Opendoor: The Market Maker in the middle of a Real Estate Market slowdown

Opendoor: The Market Maker in the middle of a Real Estate Market slowdown

How will they perform in a 6% Mortgage Rates Environment

Update: Since the original publication of this article we have also published our analysis on their Q2 earnings, you can read that here: Opendoor: Q2 Earnings , and Q3 here: Opendoor: Q3 Earnings

Opendoor was founded in 2014 with the purpose of making it easier to purchase a home online. It is one of many ibuyer (instant buyer) companies gaining strength in the last few years . Opendoor was listed via a SPAC merger back in 2020. During the pandemic went on to make an all time high of $39.24 per share. It sits today at $4.83 having lost more than 80% of its value and making it a prime subject to be analyzed in depth by our team.

Business Model:

Opendoor Purchases homes from individual homeowners

Homeowner will voluntarily go on Opendoor an request an offer

Opendoor will give the homeowner an instant offer

If the homeowner is interested in continuing the process, they will have to schedule an online walkthrough with Opendoor. Basically a video call of about 30 mins going through every section of the house answering questions, opening things etc. etc.

After the online walkthrough, they will schedule an exterior inspection. Opendoor will send their final offer after the exterior inspection

If accepted, the closing process starts and no other inspection is needed

During the process Opendoor will not enter the house until process is finish and the house is Opendoor property

Opendoor charges on average between 5% to 8% on the sale and they calculate that percentage depending on how long they expect to have the house on the market

They also offer title and escrow services to their customers

They might also add charges for ‘’repairs’’ that are needed on the house

Recently in 2021 they launched Opendoor backed offers and Opendoor complete.

How Opendoor backed offers works:

The customer submits either a pre qualified letter from a lender or applies for qualification with Opendoor

Opendoor helps submitting all cash offers.

If accepted, they can hold the house for you for 60 days (if more time is needed they apply a daily fee of 0.02% of the home price)

How Opendoor complete works: Tries to combine the transactions of selling and buying by selling your house to Opendoor while getting an open backed offers for your new home. The idea is to avoid having to have two mortgages or having to wait for your home to close to start buying a new one

The role of Opendoor, and ibuyers in general, is to become a market maker, market makers provide liquidity to markets and profit from the bid to ask spread.

For example:

For a $300K house the typical ibuyer will charge around 5%, that would leave the homeowner with 95% or $285K.

Then the ibuyer would do some quick fixes to the property and list it back at around $310K

When closing on the sale of the house they would charge also around 2% to 3% to the new buyer.

In total, they could bring around 5%-8% from the spreads between transactions of the same home

This 5%-8% would come down after taking into account other costs like any administrative related cost , interest cost and the cost of fixing homes. This could bring the margin to anything from 2% to 6% depending of the efficiency of the ibuyer

