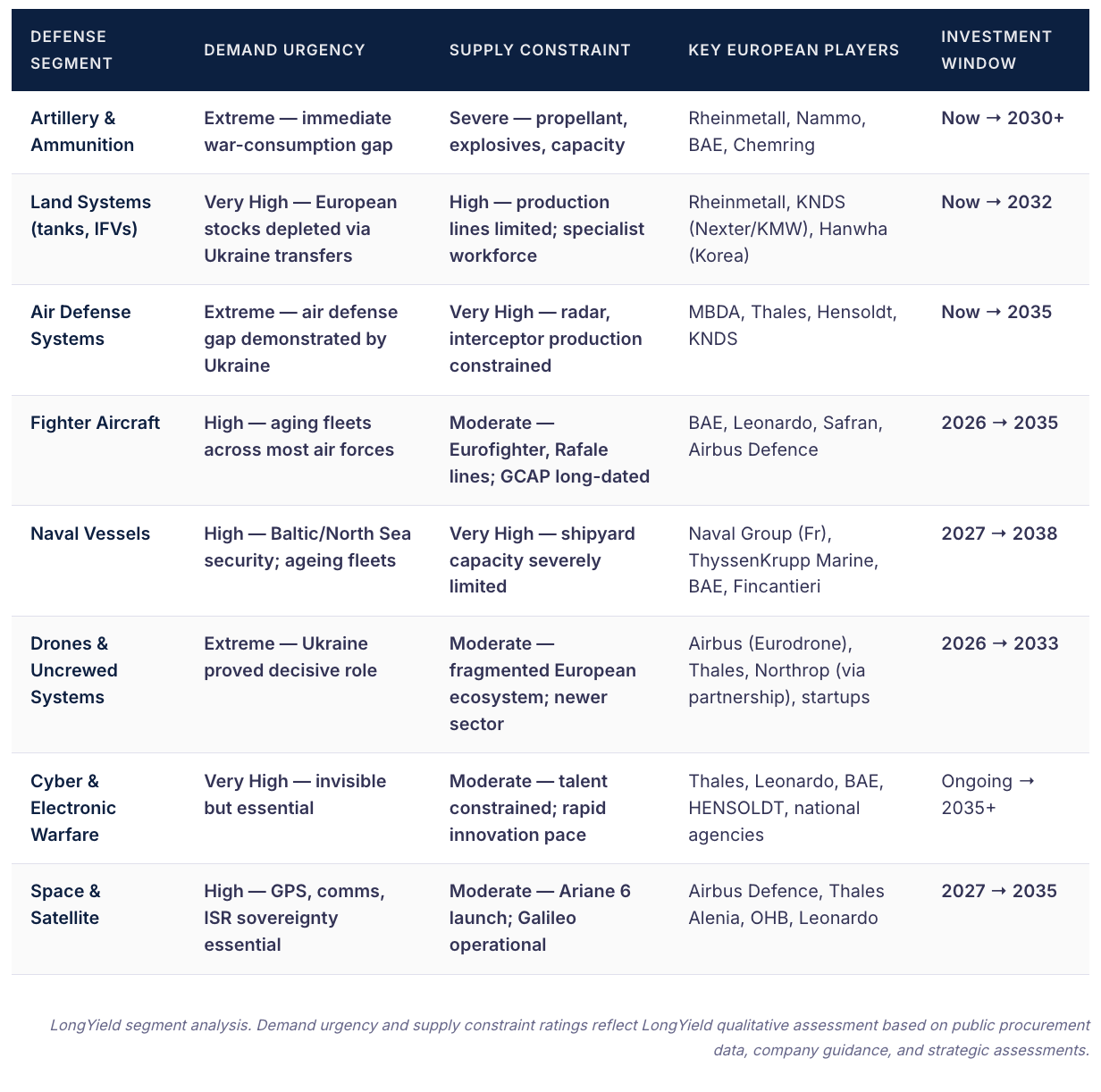

The Bottleneck Problem: Where the Constraint Actually Lives

In a capital cycle, the companies that benefit most from a demand shock are not necessarily the most visible or the most discussed. They are the companies that sit closest to the binding constraint — the chokepoint in the supply chain that limits how fast everyone above and below them can grow. Identifying where the constraint lives in the European defense industrial base is the most important analytical task for investors who want to be early in the right place

