Rivian: Could be the strongest competitor to Tesla, but has to prove itself through ‘’production hell’’

Rivian: Could be the strongest competitor to Tesla, but has to prove itself through ‘’production hell’’

and... is it really worth the $150b that had just a few months ago?

Update: Since the original publication of this article we have also published our analysis on their Q2 earnings, you can read that here: Rivian: Q2 Earnings

Rivian was founded in 2009 by Robert "RJ" Scaringe, the original name for the company was Mainstream Motors and later changed to Rivian (Good decision). The company first delivered vehicles in 2021. So it spent the first 12 years of its life without revenue from car sales. Rivian had its IPO in November 2021, raising $13.5b. Rivian’s IPO was priced at $78 ($66.5b) but on the first day of trading opened at $106.75 and closed at $100.3. The next few days Rivian kept on climbing and eventually reached a high of $179.47 or about $150b in market cap, remember that they have barely delivered any vehicles. At the day of writing Rivian trades at $29.5 ($26b) that is a drop of 84% from its high and considerably below their IPO price of $78.

Rivian previously raised about $10.5b in pre-IPO financing rounds, this plus the $13.5b from the IPO would leave the total raised at $24b

Business Model:

Current business model for Rivian is simple, but future revenue streams will start to change that. Possible revenue streams in subscription services, transportation, charging, etc.

Rivian will start servicing markets in the United States, Canada and Western Europe

Products:

Currently Rivian offers 3 type of vehicles:

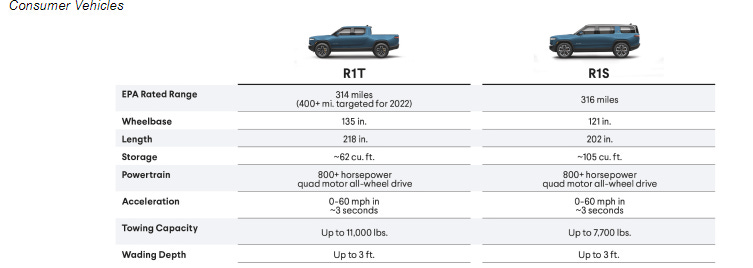

Rivian R1T: Starting at $67,500, R1T is capable of carrying five passengers and large loads with a bed that is 54 inches long with the tailgate up (84 inches long with tailgate down) and 50 inches wide.

Rivian R1S: Starting at $72,500, R1S is an all-electric SUV, capable of fitting up to seven passengers. Utilizing the same battery, propulsion, and chassis systems as the R1T. Equipped with Driver+, their autonomous driving features, geofenced to only highways. In the future it will be expanded with OTA SW updates.

Electric Delivery Van (“EDV”): designed and engineered by Rivian in collaboration with Amazon.com, the EDV is a long-range, electric commercial step-in van designed for deployment in a centrally managed fleet. Amazon has ordered an initial volume of 100,000 vehicles globally. From their S1, there are three variations of the EDV planned so far, the EDV 900 (900 cubic foot),the EDV 700 (700 cubic foot) and the EDV 500 (500 cubic foot) The EDV will be exclusive for Amazon in terms of last mile usage. Meaning for example, Fedex, Walmart, UPS, could not be a customer. But it could also find a market for small businesses (think about a small bakery in Europe or a plumbing service etc.) and other large businesses that are not related to last mile delivery

Fleet OS: end-to-end centralized fleet management subscription platform. It encompasses vehicle distribution, service, telematics, software services, charging, connectivity management, Driver+, and lifecycle management. This is a service to be offered to EVDs. FleetOS will add more features over time, including leasing, financing, insurance, driver safety and coaching, smart charging and routing, remote diagnostics, 360° collision reports, and vehicle resale

Charging: Charging vehicles throughout the nation. This will grow as they build more charging stations. They are expecting to build 600 sites or 3,500 chagrin stations

Accessories: Different types of accessories for their vehicles like cargo crossbars, rooftop bike mount, ski/snowboard mount, surfboard mount, roof tent, etc.

Emission Credits Programs: By placing EV vehicles in jurisdictions that allocated them (like California and Europe) Rivian will earn this credits that can be traded and monetized

Insurance: own insurance agency included as part of digital experience

Operational:

Selling of the consumer vehicles is direct to customers, meaning there are no dealers. As of now deliveries (maybe because there are still very limit amount of Rivian locations)

Placing orders is done online (Including customization, payments, etc.)

At the start they had many things outsourced, for example the design and manufacturing of the electric motors (from Bosch) and batteries from Samsung. They are continuing to try to become more vertically integrated.

Thousands of parts that Rivian purchases from hundreds of mostly single- or limited-source suppliers, for which no immediate or readily-available alternative supplier exists.

Currently they have a factory in Illinois with a capacity of 150K vehicles per year, this is split as follows

65K for the R1 platform

85K for the RCV platform (Rivian Commercial Vehicle)

Plan to open a new factory in Georgia with a maximum capacity of 400K vehicles a year. This will likely take into account affordable vehicles coming later in either 2024 or 2025.

Key Metrics / Performance

Highlights from recent performance:

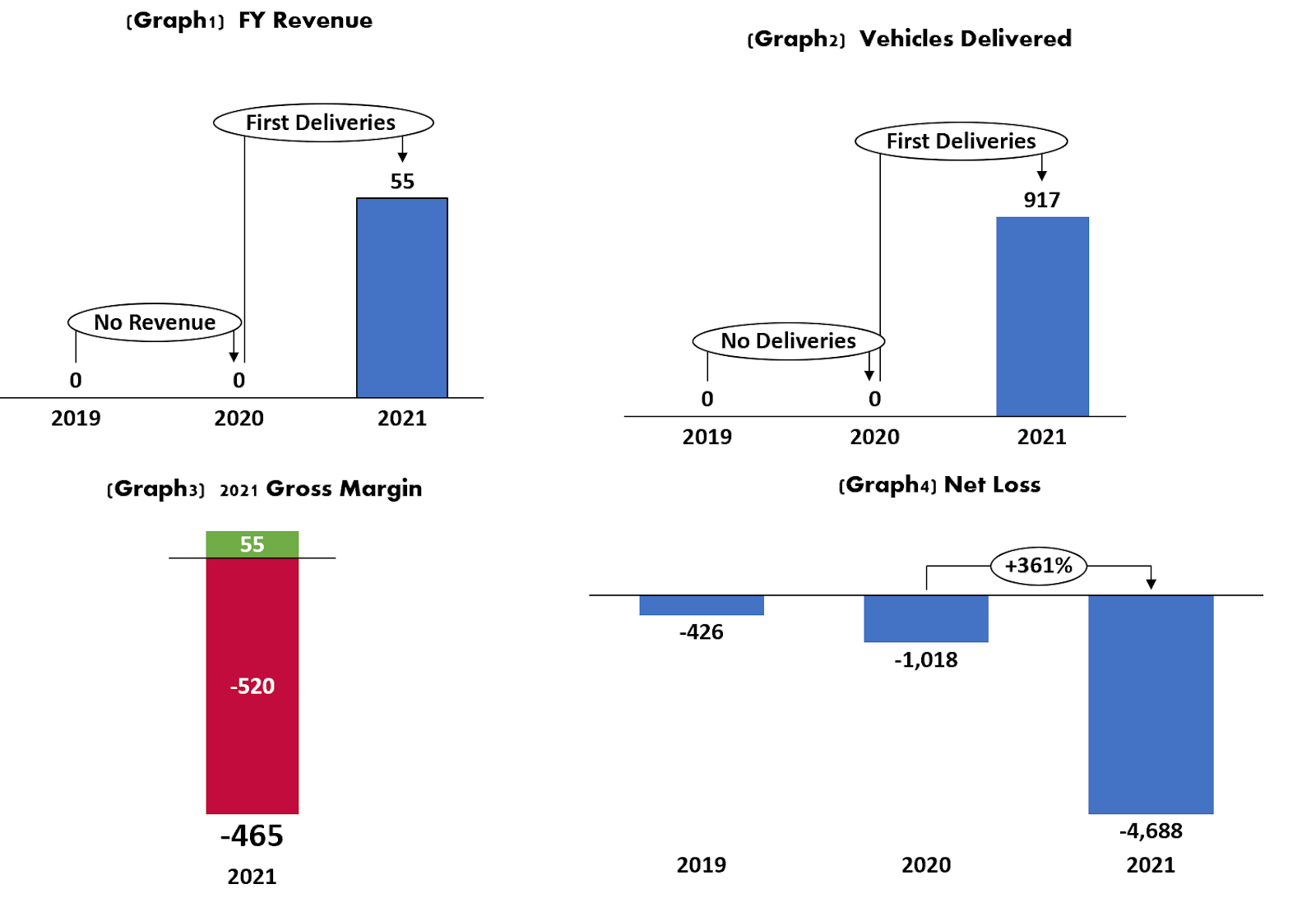

Rivian delivered 909 vehicles in Q1 2022

Rivian reported $95M of revenue in Q1 2022

The company has delivered 2,147 vehicles in its history

They produced 1,002 vehicles

Revenue figures so far are very insignificant since they have not delivered many vehicles yet, but what we see in the graph 3 below is that the cost of revenue was $525m in 2021. Considerably above the $55 m in revenue. This is mainly due to the scale, their factory has a capacity of 150K vehicles per year, and so far much of the cost of running the factory (even at a low production rate) is considerably above the small number of deliveries generating revenue.