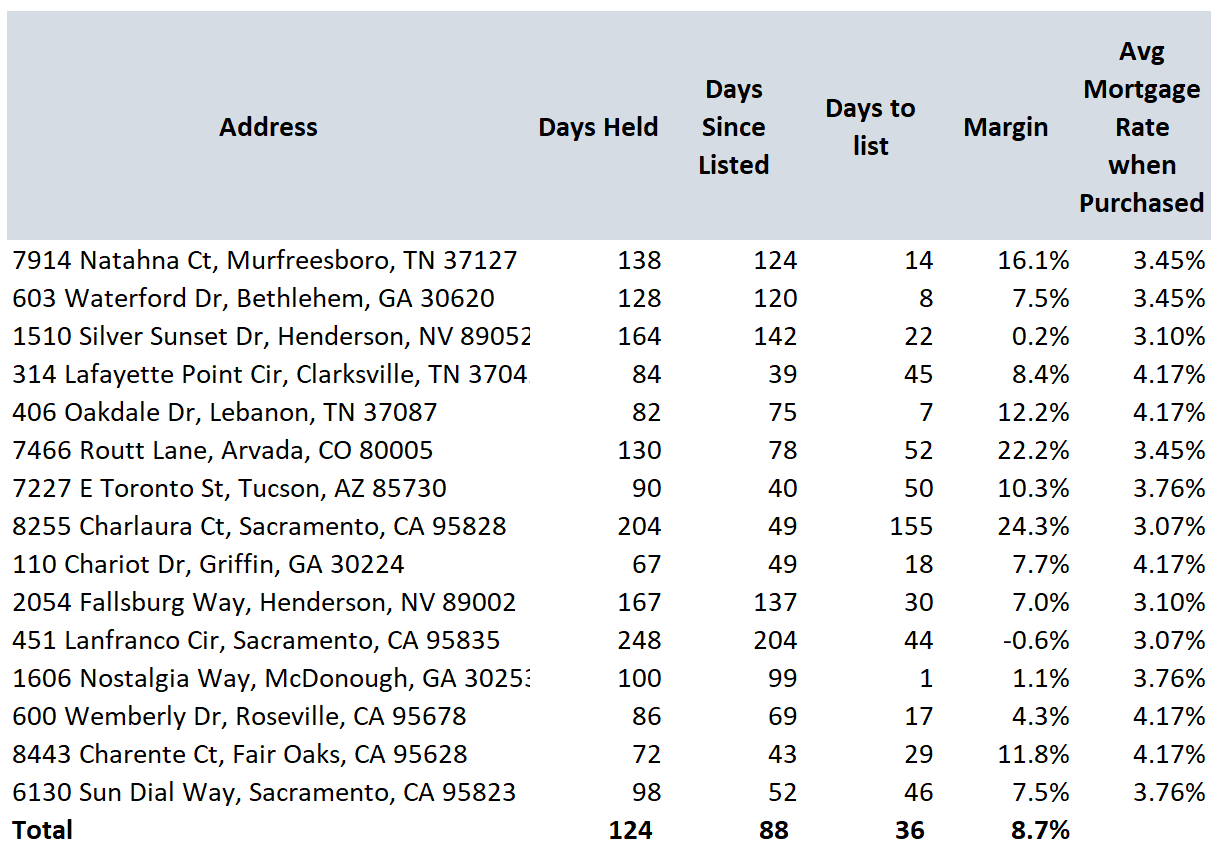

We have gone to Zillow to get some recent information of how they are doing recently (Opendoor) You can find Opendoor under the agents in the website. At the day of writing they had 4,329 listed for sale and 28,584 sold. We took 15 homes and calculated a rough estimated margin for these homes as well as days to list, held and listed. This is just a calculation with the available information, this probably is not 100% accurate but helps give an idea of what to expect. The below percentages does not include any cost of financing, administration, maintenance or anything, it just assumes price bought and price sold and a 5% fee when purchasing and a 3% fee when selling. (The sample is very small and recent, helps better illustrate the business model and perhaps not recent performance)

As you might have noticed already. The ibuyer business is an intensive working capital business. Most of the financing for the purchase of the home comes from debt, asset backed debt (backed on the asses/houses being purchased)

Key Metrics / Performance

Highlight of the recent performance

Opendoor added 23 new markets and by the end of Q1 2021 they have already reached 48 markets

21,725 Homes sold during 2021

36,906 Homes purchased during 2021

The total amount of transactions in which Opendoor participated was 58,631 or about 0.96% of the 6M sold in the country during the same year

Growth was reactivated in 2021 after a slowdown in 2020 due to the pandemic. Opendoor focused on expanding in 23 markets, after being almost flat since 2018. Opendoor has a long term goal of reaching more than 100 markets, so we could say that in absolute numbers they are close to 50% but in terms of population coverage they are even higher getting close to 70%.

