Carvana: Q2 Earnings

We covered Carvana on our deep-dive published July 11th called Carvana: Disrupting the Car Buying Process but might dilute you in the process This is a short summary and an update after their Q2 earnings were announced August 4th. During earnings Season we will do this short updates of the companies we have covered so far Opendoor Peloton Carvana Rivian Roku and UBER

Carvana reported earnings recently and ever since has been nothing but up. The stock closed at $33.54 before reporting earnings. It is now trading at $42.30, 26% higher (it was a lot higher just a week ago but has given back some of its gains recently), it was up 40% just in the first day alone. But why did the market like the results so much? Did they finally start a change in trend? Are they closer to profitability? Are they finally showing that the business does scale?

Performance Summary:

Revenue

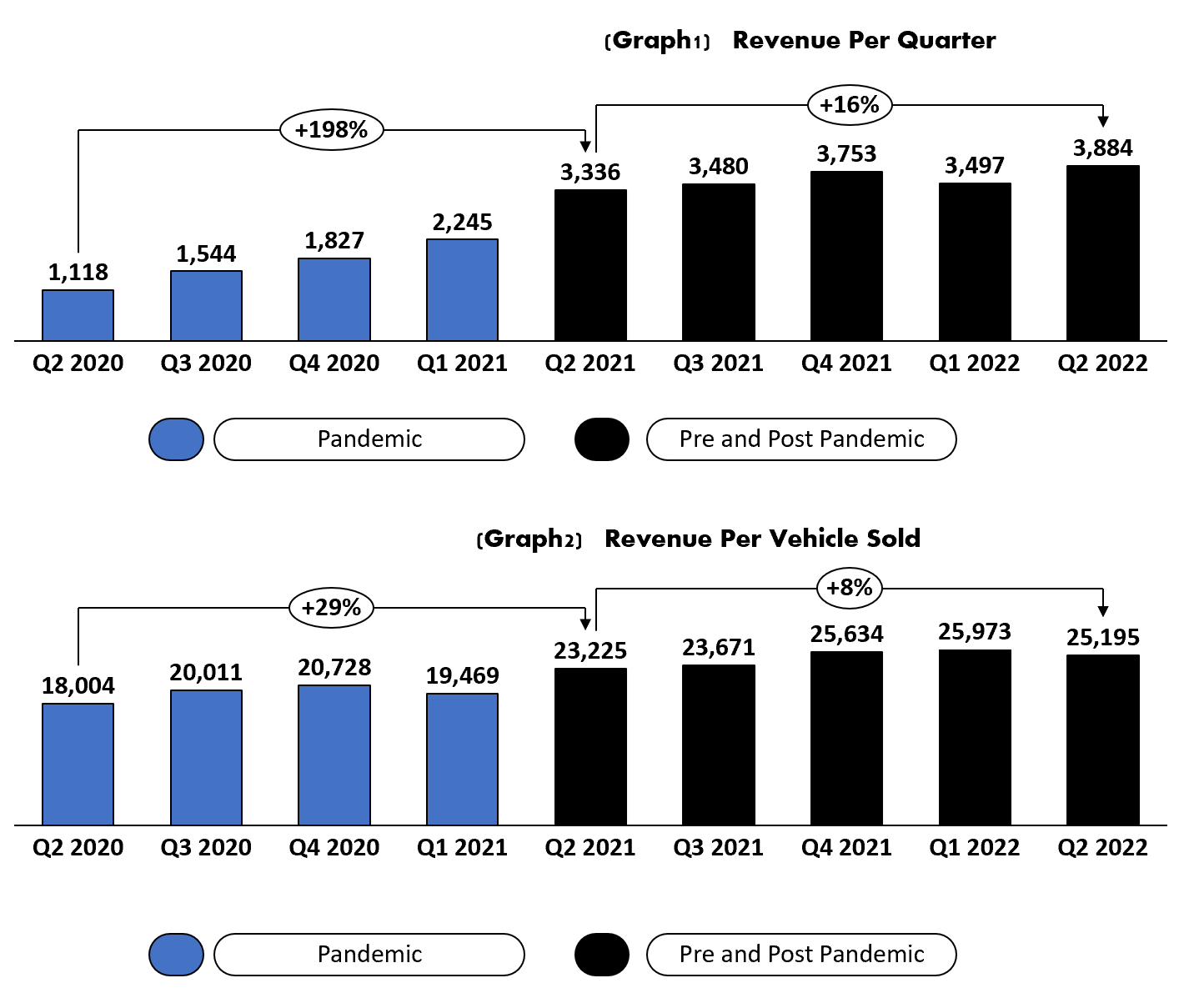

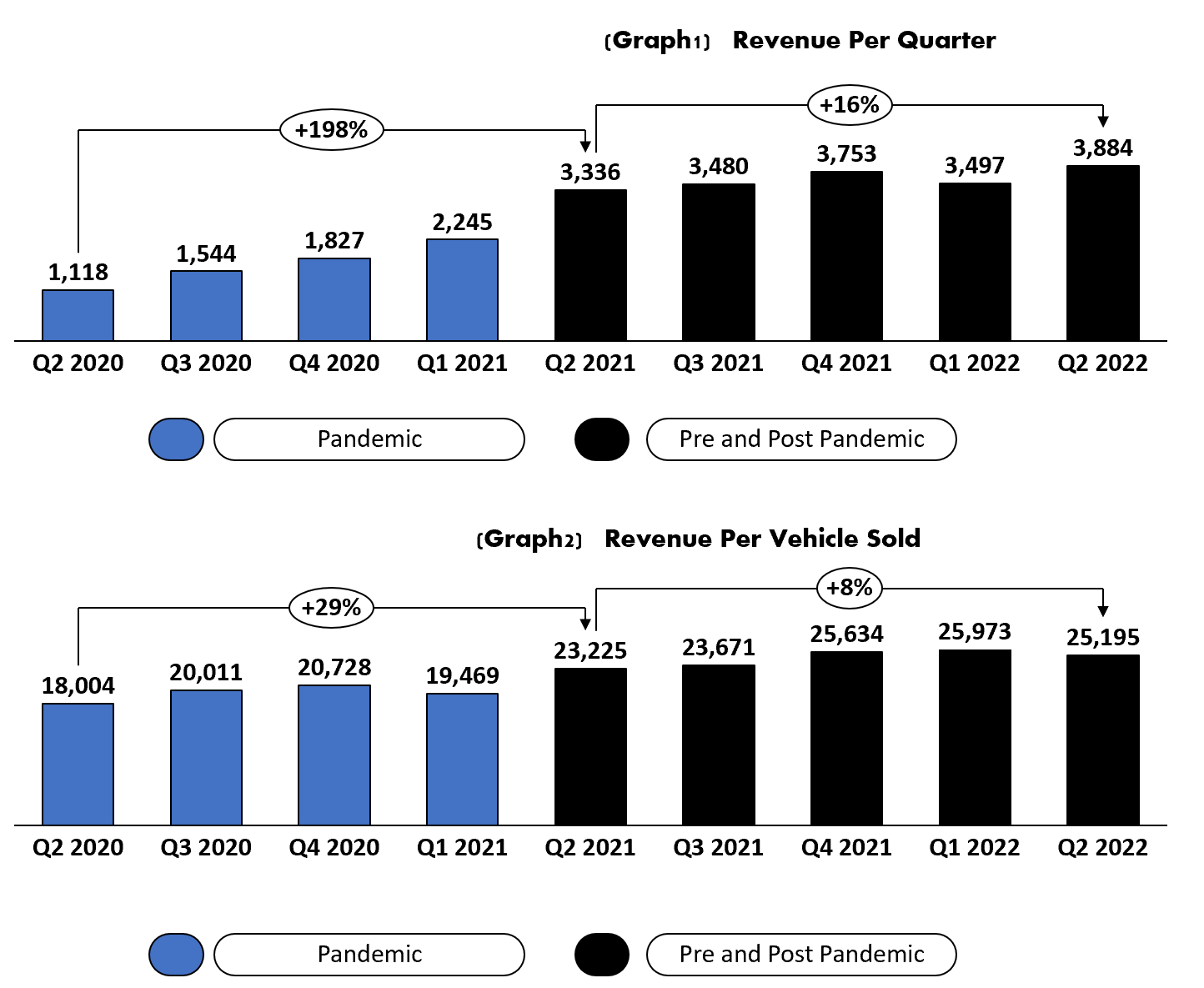

Revenue for the quarter was $3.8b an increase of 16% YoY

This revenue includes revenue from the recently acquired Adesa. The acquisition was finalized May 9th. So the quarter had revenue from this acquisition.

In Q2 the company recognized $108m in revenue from Adesa Acquisition

Total Carvana Revenue without Adesa was $3.776b and increase 13.2% YoY

If Adesa would have been accounted for the full Q2, the revenue would have been $3.968b and if this would be compared with a full Q2 2021 including Adesa, the growth would have been 11.5%

Used car vehicles sales were $2.962bb up from $2.5b the previous year

Wholesale sales and revenues, which includes sales of trade-ins and other vehicles acquired from customers that do not meet the requirements of retail inventory, totaled $704 m for Q2 2022 and $557 m for Q2 2021

Other sales and revenues, which primarily includes gains on the sales of automotive finance receivables they originate, sales commission on VSCs and sales of GAP waiver coverage totaled $218 m for Q2 2022 and $275 m for Q1 2021

Revenue per retail vehicle sold was $25K, up 8% vs last year but down from previous month. It was a very slight drop, but it is the first that it has dropped since the acceleration of used vehicles appreciation in Q2 2021.

