Rivian Q2: Earnings

Rivian Q2: Earnings

Not much has changed since last quarter, but at least now they can use the "Inflation Reduction Act" to increase prices like most of the EV companies are doing.

We covered Rivian on our deep-dive published July 11th called Rivian: Could be the strongest competitor to Tesla, but has to prove itself through ‘’production hell’’. This is a short summary and an update after their Q2 earnings were announced August 11th. During earnings Season we will do this short updates of the companies we have covered so far Opendoor Peloton Carvana Rivian Roku and UBER

The market response to Rivian’s earnings release has been a bit mixed. The stock closed at $38.95 just before earnings and closed at $38.90 the next day. Pretty much flat. But ever since that day Rivian has lost 17.4% trading at $32.11. Is this related to market conditions overall, is it specific to Rivian? We will try to answer this by analyzing and looking in detail at their latest numbers.

Performance Summary:

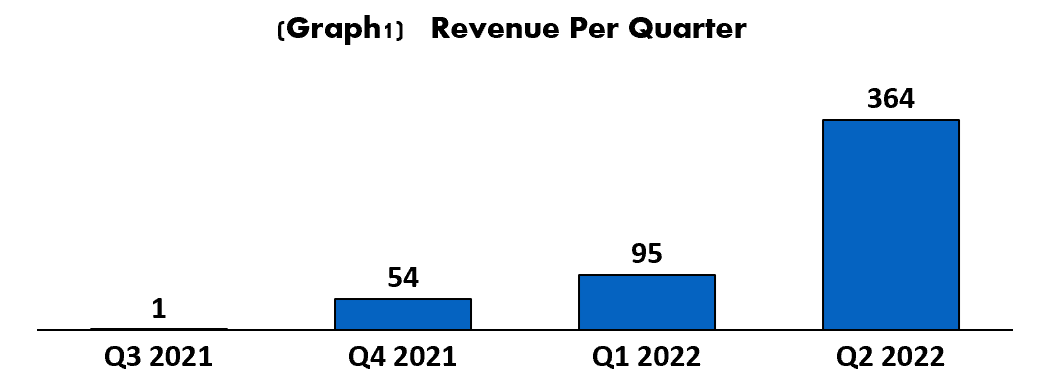

Revenue

Revenue for the time is very straight forward, Rivian has been actively delivering vehicles for very little time and the amount of vehicles that they have delivered so far is still very small.

Revenue for the period was $364m

Revenue per vehicle was $81K

With the second quarter of 2022, Rivian finally had one full year of revenue. The revenue for the previous twelve months was $514m

Key Metrics:

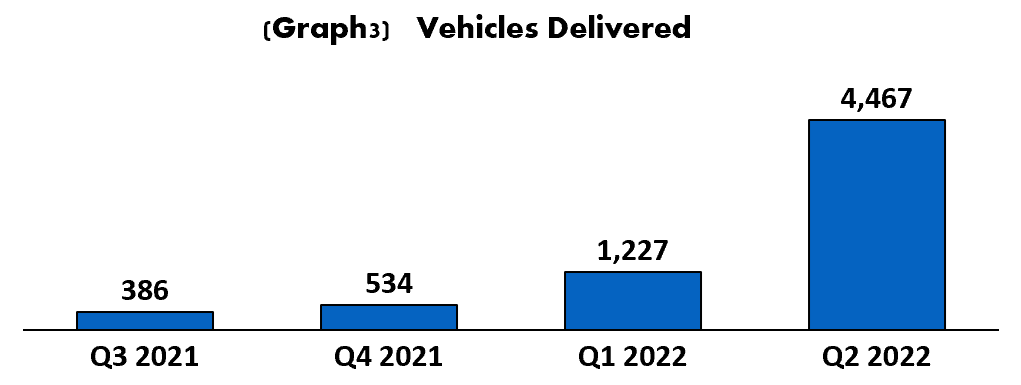

Rivian delivered 4,467 vehicles during Q2 2022. This includes booths Trucks, SUVs and the delivery vehicles.