Apart from home purchasing, a lot of their recent investments have gone to market expansion and scalability. We could expect that this will continue until they get closer to the 100 market goal. What they mention many times in their earning calls is that when entering a market, first they test the waters and start slowly, so we could expect that the additional 23 markets from 2021 still have not had their full impact in expenses, but also have not had their full impact in revenue either. You can see this in graph 5 where operation cost are growing faster than revenue (almost at the same pace though)

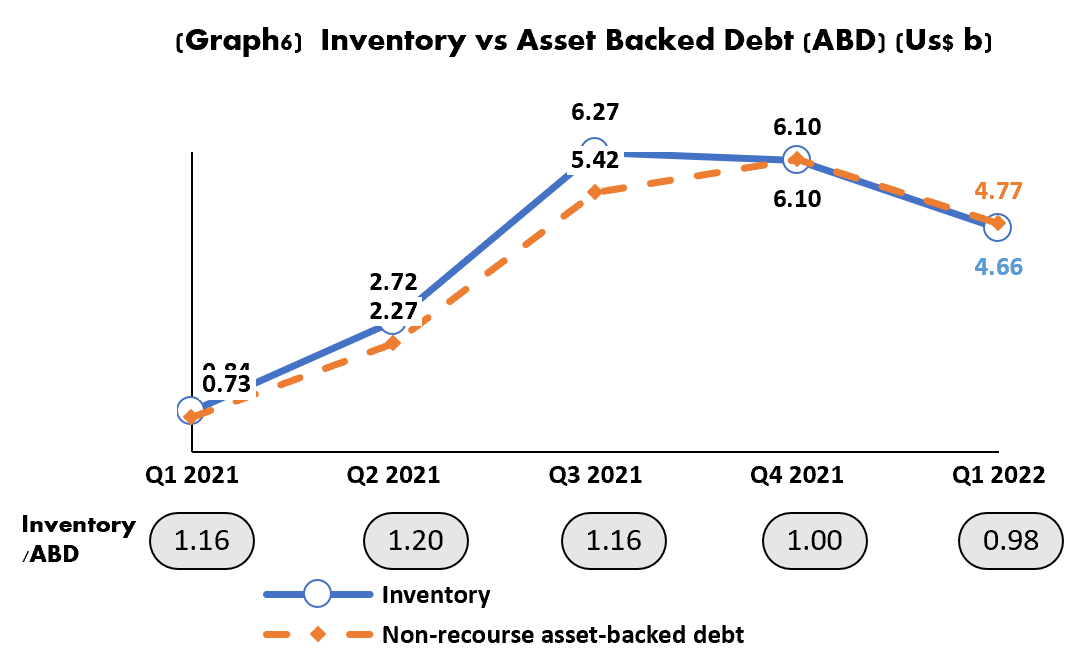

Opendoor is a very high working capital company. At a glance you might think that this company is getting in debt fast, but you would not be 100% correct. They do have more debt, but this is 100% in line with their business. As you see in graph 6, inventory goes hand and hand with debt. Opendoor finances their homes mostly with asset backed debt, meaning debt that is backed by the same homes that they are buying. Opendoor has claimed in their calls that the rotation of their homes is about 100 days. So they could have a rotation of their debt of 3.65 times, meaning they can use the same dollar to buy 3.65 homes during the year. As mentioned above, ibuyer are market makers, they are closer to mortgage lenders than homebuilders or realtors. The more they want to grow, the more debt they will use, but mainly asset backed debt, if you look at their debt you will see that is very small when excluding their asset backed debt. In graph 6 you can also see that there is almost a 1 to 1 ratio between inventory and asset backed debt, as long as this numbers remains close to 1 their debt could be covered fully by their inventory (house inventory)

Competitive Landscape

Opendoor is not alone in the ibuyer business, there are many companies doing the same or very similar things. Some of their main competitors are:

Offerpad

Redfin Now

There are other competitors that have some similarities but are not currently doing the same type of business. For example, Knock Home Swap, which helps customers buy their next home before having sold their existing one by underwriting a mortgage and giving an advance on the down payment.