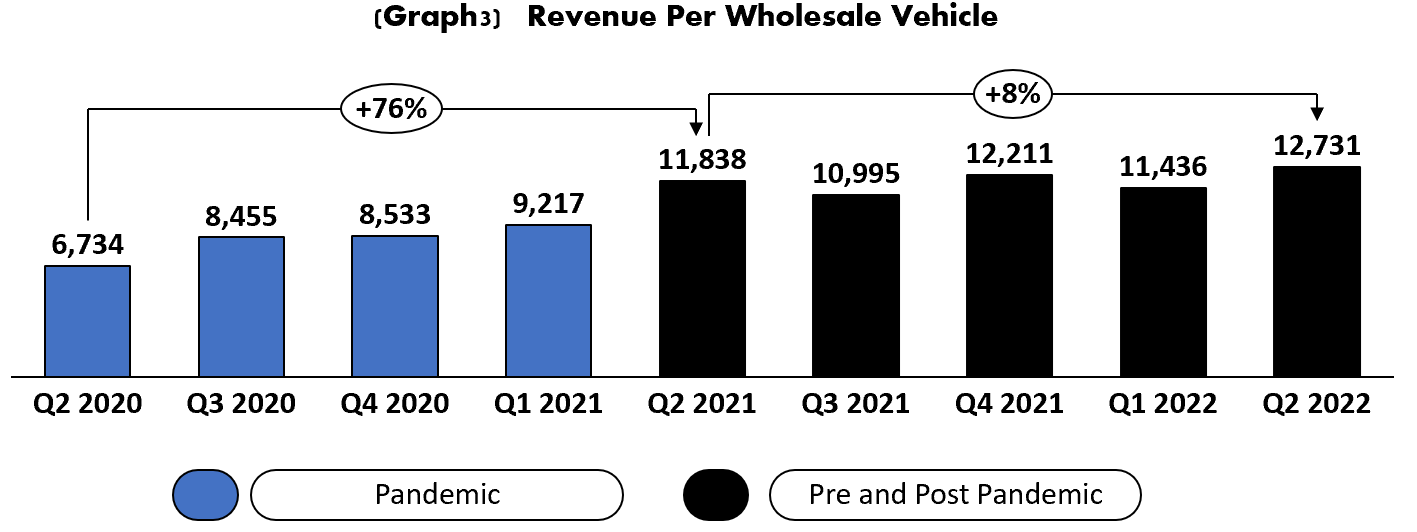

Revenue per Wholesale vehicle sold was $12.7K, up 8% as well. Wholesale revenue per vehicle was still above the previous quarter, different from what was seen for retail

Key Metrics:

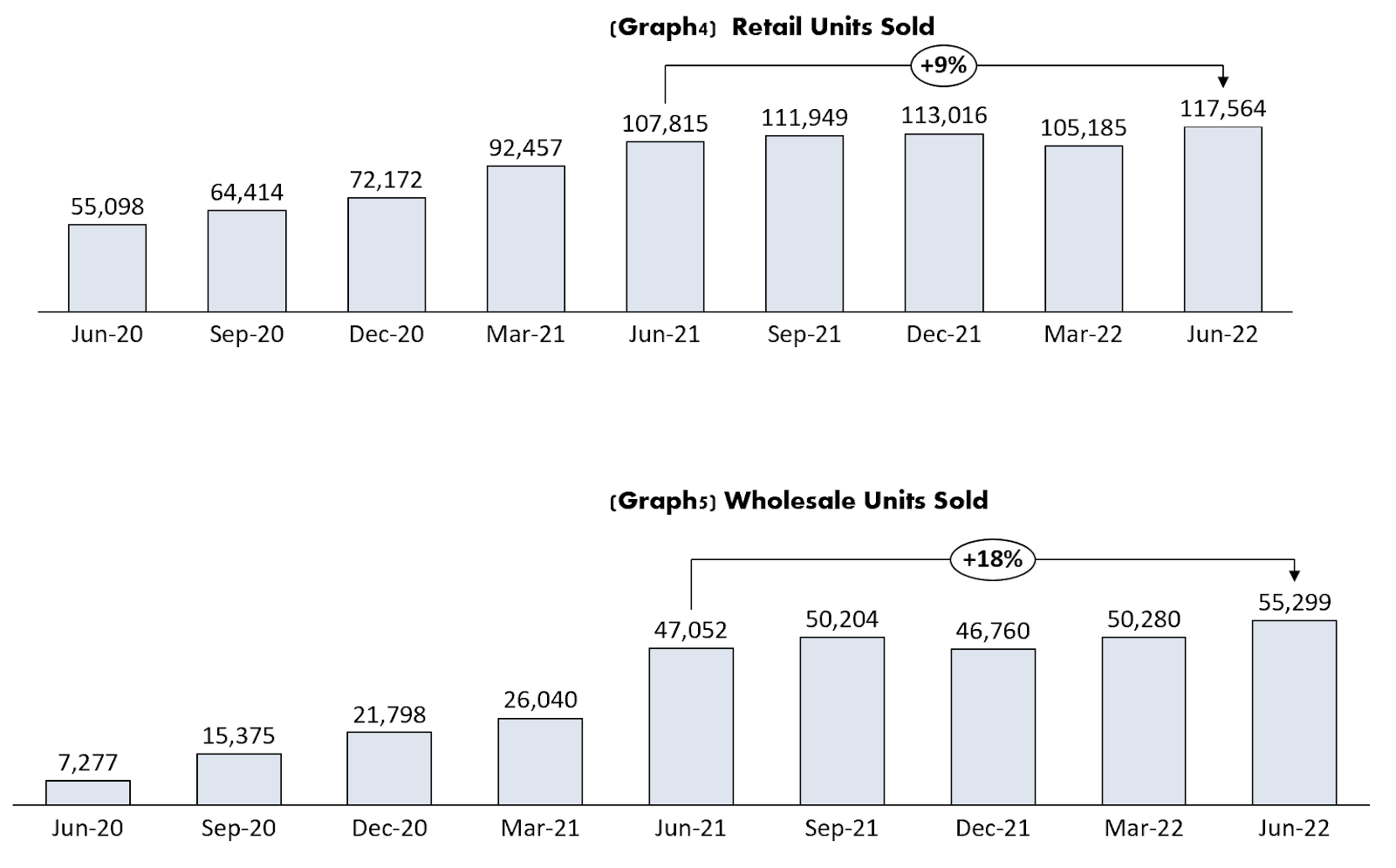

Retail units sold were 117,564 up 9.04% YoY

Wholesale units sold were 55,299 up by 18% YoY

Total population covered is 81.1%

315 markets covered

They mentioned that the used car vehicle market was down ~15% while Carvana saw an increase in volume, this means that Carvana gained market share

Average monthly unique visitor was 23.5m, up 42% from last year

17 total number of IRCs up from 13 a year ago (Inspection centers) Excludes Adesa

Total website units were 78.9K (total website units as the number of vehicles listed on our website on the last day of a given reporting period)

Cost, Expenses and Cash Flow:

Total cost of sales was $3.48b up 25% from a year ago

Gross profit per vehicle sold was $3,368, up from previous month by $535

Gross profit decreased by $1,752 when compared to Q2 2021, a quarter that was highly inflated by the start of the rapid acceleration in used car vehicles due to the issues in supply chains.

