Walmart: America's Economic Mirror Speaks — and It's Complicated

Walmart's first-quarter results delivered a $177.8B revenue beat, a 26% e-commerce surge, and a 44% advertising spike , then the stock dropped 7%

01 — Executive Summary

The Barometer Reads: Resilient, But Strained at the Edges

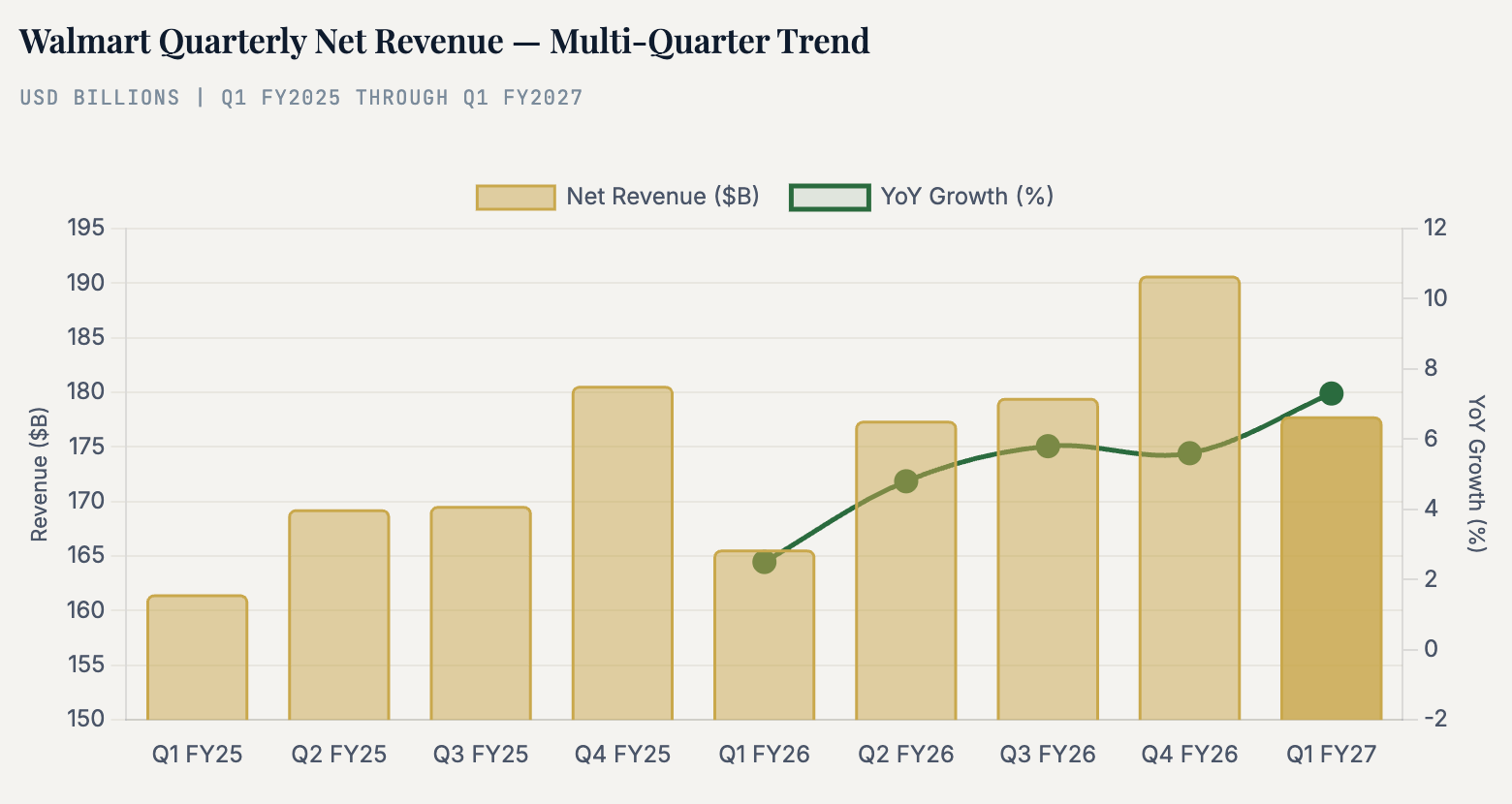

Every ninety days, Walmart hands economists and investors something that no government survey can quite replicate: a real-time, $178-billion snapshot of what 240 million weekly customers are actually buying, how often they are showing up, and how much they are willing to spend. When the world’s largest retailer reports earnings, it is not simply disclosing a corporate balance sheet — it is publishing a living census of American consumer behavior at scale. This morning’s Q1 FY2027 results, released May 21, 2026, offered a portrait that is simultaneously encouraging and unsettling: strong top-line momentum undercut by cost pressures that the company cannot fully absorb, and an increasingly anxious consumer who is trading up in frequency but trimming ticket size.

The headline numbers were unambiguously good. Revenue of $177.8 billion cleared consensus by nearly $3 billion, driven by a U.S. comparable-store sales gain of 4.1% — the strongest showing in six quarters when measured by transaction growth. E-commerce continued its now-two-year streak of 20%-plus expansion, growing 26% globally and 45% in U.S. delivery specifically. Advertising revenue surged 37% globally, and Walmart’s membership ecosystem posted 27% growth in membership and other income. Net income rose 18.8% year-over-year to $5.33 billion. On the surface, this is a company firing on every cylinder.

But the market punished the stock anyway, sending WMT down roughly 7% intraday — a reaction that tells you something critical. The concern is not where Walmart has been, but where it is going. Fuel costs hit operating income with a 250-basis-point headwind. CFO John David Rainey signaled that tariff-driven price increases will begin hitting shelves in late May and accelerate in June, potentially dampening the very consumer traffic that has been Walmart’s competitive engine. And while the full-year guidance was maintained at $2.75–$2.85 in adjusted EPS, the market had quietly built in something more optimistic. The message from Bentonville: we are running well, but the terrain ahead is rough.

What makes Walmart’s quarter especially significant in May 2026 is context. The American consumer is navigating simultaneously elevated shelter costs, a softening labor market at the margin, resumed student loan pressures, and now a tariff regime that is adding real inflation to goods categories that had been deflating for the better part of two years. In this environment, Walmart is not merely a retail company — it is the default inflation shock absorber for a majority of U.S. households. The fact that transactions grew faster than ticket size tells you that people are coming more often but spending more carefully. That is not a consumer in freefall; it is a consumer making deliberate choices. And increasingly, that consumer — including higher-income households — is choosing Walmart.