When focusing on their 2 bigger competitors we see in the graph below that Opendoor had 83% market share of homes sold and 73% of market revenue, and currently the ibuyer with the biggest market presence

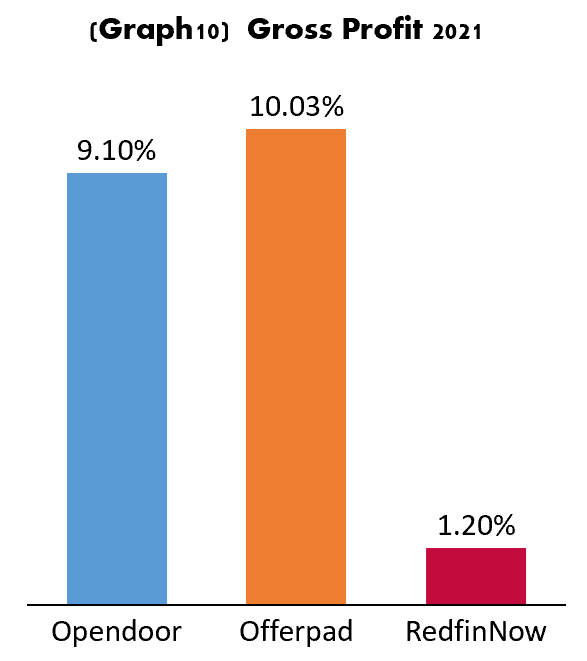

When having a look at the revenue market share we notice that revenue per home sold is higher for both Offerpad and RedfinNow. When looking at the profit margin (Revenue - Cost of Revenue) we see that RedfinNow has considerably lower margin despite having the higher revenue per home. Offerpad has the best margin, but very close to Opendoor’s

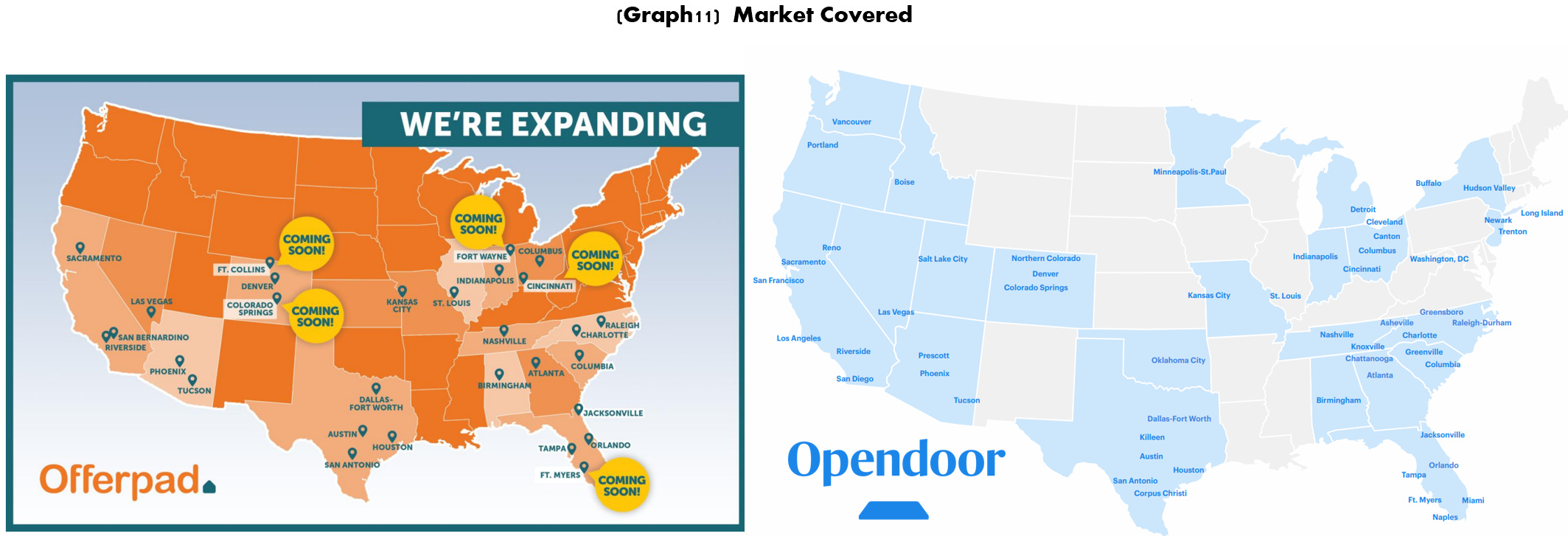

Offerpad has 29 markets ( 8 more than end of Q4 2021) Opendoor has 48 markets (4 more than end of Q4 2021) and RedfinNow at the end of Q4 2021 had 30. Offerpad claimed in their latest investor presentation that their holding time in 2021 was 76 days, this is better than the one mentioned by Opendoor of 90 to 100 days.