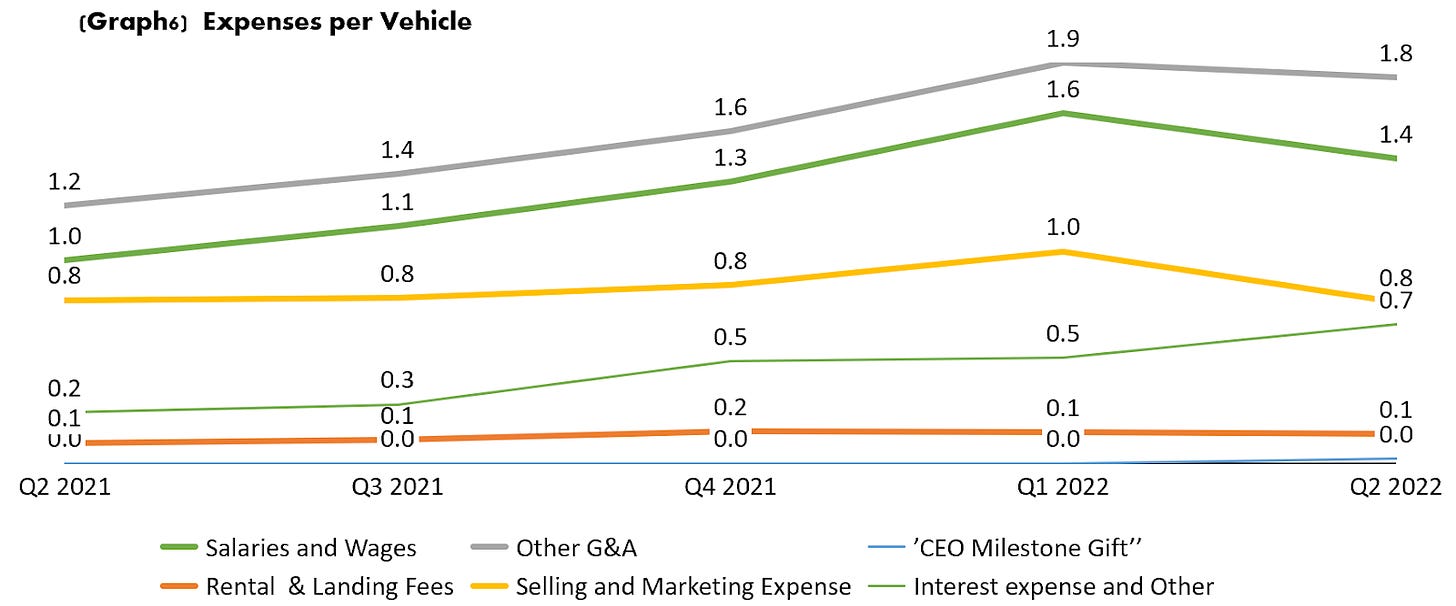

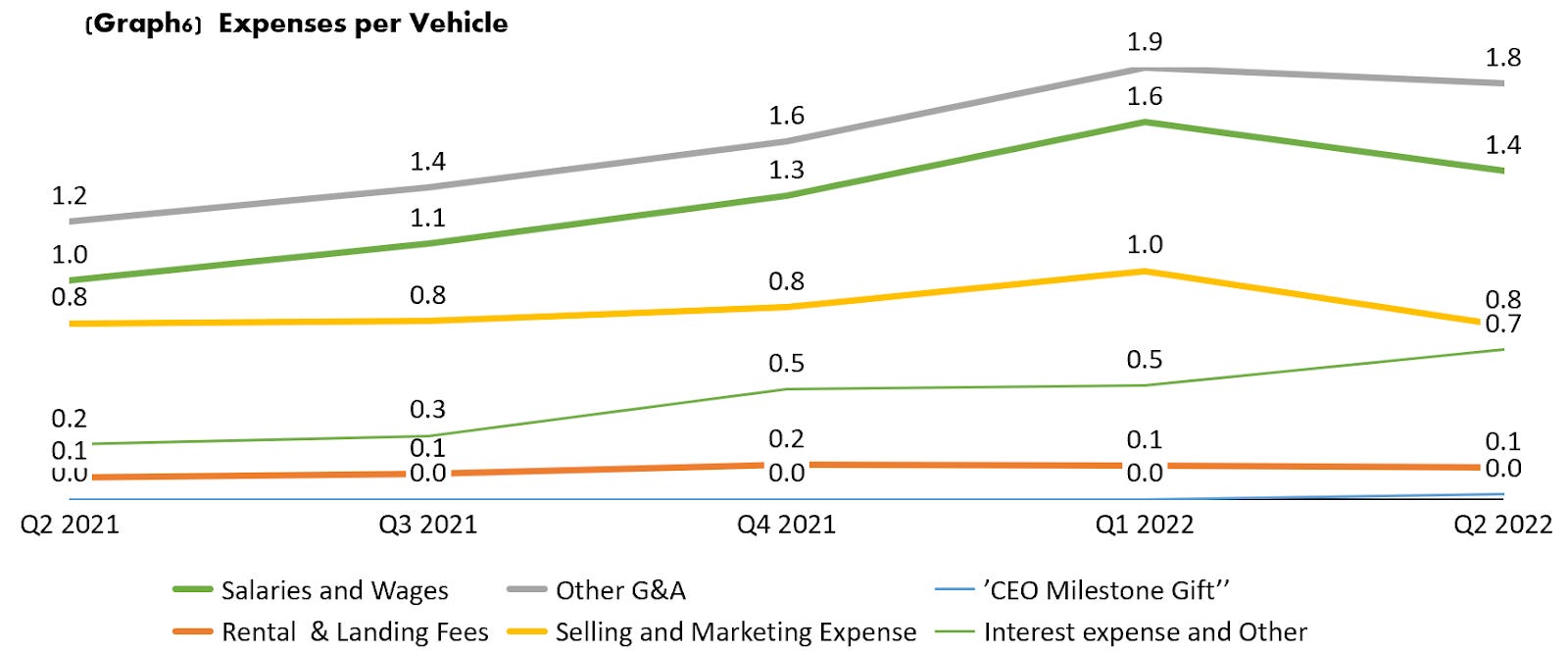

Selling General and administrative was $721 million almost flat vs last quarter ($727m)

SG&A per vehicle was $4.17K lower than the previous month by $505. The drop comes from lower expense salaries, wages and advertising.

