The Retirement Contract Is Breaking

How the U.S. and Europe Are Quietly Repricing Old Age

Executive Summary

The retirement systems of the United States and Europe are not collapsing. They are being repriced. Across the advanced economies, the implicit postwar contract — decades of work exchanged for predictable, adequate retirement income at a socially accepted age — is being quietly renegotiated through later retirement ages, weaker replacement rates, greater dependence on private savings and housing wealth, and a systematic transfer of risk from institutions to households.

This repricing is not sudden. It is the compound effect of demographic aging, fiscal constraint, the decline of defined-benefit pensions, inadequate private savings, and political unwillingness to choose between explicit benefit cuts and the tax increases needed to preserve current promises. The result is not a dramatic failure but a slow compression: retirement still exists, but it is shorter, less generous, more uncertain, and far more unequal than the systems were designed to deliver.

This article examines the structural pressures reshaping retirement in the U.S. and Europe, the distributional consequences of the repricing, the role of housing as a de facto pension asset, the political economy of retirement-age reform, and the market and macro implications for investors and policymakers. The central finding is that the retirement crisis is best understood not as a story of collapse, but as one of compression — and it is already well under way.

01

The U.S. Social Security trust fund faces depletion by 2033–2034, implying a 19–23% automatic benefit reduction absent legislative action — but the deeper problem is inadequate private savings alongside this public-pillar stress.

02

European pension systems spend 12–16% of GDP on public pensions, but aging demographics will push the old-age dependency ratio above 55% by 2050, threatening adequacy even where solvency is managed.

03

Retirement is being repriced through slower benefit growth, inflation-eroded purchasing power, rising retirement ages, and means testing — mechanisms that avoid the political cost of explicit nominal cuts.

04

Housing has become a de facto pension asset, but it is illiquid, regionally variable, and profoundly unequal: 58% of elderly renters are cost-burdened, while homeowners hold median equity of $250,000.

05

The retirement crisis is fundamentally a distributional story. Low earners, renters, women, workers in physically demanding jobs, and late savers face a qualitatively different old age than asset-rich professionals.

06

Investors should watch insurers, annuity providers, senior housing, and healthcare as structural beneficiaries — while monitoring fiscal stress indicators and retirement-age politics as macro risk signals.

SECTION I

The Retirement Contract Is Breaking

For most of the postwar period, retirement in the advanced economies operated as an implicit social contract. Workers contributed decades of labor. In return, they could expect to exit the workforce at a recognized age — typically between 60 and 65 — and receive a combination of public benefits, employer-backed pensions, and personal savings sufficient to maintain a reasonable standard of living until death. The system was not perfect, but the bargain was broadly understood and broadly honored.

That contract is now being renegotiated — not in a single dramatic act, but through a long sequence of incremental adjustments that, taken together, amount to a fundamental repricing of old age. Statutory retirement ages are rising. Replacement rates — the share of pre-retirement income that pension systems deliver — are weakening in real terms. The shift from defined-benefit to defined-contribution pensions has transferred investment and longevity risk from employers and governments to individual households. Housing wealth has become an unofficial fourth pillar of retirement, but one that is illiquid, unequal, and regionally fragile. And across the income distribution, the gap between those who can afford a comfortable retirement and those who cannot is widening.

The central argument of this analysis is that the retirement crisis in the United States and Europe is not best understood as a sudden failure or a looming collapse. It is better described as a gradual compression: retirement still exists, but it begins later, delivers less, costs more in private effort, and is far more unequal than the postwar model promised. The drivers of this compression are structural — demographics, fiscal arithmetic, savings inadequacy, and political constraint — and they are already reshaping household behavior, labor markets, asset allocation, and sovereign fiscal trajectories across the West.

The central question: Is the retirement crisis in the U.S. and Europe better understood as a gradual reduction in the generosity and certainty of retirement — a repricing — rather than a binary collapse of the systems that underpin it?

