Uber: The Platform That Ate Mobility

Q1 2026 Results — Revenue Miss, Bookings Beat, Robotaxi Inflection and the $2B Advertising Engine Nobody Talks About

Uber reported Q1 2026 with a revenue miss and a bookings beat — and the market correctly focused on the bookings. At $53.7B in gross bookings, growing 25% year-over-year (21% constant currency), Uber is compounding at a rate that belies its scale. The more interesting story, however, is structural: a $2B annualized advertising business hiding inside a mobility platform, a robotaxi network that is genuinely live (not just announced) across multiple U.S. cities through the Waymo partnership, and an EBITDA margin trajectory that suggests the profitability story remains intact even as revenue take-rate faces secular pressure. Uber is no longer a ride-hailing company valued on ride-hailing economics — and the market is only partially pricing what it has become.

01

The Quarter: Read the Bookings, Not the Revenue

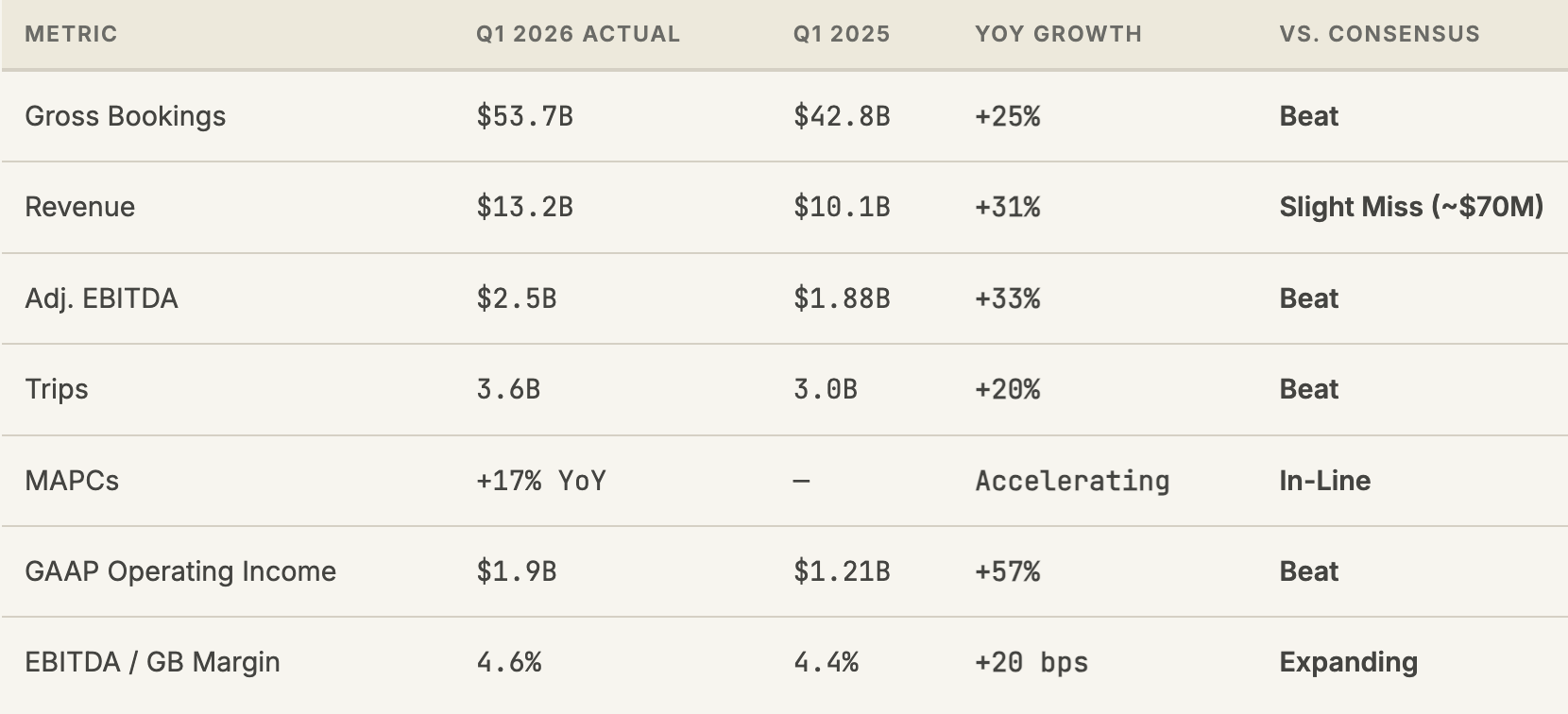

Uber’s Q1 2026 revenue of $13.2B missed consensus by approximately $70M — a rounding error in the context of a $53.7B gross bookings quarter, but enough to provide the headline writers their miss story. The revenue miss is almost entirely a function of currency headwinds and product mix, not a demand-side signal. Constant-currency gross bookings grew 21% year-over-year, and reported bookings grew 25% — the FX tailwind (yuan, euro, pound appreciation against the dollar) boosted bookings while the revenue take rate, denominated differently, created the headline gap.

The more important metrics all pointed in the right direction. Trips reached 3.6 billion in the quarter, up 20% year-over-year — suggesting the consumer demand picture is healthy across both mobility (rides) and delivery (Uber Eats). Monthly Active Platform Consumers grew 17% year-over-year, and trips per MAPC grew 3%, meaning the platform is both adding users and increasing engagement among existing ones. That combination — frequency growth on top of audience growth — is the sign of a healthy consumer platform, not a saturating one.