02 — Q1 FY2027 Financial Results

Full Breakdown: Revenue Beat, Margin Pressure, and the Fuel Problem

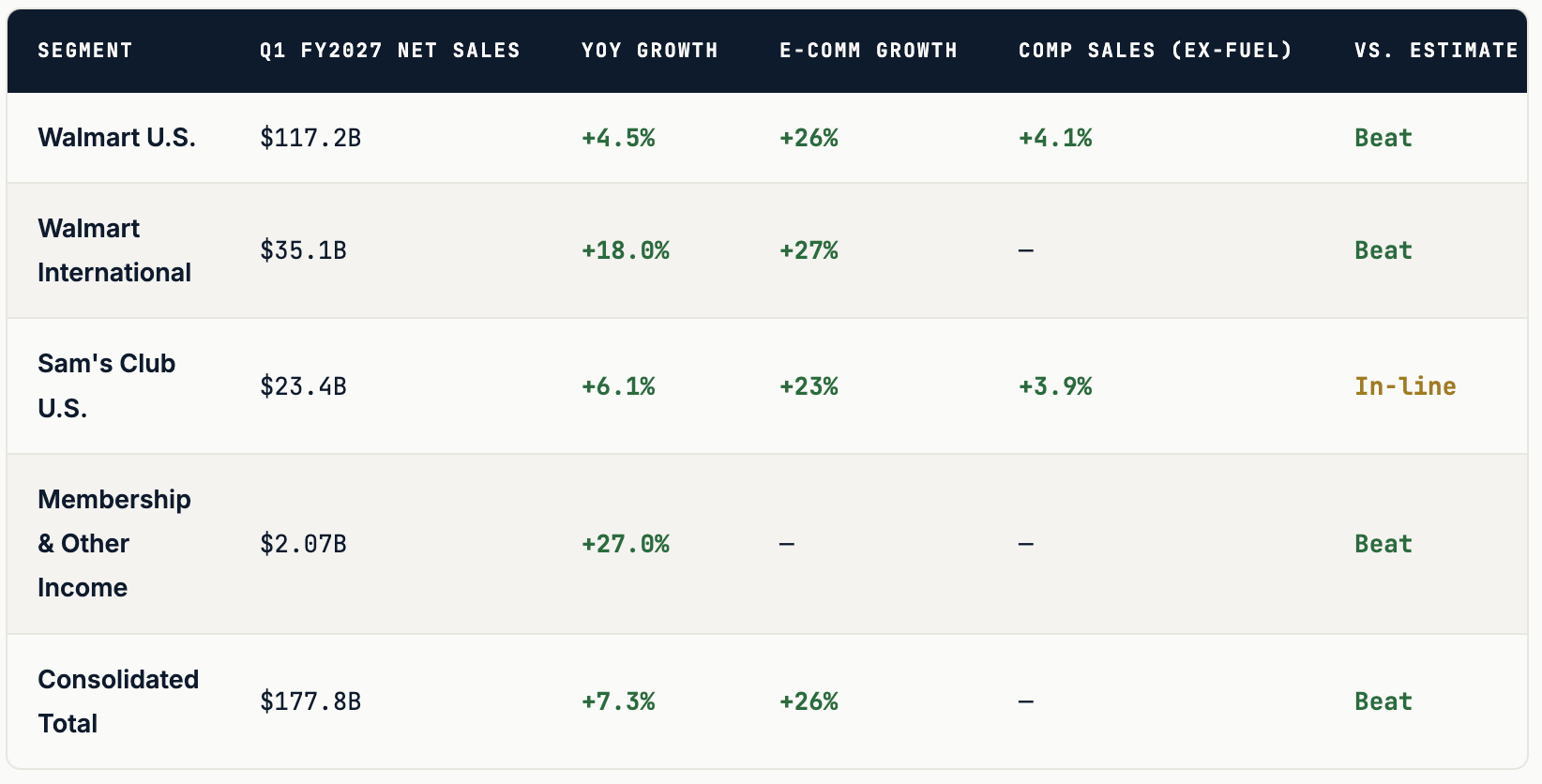

Walmart’s consolidated net sales for Q1 FY2027 reached $175.68 billion (net sales excluding membership income), with total revenue inclusive of membership and other income at $177.8 billion — a 7.3% increase from the prior-year period. The company beat analyst revenue expectations of roughly $174.98 billion by approximately $2.8 billion. Adjusted EPS of $0.66 grew 8.2% year-over-year, in line with the consensus estimate of $0.66, reflecting strong top-line leverage partially offset by elevated fuel and healthcare costs.

Operating income faced a meaningful headwind from elevated fuel costs in Walmart’s distribution and fulfillment network, which the company quantified at approximately 250 basis points of drag on operating income margin. This is a significant and underappreciated detail: even as Walmart’s higher-margin businesses (advertising, memberships) grow rapidly, the sheer cost of moving goods across a continent remains a material swing factor. Fuel prices in 2026 have been persistently elevated, and Walmart’s scale — while generally an advantage in negotiating fuel contracts — also means its absolute fuel bill is enormous.