SECTION II

The U.S. Model: Social Security, 401(k)s, and the Risk Shift to Households

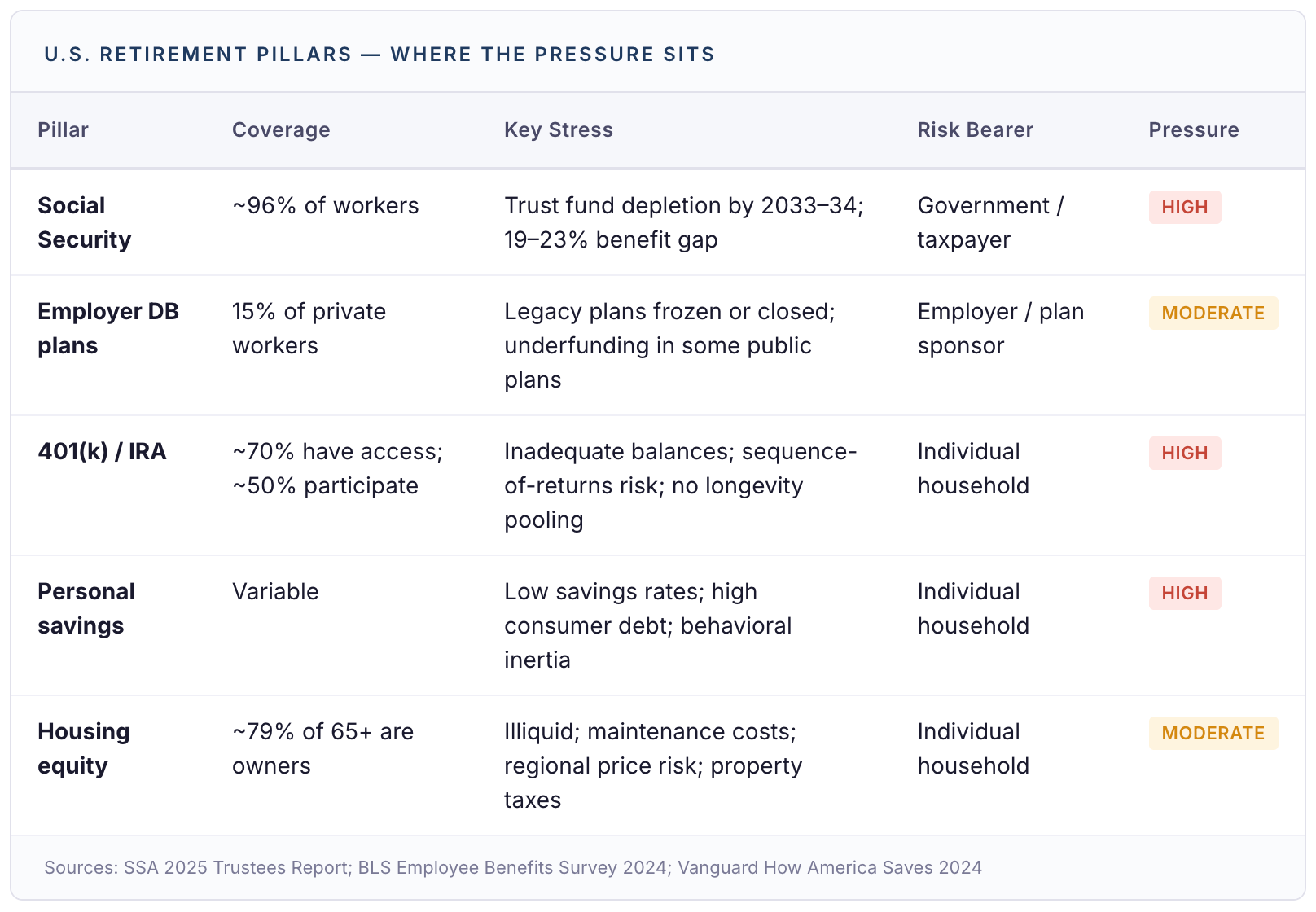

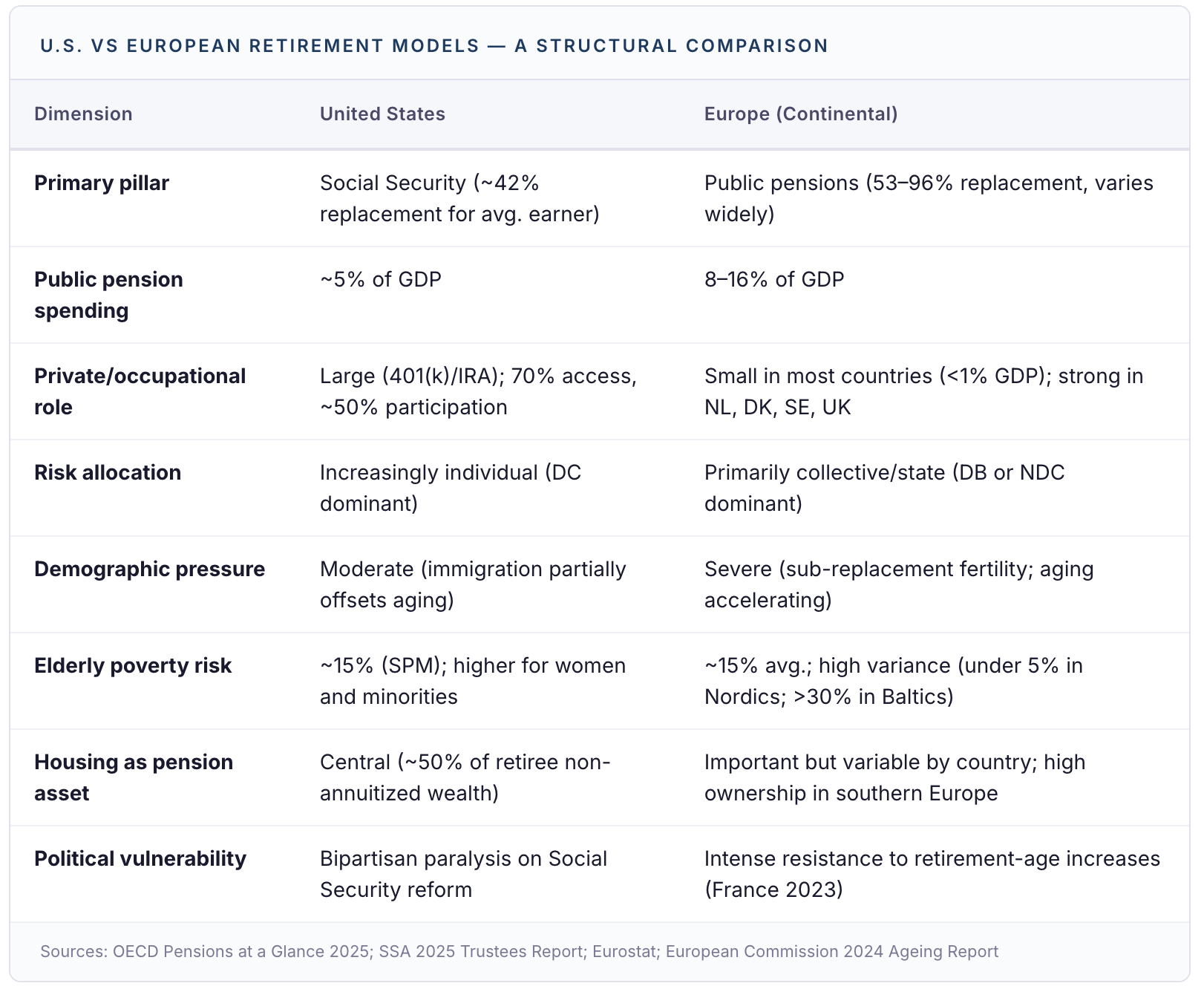

The American retirement system rests on three pillars: Social Security, employer-sponsored retirement plans, and personal savings. In theory, this produces a diversified income base. In practice, the first pillar is under demographic strain, the second has been fundamentally restructured in ways that shift risk to households, and the third is woefully inadequate for most of the population.

Social Security remains the single most important source of retirement income in the United States. Roughly 67% of seniors depend on it for more than half their income, and 27% rely on it almost entirely. The program’s finances, however, are on an unsustainable trajectory. The 2025 Trustees Report projects that the Old-Age and Survivors Insurance trust fund will be depleted by 2033. At that point, incoming payroll tax revenue would cover only 77% of scheduled benefits — implying an automatic 23% cut absent legislative intervention. The combined OASDI trust funds face depletion by 2034, with payable benefits falling to 81% of scheduled levels.

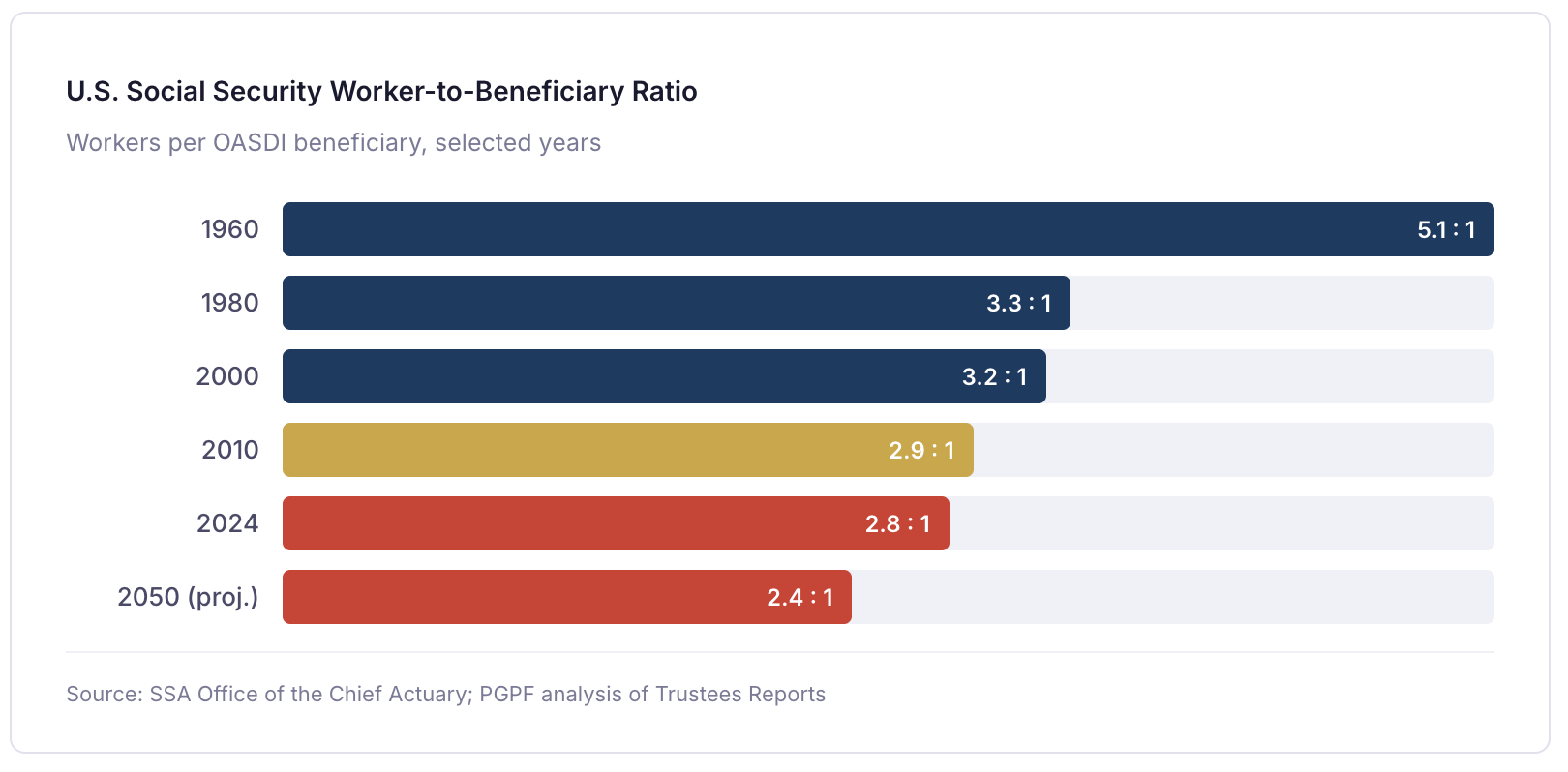

The demographic pressure is straightforward: the worker-to-beneficiary ratio has fallen from 5.1:1 in 1960 to 2.8:1 today, and it will continue to decline as the baby-boom generation ages through the system and life expectancy extends the payout period. The system was designed for a younger, faster-growing population. It now operates in a society that is older, longer-lived, and growing more slowly.