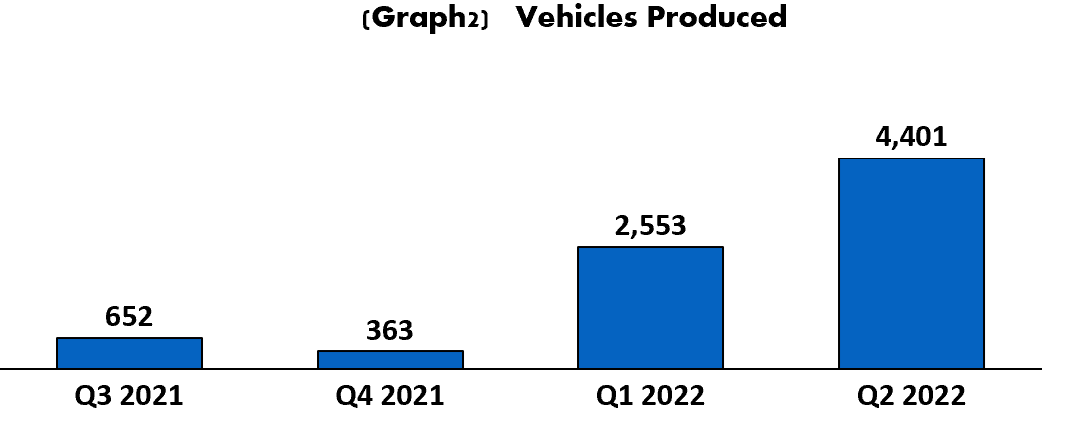

4,401 vehicles were produced during the quarter, up from 2,553 during Q1 2022.

Rivian and Amazon finally rolled out the EDVs 700 vehicles in about 12 cities in the US.

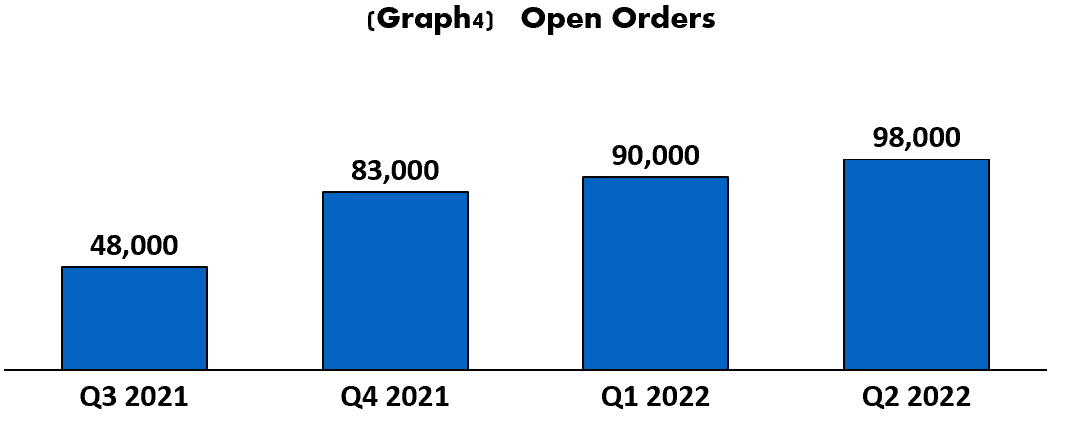

They closed the quarter with 98K open net orders. This is up from 90K previous quarter

They have accumulated 7,969 vehicles produced since the start of production.

They have accumulated 6,614 vehicles delivered since the start of deliveries.

25K production target for 2022 confirmed. This means that the second half should considerably accelerate the current pace.

Cost, Expenses and Cash Flow:

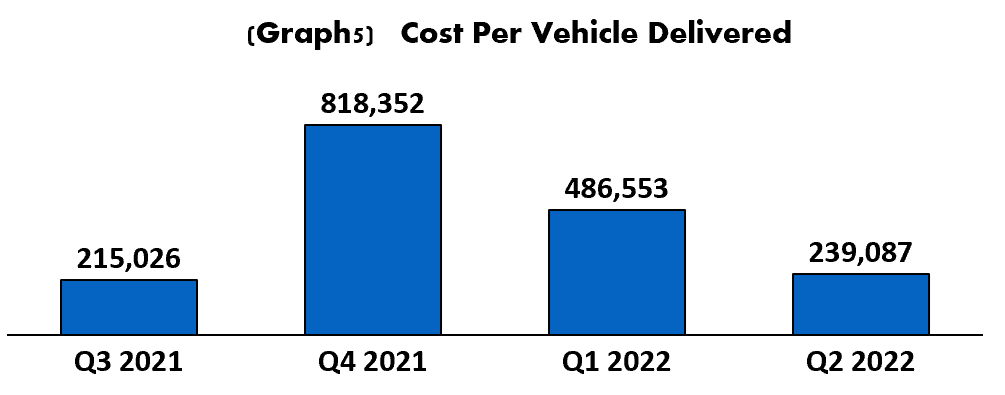

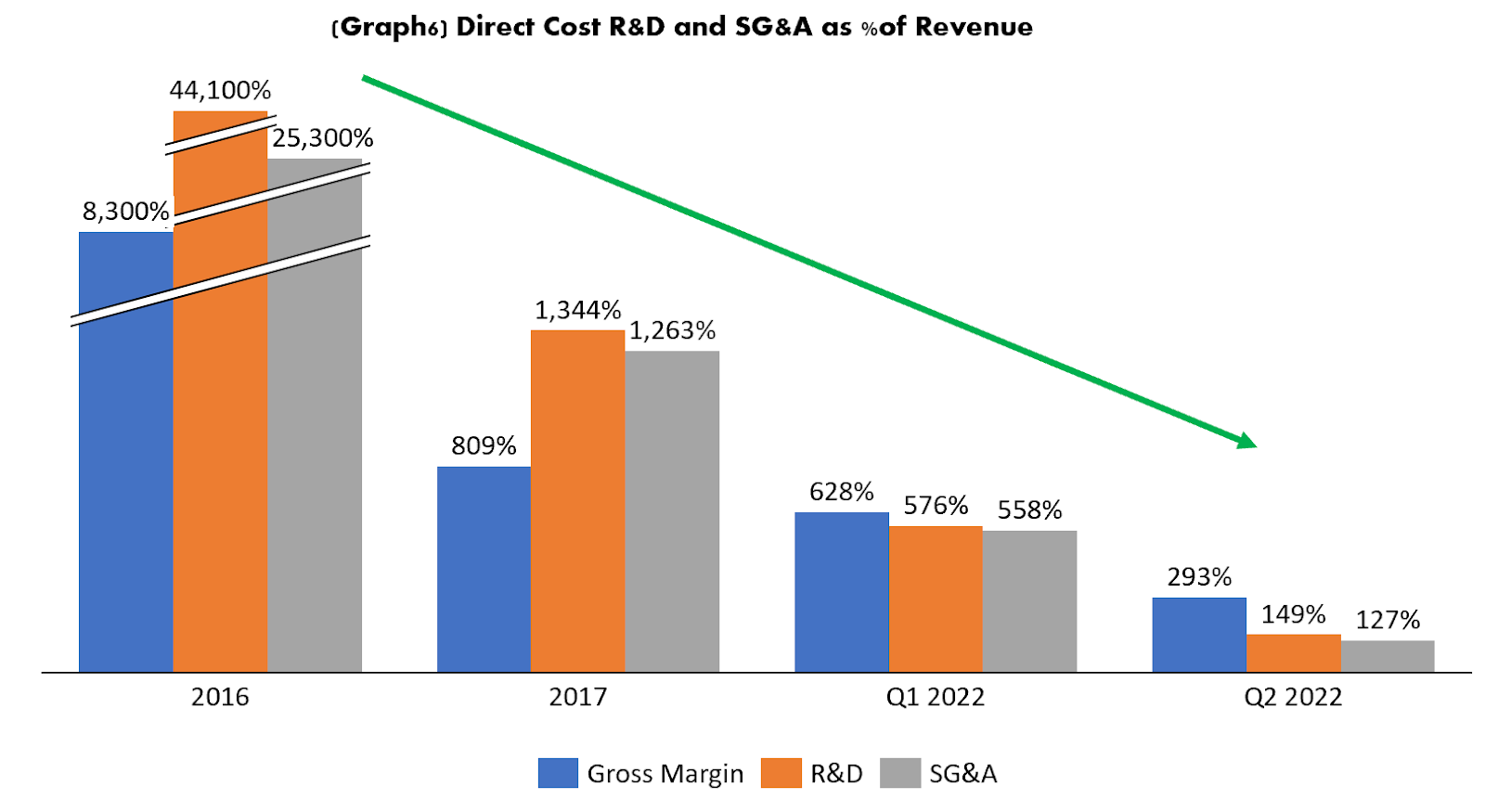

Direct cost for the period was $1b, considerably higher to the $597m from the previous quarter

Cost per vehicle delivered was $239K when calculating total direct cost divided by the number of deliveries. This was an improvement from the previous quarter that was $486K per vehicle. This should improve as they produce and deliver more cars. There is a lot of idle capacity that will continue to keep cost ahead of revenue as long as deliveries remain low.