They currently have about 100K open orders with amazon for the EDV and about 90K orders of the R1s

Pricing Issues:

Rivian announced a price increase in Q1, after the price increase (on March 1st) they received 10K new orders with an average price of $93K. Despite the 10K added orders the net increase in orders were only about 7K, which implies that they had some churn due to the price increase

Rivian’s price increase was drastic, up to 20%. Their intention was to apply this price increase to all their open orders, but customer response was extremely negative and in order to avoid further brand damage Rivian retracted and announced that they will honor the original pricing for any order before March 1st 2022. The price increase applied only if you want to have a dual motor configuration in your vehicle.

If a customer placing an order today wants to go for the lowest price configuration currently offered, they would need to wait for delivery in 2024. Since Rivian won’t deliver new orders for the single motor in 2023. So basically the starting price is not available for the next two years and making it less attractive for marginal buyers.

Cash Burn?

Like any other start up and specifically for startups in the car manufacturing business. Cash burning is really important. Tesla is the first car manufacturing startup that managed to survive in over 100 years. So it is not an easy industry to get into.

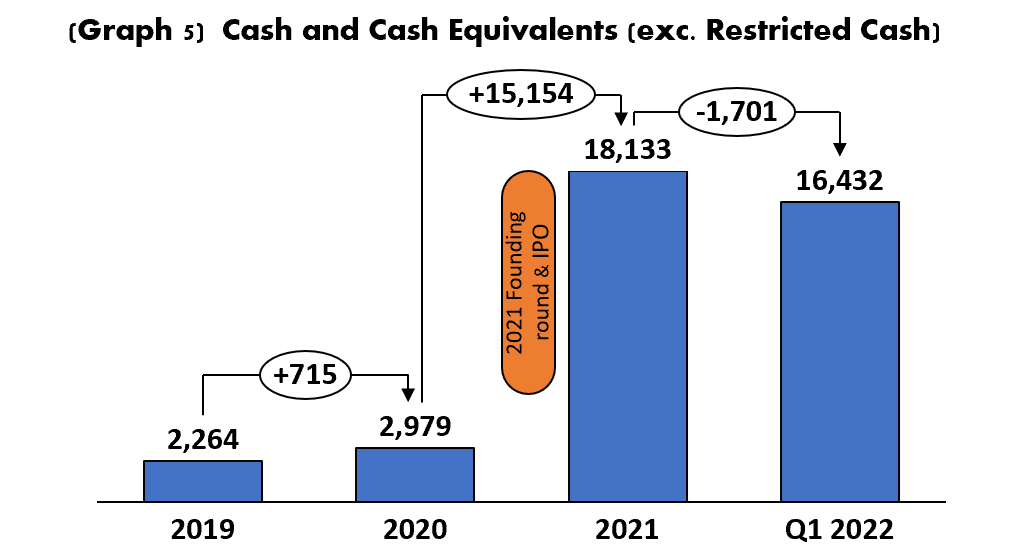

Rivian so far has raised in its life about $24b. At the close of Q1 2022 they still have about $16.4b. Since the IPO, and since the start of vehicle delivery, Rivian has started to accelerate their burn rate. For the last two quarters they have had an accumulated net loss of $4b. We must take a look at where their money is going and how long they could sustain this.

When looking at the P&L we notice that:

Cost of Sales for Q1 2022 was $597,as mentioned above there is still very little scale for their factory size vs. the size of their deliveries.

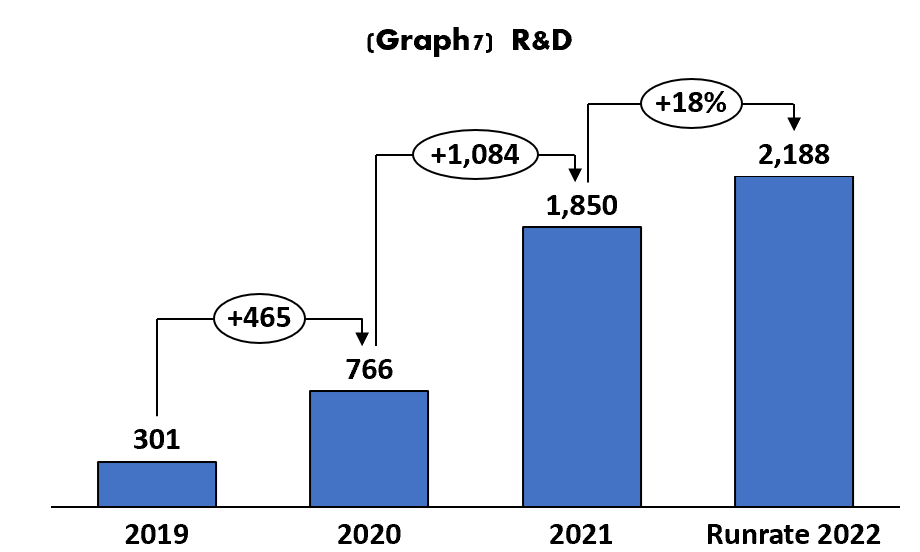

Below gross margin, most of their money is going to R&D and SG&A (Selling, General and Administrative)

These two comprise almost $1.1B of the $1.6B loss of the period.

The Year before (2021) Rivian put $1.8b in R&D and $1.2b in S&A, most of their money going into these two.

When looking at both R&D and S&A closely, we noticed that there is a big percentage of these expenses that are financed via stock based compensation. The following table we can see that 25% of the R&D and 32% of S&A. It is important to keep track of this. The more they finance this type of activity in the P&L through equity, the more the shareholders will be diluted, and 317 million of the expenses in the P&L represented close to 20% of all expenses in the quarter.

What to expect for 2022? How much money is expected to be ‘’burned’’ this year?

The Guidance they gave for FY 2022 is -$4.75b Ebitda

They have guided 25K deliveries. That could be around $2b in revenue

From that level of revenue to the -$4.75b guided there is a difference of about $7b in expenses.

Cost of Revenue margin should increase since 24K of the vehicles are still pending to be delivered so the scale should improve considerably.

R&D it should remain close to $2b if they continue current rates

S&A will definitely accelerate more since they will have a lot more deliveries and as of now nearly all deliveries are done at the customer's home.

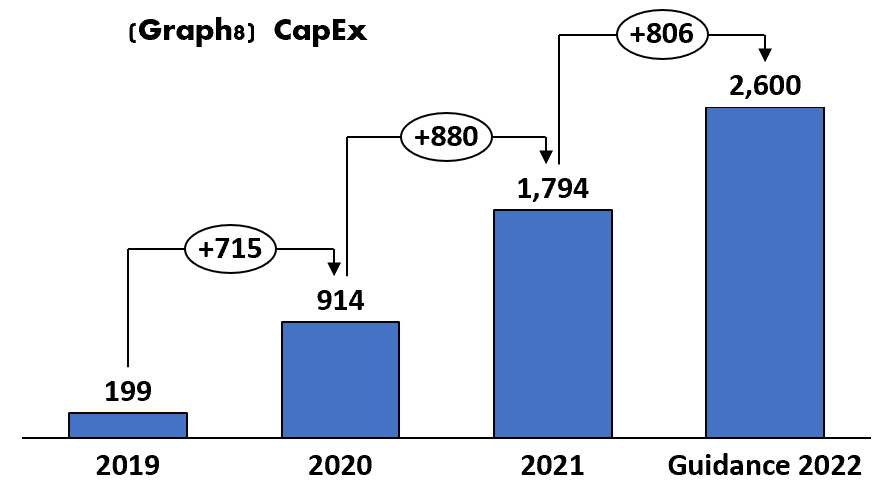

Capex will also be a big investment for 2022. In Q4 they invested $418M and in their latest earning call they confirmed their guidance for CapEx of $2.6b. So it will definitely accelerate from here.

