The Swiss Machine Keeps Running: On Holding's Record Quarter Tests the Limits of Gravity

Record Q1 net sales of CHF 831.9 million, a gross margin that crossed 64%, and Asia-Pacific finally crossing the 20% threshold. On Holding posted a Q that would make even the skeptics lace up

01 · Quarter at a Glance

A Quarter That Redrew the Margin Story

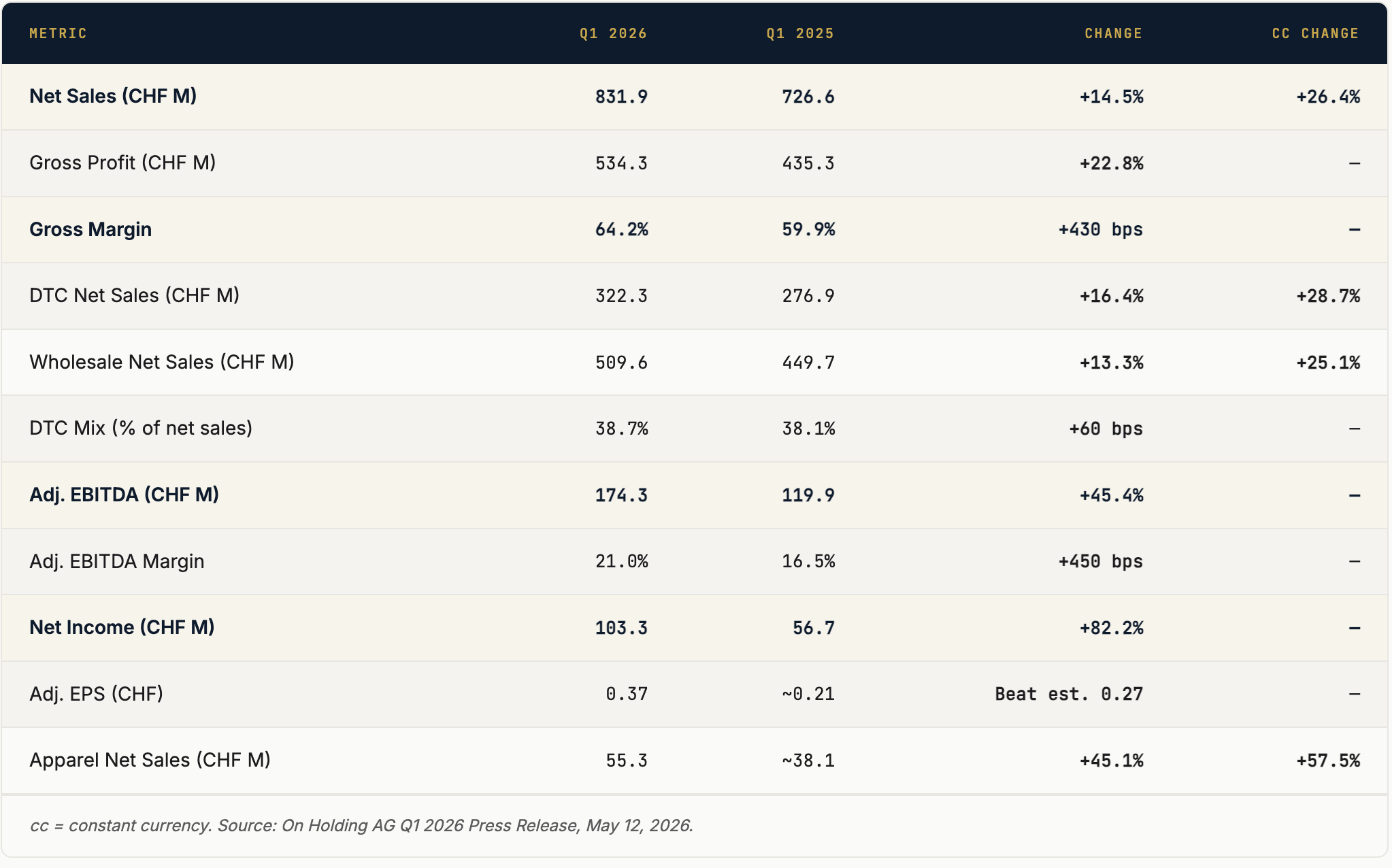