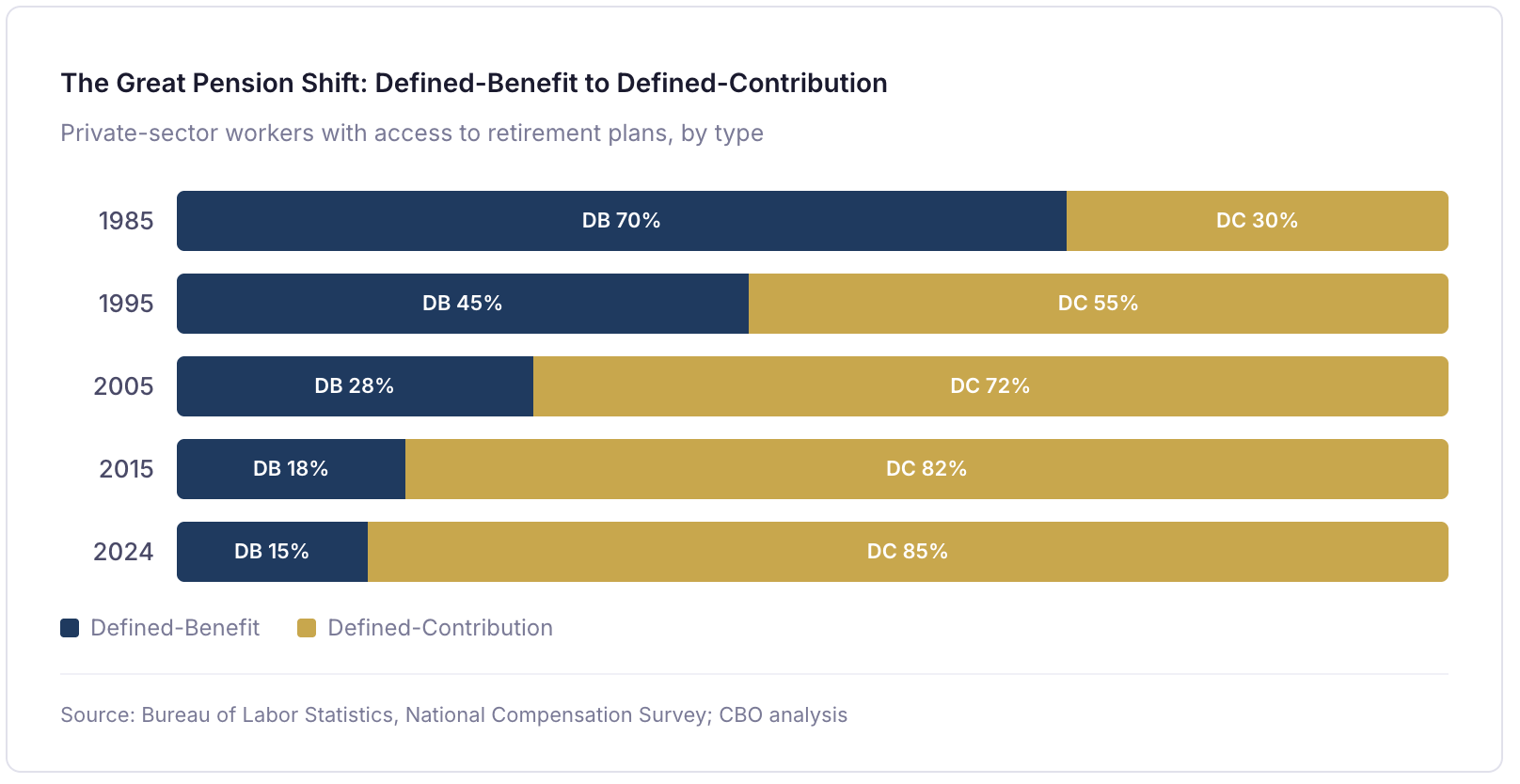

But the Social Security problem is only one dimension of the American retirement challenge. The second — and arguably more consequential — transformation has been the wholesale shift from defined-benefit to defined-contribution retirement plans. In the early 1980s, the majority of private-sector workers with retirement coverage had access to a traditional pension that guaranteed a specified monthly benefit for life. Today, only 15% of private-sector workers have access to a defined-benefit plan. The dominant vehicle is now the 401(k), a defined-contribution structure that places investment risk, longevity risk, and withdrawal-sequencing risk squarely on the individual participant.

The results of this shift are visible in household balance sheets. The median 401(k) balance for workers aged 55–64 — the cohort nearest to retirement — is approximately $72,000, according to Vanguard’s most recent data. Even the average balance for this group, inflated by high-balance accounts, sits at roughly $178,000. These figures are starkly insufficient to replace even a modest share of pre-retirement income over a 20-to-25-year retirement horizon. Meanwhile, nearly 30% of private-sector workers have no access to an employer-sponsored retirement plan at all, and among those who do, participation rates remain uneven — particularly among lower-wage workers and those in smaller firms.

Why the U.S. Retirement Crisis Is Not Just a Social Security Problem

The political debate around American retirement tends to focus on Social Security solvency. But the deeper structural problem is the interaction between a weakening public pillar and an inadequate private one. Social Security’s average replacement rate for a medium earner retiring at full retirement age is approximately 42.6% — well below the 70–80% replacement threshold most financial planners recommend. The 401(k) system was supposed to fill the gap. For most households, it has not. The median near-retiree household faces a retirement supported primarily by a Social Security benefit that may be cut by a fifth within a decade, supplemented by private savings that would generate only a few hundred dollars per month in sustainable income. Add the burden of healthcare costs — average out-of-pocket spending for Medicare beneficiaries exceeds $6,300 annually, and lifetime healthcare costs for a 65-year-old couple can exceed $395,000 — and the arithmetic becomes sobering.