With the negative Ebitda and CapEx they will bring down their cash by at least $7.3b leaving them with around $10.8b by the end of Q4 2022. That would leave still a lot of cash, but during 2023 revenue must accelerate considerably, because they cannot have a lot of $7b years

Competitive Landscape

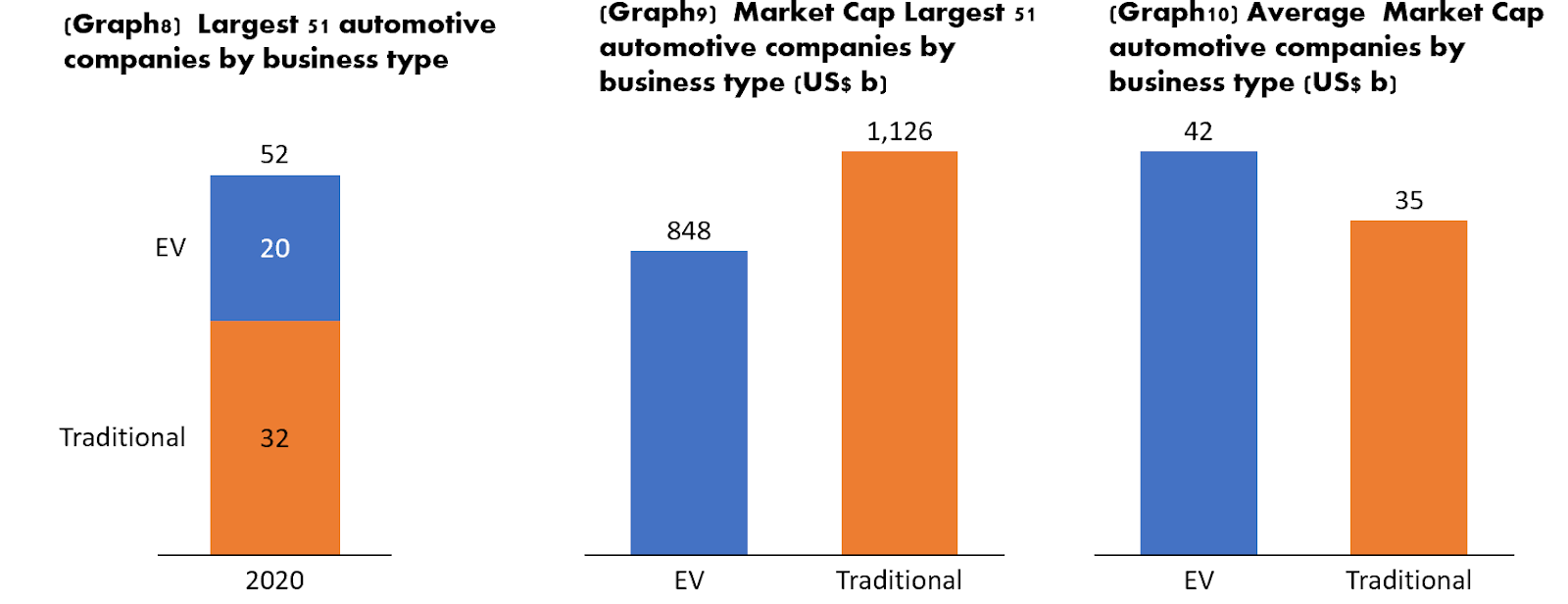

First, let's have a look at the market cap of the largest 52 automotive companies. This list includes both Electric and traditionally combustion engine companies.

A few things that are striking from graph 8 to 10:

EV companies are already 38% of the top 52

The combined market cap of EV companies is close to equal when compared to Traditional companies. Which is crazy considering that traditional companies deliver millions of vehicles every year. Many times the amount EVs. Investors clearly are focused on potential

Average market cap per EV company is higher than the average of a traditional company. Just amazing!