They did mention in their calls that they do have some pressure on prices of materials, paying for expedited freight cost and higher cost than expected from ramping up four types of vehicles in two lines. Meaning, the cost per vehicle dropped, but it should have dropped a lot more with the better scale from producing more vehicles.

Gross margin falls to -193%, better than -528% in Q1 2022

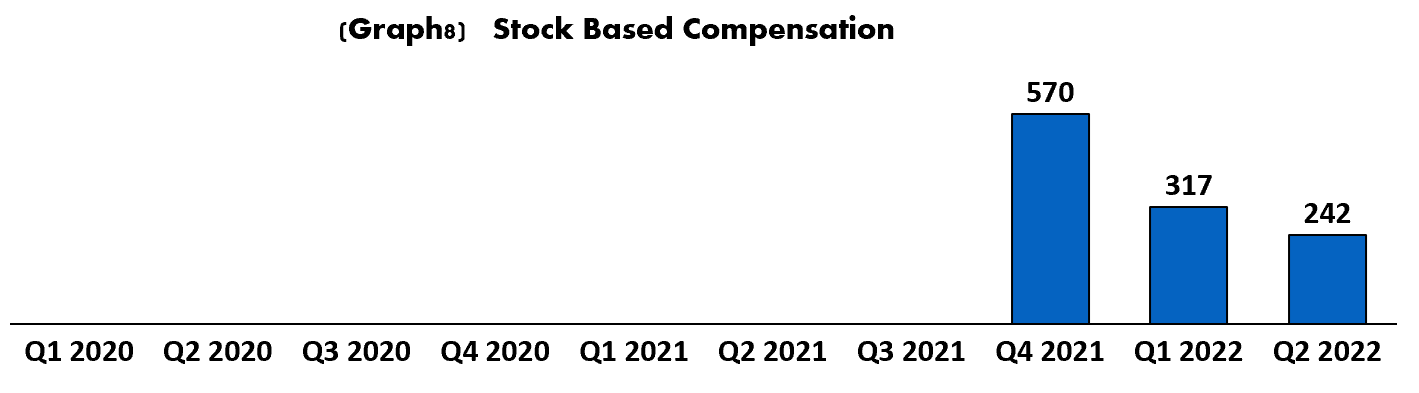

Research and Development when up to $543m from $394 during Q2 2021

R&D increase was primarily due to $115 million of stock-based compensation expense, a $109 million increase in payroll and related expenses

The investments in R&D include early development of the R2 platform, future propulsion platforms, and updated vehicle network architecture

Selling, general, and administrative was $461m up from $186m a year ago

SG&A drivers for the higher expenses were scaling sales operations, including customer-facing facilities and corporate functions to support future business growth, including higher headcount and increased personnel costs, as well as stock-based compensation