Interest expenses per vehicle went up tp $614 vs $239 a year ago and $495 vs last quarter

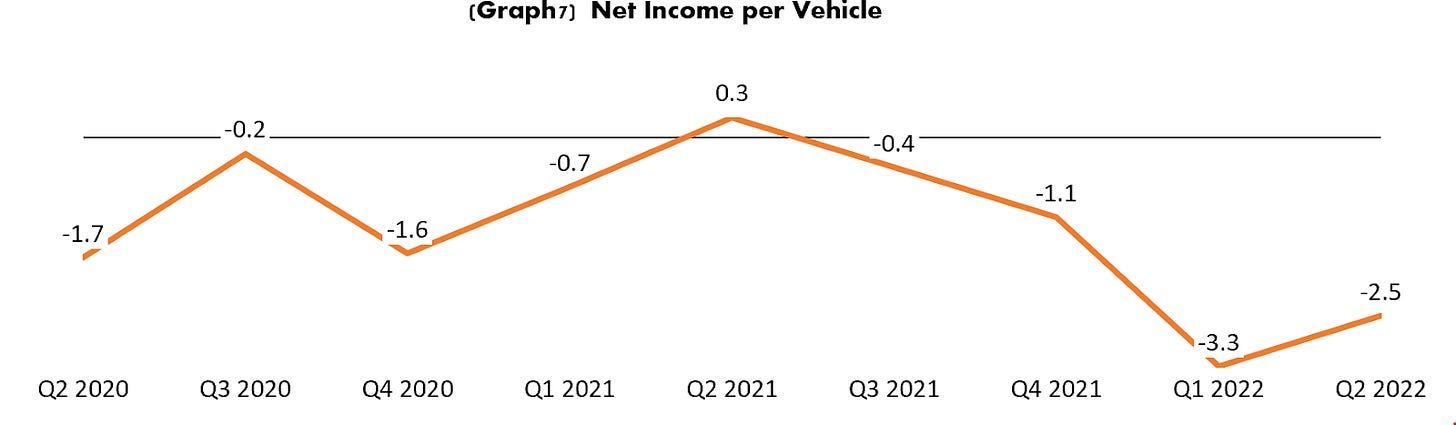

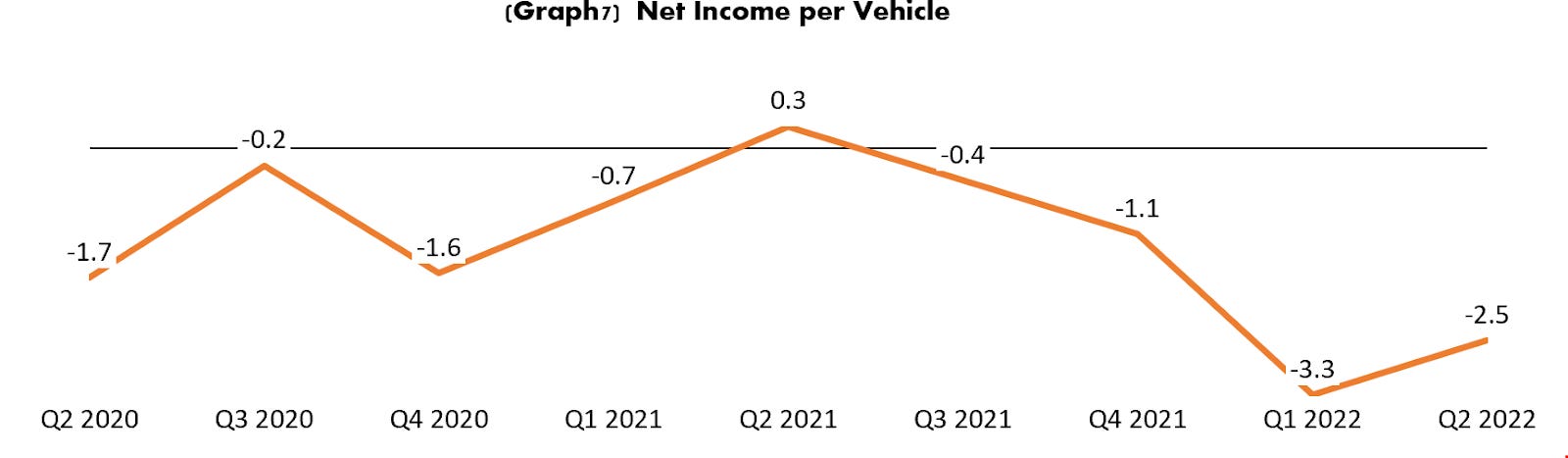

Net income per vehicle continues to be negative, but it improved to a loss of $2.5K per vehicle.