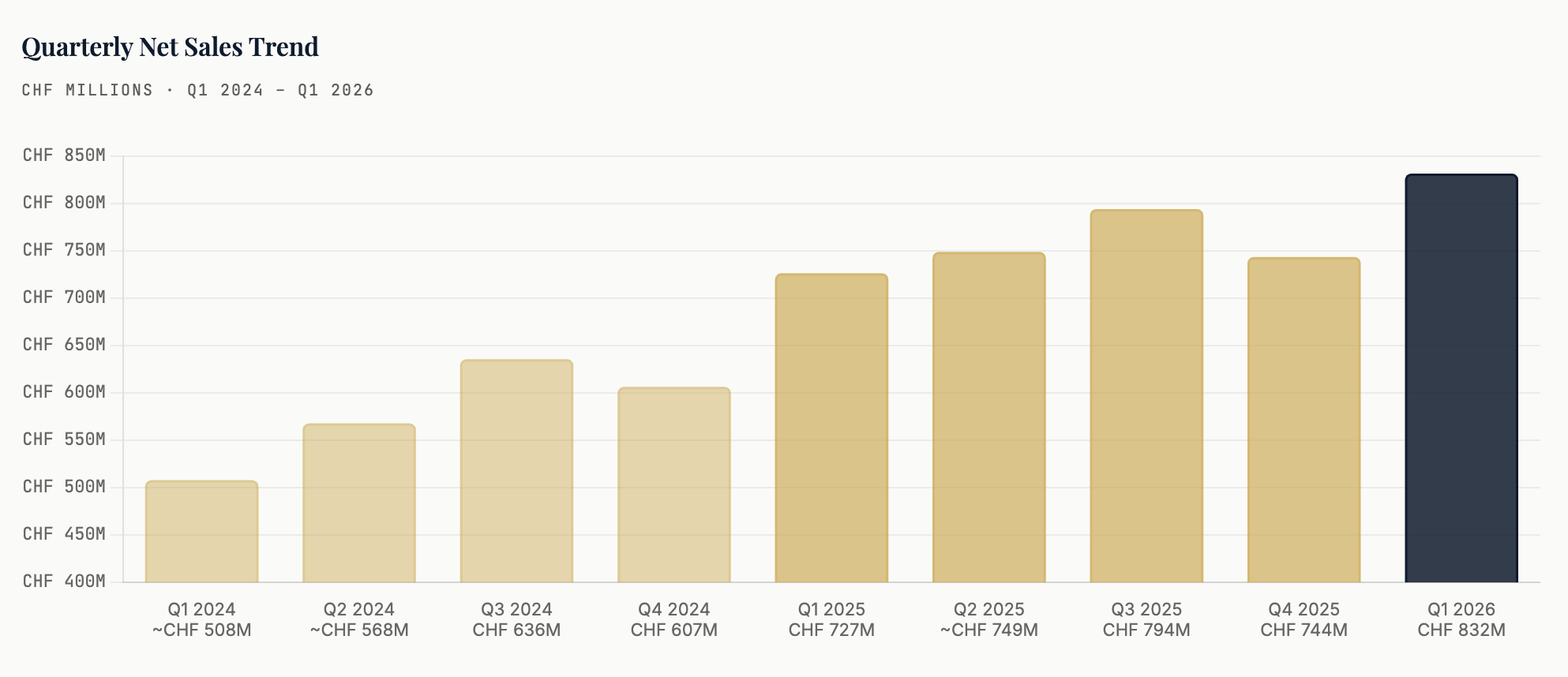

On Holding AG arrived at May 12, 2026 carrying the weight of investor expectations built on three years of relentless outperformance. It delivered. The Swiss athletic brand reported record first-quarter net sales of CHF 831.9 million — a gain of 14.5% on a reported basis and a far more impressive 26.4% when stripped of the Swiss franc’s punishing appreciation against the U.S. dollar.