Offerpad and Opendoor are clearly the leaders in this business, both are pure ibuyers. Redfin continues to lag in both market share and profit margins, but we have to take into account that similar to Zillow, they are not pure ibuyers, they have other core businesses and they might need to be more conservative in terms of growth push.

Even when looking (graph 12) at the revenue guidance for Q2 2022 we see a lag in Redfin having guided down by a larger percentage than its competitors. Another important highlight from graph 12 is that all three are guiding down in revenue. This does not seem to be seasonal since all three grew in Q2 to Q1 2021, and historically spring is usually the most active part of the year. This could be that the three are being conservative given the higher mortgage rates, but still given their market share over the total real estate market (close to 1%) and having a role as market makers, the higher rates should still not impact them since they still have a lot of market to capture. (that if the do capture it)

Zillow Offers

We believe that it is important to briefly comment on the fact that Zillow offers decided to abandon the ibuyer business in the second half of 2021.

The following is a quote from their shareholders letter from Q3 2021:

‘’Ultimately, we determined that further scaling up Zillow Offers is too risky, too volatile to our earnings and operations, provides too little opportunity for return on equity, and serves too narrow a portion of our customers. ‘’ ‘’ We have been unable to accurately forecast future home prices at different times in both directions by much more than we modeled as possible, with Zillow Offers unit economics swinging approximately 1,200 basis points from Q2 to an expected -500 to -700 basis points in Q4 2021.’’ ‘’A final factor in the wind-down decision is that, to date, we have been able to convert only about 10% of the serious sellers who ask for a Zillow Offer’’

Mainly they cite difficulty to accurately estimate prices and a low conversion rate of 10%. By comparison Opendoor has currently +30% conversion rate of ‘’serious buyers’’