SECTION III

The European Model: Public Pensions, Aging, and Adequacy Pressure

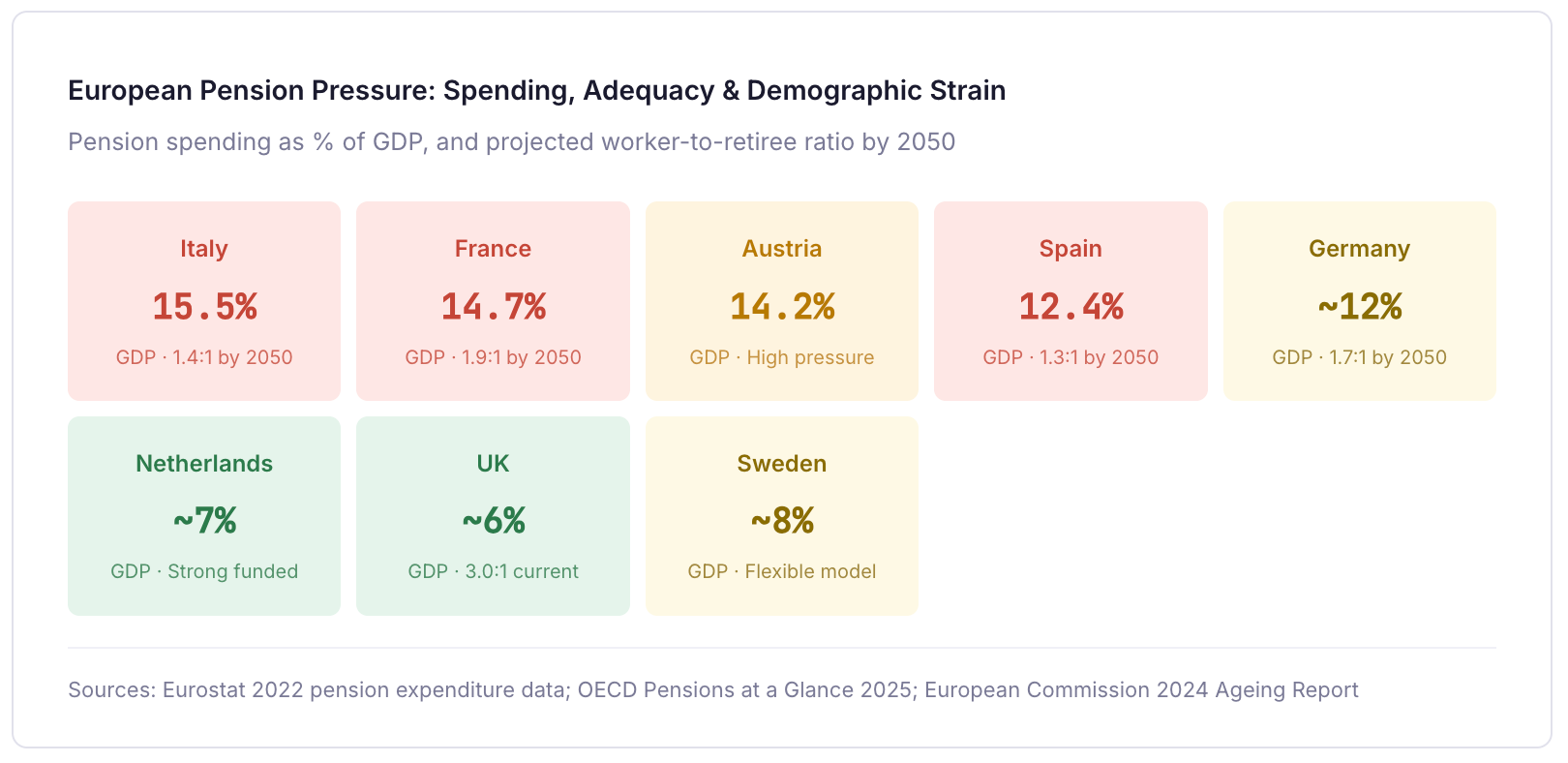

Europe’s retirement systems operate under a fundamentally different architecture than the American model. Public pensions play a far larger role, replacement rates are generally higher, and the state bears a greater share of retirement income provision. Italy, France, and Austria each spend more than 14% of GDP on public pensions — roughly double the OECD average of 8.1% — and several countries deliver net replacement rates above 80% for average earners. On the surface, Europe looks better protected against retirement insecurity than the United States.

But the European model faces its own acute pressure, driven primarily by demographics. The EU-27 old-age dependency ratio — the number of people aged 65 and over relative to the working-age population — stands at roughly 33% today. By 2050, it is projected to exceed 55%, meaning fewer than two workers for every retiree across the bloc. In Italy, already the oldest major economy in Europe, the worker-to-retiree ratio is expected to fall from 2.4:1 today to 1.4:1 by mid-century. Spain faces a similarly severe trajectory, with projections of just 1.3 workers per retiree by 2050.

The European Commission’s 2024 Ageing Report projects that EU-wide pension spending will rise only modestly — from 11.4% of GDP in 2022 to about 12.1% by 2045 — but this aggregate figure masks significant cross-country divergence and, critically, conceals the policy adjustments being made to hold spending stable. Countries are achieving fiscal sustainability not by maintaining the same level of generosity at higher cost, but by reducing generosity to hold costs roughly constant. Germany’s net replacement rate of 53.3% is already below the OECD average of 63.2%. The Netherlands achieves a 96% replacement rate, but relies heavily on funded occupational pensions that sit outside the public budget. Southern European systems face a particularly acute tension: high current spending, rapid aging, and limited funded private-pension alternatives.

The gender pension gap adds another dimension. Across the EU, women receive pensions that are on average 24.5% lower than those of men, reflecting lifetime earnings gaps, career interruptions for caregiving, and lower rates of occupational-pension coverage. In the Netherlands and Austria, the gender pension gap exceeds 35%.

Why Europe May Look Safer on Public Pensions but Still Face a Retirement Crisis

Europe’s advantage in public-pension coverage is real but narrower than it appears. The continent’s systems are being preserved partly by reducing what they promise: raising retirement ages, adjusting indexation formulas, and tightening eligibility. France’s politically explosive 2023 reform — which raised the minimum retirement age from 62 to 64 and was ultimately suspended in late 2025 — illustrates both the fiscal necessity and the political fragility of these adjustments. Meanwhile, private pension coverage in most continental European countries remains far weaker than in the Anglo-Saxon world, leaving households with limited alternative income sources if public-benefit adequacy declines.