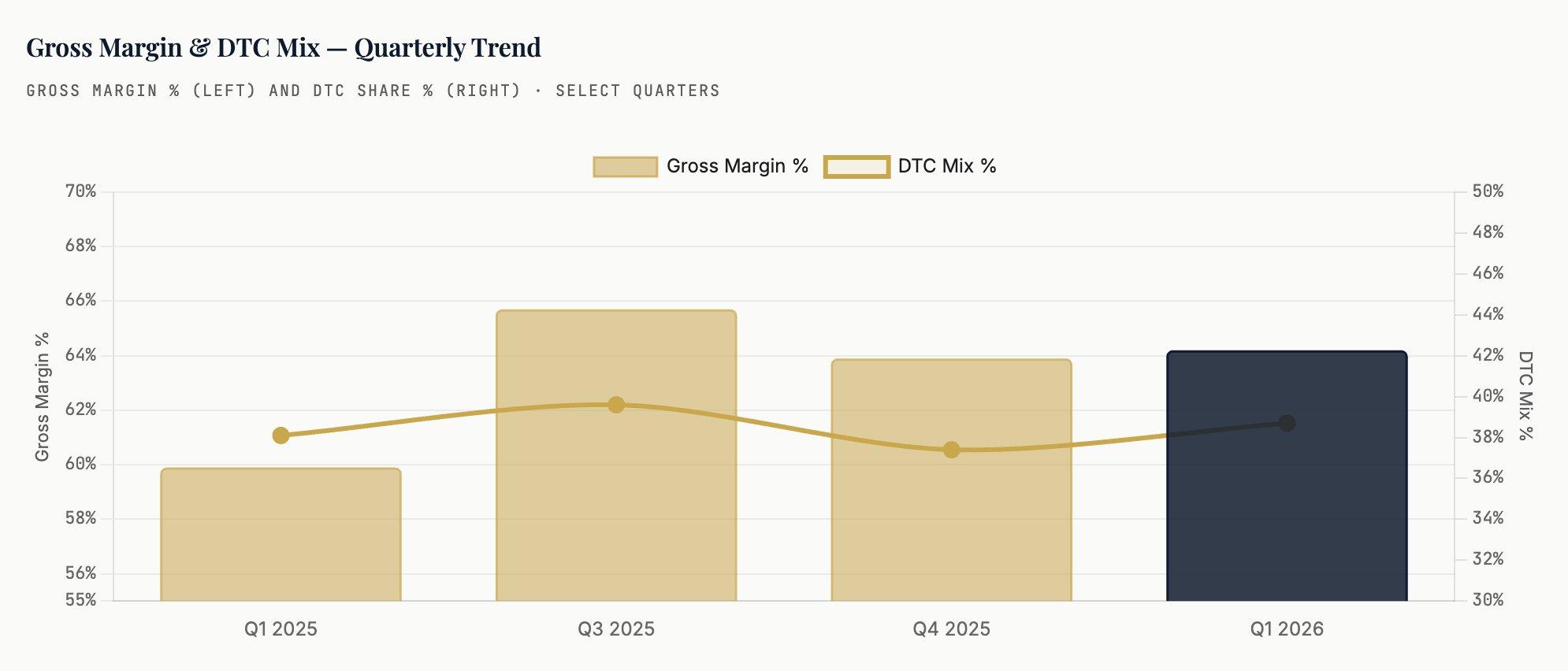

The headline growth figure, though, was almost a distraction from the more consequential story developing in the income statement. Gross margin printed at 64.2%, up 430 basis points from the same quarter a year ago, accelerating a trajectory that management has now codified into its official guidance. Adjusted EBITDA of CHF 174.3 million represented a 45.4% increase year-over-year, with the margin expanding 450 basis points to 21.0% — numbers more commonly associated with luxury goods than athletic footwear. Net income of CHF 103.3 million surged 82.2%, and adjusted earnings per share of CHF 0.37 bested consensus estimates by a meaningful margin.

The quarter also carried the weight of a significant leadership transition. Martin Hoffmann, who had served as both CEO and CFO and was widely credited with architecting the company’s financial discipline, stepped down. Caspar Coppetti and David Allemann, two of On’s original three co-founders, assumed the co-CEO roles, while Frank Sluis took the CFO chair on May 1, 2026. That the company posted record results in the quarter framing this transition speaks to the institutional depth the brand has cultivated since its 2021 NYSE listing.

02 · The Brand Flywheel

CloudTec, Federer, and the Architecture of a Premium Athletic Brand

To understand why On Holding’s margins are expanding at a pace that embarrasses most of its athletic footwear peers, you need to understand the flywheel the company’s founders assembled over fifteen years — and why it is only now spinning at full velocity.

On was founded in 2010 in Zurich by former professional triathlete Olivier Bernhard alongside Caspar Coppetti and David Allemann, two former brand strategists. The original insight was not merely technological but philosophical: performance running shoes had become an arms race of foam compounds and carbon plates, all of them growing progressively uglier in the name of speed. Bernhard’s CloudTec sole — hollow rubber cloud pods designed to compress on landing and firm up on push-off — delivered genuine biomechanical benefits, but it was the aesthetic decision to make those pods visible and distinctive that created something rarer in athletic footwear: a shoe that runners wanted to wear off the track.