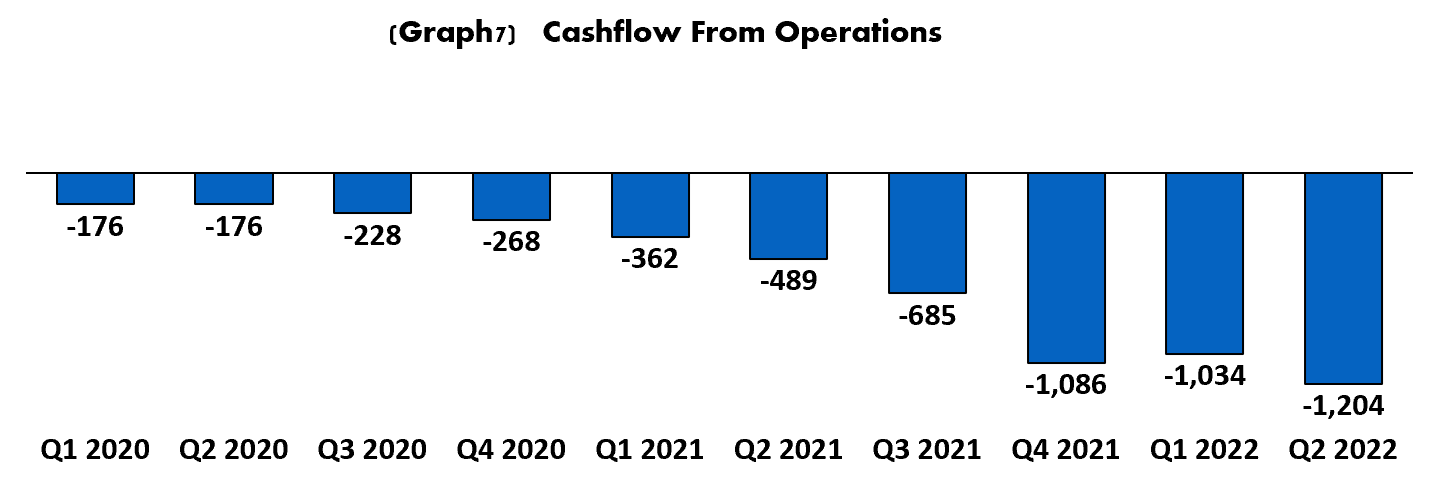

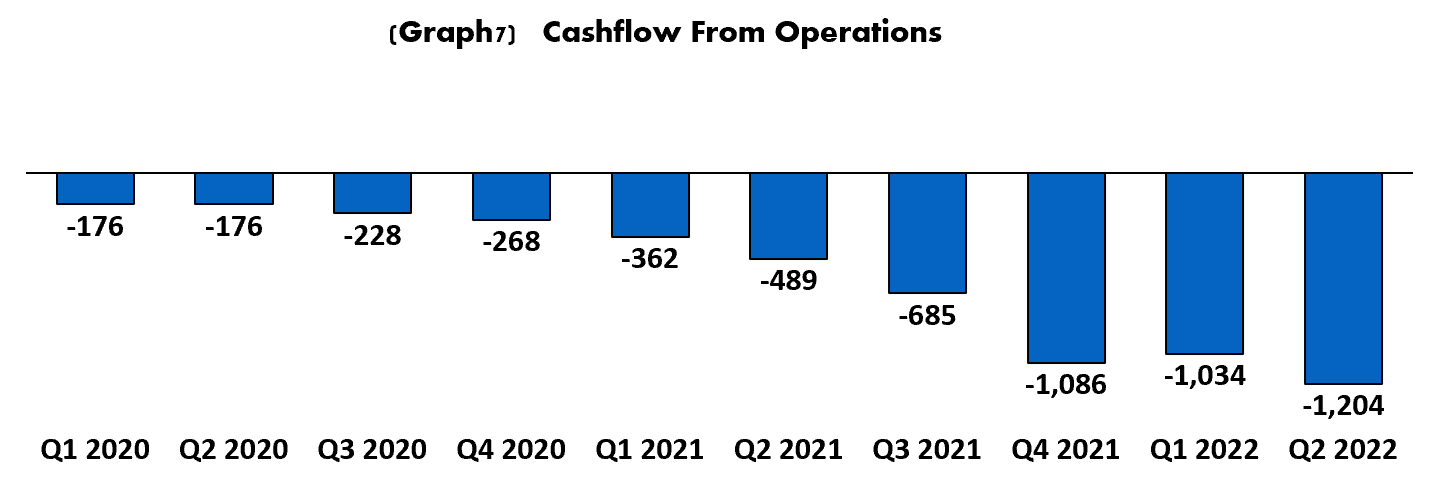

Rivian has accumulated $9.7b in losses since their start

Net income so far this year has been $3.3b

When looking at cash from operations in their Cash Flow statement they have used $2.2b which is a lot less, $1.1b less. They have been using many non cash items to achieve this. Stock based compensation so far this year has accumulated $559m