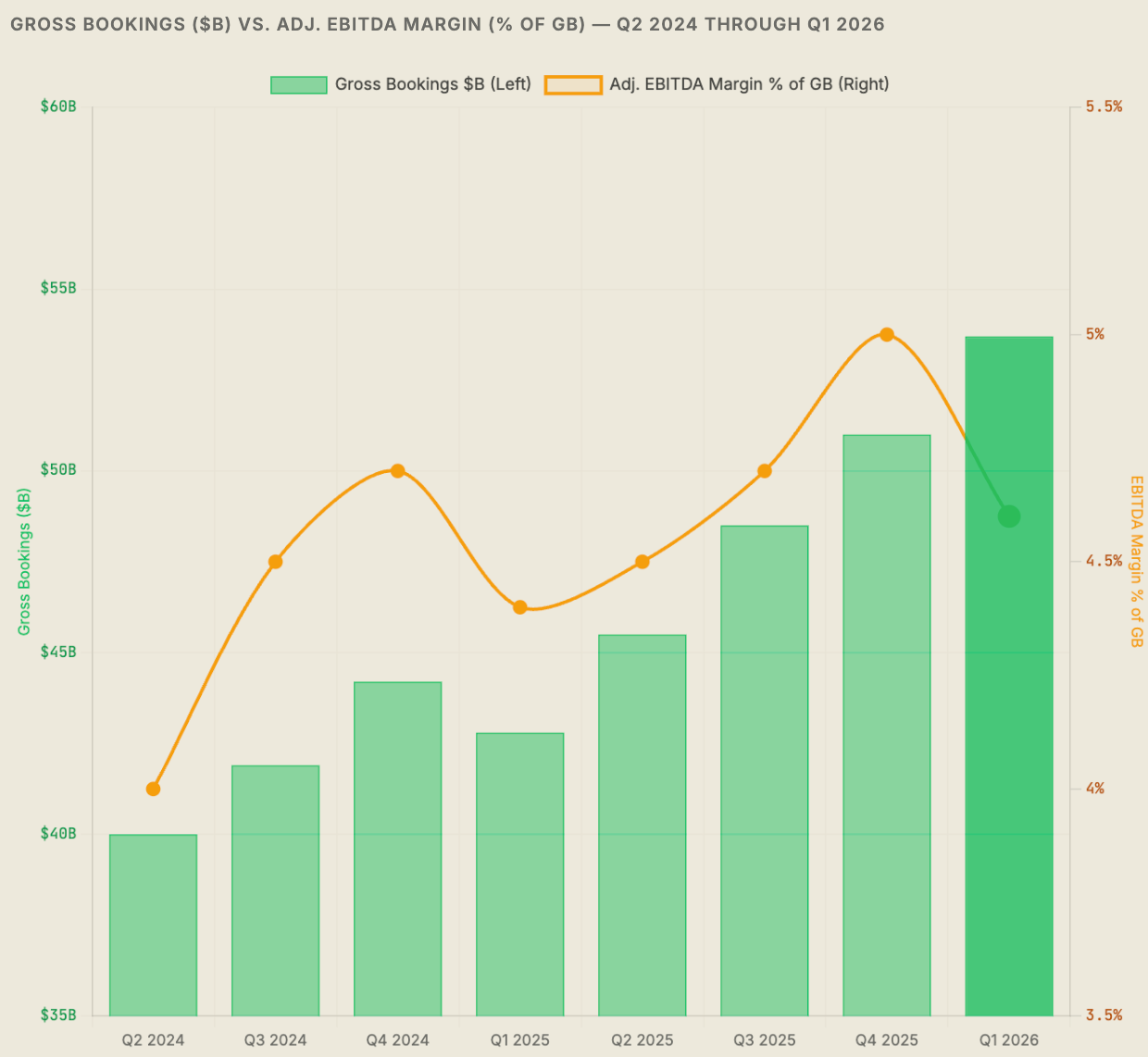

Adjusted EBITDA of $2.5B grew 33% year-over-year, well ahead of the 25% bookings growth rate — a margin expansion signal. The EBITDA margin as a percentage of gross bookings reached 4.6%, up from 4.4% in Q1 2025. Twenty basis points of EBITDA margin expansion on a $53.7B gross bookings base represents roughly $107M of incremental EBITDA — not trivial. GAAP operating income of $1.9B grew 57% year-over-year, reflecting both the EBITDA improvement and lower stock-based compensation as a share of revenue. GAAP net income of $263M was distorted by a $1.5B pre-tax headwind from equity investment revaluations — a non-operating item that moves with the valuations of Uber’s minority stakes in Didi, Aurora, and others.

02

Q2 2026 Guidance — Confidence, Not Sandbagging

Uber guided Q2 2026 gross bookings to $56.25–57.75B, implying 18–22% constant-currency growth. Adjusted EBITDA guidance of $2.70–2.80B represents a midpoint of $2.75B — another sequential increase from Q1’s $2.5B, and approximately 4.8% of bookings at the guidance midpoint, continuing the margin expansion trajectory.

Non-GAAP EPS guidance of $0.78–0.82 represents 31–38% growth year-over-year — a range that implies the equity investment revaluation headwinds of Q1 won’t recur at the same magnitude. The guidance cadence is notable: Uber has beaten its own gross bookings guidance in six of the last seven quarters, with the one exception attributable to an acute FX event. Management’s guidance style is not aggressive sandbagging, but it is conservative enough that the guidance midpoints have typically been achievable without heroics.