That decision, mundane in hindsight, laid the foundation for On’s ability to charge premium prices without significant markdown pressure. When Swiss tennis legend Roger Federer became an investor and co-creator of On’s luxury line — the Roger collection — in 2019, the brand acquired something that no marketing budget can purchase: genuine cultural credibility at the highest end of the sport-lifestyle intersection. The Roger line sits above On’s core running assortment in price and prestige, functioning as a halo that elevates perception across the entire catalog. In an industry where Nike and Adidas spend billions to maintain the illusion of exclusive athletic heritage, On assembled that heritage organically and relatively cheaply.

“APAC surpassed 20% of overall revenue for the first time. Apparel exceeded 10% of DTC sales for the first time. When a company hits two ‘for the first time’ milestones in a single quarter, it is rarely an accident.”

LongYield Analysis · Q1 2026

The flywheel mechanism works as follows. Performance credibility — earned by elite athletes running Boston and Tokyo in Cloudflows and Cloudmonsters — drives consumer trust and allows entry pricing above mass-market competitors. That premium pricing supports higher gross margins, which fund brand investment, which deepens the cultural cachet, which allows the price premium to persist. The DTC channel accelerates this loop: by controlling the store environment, the on-site experience, and the data on who is actually buying, On learns its customer faster than any wholesale partner can tell it. Each increment of DTC mix — which stood at 38.7% in Q1 2026, up 60 basis points year-over-year on a path management targets at 100-200 basis points of annual improvement — feeds more proprietary data back into the system.

The gross margin expansion playing out in real time is the financial proof of this flywheel. At 64.2% in Q1 2026 — 430 basis points above Q1 2025’s already-elevated 59.9% — On is now posting margins that approach luxury apparel territory rather than athletic footwear. For context, Nike’s gross margin has been mired in the low-to-mid 40s as the company digests excess inventory and restructuring charges. Adidas has been working back toward the high 40s after years of disruption. Hoka’s parent Deckers Outdoor operates in the low 50s. On is in a different air column entirely, one sustained by product mix, pricing power, and a rapidly expanding high-margin DTC business.