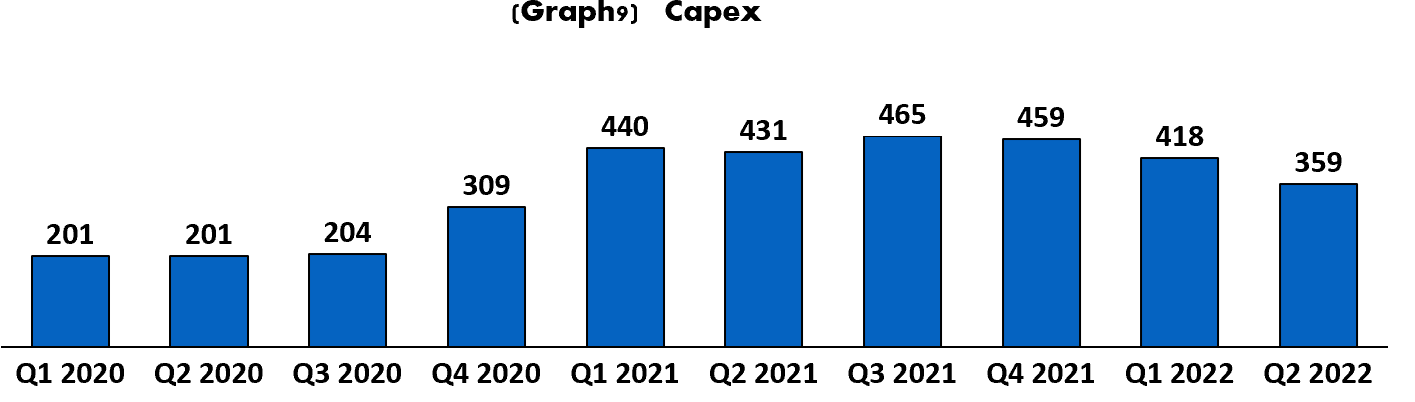

Additionally to those $2.2b used from operations, Rivian has used $777b in Capex so far this year. They did say that in order to save cash in 2022 they will push some of the Capex originally planned for 2022 to 2023.

When taking into account the Capex so far they have gone through $3b in 6 months of 2022. That would be a run rate of $6b a year.

Balance Sheet

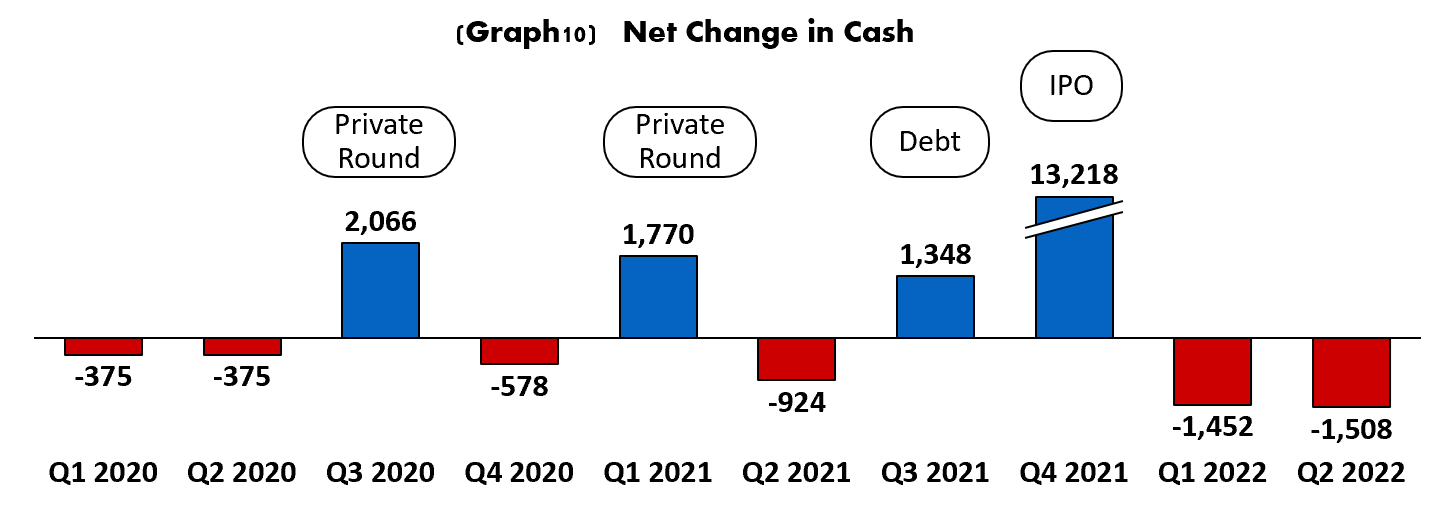

Rivian closed the quarter with $14.9b in cash and $0.5b in a ABL Facility et based Lending)

Debt for the company sits currently at $1.2b, practically unchanged from the previous quarter.

Inflation Reduction Act

Recently the US government has passed the inflation reduction act. RJ Scarinje mentioned this law many times during the last quarterly earnings. They gave the impression that this will accelerate the transition to EV vehicles and overall help Rivian. Let have a look a bit in detail what is included in this law just to see if actually will help them

The Inflation Reduction Act, first has a very political and misleading name, so now let's call it IRA. IRA has two main aspects, one that raises taxes and one with 3 types of investments. Rivian is influenced primarily by the investment part and specifically $370b that will be invested in Energy ‘’Security’’ and Climate Change.