Gross margin improved by a modest 6 basis points on a consolidated basis. Within Walmart U.S. specifically, merchandise mix contributed a favorable 29 basis points of gross margin expansion, reflecting the ongoing shift toward general merchandise (which recovered strongly in Q1 after a softer FY2026) and the growing weight of high-margin advertising and membership revenue in the consolidated P&L. The gross margin expansion would have been more pronounced without the fuel headwind dragging on fulfillment economics.

03 — The Consumer Health Signal

Traffic Up, Ticket Tight: What Walmart’s Cart Is Telling Us

Strip away the financial engineering and the margin analysis, and the most important number in Walmart’s Q1 report is this: transaction growth of 3.0% with average ticket growth of only 1.1%, both excluding fuel. That decomposition is a clear signal. The American consumer is showing up at Walmart more frequently than ever — this was the strongest transaction growth in six quarters — but they are managing their basket size with deliberate precision. They are not spending lavishly; they are spending strategically, trading dollars across a carefully chosen mix of categories.

“Market share gains were broad-based across categories and income tiers, led by upper-income households. We saw our best share growth in fashion in five years.”

— Dave Guggina, President & CEO, Walmart U.S., Q1 FY2027 Earnings Call, May 21, 2026

The grocery-versus-general-merchandise split inside Walmart U.S. was revealing. Food declined roughly 100 basis points as a category share contributor — largely attributed to a normalization in egg prices, which had been running at extraordinary levels during the avian flu cycle of late 2025. General merchandise, meanwhile, rose nearly 200 basis points, reflecting improving unit economics and a consumer who, after years of constrained discretionary spending, is beginning to loosen slightly on apparel and home goods. Walmart’s fashion performance in particular — described by management as its strongest share-growth print in five years — suggests the chain’s private label and curated national-brand mix is resonating beyond the value-shopper archetype.

Perhaps the most strategically important consumer trend in this quarter is the continued influx of higher-income households. Shoppers earning $100,000 or more per year now represent a substantial and growing component of Walmart’s market share gains — a demographic that, twelve months ago, might have defaulted to Target or specialty grocers but is increasingly drawn by Walmart’s improving digital experience, expanded fresh food assortment, and premium private-label offerings. This is not trade-down in the traditional sense; it is Walmart executing a deliberate quality upgrade that is eroding the perceived gap between itself and more aspirational competitors. Around 72% of all U.S. households now get at least some of their groceries from Walmart — a penetration rate that no other retailer approaches.

The implication for the broader economy is sobering. When Walmart sees its highest transaction growth in a year and a half, it means consumers are consolidating trips and spending at the same destination that promises the best everyday value — a behavior historically associated with households under financial pressure. The data is internally consistent: people are not cutting back; they are optimizing. In the 2026 consumer landscape, Walmart is less a last resort and more a rational first choice for a majority of American households across the income spectrum.