Real Estate Market

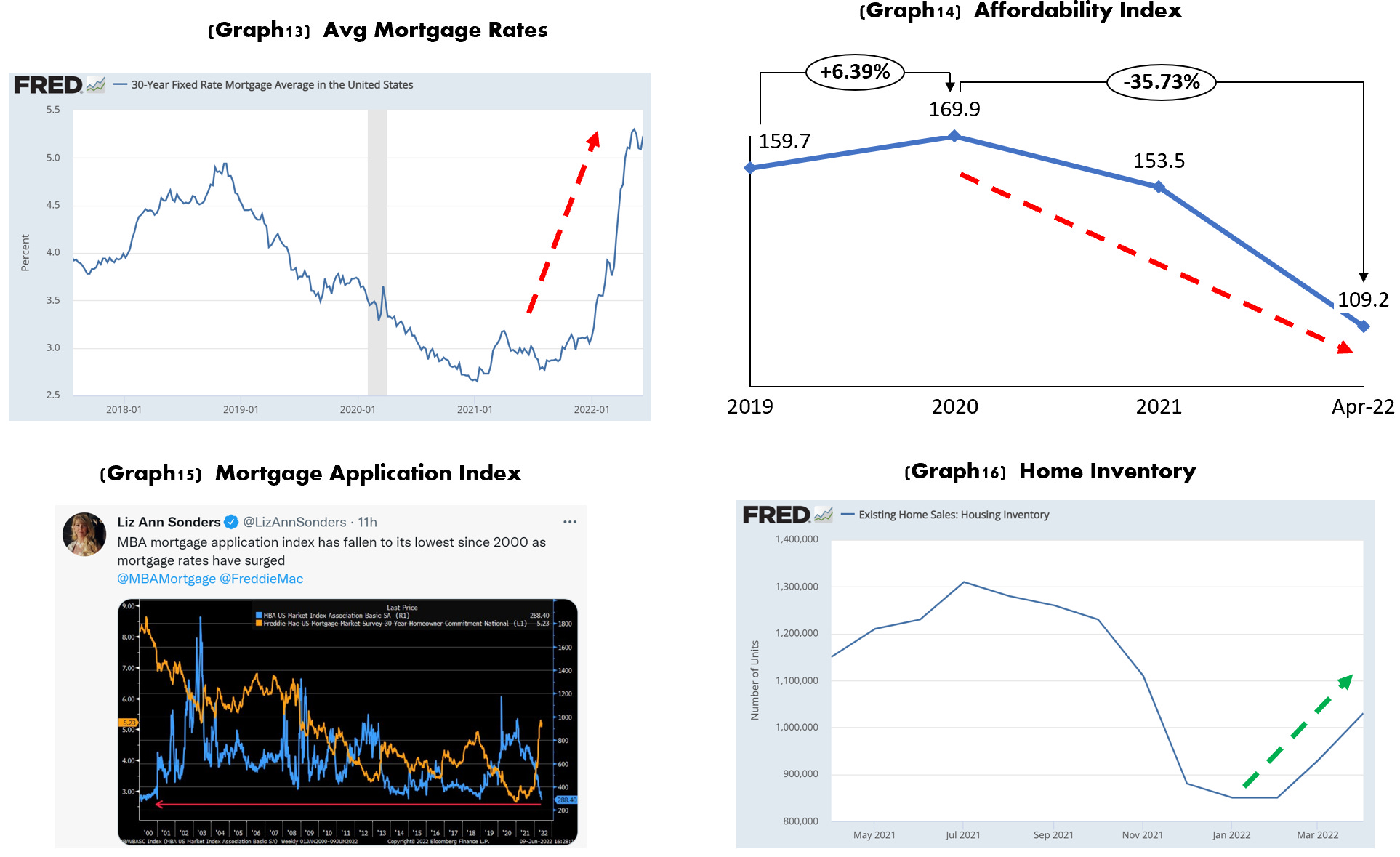

For the past two years the Real estate market has been on a roll. Median Priced Existing Family Home has gone from $275K in 2019 to $398K in April 2022 (up 44%!). But the macroeconomic situation in the country has given these worrying facts about short term future of the real estate market:

Mortgage rates have gone from low of about 2.68% in 2020 to 5.23% in may. (195% increase) Graph 13 (Close to 6% already in June)

The Home Affordability index has collapsed, from 169.9 in 2020 to 109.2 in April. $82K in income is needed to qualify for the average price of a single family home. (Graph 14)

Mortgage application is the lowest in 22 year as Liz Ann Sonders highlights in her tweet (Graph 15)

Home inventory is rising but still low when compared to historic values and market need.

We could expect that the Real Estate will definitely come back to earth. We don't expect the Home Price Appreciation to continue its trend of 2021 and 2020, we expect that it will come back to at least a normal historic trend. It is difficult to see a huge drop in the market considering that a lot of homeowners now have a mortgage rate close to 3.0% or lower and will not be incentivized to sell and face 5% rates, this will likely maintain inventory low.

Outlook:

Opendoor is a young company, despite starting in 2014, it has been since 2020 that it has accelerated rapidly in revenue growth. Going hand in hand while the real estate market was going crazy, hence, one might ask if Opendoor would perform differently in normal market conditions.

Some of the possible risks for the company are:

Lower Home Price Appreciation: This will be a headwind, since rapid appreciation, specifically in 2021 helped Opendoor improve their margins to 9.1%

Very low margins: This is an industry that will operate in low margins. Long term margins guided by the company during its calls and fillings is 2% to 4% (Adjusted Net Income Margin) If their pricing models fail, or they have bad execution, their margins could disappear fast. This is almost like a supermarket, where execution is key and there is not a lot of room for strategy and execution mistakes (i.e Zillow Offers)

Debt cost: Opendoor in its calls mentioned that a 100 basis points raise in debt servicing would translate in about 25 basis points increase per home.