The Investment Implication of Bottleneck Analysis: The companies sitting closest to the hardest physical constraints — propellant chemistry, forging capacity, naval workforce — have the most pricing power for the longest duration. Nammo (joint Norwegian-Finnish propellant/ammunition company, not publicly listed but indicative of the segment), Chemring (UK-listed, propellant and countermeasures), and the ammunition businesses of Rheinmetall and BAE sit closest to the hardest constraints. In a capital cycle, the companies that own the bottleneck earn above-normal returns for the entire duration of the bottleneck — and the bottleneck in propellants and shell forging will not clear for 5–8 years from first serious investment. That is the pricing power window.

Section VI

The US Factor: Accelerant, Not Cause

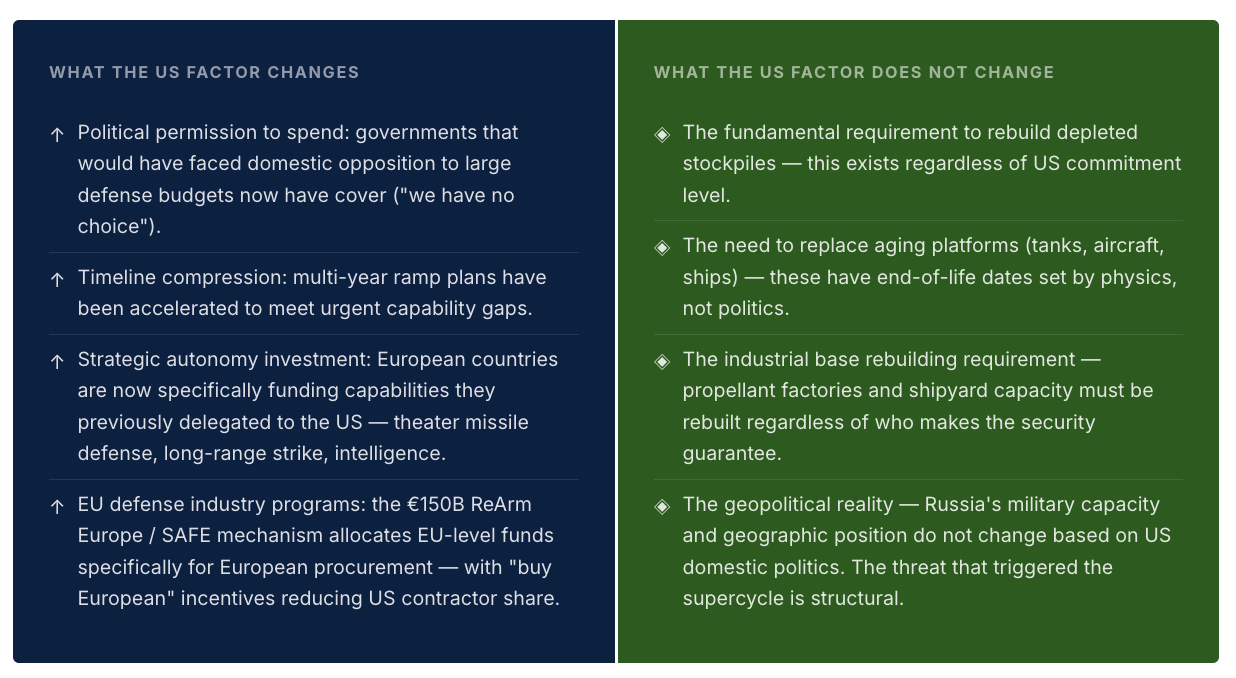

No analysis of the European defense supercycle in early 2026 can ignore the role of the United States — specifically, the Trump administration’s explicit questioning of the US commitment to NATO and its demands for European countries to dramatically increase their own defense contributions. The Munich Security Conference of February 2025, at which US officials made clear that the US would not automatically defend NATO allies who had not met spending targets, was a crystallizing moment for European strategic thinking.