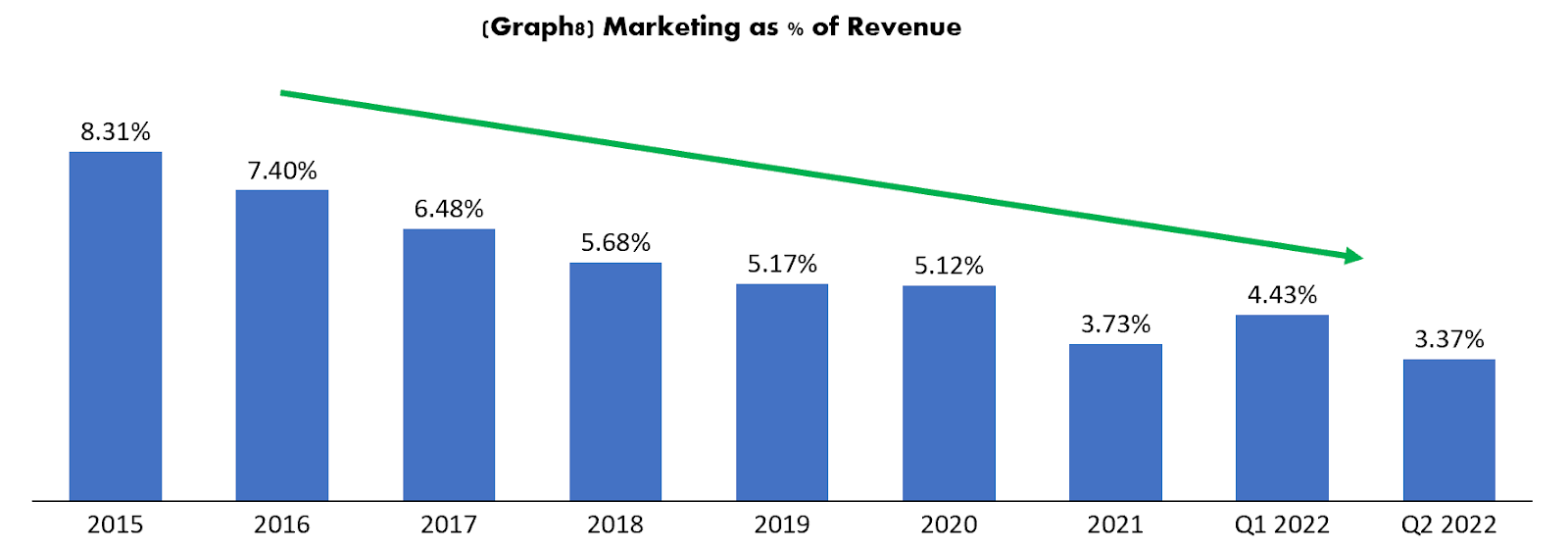

Marketing as a percentage of revenue represented 3.37% of revenue. Remains stable but still about 3 times what a competitor like Carmax is doing. (around 1%)