The 25 basis point seems to assume about 100 days of home rotation. If the market slows down and time to sell takes longer this could bring an impact to margins.

Especially if overall rates in the economy continue to rise, 10 Year Yield is above 3% and could continue to rise given high inflation (8.6% YoY in May 2022) The important fact here will be when inflation comes down (it will eventually) what would be the next average inflation for the next decade, are we going back to ~2%, or will it be higher? There are geopolitical reasons why we could believe that this will be higher than the 2% the Fed wants. Relations with China and Russia will likely force Europe and the US to have supply chains closer to their markets. This is a slow process that will likely have an impact for the next few years.

Higher inflation will force higher cost of debt due to higher fed funds rate etc. If the cost of debt comes back to normal (and by normal we mean real cost of debt not the artificially low debt that we have had for the past 15+ years) , the cost basis per home purchased could eat away a little more of the expected 2% to 4% margin.

What could be the case for Opendoor being a good opportunity for the next 10 years?

Addressable market is very big. More than 6 million homes are sold per year. The total market is close to 2 trillion dollars a year. Penetrating this even with low margins could be a huge possible earnings potential

New revenue streams that are just starting, like Opendoor backed offers and Opendoor complete.

Recent acquisitions that signal future opportunities to bundle services:

Pro.com - Quotes for construction services: Could bundle or make it easier for a customer looking for a home to have included the improvements to the house before they move in

Skylight: Dedicated to home renovations, hand in hand with pro.com

Reddoor.com - Mortgage brokerage, important help to their open backed offers product

Could become a more attractive option when a market has a longer time to sell. Penetration could be accelerated in an environment where it is more difficult to sell. Opendoor is more attractive to customers due to their fast approach to closing, this will likely improve penetration in markets. But like was mentioned above, the holding time could make the debt rotation slower and debt cost per home higher. Opendoor addressed this topic in their latest calls by saying that they have been since late 2021 working with the spreads to better handle a market with lower HPA. The second half of 2022 will give us the best evidence on how they handle this.

Not a long term holder of inventory: Despite the fact that a slowdown is coming. The risk of having a death blow to the company is very low. The holding period of about 100 days helps in the case of a drop in the home prices. The biggest one quarter (90 days) drop during the crash of ‘07 to ‘11 was close to 3%. This is the biggest drop. Meaning that this would likely have an impact in the margin of one quarter, taking into flat or slightly negative. But they could recover fast since the purchase of a new home now will come at a lower price. So we believe that is not a risk that would kill the company but it could ruin a quarter or two in terms of profitability. Let's take into account that drops like the one in ‘07 to ‘11 are not very common in history.

Valuation

This is a company that is still in growth mode and still mostly losing money, DCF model (discounted cash flow) is not the most appropriate tool to determine if the company is undervalued or overvalued. But we could use a simple calculation to what the current valuation implies for growth.

As of day of writing the company is valued at $3.02b. This translates in the following assumed Ebitda:

For a company in Real Estate Services industry the implied Ebitda is $145M

For a company in Real Estate Development/Operations industry the implied Ebitda is $318M

Ebitda for the last 12 months has been -$127M. So it still has to grow to get to either of the two. Something that could very well do if the trend continues. H2 2022 is very important to see how their margins behave in a more normal market condition.

The market size that they are participating in will give them a great opportunity to become very big i.e if they manage in the long term to reach 5% market share in the country, that could be around a $4.7B Ebitda margin (when using the low end of their guidance of ‘’Adjusted EBITDA Margin’’) The opportunity in this market, if scale is achieved, is huge.

Execution is key for Opendoor, if they thread the needle with good execution they have the potential to grow a lot. The thing is that they must remain focused and not lose control of the tight model where they operate

Read our Previous Pieces on:

Opendoor Peloton Carvana Rivian Roku