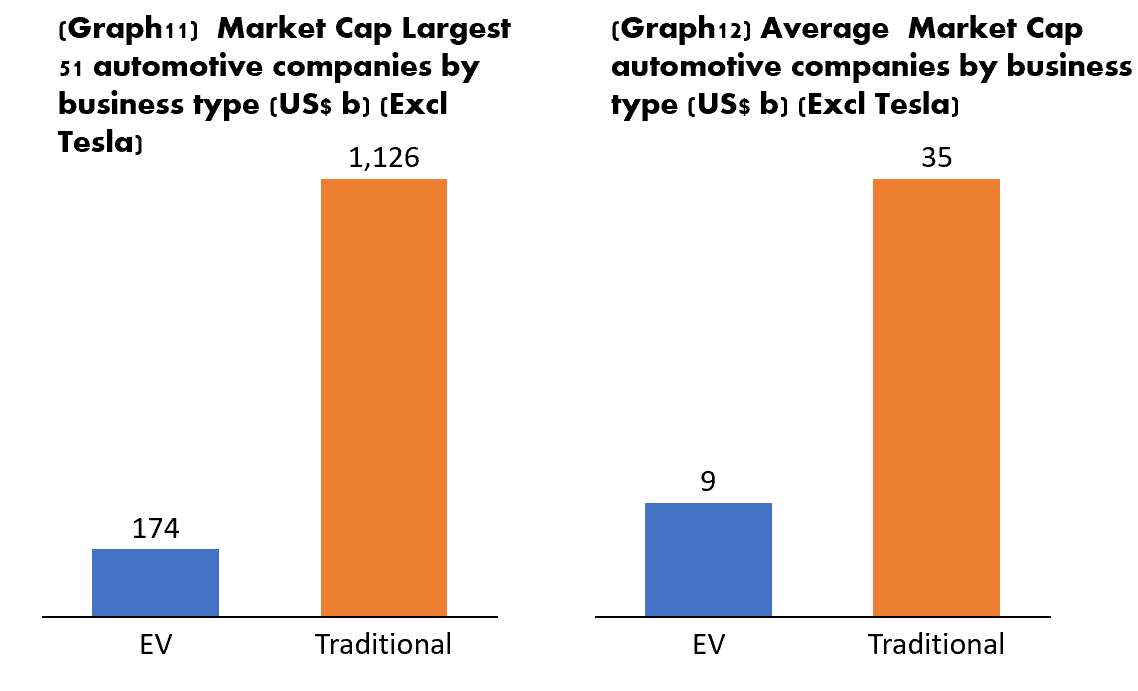

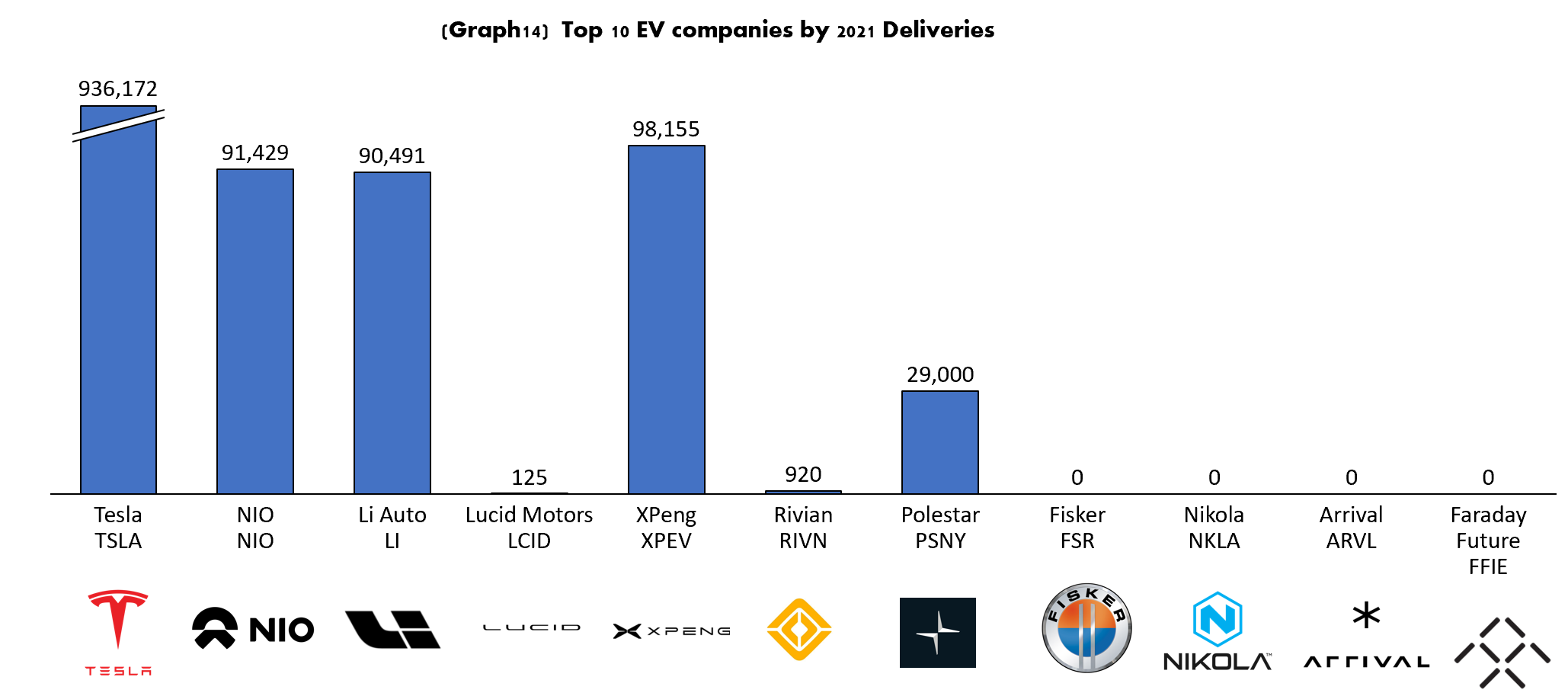

We know Tesla is a big part of the market cap of EVs (and deliveries) but let's have a look at the same graphs, excluding Tesla. The numbers as presented in graph 11 and 12 become more reasonable. But still, the amount of deliveries in these companies is still very low. Both Lucid and Rivian have delivered less than 5K vehicles and they make $50b of the $174 b market cap below

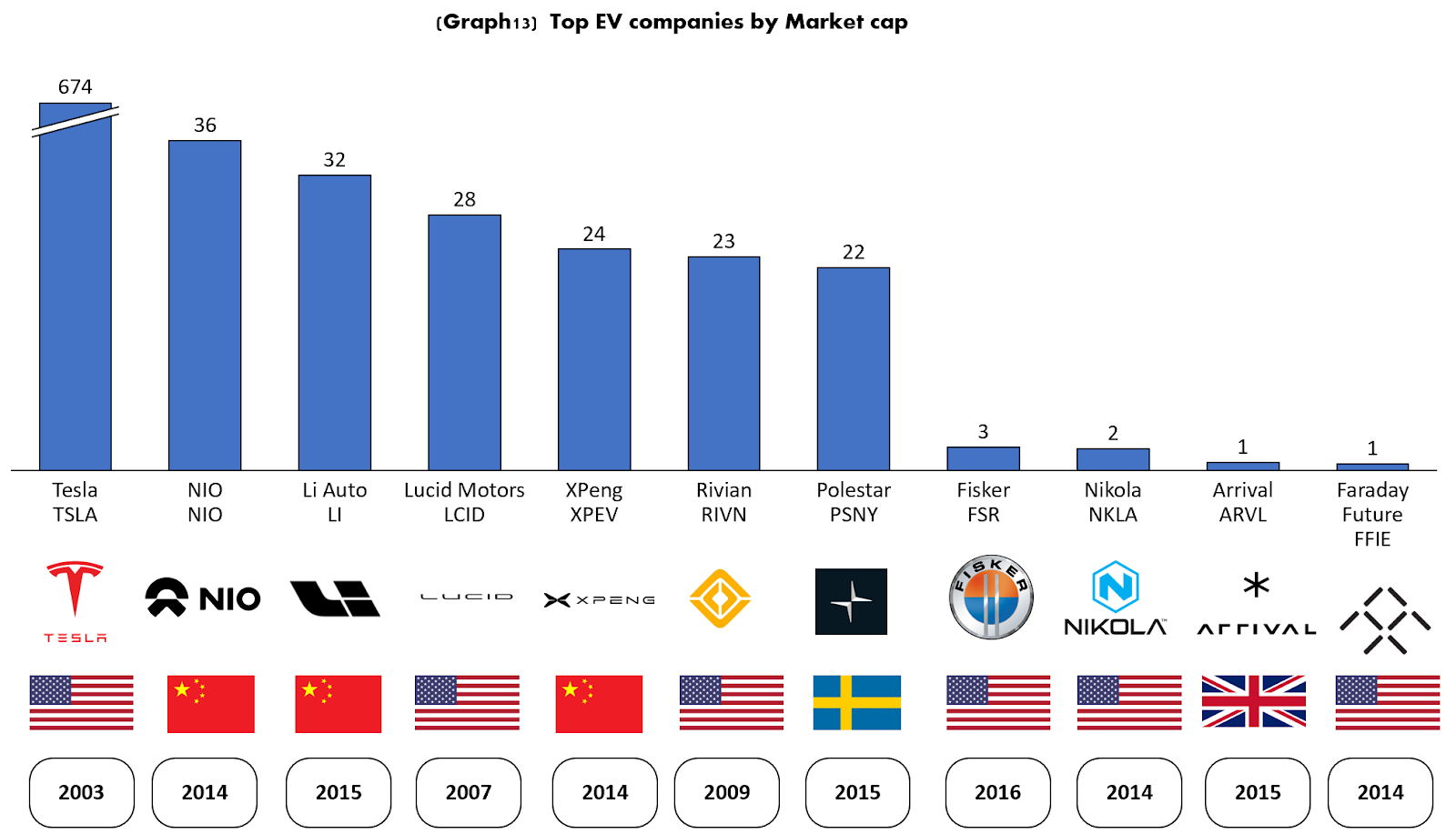

The EV market is dominated by China and the US, and deliveries, at least for now, are focused on only four companies, Tesla, Xpeng, Li, and Nio. They are followed by Polestar, Rivian and Lucid. Rivian and Lucid delivered a very limited number of cars in 2021, but are guiding to have 10K to 25K vehicles this year. Their current market caps are ‘’based’’ on the fact that they are already delivering while the rest are still pre revenue.

Tesla is in a league of its own. It is the leader in this category and has been selling and producing cars for a while. Tesla is clearly the leader worldwide in EVs. Everyone is trying to catch Tesla.

Revenue has a clear lead from Tesla, they hold still 79% of the share of the EV market (Graph 16) Out of the companies that have ramped up production already, Tesla has the highest P/S ratio. If Tesla were to drop to the closest competition levels the stock would still drop by 40%. If the three Chinese companies would go to Tesla's P/S level then their stock would go up by about 67%.

Lucid and Rivian both would expect to have a lot more revenue in 2022 since they are both in the middle of a ramp up in production. Rivian has guided to 25K deliveries in 2022. That would be something around $2b in revenue, hence, the forward P/S ratio for Rivian today is around 11.5, similar to Tesla’s