SECTION IV

Why Retirement Is Being Repriced, Not Simply Cut

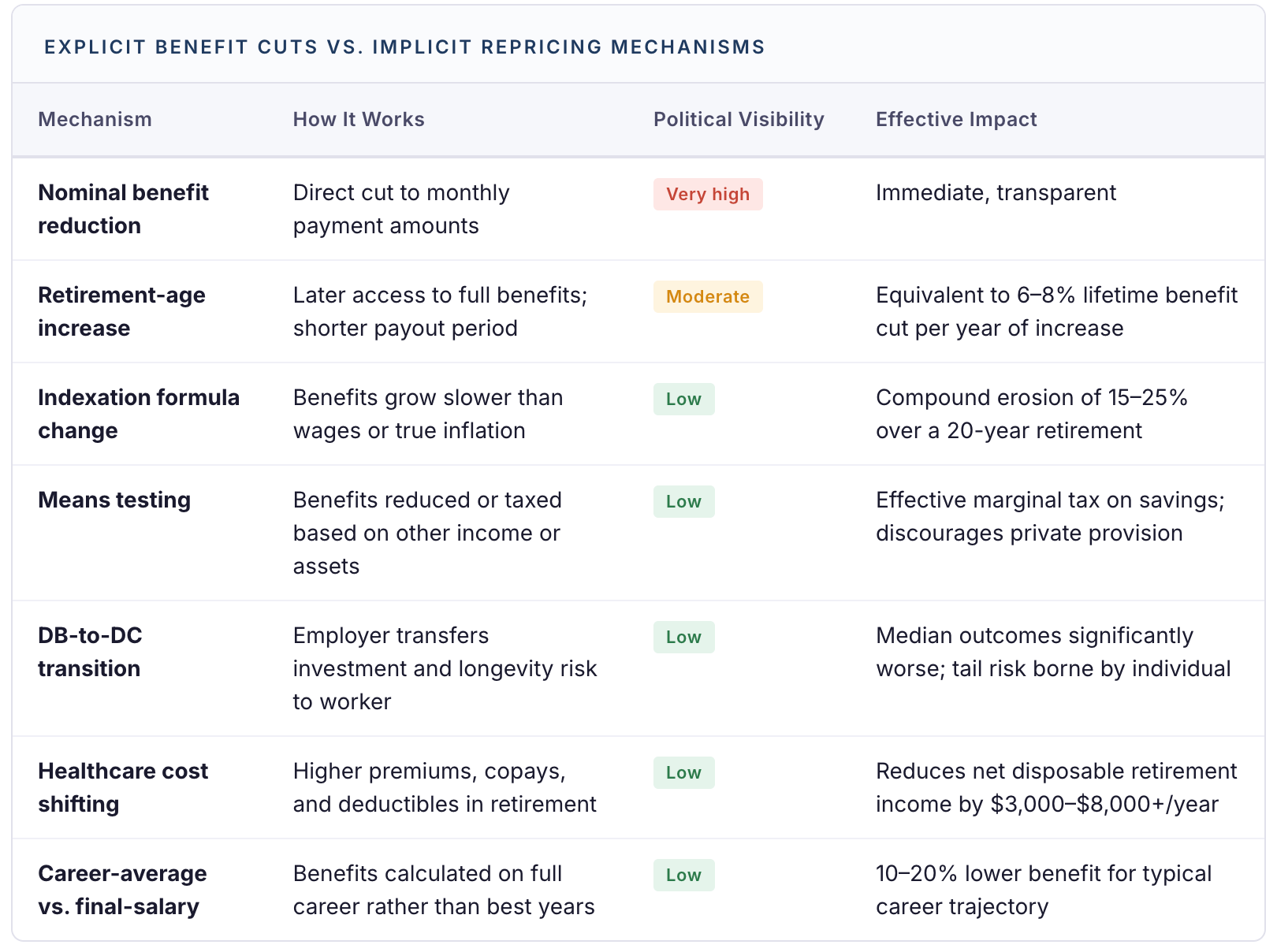

Governments rarely announce that retirement benefits are being reduced. The political costs are too high, the constituencies too large, and the backlash too immediate. Instead, the repricing of retirement happens through mechanisms that are technically distinct from nominal benefit cuts but produce functionally similar outcomes: later access, lower real purchasing power, greater private burden, and more uncertain retirement timing.

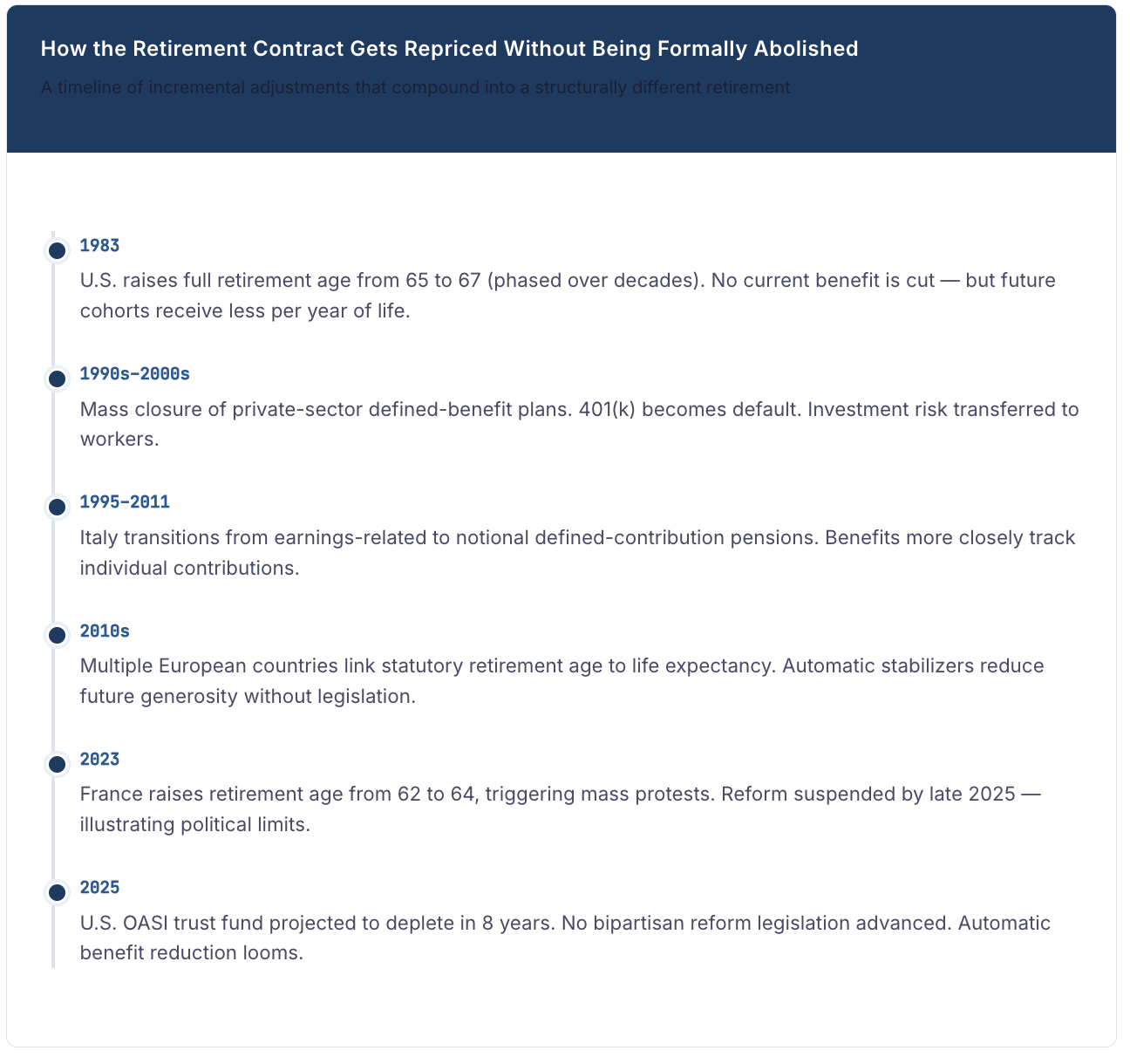

This distinction between explicit cuts and implicit repricing is central to understanding the current moment. In the United States, no Congress has voted to reduce Social Security benefits. But the full retirement age has been raised from 65 to 67 for those born after 1960 — a change that reduces the lifetime benefit for anyone who retires at the same age their parents did. Inflation-indexation formulas that lag actual cost-of-living increases erode purchasing power incrementally. Means testing of Medicare premiums introduces a wealth-dependent cost structure. The cumulative effect is a benefit that is nominally preserved but functionally diminished.

In Europe, the same logic operates through retirement-age linkages to life expectancy, adjustments to pension-indexation formulas, transitions from final-salary to career-average benefit calculations, and the shift from defined-benefit to notional defined-contribution accounting. Italy’s NDC reform, for example, preserves the structure of a public pension while tying the benefit more tightly to individual contributions — effectively making the pension less redistributive and more reflective of market earnings, which disadvantages workers with interrupted careers.

Why “You Can Still Retire” and “Retirement Is Unchanged” Are Not the Same Thing

The political narrative around retirement reform tends to emphasize continuity: the system is being modernized, not dismantled. But the lived experience of the repricing is material. A worker who must work two additional years to receive the same benefit has experienced a reduction in the retirement contract. A retiree whose benefit grows at CPI minus 0.5% loses purchasing power every year relative to the actual cost of housing, healthcare, and food. A household that must self-fund a $395,000 lifetime healthcare liability bears a burden that previous cohorts did not. The contract is formally intact; the substance has been thinned.

SECTION V

Who Gets Hit First: Renters, Low Earners, Women, and Late Savers

The repricing of retirement does not affect all households equally. It is, at its core, a distributional phenomenon. Wealthier households with diversified assets, employer-matched retirement accounts, and paid-off homes face a manageable adjustment. Lower-income households, renters, women, workers of color, and those in physically demanding occupations face a qualitatively different retirement — one that may be characterized less by leisure and security than by financial precarity and involuntary labor-force participation.