The bill includes $161b in new tax credits to encourage clean electricity and $80b to encourage consumers to purchase new or used Vehicles. On the clean electricity side Homeowners will be able to install solar on their roofs with a 30% tax credit. On the purchase of EVs the tax credits will be $7,500 for new vehicles and $4,000 for used EVs. This last tax credit is the one that impacts Rivian more directly, but it does have some details that are worth being mentioned:

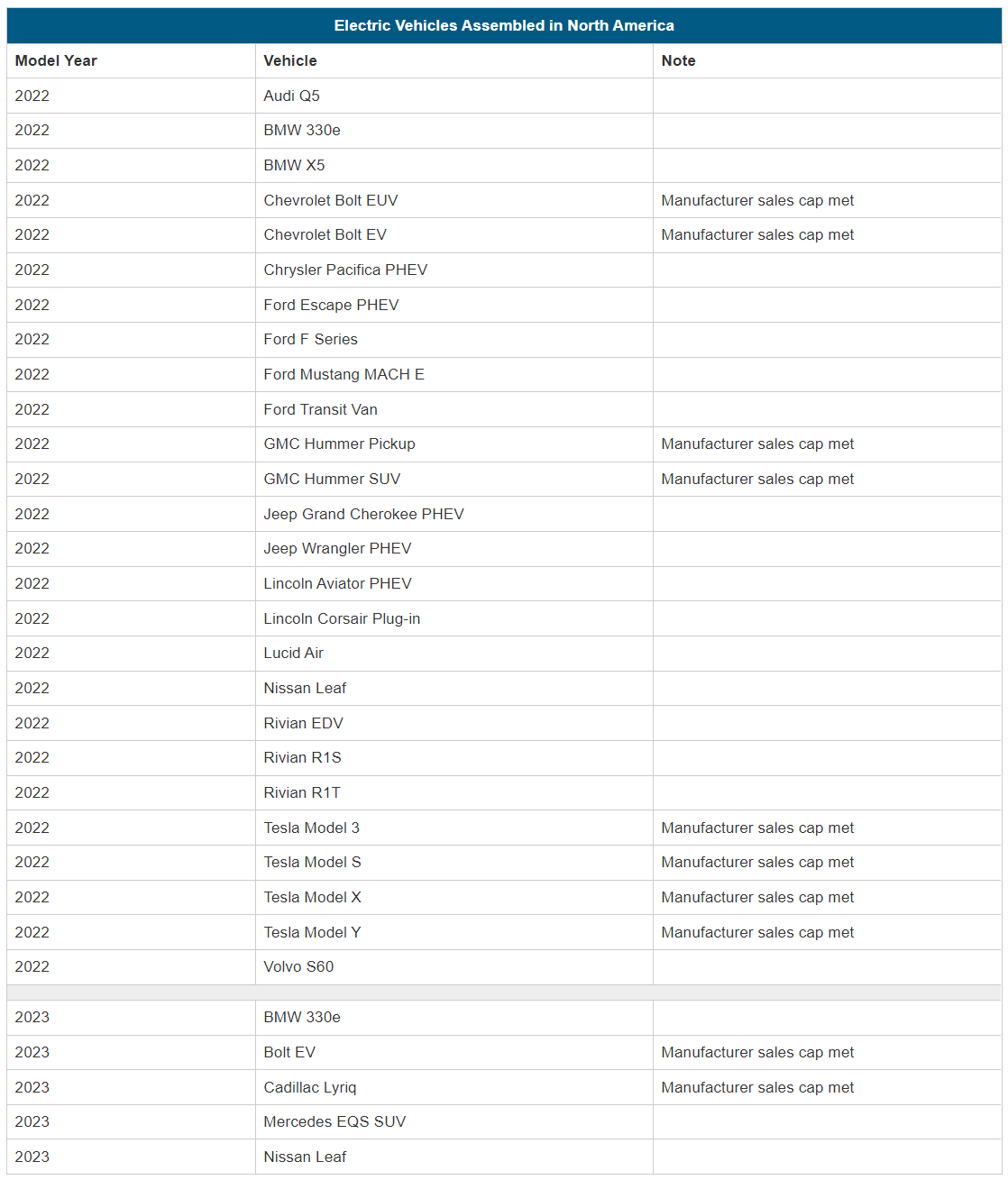

Only vehicles assembled in North America will apply.