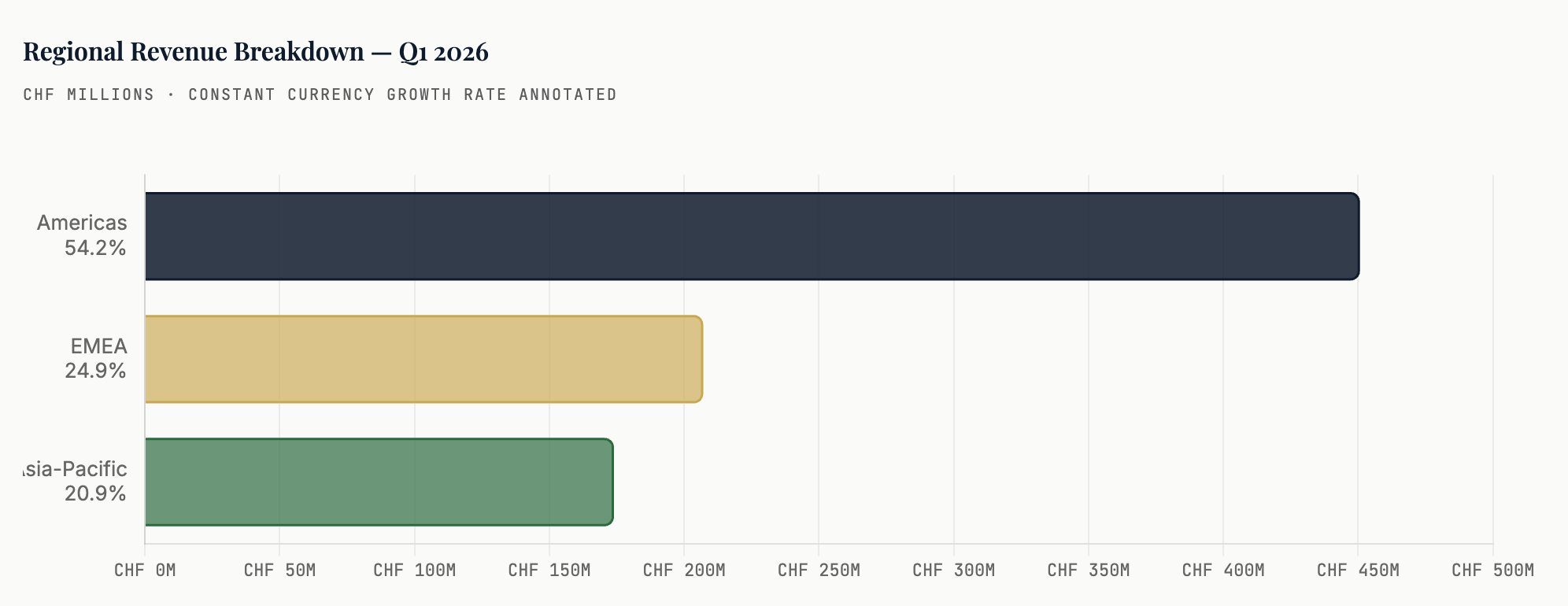

03 · Geography

Asia’s Acceleration, America’s Headwind, and Europe’s Steady Climb

The geographic decomposition of On’s Q1 2026 results tells three distinct stories simultaneously — and the most important one is unfolding roughly 9,000 kilometers from the brand’s Swiss headquarters.

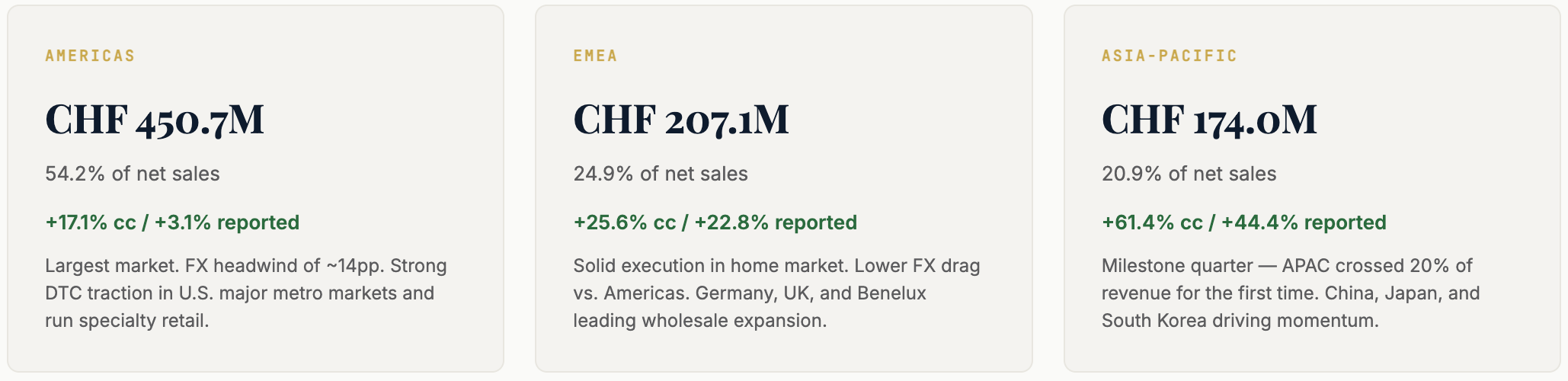

The Americas, which generated CHF 450.7 million in the quarter, remains On’s largest regional market by a significant margin, accounting for 54% of total net sales. But the Americas figure requires careful reading. Reported growth of just 3.1% masks an entirely different business reality: strip out the effect of the Swiss franc’s sharp appreciation against the U.S. dollar, and Americas revenue grew 17.1% in constant currency. This is not a growth deceleration in the underlying business. It is a foreign exchange translation effect, and a severe one at that — one that will continue to shadow reported results for as long as the CHF commands its current premium against major trading currencies.

Europe, the Middle East and Africa delivered CHF 207.1 million, growing 22.8% reported and 25.6% in constant currency — the most “clean” regional number in that the FX distortion between Swiss francs and the euro is smaller than the transatlantic gap. The European performance is notable for its consistency: EMEA has been a reliable double-digit grower across multiple years, benefiting from On’s early establishment as a premium running brand in German-speaking markets and its subsequent geographic expansion across the UK, Benelux, France, and Scandinavia. The gorpcore aesthetic trend — the intersection of outdoor, performance, and luxury fashion — has been particularly potent in European markets, where On’s product lines sit comfortably across all three vectors.