The analytical point, however, is this: the US factor is an accelerant of a cycle that was already structurally inevitable, not the cause of it. Even in a world where the US committed fully and warmly to NATO indefinitely, Europe would still need to recapitalize its defense industrial base, rebuild its stockpiles, and modernize its platforms — because Russia’s 2022 invasion demonstrated that the geopolitical threat environment had changed permanently. The US political pressure has compressed the timeline and removed the political cover for European governments that might have preferred to defer the spending. It has made the supercycle start sooner and move faster. It has not created the supercycle.

The “buy European” dimension deserves specific attention. The EU’s ReArm Europe initiative — a €150 billion loan facility and series of incentives for joint European procurement launched in 2025 — explicitly favors European-sourced defense equipment. This is a structural headwind for US defense contractors seeking to sell into the European market, and a structural tailwind for European incumbents. Companies like Rheinmetall, Leonardo, and Thales are positioned to benefit not just from higher total European spending but from a higher European share of that spending — a double-layered tailwind that makes the earnings growth case more durable than it would be if European countries simply bought American equipment.

Section VII

Valuation: Has the Market Priced the Supercycle?

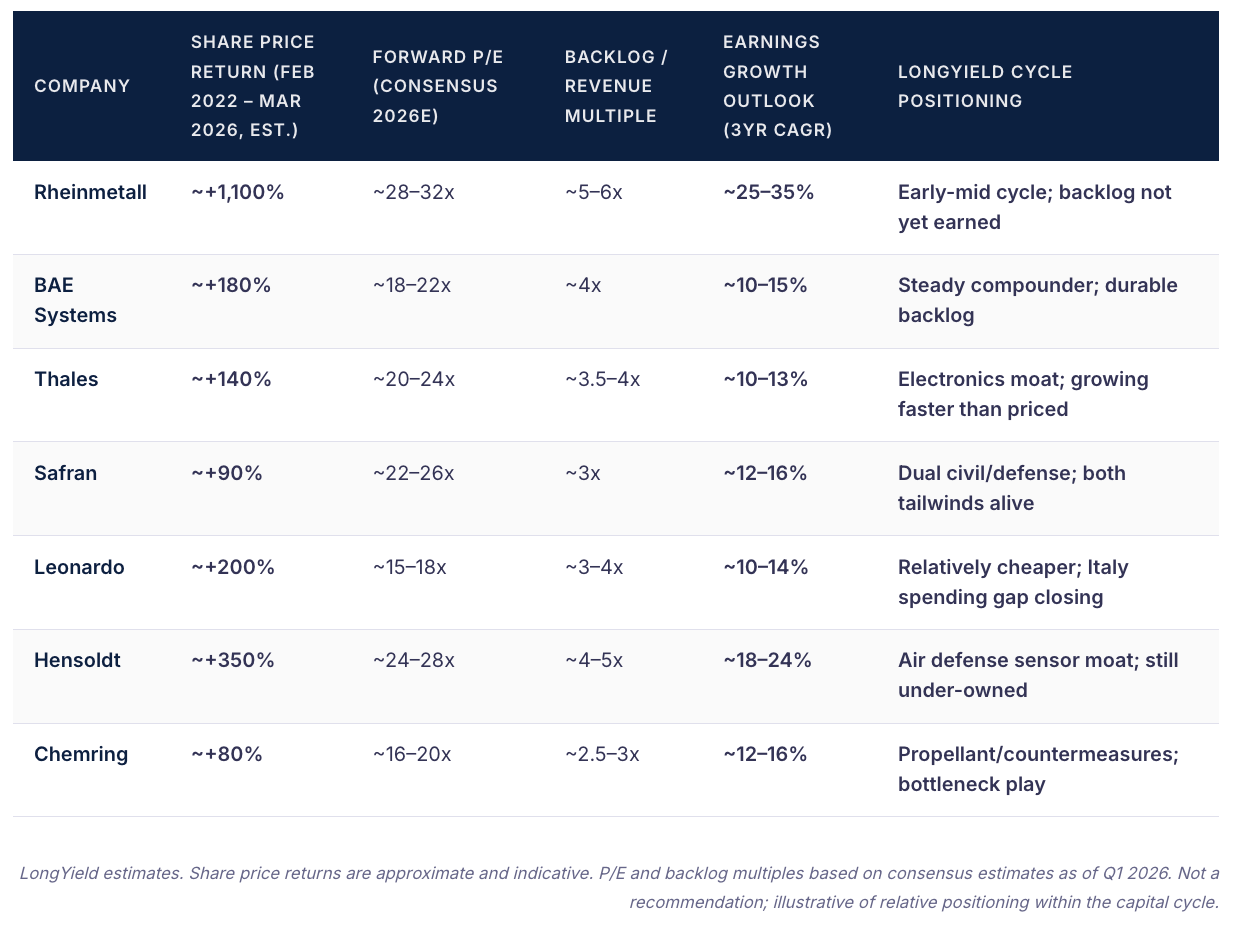

The honest answer is: partially, but not fully, and not uniformly. European defense stocks have been among the best-performing equity sectors since Russia’s February 2022 invasion. Rheinmetall’s share price increased more than 10-fold between early 2022 and early 2026. BAE Systems, Thales, Leonardo, and Safran have all seen significant re-ratings. For investors who positioned in 2022 or 2023, the thesis has already delivered extraordinary returns.