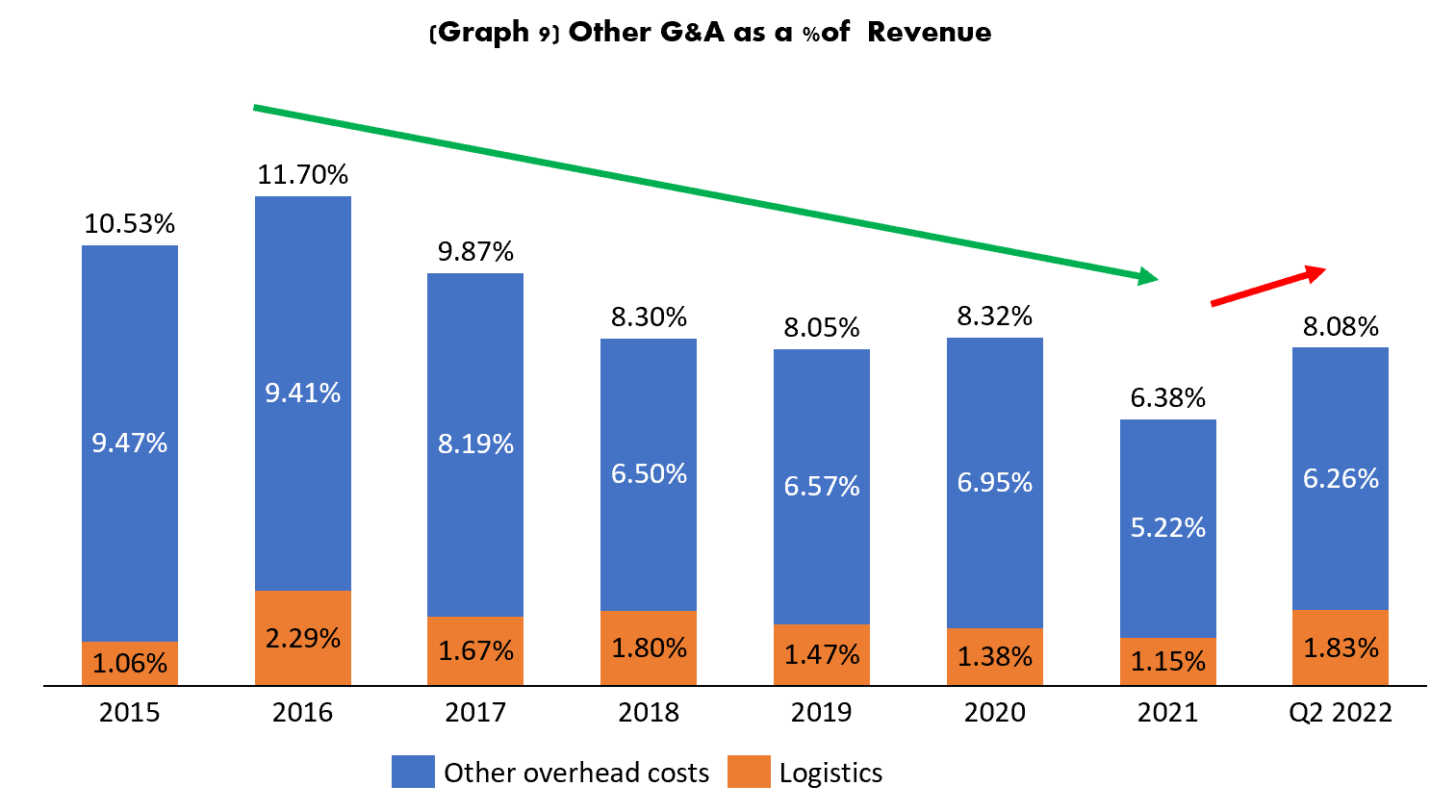

Other G&A continues to be their biggest issue. It has actually came back up and it continues to be incredibly higher than Carmax’s ~1.4%

Operating income for the company was a loss of $321 million. A little better but close to the previous quarter (loss of $401 million) Like all other companies Carvana shows an adjusted Ebitda measure. This again, is a Non GAAP measure and should be looked at in detail. Since you can adjust to anything you want, like “Wework’s Community Adjusted Ebitda’’

The Adjusted Ebitda they present is still at a loss, smaller, but still a loss of $230m. They stay in negative territory even when taking out most of the non cash expenses like D&A and any Stock based compensation not related to the milestone gift that was given to employees (That they made the terrible decision to call it “CEOs Gift” or “Ernie’s Gift,”, if it were his gift it would not be in the company’s financial statements. It is Carvana’s gift, making it a gift from all the shareholders, even if they want to brand it some other way)

When looking at their same measure from a year ago, the company had a worse performance. Last year the adjusted Ebitda was $121m, this is the same and only quarter in which the company was profitable but was the same quarter in which the used car market saw a rapid acceleration in price appreciation.

Carvana on average over the last 6 quarters has lost (from its operations) $513m each quarter. At this rate the amount of cash that they have would last them about 3 to 4 quarters. Q2 though had positive cash from operations, this came by the positive impact from the change in inventory, inventory came down by about $430m which helped return positive cash flow from operations. This could be a good step that they are taking towards having less exposure to high priced inventory when a possible crash in used car prices might come.

Balance Sheet

Carvana cash balance went up by nearly $800m to $1.4b

Carvana issued $3.275 billion in aggregate principal amount of 10.25% senior unsecured notes due 2030

The Company used the net proceeds from the issuance and sale of the 2030 Notes (a) to finance the $2.2 billion acquisition of the U.S. physical auction business of ADESA, Inc. ("ADESA") and other ancillary transactions to occur in connection therewith, and to pay related fees and expenses in connection therewith and (b) for working capital, capital expenditures and other general corporate purposes

During the quarter Carvana raised $1.2b in issuance of common stock

The Company used a portion of the net proceeds from the Class A common stock offering for general corporate purposes

Total debt at the end of the period was $8.6b, up from $6.7b the previous quarter