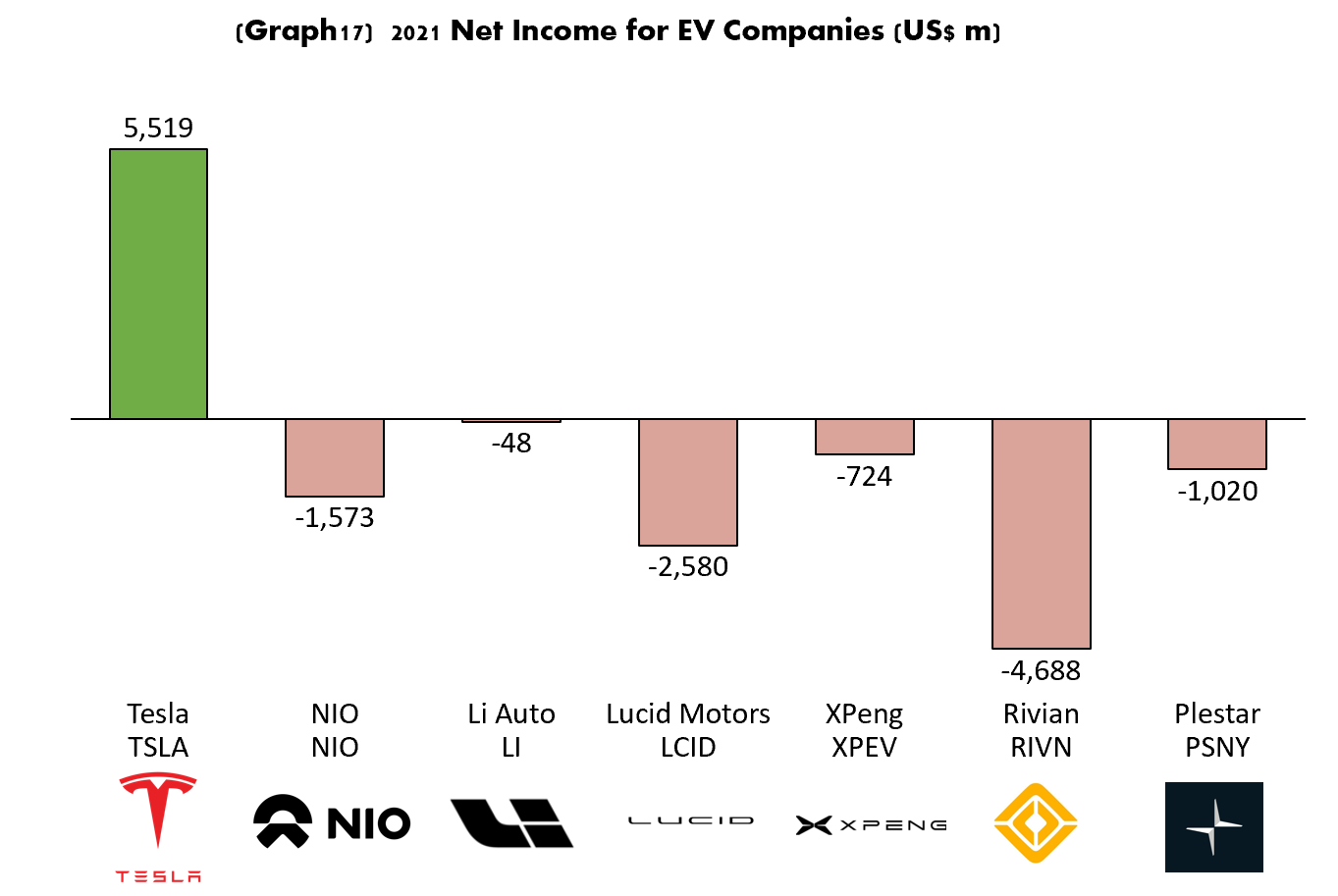

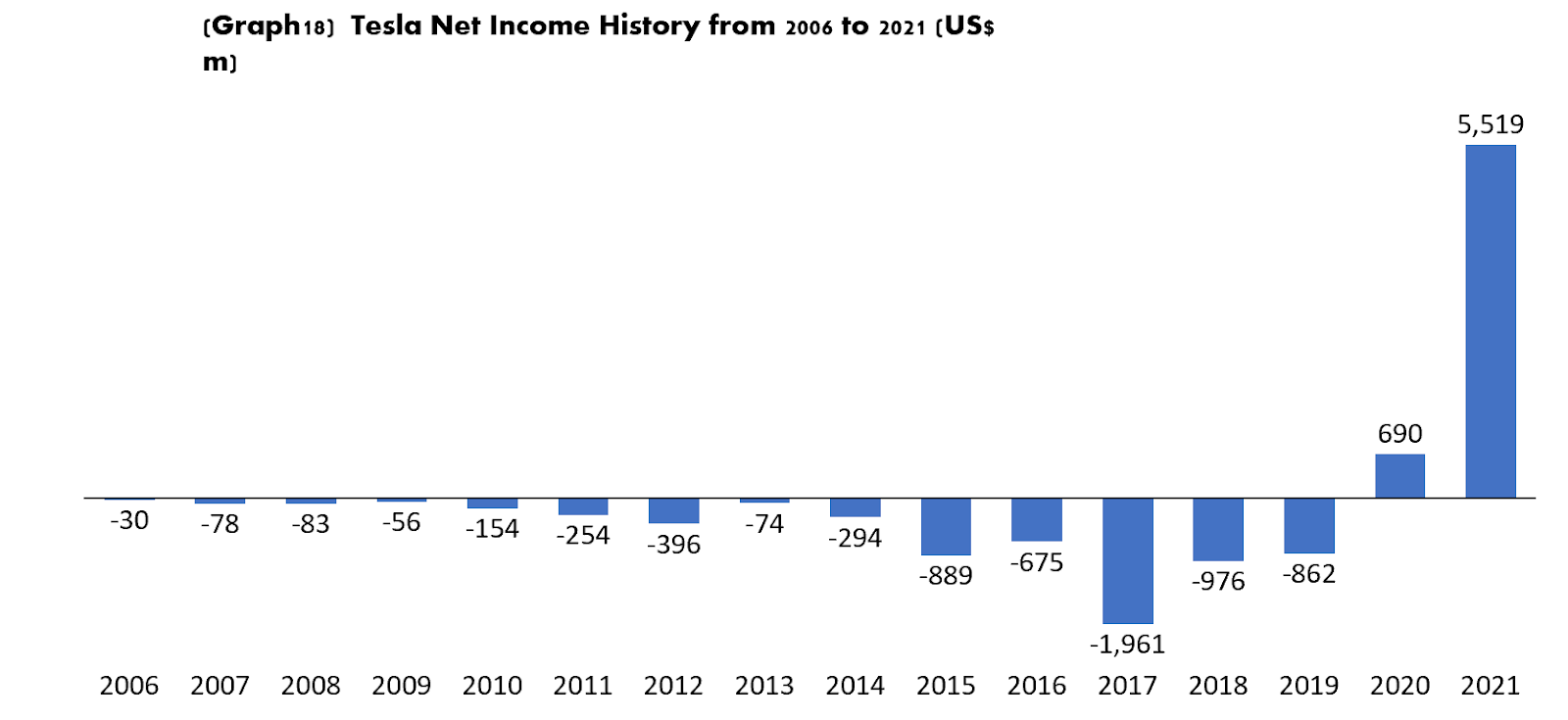

Regarding net income we see in graph 17 that only Tesla had a positive return for 2021. Even companies that are delivering close to 100K vehicles per year are still losing Money. This raises the question for Rivian on how many quarters / years will continue losing Money? To have an idea let's have a look at how many years it took Tesla to start turning a profit. From 2006 to 2019 Tesla accumulated $6.8b in losses. It was until 2019 that Tesla started to be profitable. This was the year that Tesla delivered 500K vehicles.

Production Hell

Rivian is about to enter what Elon Musk called “Production Hell”. That is the time where a ramp up in production is expected. Elon Musk says that it is very easy to produce a perfect car when there is a small amount of cars to produce, but when you produce a lot they will ‘’suck’’.

On top of that, Rivian is already struggling producing cars due to supply chain issues around the world. Rivian uses over 2,000 parts from over 400 suppliers, semiconductors and plastic parts have already had an impact. They have already changed their original target of 50K deliveries this year to 25K. They mentioned in one of their latest earning calls that they will produce as many vehicles as they have semiconductors. So don't expect a much higher amount of deliveries next year if they don’t get this semiconductor issue in order by 2023. Tesla for example, coded new software, so that their vehicles are compatible to semiconductors that are more highly available, instead of the ones that have a shortage. This is possible since Tesla’s vehicles are considerably more vertically integrated than today’s Rivian.

They are spending a lot of money to accelerate delivery of parts and to be able to reach their 25K. The next few quarters the good news in this department will have to start to come, otherwise 2023 won't look terribly different. They must think this will improve since they are still committed to deliver their original open orders by the end of 2023. (around 50K orders from before the IPO)

Automotive Market and EV Market

Automotive Market

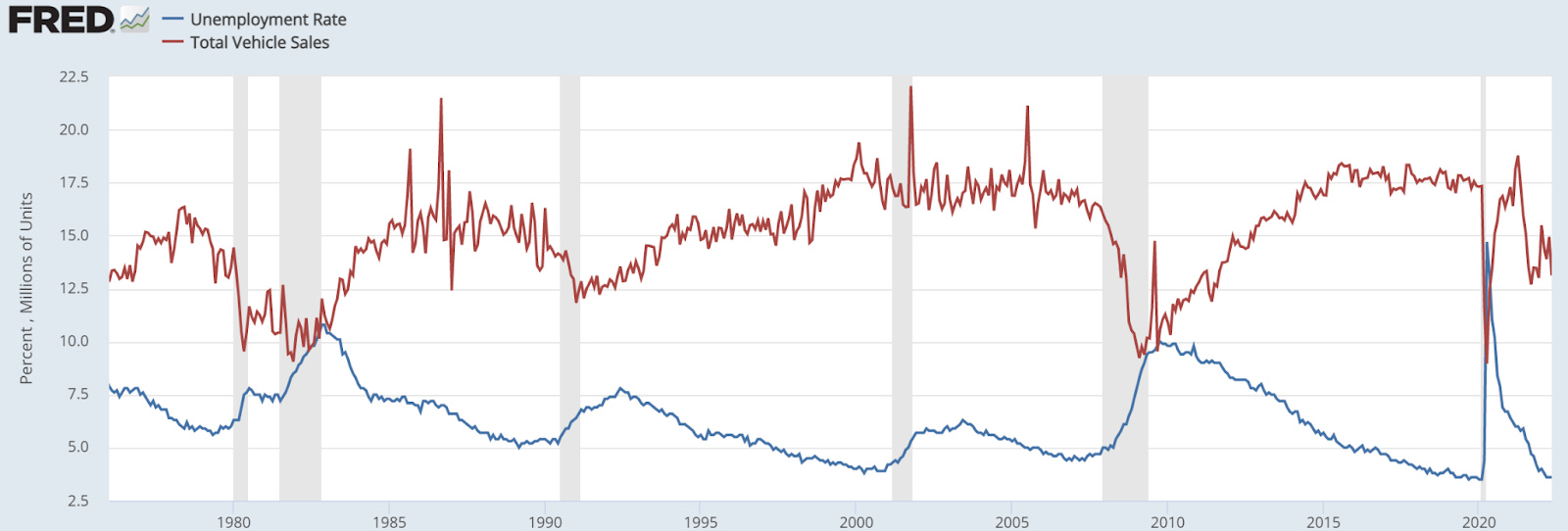

The United States market sells between 10m to 17m vehicles per year. That wide range is highly dependent on the economic conditions of the country. People in recession tend to avoid replacing their vehicle. When unemployment rises by a significant percentage the sales of vehicles tend to drop considerably.