The question for new investors is whether meaningful upside remains — and the answer requires separating the valuation of the companies from the valuation of the cycle. The stocks have re-rated. The earnings have not yet fully reflected the spending that has been committed. Order backlogs at European defense majors are at record levels — in many cases, 5–8 years of current revenues. Those backlogs are priced at the front-end of the earning curve; the outyear earnings from orders placed today have not yet flowed through income statements.

The Valuation Framework for Capital Cycle Stocks: Traditional P/E analysis systematically undervalues companies in early-mid capital cycle recovery because it discounts near-term earnings — which are still depressed relative to the backlog commitment — while underestimating the duration and trajectory of the earnings ramp. The correct framework is backlog-based: a company with €50 billion of backlog and €7 billion of annual revenues will deliver those revenues over 7 years, with operating leverage expanding margins as the fixed cost base spreads over higher output. The resulting earnings trajectory is far steeper than any single-year P/E captures. Investors who refused to pay 25x earnings for Rheinmetall in 2023 because it “looked expensive” missed one of the most profitable trades in European equity history. The lesson: cycle-aware valuation, not static multiples.

Section VIII

Three Scenarios for the European Defense Supercycle

We weight these scenarios approximately 35% / 50% / 15% — placing the base case as most likely while assigning meaningful probability to the full bull case, which has strengthened since Germany’s debt brake suspension. The bear case is the lowest probability because it requires a simultaneous reversal of multiple independent geopolitical variables, including a credible and sustained Russian de-escalation and a reversal of the domestic political consensus that has formed in Germany, Poland, and the Nordic countries around defense investment. The direction of the structural forces is clear; the pace is the variable.

In the bear case, it is important to note that even modest spending increases — stopping at 2% rather than moving to 3% — still represent a multi-decade demand uplift relative to the industrial base that was dimensioned for 1.5% spending. Even in the bear case, European defense companies grow meaningfully. The bear case is a slower, lower-amplitude supercycle — not an absence of one.