The data on retirement preparedness by income is striking. Among workers in the bottom income decile — those earning less than $27,400 annually — nearly 79% lack access to any employer-sponsored retirement plan. Among the top decile, the figure is 18%. The retirement savings gap by race is equally stark: white households hold a median net worth approximately six times that of Black households, and retirement account ownership is 63% among white households compared to 41% among all other racial groups. Women, meanwhile, reach retirement with roughly 30% less in savings than men, a gap driven by lower lifetime earnings, career interruptions for caregiving, and more conservative investment behavior.

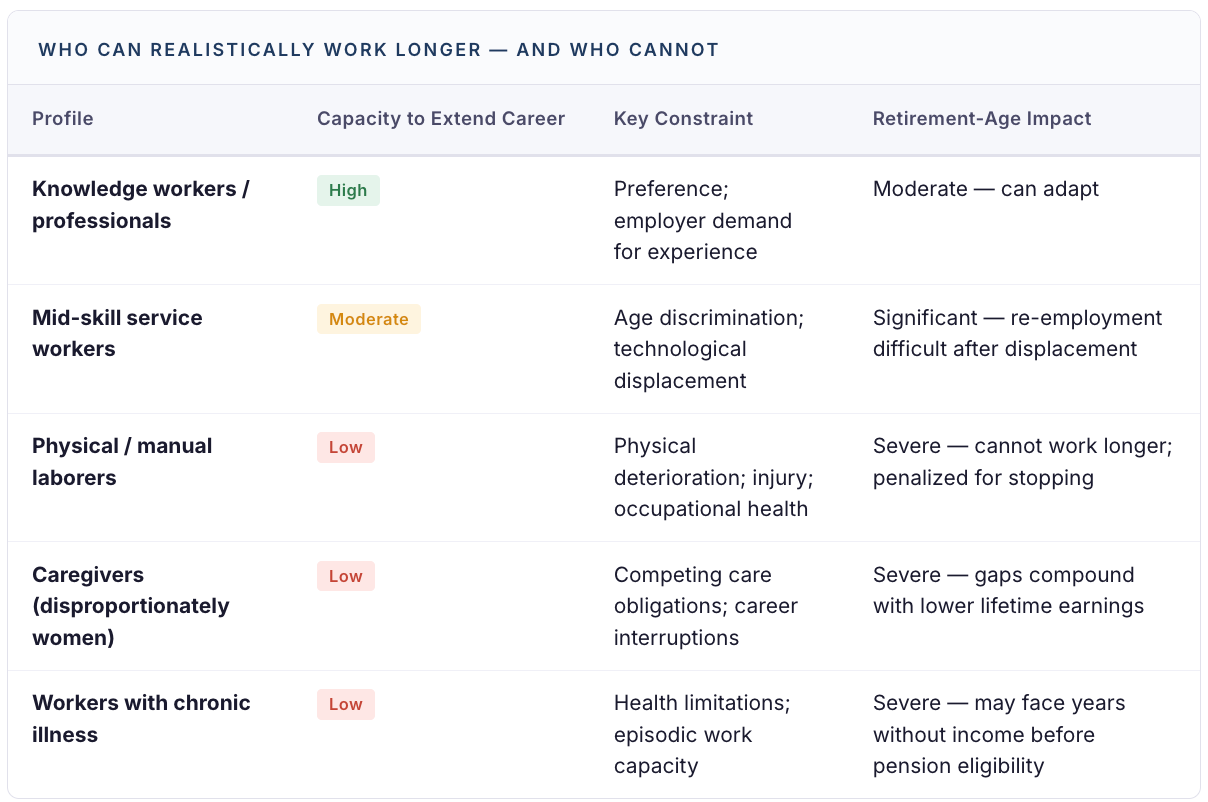

Physical capacity is another underappreciated dimension of inequality. Nearly 32% of workers aged 55–64 are employed in physically demanding occupations. For these workers, the aspiration to “work longer” — the preferred policy response to retirement shortfalls — is often unrealistic. A knowledge worker can plausibly extend a career into the late 60s or early 70s. A construction worker, nurse, or warehouse operative frequently cannot. The gap between who can work longer and who must work longer is a class divide that retirement-age reform tends to obscure.

Why the Retirement Crisis May Widen Class Divides More Than It Widens Average Poverty

National poverty statistics can mask the distributional reality. If wealthier households adapt successfully — working longer by choice, drawing on diversified portfolios, downsizing from appreciated homes — while lower-income households experience the full force of benefit compression and savings inadequacy, aggregate elderly poverty rates may remain roughly stable even as the gap between the retirement haves and have-nots widens dramatically. The retirement crisis, in this framing, is less about a rising poverty line and more about a bifurcating retirement experience.

SECTION VI

Housing as the Hidden Pension System

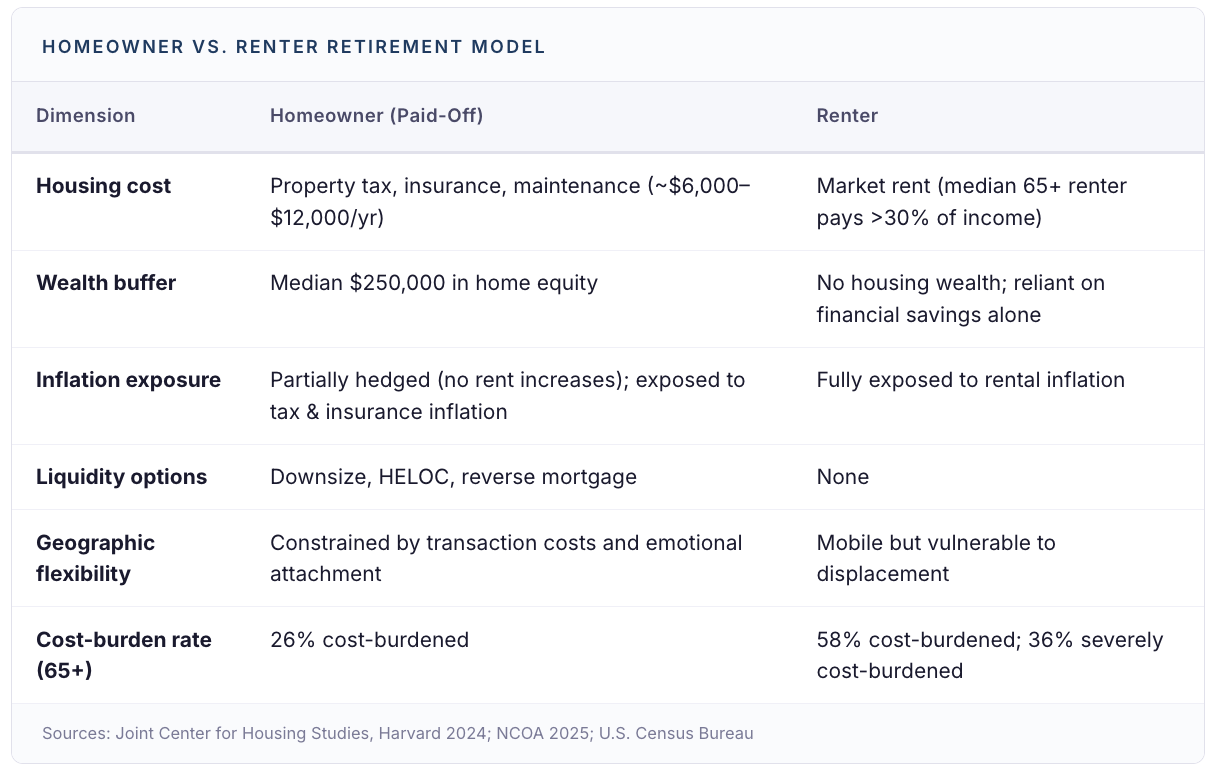

Across the advanced economies, housing has quietly become the single largest non-annuitized asset in retirement. For American homeowners aged 65 and over, housing equity represents approximately 50% of total non-annuitized wealth. The median home equity for this group is roughly $250,000 — a figure that exceeds the typical 401(k) balance by a factor of more than three. Baby boomers collectively hold an estimated $19 trillion in housing wealth, nearly 40% of all U.S. residential real estate.