But Asia-Pacific is the story. CHF 174.0 million, up 44.4% reported and a staggering 61.4% in constant currency — this is the kind of growth rate that rewrites investment narratives. The milestone of APAC crossing 20% of total revenue “for the first time” carries outsized significance not merely as a round number but as a marker of structural change. China represents On’s most consequential whitespace opportunity: a market of hundreds of millions of athletic consumers, a growing appetite for premium Western sportswear brands, and an increasingly sophisticated running culture in tier-one and tier-two cities. On has been investing in its China infrastructure — flagship stores, digital presence, local partnerships — for several years, and the returns are now hitting the income statement with force.

The Japan and South Korea markets add depth to the APAC picture. Both countries have sophisticated running cultures with strong communities around ultramarathon, trail, and road racing. On’s shoes have achieved meaningful penetration in Japanese specialty running retail, benefiting from the country’s famously discerning athletic consumer base and the cultural premium attached to Swiss-engineered precision. South Korea’s luxury lifestyle consumer demographic — younger, brand-conscious, willing to pay for design distinction — maps almost precisely onto the Roger Federer collection’s target buyer.

Looking forward, the geographic opportunity set remains asymmetric. Americas and EMEA are not saturated, but they are established. Asia-Pacific at 20.9% of revenue is still structurally under-penetrated relative to the addressable market. Management’s guidance of continued APAC outperformance is less a prediction than an observation of the pipeline already under construction.

04 · The Apparel Bet

Past the 10% Threshold: On’s Quiet Revolution in Performance Apparel

Athletic brands are not built on shoes alone. Every durable athletic franchise eventually reaches the same strategic inflection point: the moment when footwear dominance justifies the expansion into the far larger and higher-frequency world of apparel. On Holding reached that inflection point in Q1 2026.

Apparel net sales of CHF 55.3 million grew 45.1% on a reported basis and 57.5% in constant currency — the fastest-growing major product category in On’s portfolio. More symbolically, apparel crossed 10% of DTC sales for the first time. That threshold matters because it signals the transition from a novelty category to a meaningful revenue contributor in the channel where On has the most pricing power, the most brand control, and the richest customer relationships.

The strategic logic of On’s apparel push mirrors, in accelerated form, the playbook executed by Lululemon Athletica over the past two decades. Lululemon began as a yoga-focused apparel brand in Vancouver and methodically expanded into running, training, and eventually full lifestyle — building a community-driven brand that commanded premium prices and extraordinary loyalty. On is attempting something similar but in reverse: starting from the performance running shoe and moving outward into the apparel categories that the same consumer buys. The advantage of this approach is that On already owns the performance credibility; the challenge is building apparel design and manufacturing expertise at scale.

The Full-Kit Thesis

The athletic consumer’s brand consolidation behavior — the preference, once trust is established, to outfit an entire workout in a single brand — creates significant revenue leverage for brands that execute. Nike’s peak EBIT margins were not built on shoes alone. Adidas’s operating leverage came when apparel and footwear amplified each other. On is building toward the same dynamic: a consumer who starts with Cloudrunners, adds the lightweight training shorts, then the aerodynamic half-zip, then the Roger tennis jacket for weekend coffee. Each category extension that hits performance and aesthetic standards extends the share of wallet On can capture.

At CHF 55.3 million on a quarterly run rate, apparel is still roughly 6.6% of total net sales — a small number with a steep growth vector. If On sustains even half the current constant-currency growth rate, apparel could represent 15-20% of revenue within three years, fundamentally reshaping the company’s revenue mix and its relationship with consumers.

On’s apparel design language borrows deliberately from the minimalism that defines its footwear: clean Swiss geometry, restrained color palettes punctuated by the company’s elongated logo, and materials chosen for genuine performance function rather than marketing specification alone. The Lightweight Running collection — ultra-minimal shorts, breathable tops, reflective trim — has found particular resonance with serious runners who have previously managed their performance wardrobe across multiple brands. The Movement collection, bridging gym and street, pursues the same aesthetic consumers who buy the Cloudnova sneaker: elevated basics with a distinctive design signature.

The apparel category also carries a structural margin advantage over footwear. Sole engineering, foam formulations, and outsole tooling create high capital requirements and long production cycles in shoes. High-performance technical apparel, by contrast, benefits from shorter development cycles, more flexible supply chains, and materials innovation that can be applied across multiple silhouettes. As On’s apparel mix grows, it will apply incremental upward pressure on blended gross margins — which, at 64.2% in Q1 2026, are already exceptional.

05 · Margins & Profitability