Section IX

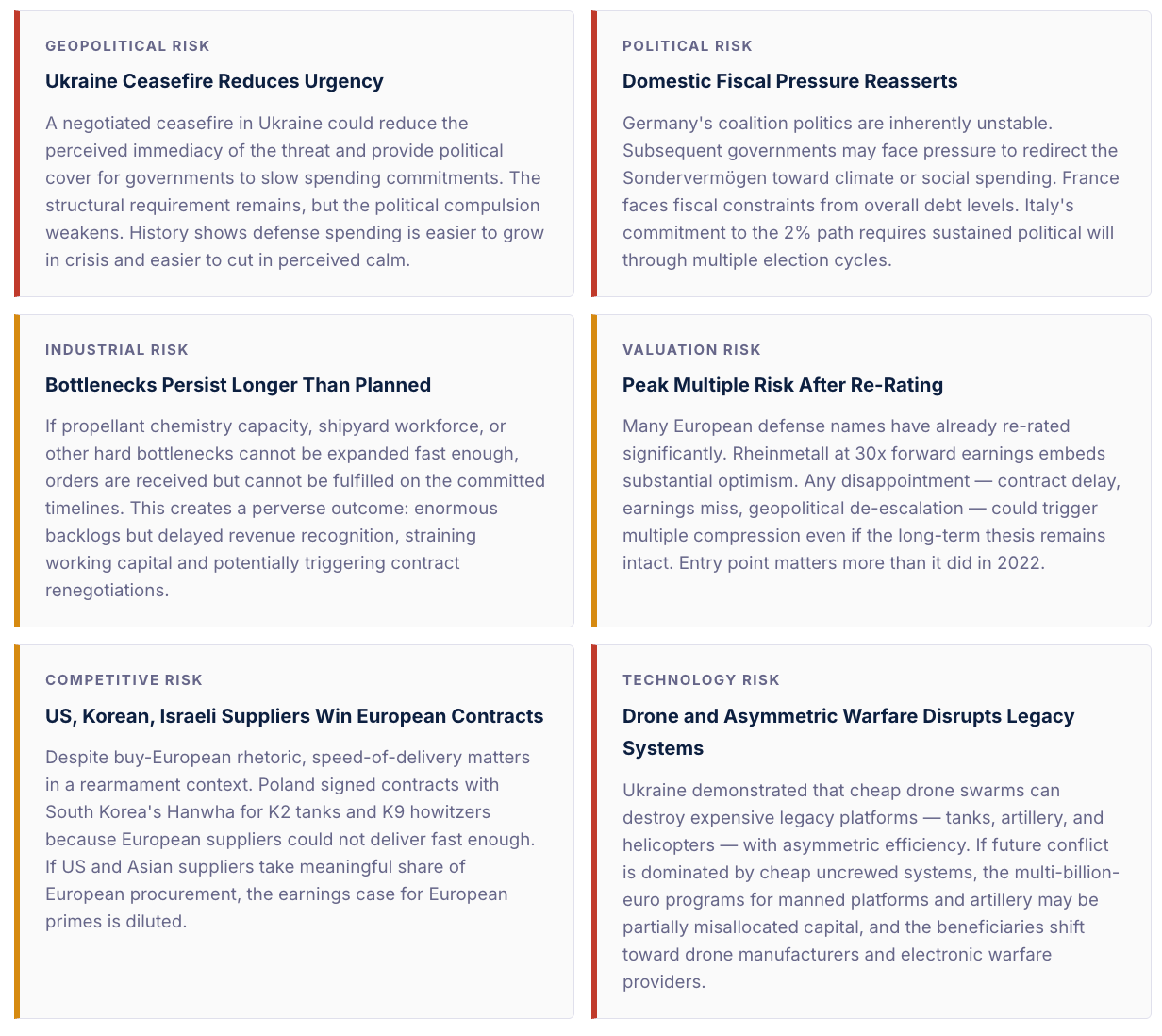

Risks to the Thesis

Section X

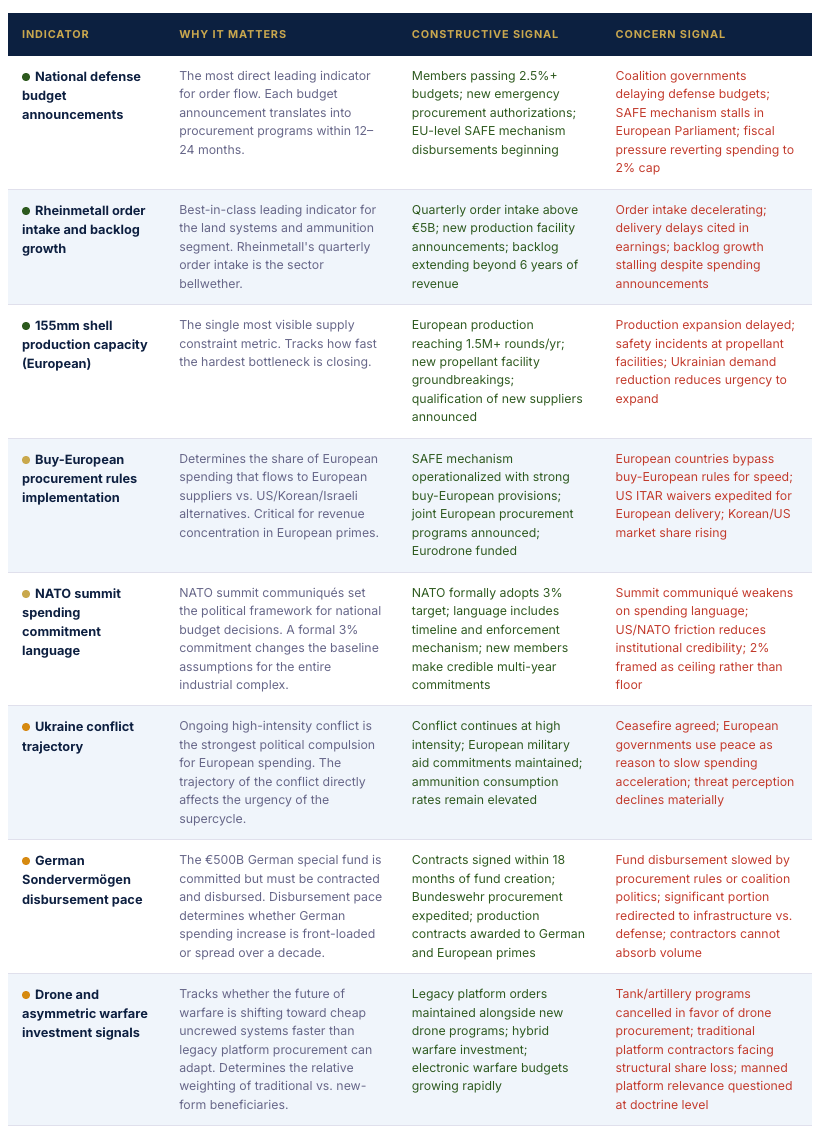

What Investors Should Watch

Conclusion

The Peace Dividend Is Over. The Bill Has Arrived.

For 30 years, Europe ran a security subsidy from the United States and a threat subsidy from the post-Cold War peace. Both are now withdrawn — one by geopolitical reality and one by political choice. The combination has created the most compelling capital cycle opportunity in the European equity market in a generation: sovereign demand that is politically compelled and legally committed, industrial supply that cannot ramp quickly enough to meet it, and a pricing power window that will remain open for years while new capacity is painfully rebuilt from the ground up.

The companies that sit closest to the hard physical constraints — artillery and ammunition at Rheinmetall and Chemring, sensors and air defense electronics at Thales and Hensoldt, naval systems at BAE — will generate above-normal returns for the duration of those constraints. The broader set of European defense primes will benefit from the tailwind for a decade or more, as order backlogs are earned through income statements and the industrial base laboriously rebuilds the workforce and facilities that the peace dividend dismantled.

The risk for investors is not that the supercycle will not happen. It is already happening. The order books, the budget commitments, and the geopolitical compulsion are all in place. The risk is valuation timing: many of the most obvious beneficiaries have already re-rated significantly, and investors who missed the 2022–2024 entry window will need to be more selective and more patient about valuation. The cycle is real and durable. The most attractive entry points may now be the less-covered names — the bottleneck plays in ammunition components, the emerging drone ecosystem, and the electronic warfare companies — rather than the large primes whose stories are now broadly understood.

Europe is rearming. The capital cycle framework tells us that industrial supply cannot follow sovereign demand quickly. The gap between demand and supply is where pricing power — and returns — live. That gap, in European defense, will not close for a decade. The only real question is who captures the value it creates.

The Single Most Important Framing: Do not analyze European defense as a political story — “will governments keep spending?” The political commitment is as locked-in as any in modern European history. Analyze it as a capital cycle. The binding constraint is industrial capacity, not political will. The companies that can actually deliver — the ones with the facilities, the workforce, the supply chains, and the regulatory qualifications — are the ones that will earn the returns. The defense ministry is writing the checks. The question is who can cash them. That question, mapped carefully, is one of the most tractable and high-quality investment problems available in European equity today.