In many respects, a paid-off home functions as a pension: it eliminates the largest recurring household expense, provides a buffer against inflation in shelter costs, and represents a liquid-adjacent asset that can be accessed through downsizing, sale, or reverse mortgage. For the roughly 79% of Americans over 65 who own their homes, housing equity is a meaningful — and sometimes dominant — component of retirement security.

But housing wealth is also deeply unequal. Median home equity for Black homeowners aged 65 and over is $123,000, compared to $251,000 for white homeowners — a gap that mirrors and reinforces the broader retirement wealth divide. Homeownership rates among younger cohorts have been falling, raising the prospect that future retirees will be less likely to enter old age with a paid-off home. And for those who do own, housing is not costless: property taxes (averaging $3,119 annually, with wide state-level variation), insurance premiums (which rose 21% in a single year from 2022–2023), maintenance, and HOA fees impose ongoing carrying costs that can stress fixed-income budgets.

Why Housing Can Stabilize Retirement for Some and Become a Trap for Others

The role of housing in retirement security is fundamentally bifurcated. For asset-rich households in appreciating markets, a paid-off home is a powerful stabilizer — effectively a self-funded annuity in shelter. For elderly renters, housing is the single largest source of financial stress: 58% of renters over 65 are cost-burdened, and more than a third spend over half their income on rent. For homeowners in depreciating or high-cost-of-maintenance markets, housing wealth can prove illusory — equity that exists on paper but cannot be efficiently or affordably converted to income. Reverse mortgage usage remains low (just 26,521 originations in FY 2024), reflecting both product complexity and borrower reluctance, and the senior housing market — while growing rapidly toward $1.3 trillion by 2033 — serves primarily higher-income segments.

SECTION VII

Why Retirement Age Is the Political Pressure Valve

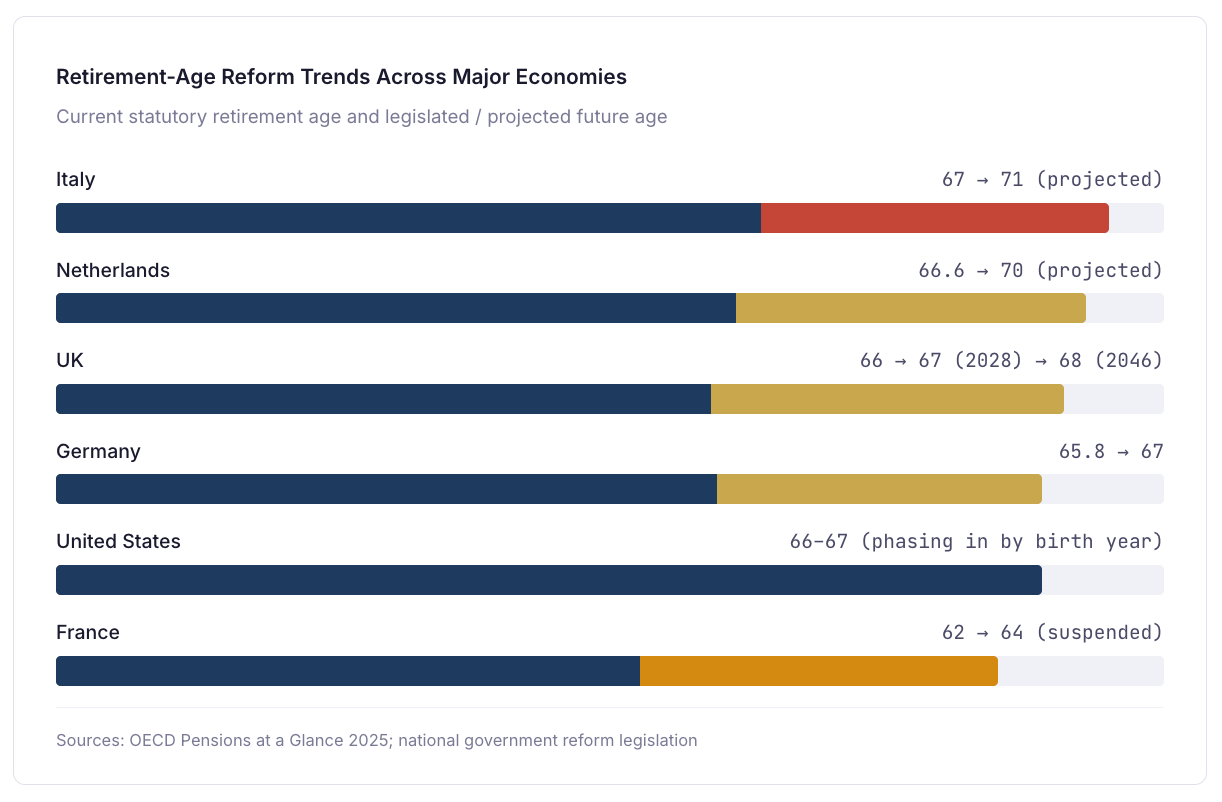

Of all the mechanisms through which retirement is being repriced, raising the statutory retirement age has become the preferred instrument of fiscal adjustment across the West. It achieves two goals simultaneously: it reduces the actuarial cost of pensions by shortening the payout period, and it increases the tax base by extending the working life. Critically, it avoids the political toxicity of nominal benefit cuts — no monthly check is reduced; instead, the age at which one can claim it is moved forward.

The trend is unambiguous. The UK is raising its state pension age to 67 by 2028 and to 68 by the mid-2040s. Germany is phasing in a retirement age of 67. Italy’s system already incorporates life-expectancy linkages that project an effective retirement age above 70 for younger cohorts. France’s attempt to move from 62 to 64 — modest by international comparison — triggered the most significant social unrest the country had seen in years, culminating in the reform’s suspension in late 2025.

The labor-market reality complicates the policy logic. While labor-force participation among Americans aged 65 and over has risen to approximately 19%, it remains overwhelmingly concentrated in professional, managerial, and knowledge-economy roles. For workers in physically demanding sectors — construction, manufacturing, healthcare, logistics — the capacity to extend careers is sharply limited. The gap between expected retirement age (66) and actual retirement age (62) reflects this: 58% of workers retire earlier than planned, and nearly half cite health problems or job loss as the reason. Raising the statutory retirement age does not change the body’s capacity to work; it changes the penalty for stopping.

Why Later Retirement Is Often Framed as Modernization but Functions as a Benefit Reduction

The rhetoric of retirement-age reform tends to emphasize alignment with rising life expectancy. If people live longer, the argument runs, they should work longer. The framing is one of fairness and sustainability. But in practice, the gains in life expectancy are unevenly distributed — wealthier, more educated individuals live significantly longer than poorer ones — meaning that a uniform retirement-age increase is effectively regressive: it reduces the retirement period most for those who already have the shortest life expectancies and the least capacity to extend their working lives.

SECTION VIII

Market and Macro Implications

The repricing of retirement is not merely a social-policy problem. It carries significant implications for asset allocation, sector positioning, fiscal sustainability, and macroeconomic dynamics. The shift from institutional to individual retirement risk creates both demand for new financial products and structural vulnerabilities in consumption and labor markets.