04 — The Tariff Test

Price Hikes Are Coming — and Walmart Cannot Shield Everyone

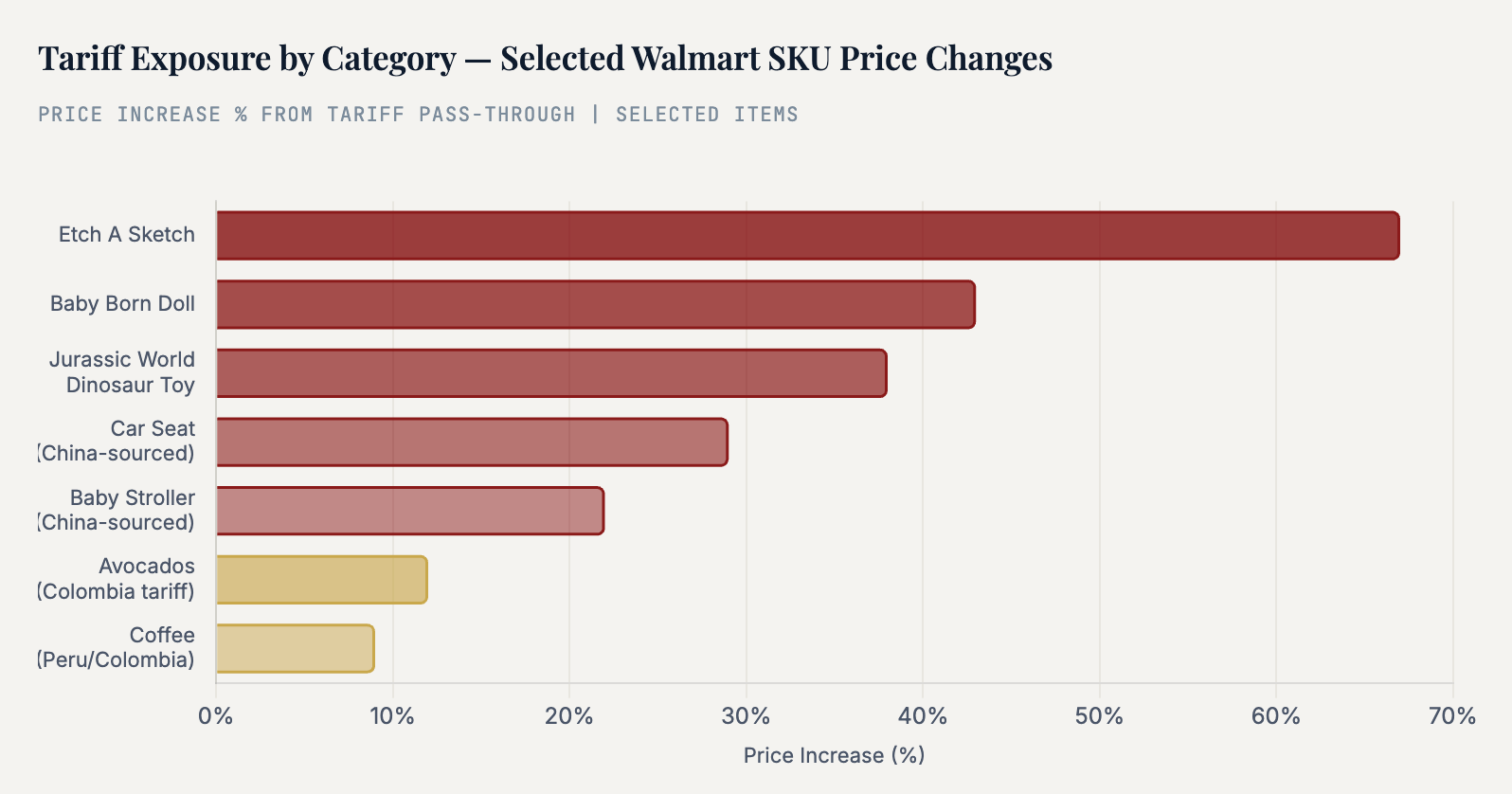

For months, the central question in U.S. retail has been which company would be the first to put a number on tariff pass-through. On this earnings call, Walmart answered clearly — and the answer was uncomfortable. CEO John Furner confirmed that price increases on a range of imported goods are imminent, beginning in late May 2026 and accelerating through June. The categories most exposed are those with the highest sourcing concentration from China: toys, electronics, baby gear (car seats, strollers), and apparel accessories. Beyond China, tariffs on agricultural-exporting nations including Costa Rica, Peru, and Colombia have raised costs on tropical fruits, avocados, coffee, and cut flowers.

“Given the magnitude of the tariffs, even at the reduced levels announced this week, we aren’t able to absorb all the pressure given the reality of narrow retail margins.”

— John Furner, President & CEO, Walmart Inc., Q1 FY2027 Earnings Call

The numbers on individual SKUs are stark. A Jurassic World dinosaur toy moved from $39.92 to $55 — a 38% increase. A Baby Born doll jumped from $34.97 to $49.97, a 43% premium. An Etch A Sketch rose from $14.97 to $24.99 — nearly a 67% markup. Car seats sourced from China, currently retailing around $350, may add $100 or more. These are not rounding errors; they are category-level shocks that will test consumer willingness to absorb cost, and they arrive at a moment when household budgets are already stretched by housing and healthcare inflation.