(Graph 20 Vehicles Sold vs Unemployment)

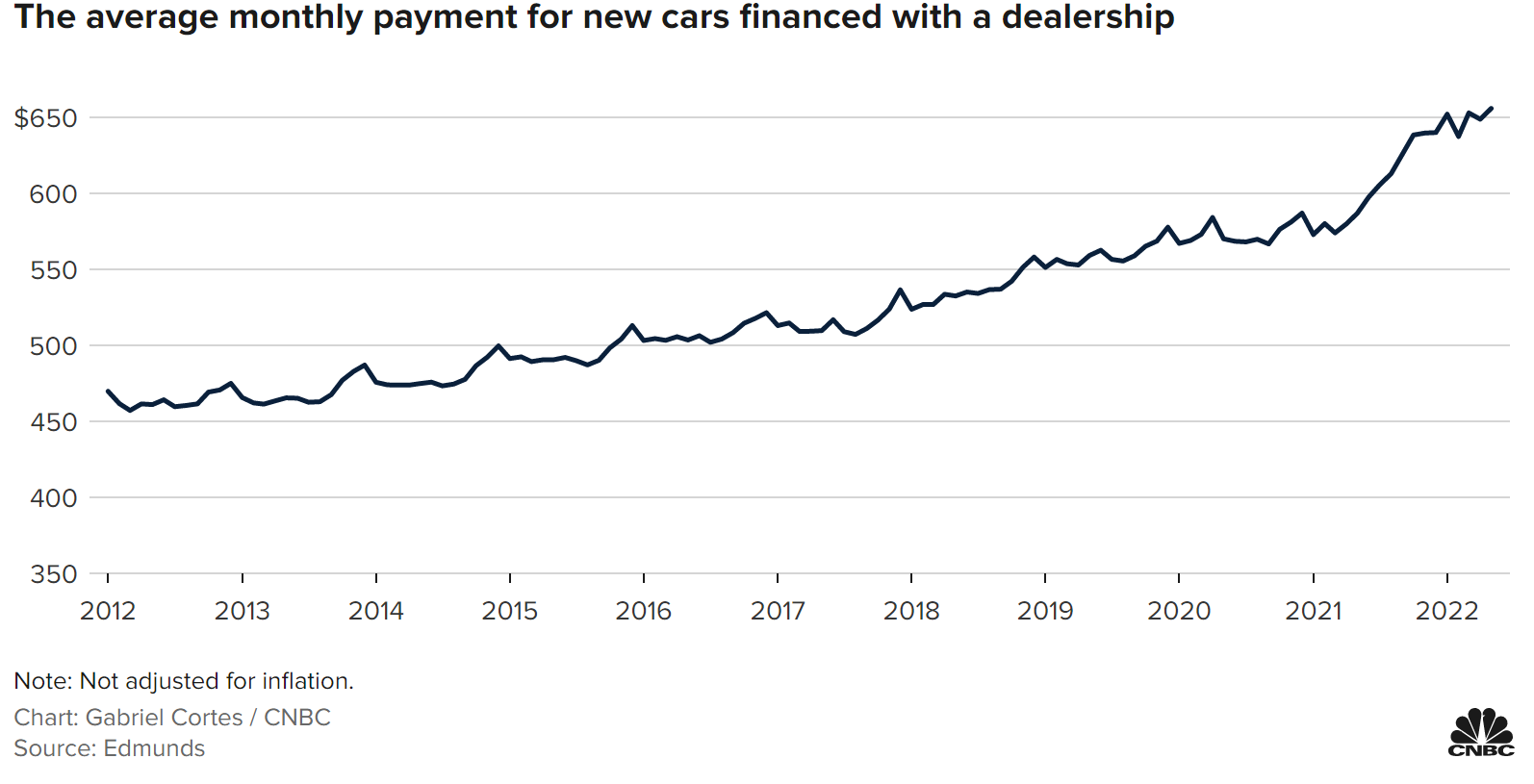

Currently there are two other forces impacting the overall vehicle market. Inventory is very low (Covid 19) and debt cost is starting to rise, and fast. Just look at the average monthly payment to finance at a dealership for used cars, it has skyrocketed from $411 pre pandemic to $546 (average rate of 8.2% and loan length of 70.8 months) and for new cars from $569 pre pandemic to $656

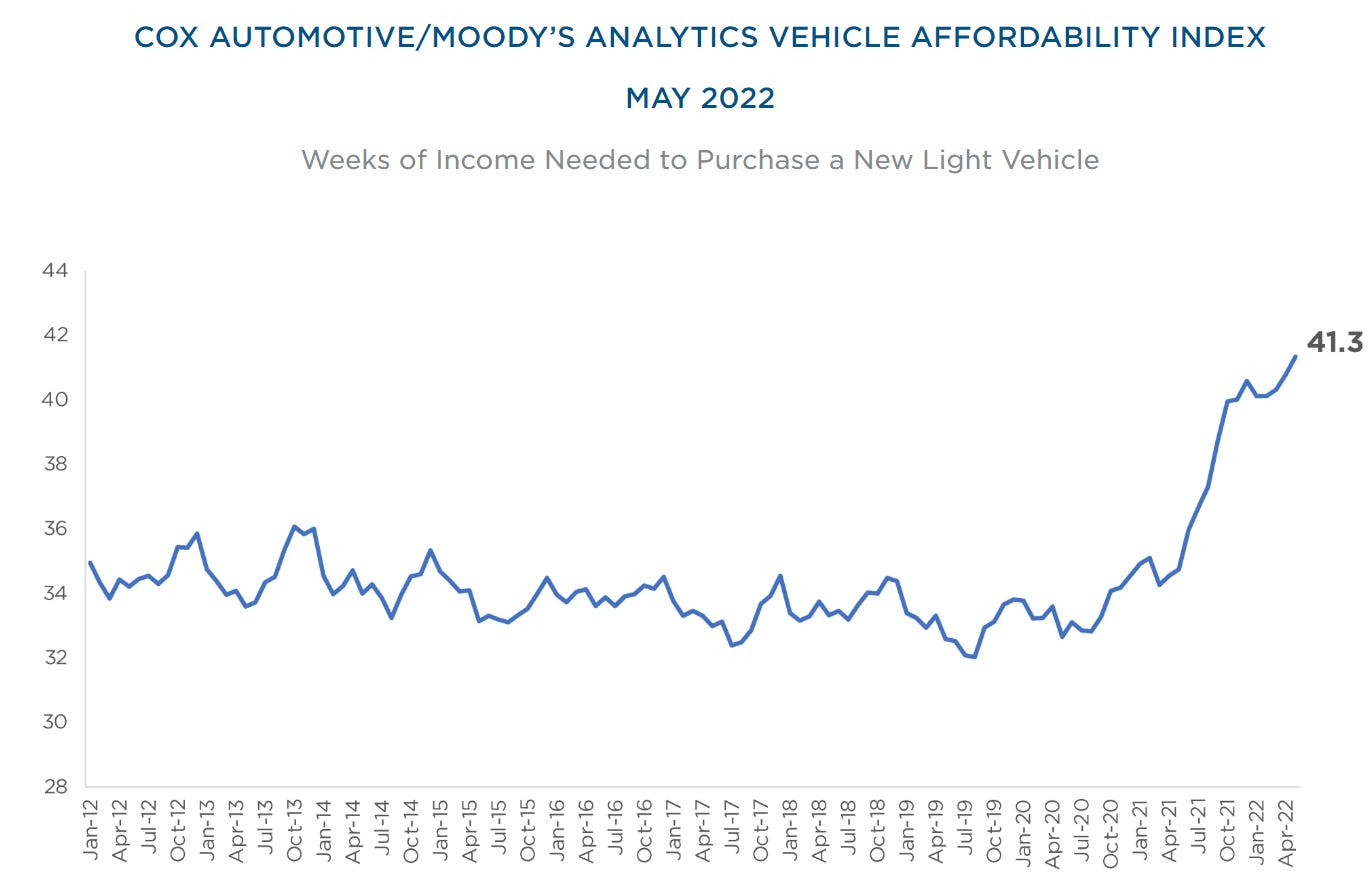

The affordability index is also having a dramatic rise; it has now reached 41.3 weeks of income to purchase a light vehicle.