Some manufacturers that have vehicles assembled in North America have reached a cap of 200,000 EV credits used and are therefore not currently eligible for the Clean Vehicle Credit

Below the list of vehicles the government announced that are eligible, some have the 200K units cap that should be lifted on January 1st 2023.

Is it really going to be cheaper for customers though? There have already been very ‘’dirty’’ moves by some car manufacturers. Three specifically, one is Ford and the second one is Rivian itself and third Tesla. First Ford, they announced early in August that they would be raising the price of their very popular Electric F150 by $8,500. The base version of the F150 was previously listed at $40,000 and it is now priced at $47,000, better more equipped versions saw their price increased by $8,500. They recently announced a price increase for their Mustang Mach e EV.

On the Rivian side, they recently announced that they had canceled their most affordable version of their R1T effectively raising the price of its base model electric truck by over $6,000. The move, same as the one from Ford, is very timely and very suspicious. Especially for Rivian that had already tried to raise the price of this vehicle but received horrible backlash resulting in Rivian backing down from the increase in order to preserve brand value. It seems that this time brand is not important any more.

Last Tesla announced that is raising the prices of their of their full self driving by $2,000, this on top of recent price increase on all models in June.

The tax credit either in full or a portion will be absorbed by car manufactures like we are seeing already. This might not help as much as RJ mentioned in their call because the net effect could be almost zero. Will be beneficial for them in terms of improving margin, not necessarily for accelerating volume for them.

Outlook

Rivian is still struggling greatly with production. They have a long way to go to get to their target of 25K produced vehicles. They will need to produce 18K vehicles in the second half of the year. So far they have claimed that they do have the capability but the issue has been related to supply chain issues. They claimed even that during Q2 they had days in which some shifts did not have any activity due to missing parts. When they had the parts they were more efficient than the previous quarter. The issues that they most commonly have are related to semiconductors, their providers still have not had the capability of ramping up their capacity.

Rivian has still not gotten yet to what Elon calls “production hell”. This is the time when you go from building just a few perfect cars to trying to scale into thousands of cars every quarter. We believe that this will star to happen whenever they try to build 18K vehicles at the end of this year. They have a lot of pressure now to be able to get to this goal. If they don’t fix these supply chain issues soon, and by soon we mean they should have it fixed already today in the second half of August, they will go into panic trying to reach 18k vehicles . It will be very likely that either they announce that they will reduce their target for the year or they will start having a lot of quality issues. They are underestimating the difficulty of building that many cars for a startup in that very few months Tesla did it in the second year of the Model S but for Tesla was a lot simpler, they were focused only on the Model S, in the case of Rivian they have at least 3 different type of vehicles to focus on.

Rivian has a lot more cash and is going through cash faster than Tesla did. But it is actually very important that they do something with it, they need to get to the R2 series as soon as possible. The R2 series will be the affordable set of vehicles that Rivian will develop. As of now it is believed that these vehicles will start to be delivered somewhere in 2024, but as of today, this sounds like a million years from now. They will have to fight with a huge amount of competition once they get there. Just look at the list from above. There are many electric vehicles already and there are many ‘’cheap’’ ones that are gaining a lot of market from even the Model 3, vehicles like the Hyundai Ionic. They cannot afford a lot of delays from the 2024 dates otherwise competition will be a lot more difficult. The number of new vehicles sold in the US an in the world will not expand. It is not as if we will suddenly sell 20 million new vehicles in the US every year. It is almost certain EVs will gain market share, but as of now 2024 sounds late, a lot of companies will have gained from them and it will be an uphill battle.

Even though the next two years are very important for Rivian, they need to get through production hell and they need to get their affordable vehicle on the market. The likelihood is that, like we mentioned in our previous piece, they will be an important player in the EV market for years to come. They have very important investors like Amazon, this makes money less of an issue and the focus becomes all about execution. We are now convinced that the valuation for Rivian should be somewhere around $25b as a base scenario, this is assuming that they deliver on execution. For a conservative case we see a valuation of about $16b, this is a scenario that assumes more production issues, similar to the ones Tesla had for years.

Rivian has a lot of promise. Execution will be the most important thing followed by monitoring that they are not wasting their cash. They have a lot of cash and they could act spoiled with it. This valuation could change dramatically once they announce or get closer to the R2, but we consider that if we hope for that already today we are entering more of a speculative space, and with the current market and economic conditions, speculative plays are the ones that suffer the most.