Walmart’s strategy in this environment is layered. The company is prioritizing price protection on essentials — food in particular — using its extraordinary scale to negotiate with domestic and alternative-source suppliers where possible. It is also leaning on its private-label portfolio, where it has greater pricing authority, to offer consumers a credible alternative to branded goods that are absorbing tariff increases. In categories where imported goods dominate and there is no substitute, Walmart is essentially acting as a passthrough, accepting that its role as a value provider cannot override arithmetic when import duties are running at 30% or above (still elevated even after the temporary U.S.-China tariff reduction from 145%).

The timing could not be more complicated. Walmart’s CFO noted that strong tax refund activity in Q1 may have partially buffered consumers against fuel-price headwinds during the quarter. That buffer is now largely spent. As Q2 begins, the consumer faces both a moderation in tax-refund tailwinds and the arrival of tariff-driven price increases across multiple product categories — a combination that could pressure discretionary spending meaningfully. The conservative tone on Q2 and full-year guidance reflects this calculus directly.

05 — Walmart’s New Revenue Streams

The Margin Transformation: Advertising, Memberships, and Data

The structural story of Walmart’s multi-year evolution — from commodity retailer to a diversified services and data company built on a retail chassis — showed its clearest evidence yet in Q1 FY2027. CFO John David Rainey stated explicitly that advertising and membership income now account for approximately one-third of Walmart’s total earnings. Let that sink in: a third of earnings at the world’s largest retailer now come not from selling physical goods, but from monetizing the audience, attention, and data generated by its 240 million weekly shoppers. This is a fundamental transformation, and the market has not fully priced it.

Walmart Connect (Advertising): Walmart’s U.S. advertising business grew 44% year-over-year excluding the VIZIO contribution — and when VIZIO’s connected TV inventory is included, global advertising revenues grew 37%. Marketplace sellers grew their advertising spend by over 50%, corresponding to a meaningful lift in their sales volumes. The VIZIO acquisition, completed in 2024 for $2.3 billion, is now demonstrating its thesis: by combining first-party purchase data from Walmart’s stores and app with connected TV inventory from VIZIO’s SmartCast platform (found in tens of millions of American living rooms), Walmart can offer advertisers a closed-loop attribution model that rivals anything available on digital platforms. At approximately $8.7 billion in annualized advertising revenue (based on Q1 FY2027 growth of 37% over the prior year), Walmart Connect is now a larger retail media network than most pure-play digital advertising companies.

Membership (Walmart+): Membership and other income grew 27% to $2.07 billion, with global membership fee revenue rising 17.4%. Walmart+ continues to expand its value proposition — unlimited free delivery, Paramount+ streaming, fuel discounts, prescription savings — and renewal rates are strengthening as the service matures and members internalize its embedded discounts. The service’s unit economics are favorable: a member who pays for Walmart+ shops more frequently, has a larger basket, and is significantly more likely to engage with Walmart’s digital channels, generating both direct fee revenue and indirect advertising and marketplace revenue uplift.

Walmart Luminate / Scintilla (Data): Less visible in the headline numbers but strategically significant, Walmart Data Ventures operates a supplier-intelligence platform called Luminate — rebranded to Scintilla in early 2025 to reflect its shift from retrospective reporting to proactive AI-driven recommendations. Suppliers pay Walmart for access to cleaned, aggregated first-party shopper behavior data across Shopper Behavior, Channel Performance, and Customer Perception modules. This business carries extremely high margins (the marginal cost of an additional data subscription is minimal), is expanding internationally to Walmex and Walmart Canada, and represents a long-duration monetization optionality that sits almost entirely outside Walmart’s current valuation frameworks.

06 — eCommerce: Closing the Gap