We definitely would expect that a drop in demand will be coming for the rest of 2022 and perhaps 2023. That impact is already seen in repossessions that are already back to around 2m this year

EV Market

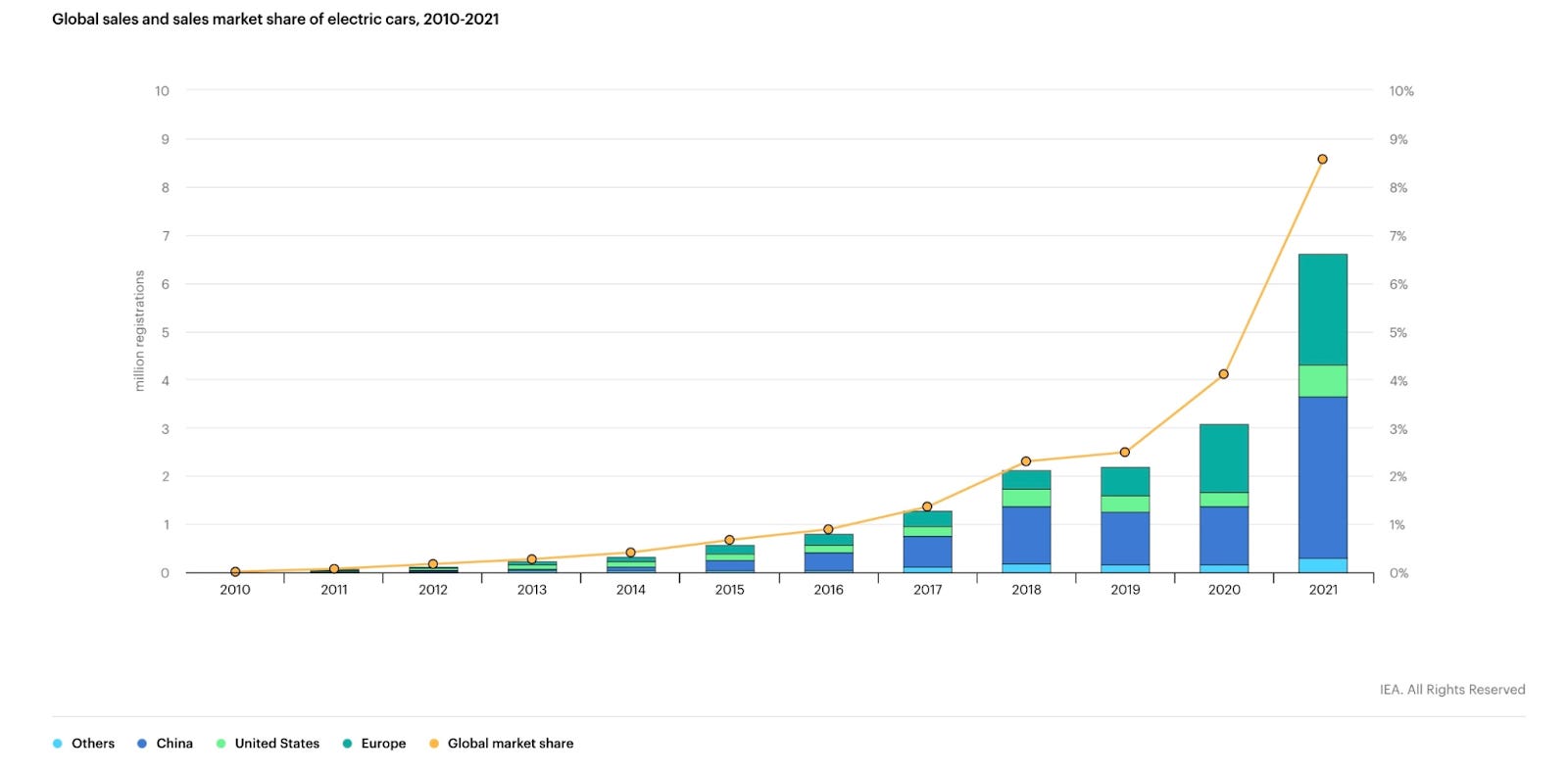

The EV market has grown fast in the past few years. Penetration in the US is still low at around 2 to 4%. In Europe this is much higher at around 10%.

There is no sign yet that the new offer of EVs are growing the total light vehicles market. For now, they are growing by simply penetrating the existing markets while replacing combustion engine vehicles. Even traditional companies themselves are pushing for this (i.e. Hyundai Iqonic, Ford Mustang Mach e, Hummer EV, Ford F 150 Lightning etc) The EV market will definitely grow as penetration of the total market grows, but it will be a factor of affordability that it will continue to determine the speed at which the EV market grown.

Rivian’s vehicles, at least the one being sold to the consumers now, are classified as Luxury or high end vehicles, this is 4.5% of the total US light vehicle market. (Around 675K Vehicles per Year)

Where does Rivian go from Here?

First of all Rivian has to solve their current production issues. After that they will be in a much better position to what is next. They need to start generating consistent revenue.

Their revenue will come in the first years from the three types of vehicles that they are producing right now.

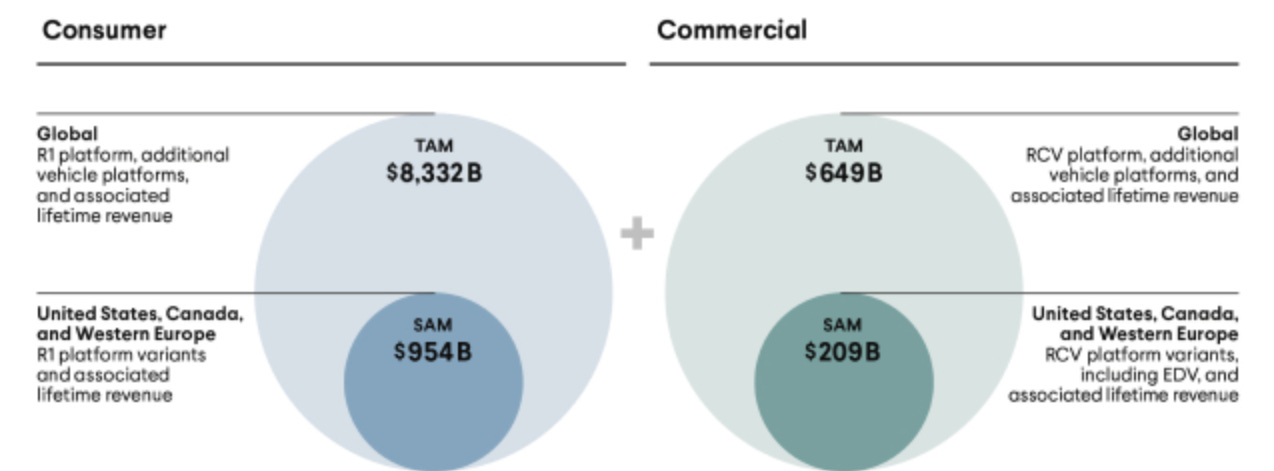

To have a better idea of the future of Rivian we looked at their S1. In their S1 they detailed the size of their TAM (Total Addressable Market) and SAM (Serviceable Addressable Market) as follows:

Consumer:

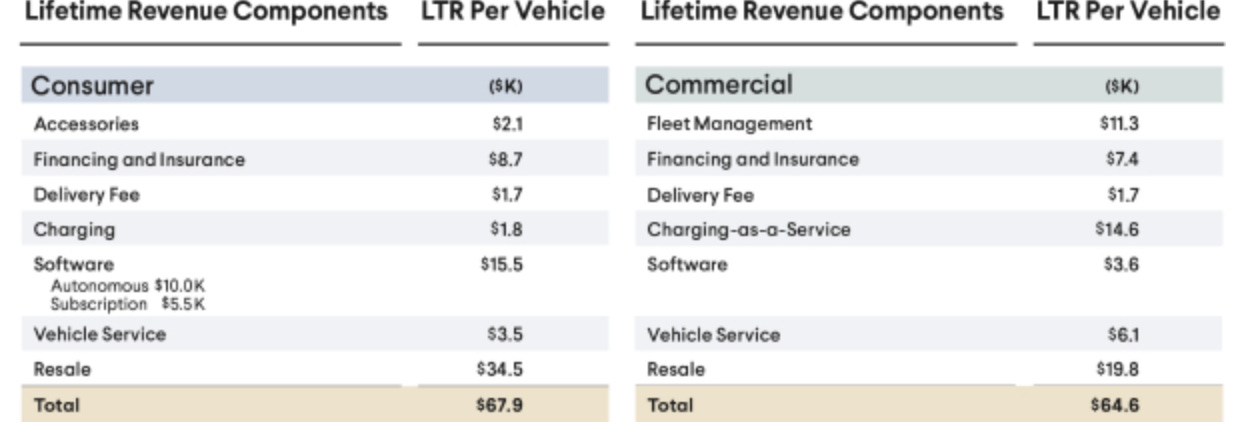

‘’Our Consumer TAM consists of market sales of 81.1 million new vehicles per year and the $67,900 LTR potential of their associated services, representing an estimated $8 trillion global market opportunity.’’