03

The Three-Segment Story: Mobility, Delivery, and Freight

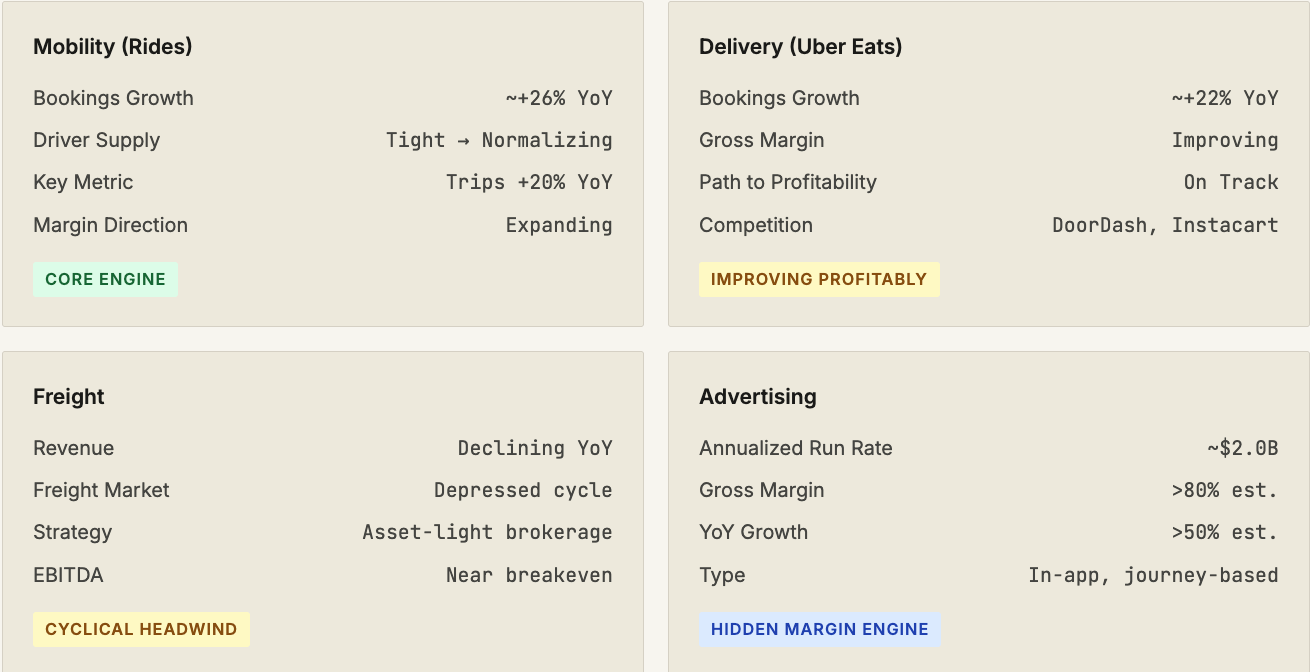

Mobility continues to be the primary driver of both growth and profitability. Delivery has completed its transition from loss-leader to margin contributor — the path from the Uber Eats launch era, when the segment burned cash to acquire market share, to today’s improving margin contribution illustrates the operating leverage inherent in marketplace platforms once they achieve local density. Freight remains a headache, caught in a multi-year freight market downcycle that has compressed trucking rates industry-wide; Uber’s strategy of running an asset-light brokerage (it owns no trucks) limits the downside but also limits the upside until freight rates recover.

04

The Advertising Business — $2B That Changes the Margin Math

Uber’s advertising segment deserves far more analytical attention than it receives. The business has grown to approximately $2B in annualized revenue — a number that, if the segment were standalone, would make it a mid-cap company. More importantly, the gross margin on advertising revenue is estimated above 80%, dramatically above Uber’s blended gross margin of roughly 30%. Every incremental advertising dollar contributes to EBITDA at a rate that no other segment can match.

The advertising inventory is genuinely differentiated. Uber serves ads within the ride app during trip booking and in-journey, and within the Eats app during food ordering and delivery. These are high-intent moments — a rider waiting for their car, a diner looking at menu options — with first-party location data that makes targeting precise without relying on third-party cookies. In an advertising ecosystem that has been structurally degraded by iOS privacy changes and the deprecation of third-party tracking, Uber’s first-party intent data is an asset that cannot be replicated externally.

The competitive analog is Amazon’s advertising business, which grew from a curiosity to a $50B+ revenue stream by monetizing purchase-intent moments. Uber’s addressable advertising inventory is smaller — fewer high-intent moments, lower dwell time — but the structural argument is similar: a platform with first-party behavioral data at the moment of decision is a premium advertising environment. At $2B annualized and growing at an estimated 50%+, the advertising business will be a $3–4B revenue contributor within 24 months. At 80%+ gross margin, the EBITDA contribution will be material to any serious valuation model.

05