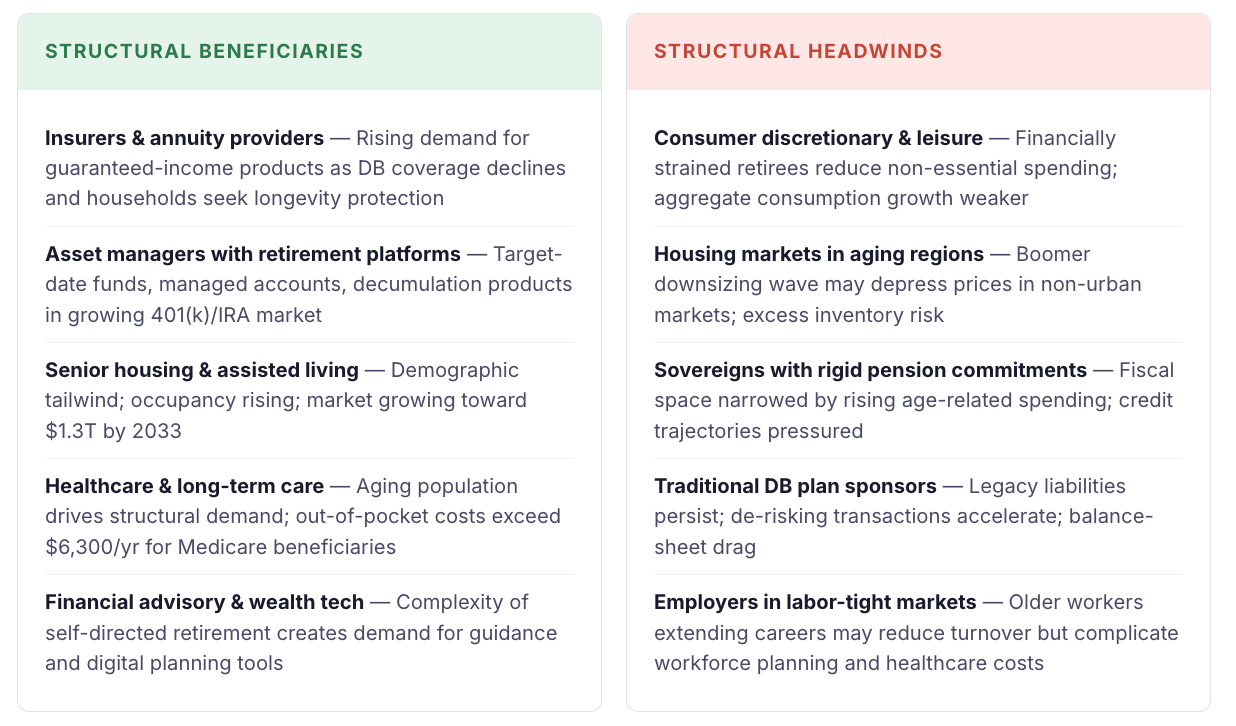

As retirement security becomes more individualized, demand for income-generating and risk-mitigation products will rise structurally. Annuity markets, target-date funds, retirement-income platforms, and longevity insurance are positioned to benefit. Insurers with strong annuity businesses and asset managers with retirement-focused product suites face a growing addressable market as defined-benefit coverage continues to decline and households seek to replicate — through private markets — the income certainty that institutional pensions once provided.

The senior-housing and long-term-care sectors are similarly positioned. With the 65-and-over population projected to reach 22% of the U.S. total by 2040, and senior housing occupancy already at 88.7% with 17 consecutive quarters of increases, the structural demand case is strong. Healthcare spending in retirement will continue to represent a dominant and growing share of household budgets, benefiting providers, insurers, and drug manufacturers focused on age-related conditions.

On the macro side, the fiscal arithmetic is daunting. U.S. Social Security and Medicare represent the largest and fastest-growing categories of federal spending. In Europe, pension-related expenditures above 14% of GDP in countries like Italy and France constrain fiscal space for investment, defense, and discretionary spending. Sovereign-credit trajectories are increasingly shaped by aging-related liabilities, and the political inability to reform these systems introduces a slow-moving but persistent fiscal risk premium.

SECTION IX

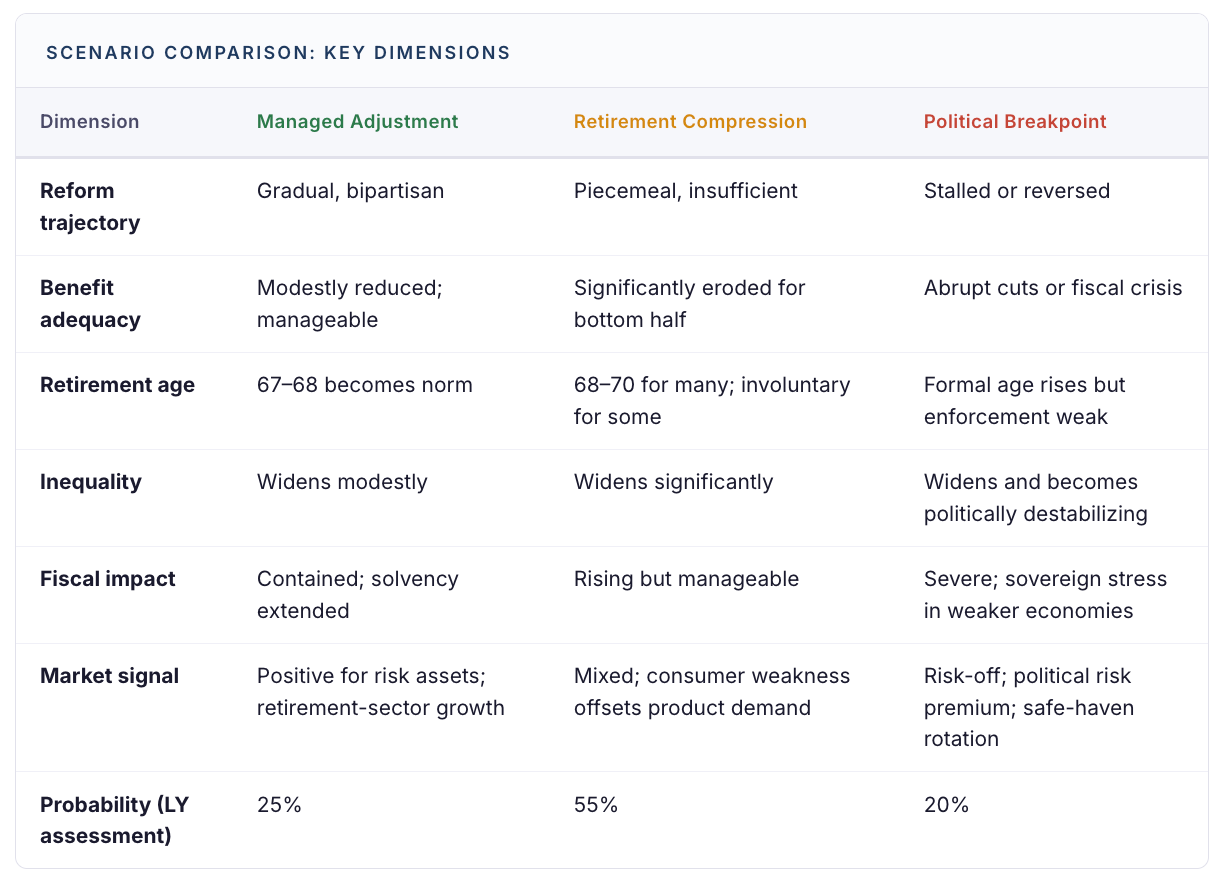

Scenario Modeling: Managed Adjustment vs. Retirement Compression

The trajectory of retirement across the West is not predetermined. Policy choices, demographic developments, and market dynamics will shape outcomes. Three scenarios frame the plausible range over the next five to ten years.

SECTION X