‘“Our Consumer SAM consists of market sales of 7.9 million new vehicles per year and the $67,900 LTR potential of their associated services, representing an estimated $1 trillion market opportunity in the United States, Canada, and Western Europe”

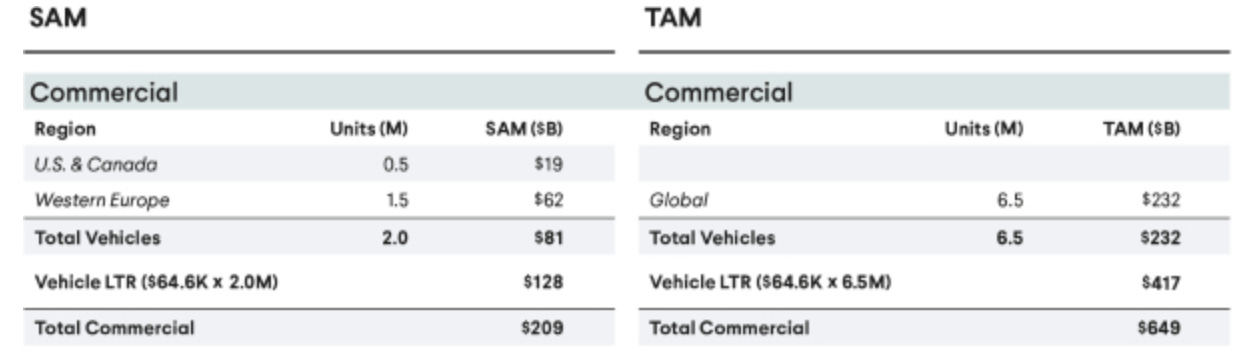

Commercial

“Our Commercial TAM consists of market sales of 6.5 million new vehicles per year and the $64,600 LTR potential of their associated services, representing an estimated $649 billion global market opportunity.’’

‘’Our Commercial SAM consists of market sales of 2.0 million new vehicles per year and the $64,600 LTR potential of their associated services, representing an estimated $209 billion market opportunity in the United States, Canada, and Western Europe’’

Lifetime Revenue Potential

Rivian defines LTR potential as the revenue it can generate from its Rivian vehicles throughout its lifetime (considered to be 10 years), if the owner, in this case, subscribes to everything possible. That includes Level 3 driving capabilities, and a monthly subscription plan for infotainment, connectivity, diagnostics, and other services

The assumed LTRs for commercial and consumer are shown below

Given that Rivian will initially focus on Western Europe, the US and Canada. The main SAMs are $1 Trillion for consumers and $209 billion for commercials.

Some of the possible risks for the company are:

They have not gone through “production hell” yet, and on top, they have Covid related supply chain issues. This could be a short term recurring problem (next 2 years) Their vehicles are great, they have a lot of cool features and cool new gadgets. But producing these on a massive scale will be challenging.

The total market of the current vehicles is more limited than they assume. Pickup trucks and SUVs are not really popular in Europe

Their current offer is expensive, the vast majority of the population is not able to afford any of the Rivian vehicles currently available, and more affordable vehicles won’t be offered until at least 2024. By then they could burn through more than $10B

The sooner they start with affordable vehicles the better. But with the current supply chain conditions, is it realistic that they will have something by 2024 or 2025? Without these, their revenue would be limited for a few years. Look at Tesla, it managed to break-even until they got their Model 3 manufacturing under control. Rivian in the very early stages of their first production vehicles.

TAM calculation is very optimistic. The trillions of TAM and SAM assumes 100% attach-rate for each service. That is not realistic, that is an inflated number which also includes retail and trade in which we can’t expect to have a huge margin. The more promising of the LTRs could be the autonomous driving and subscriptions services. But still won’t be 100% penetration.

Heavy stock compensation: Research and development and other expenses were financed via R&D during Q1. They mention that this is something lagging from the IPO, but is important to track in the next few earnings calls. Because if this continues, there will be very heavy dilution of shareholders.

Spoiled with Cash: They have a lot of cash. But this could be an issue long term. They don’t have the urgency as Tesla to be 100% efficient with every single part of the process and every single dollar available. This could accelerate their cash burn and damage their creativity to fix issues.

Recession: A recession is likely coming and car sales will be dramatically impacted, this can heavily slowdown new orders. We will see in the next two quarters

What could be the case for Rivian being a good opportunity for the next 10 years?

Their product is very good and the brand so far is very well positioned.

Cash is not an issue: Despite the fact they are spoiled, they are not in danger of running out of cash. That might make them more inefficient, but at least they will survive.

They are spending a lot of money, about $7b in 2022. The timing of their IPO was perfect. Tesla was being valued at more than a trillion dollars, enough to ‘’justify’’ raising $13.5b at a valuation of about $80b. In addition they have Amazon as a big investor with about 20% ownership and likely a recurrent customer. They have enough backing to give it a shot as becoming a comparable competitor to Tesla worldwide. (Not to mention that Ford is also an investor, they sold a portion but they still hold a very large percentage)

Better positioned to scale than Tesla. Tesla had to make a whole new category and had a lot less cash available. Rivian can leverage from all the groundwork made by Tesla on the EV field and the $17b in cash.

Affordable vehicles are coming : We expect that heavy investments for R&D and CapEx are going to the development of their second vehicle platform, which would be used for affordable vehicles. Rivian has already registered the names R2S, R2T, R2A, R2C, R2R, R2X. Deliveries are years away, but will be the main driver of growth.

Valuation

There are many EV startups trying to break into the market, but the likelihood that Rivian will be one of the successful ones is high. They have enough money, enough backing from serious investors and great products. The issue with Rivian and all EV companies right now is, right valuation.

Rivian is still almost a pre revenue company making it not a great candidate for fundamental DCF analysis. Their valuation could then be seen from two different lenses, Tesla’s and fundamental

Tesla Lens

Tesla Valuation in 2013, when they delivered 22K vehicles was at ~ $18b, when they delivered 33K in 2014 they were valued at ~$27b.

Rivian currently is trading at $26 b with an expectation to deliver 25K consumer vehicles this year and also a big amount of EDVs for Amazon. So in terms of valuation when compared to Tesla, you could say that right now they are correctly valued

Fundamental Lens

When taking a more fundamental approach we see that Rivian trading at $26b translates in the following assumed Ebitda:

For a company in the Auto industry the implied Ebitda is $1.3billion

The Ebitda is negative for now, but let's take their long term guide for Ebitda of high teens. Let's say 17% to be safe. At 17% Ebitda their revenue would have to be $7 billion. To reach this revenue they should be delivering about 77K to 87K deliveries. If we use their original target for 2022 (50K) their valuation would be around $14 b or $16 per share. They should be producing at least 150K cars a year in the next 2 years. That would take them to about $36b valuation or about $42 per share, but that highly depends on actually having the demand for 150K vehicles per year.

Rivian has come down from the sky high valuation that was definitely in bubble territory. Now it is closer to its reality. Rivian's previous valuation of $150b reminds us a lot about Cisco in the dotcom bubble. Cisco is a sound company that has continued to grow for the past 20 years. But it has never reached the market cap from its high of the dot com bubble

Rivian might be similar, at least for the next 5 years it will be difficult to get back. To get to $150 billion valuation Rivian should have a revenue of about $45 billion, that is more than 1 million deliveries. They don’t even have the factory capacity for that and also competition will get more and more complicated for EVs. Is not only coming from EV companies, is coming greatly from traditional ones.

Rivian has great cars and a lot of cash. They just need to execute. They will grow and will be a great player, just the $150 b valuation will not come back soon unless there is another easy money bubble created.