Inventory is now down to $2.8b from $3.3b at the end of Q1

Used Car Market

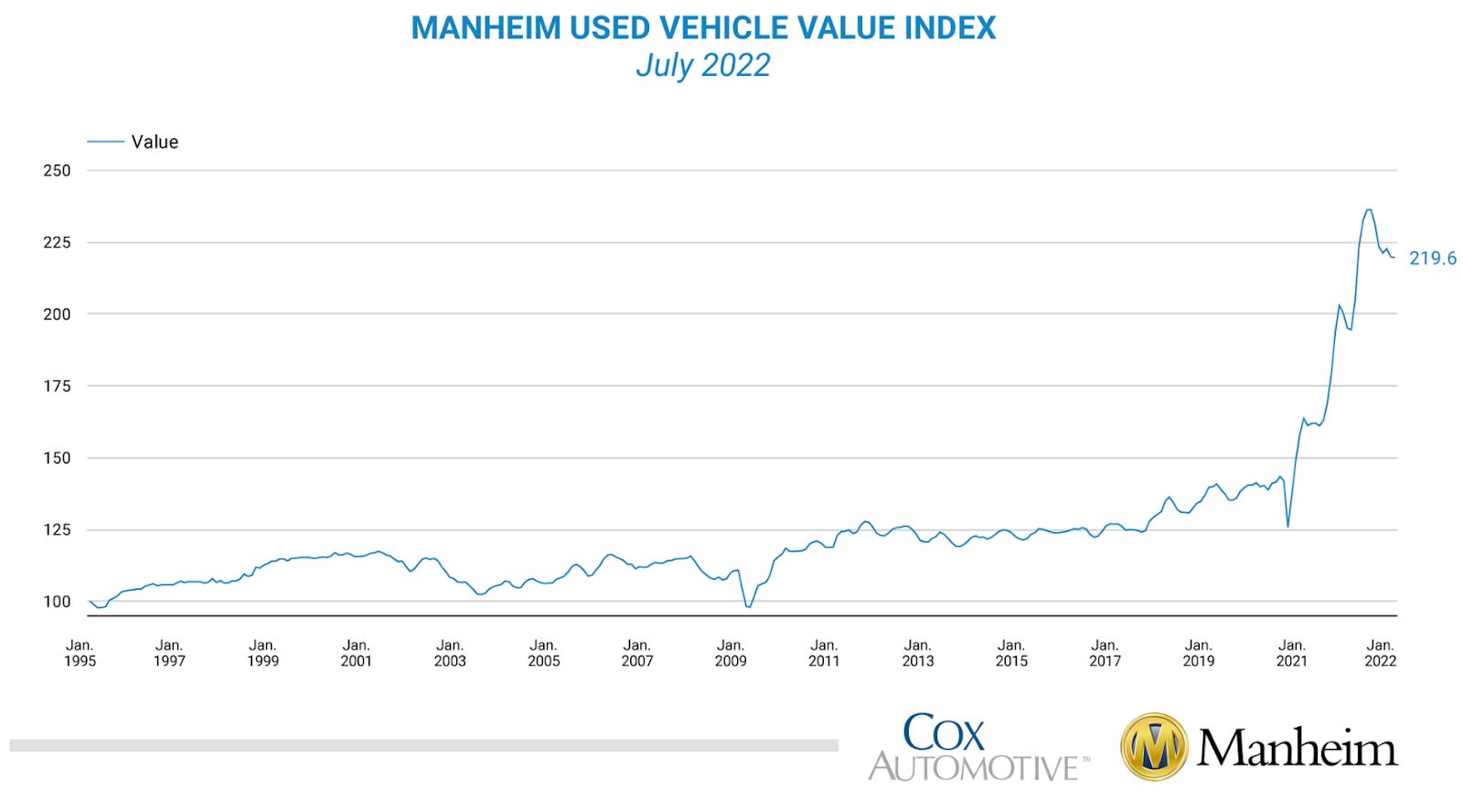

The used Car market seems to be holding for its next move. When looking at the Manheim Used Vehicle value index we see that it barely moved in July, it went down to 219.6 from 219.6. Still close to all time high, or at least, highest since 1995. This is not sustainable, we all know that prices will come crashing back down, and most likely this will be a fast correction. Either because supply chain issues start to improve, adding in the process more supply of new vehicles and removing pressure from the used car market, or, by economic issues of people that can no longer make payments of used cars that they got in the middle of the pandemic. When credit and stimulus cash was plentiful.

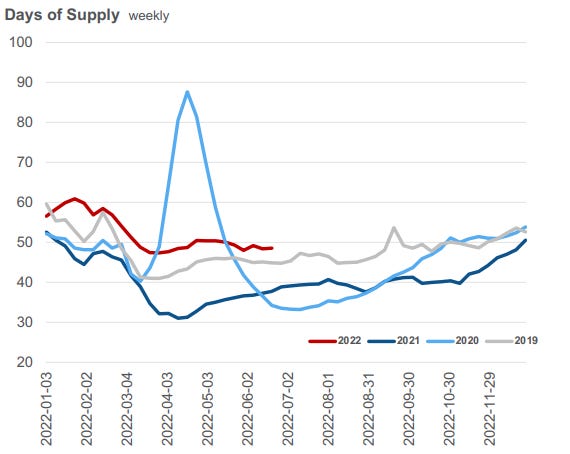

Available supply continues below 2019 levels by around 300K units, yet days of supply is above 2019

The risk here for Carvana is on their inventory. If the move in the revaluation of inventory is dramatic they might take a big impact in one quarter. It will not be anything dramatic that could bankrupt the company, but we will find out whether the cost structure at lower used car prices gets a hit degrading scale in the process. If they have many big fixed costs, their scalability will take a hit from lower prices. We will have to wait, what you see from the Manheim index is that it is not a matter of if? But when will the prices return to normal? these are not houses, these are depreciating assets, so it is far easier for them to correct back to normal levels.

Outlook

Carvana continues to operate in what we believe is the future of car buying. Everyone hates going to a dealership and having to go through the negotiating process, the haggling etc. Dealerships are the most annoying places for customer experience. So Cravana is playing in the right market. The question is whether they will have enough cash to last until they gather scale to make it a profitable business. Carvana reminds us a lot of Uber. A company that has had many cash burning quarters just to get to a point where their market situation is established, they have gathered a dominant market position and they can start having better profitability (Even Uber is not there yet as we have discussed on our Uber piece, but they sure are very close.)

For Carvana is growth at all cost, they are barely using the stock based compensation tool so far. (They average about $15m per quarter) They could use this a little more to preserve more cash and avoid having to go back anytime soon to the debt or equity markets. Yet despite this, their biggest question is whether they can scale or not. They are spending more today in absolute values in “Other G&A” than what an established company like Carmax does. This is where they have either an opportunity or a challenge, however you want to call it. It has not come down, it went up again above 8%, this is extremely high when their average (last 6 quarters) direct cost is at 87% (and 90% in Q2 and 91% in Q1) That leaves 5% for interest payment, marketing, others and profits. Not a whole lot of room to become profitable. Other G&A as seen in the graph has stalled at about 8% since 2018, without this improving they won’t have profitability. There are others expenses above industry benchmarks (like marketing) but nothing can really make an impact as much as fixing “Other S&A”

At LongYield we believe that nothing has changed fundamentally since our last piece on July 11th. The company is still yet to show improvements in their path to profitability. They still are not showing how they will stop burning cash through their operations. They need to take the turn fast, because the more they grow in terms of units sold, the likelihood that the more they will lose in absolute values and then the faster they will go through their cash and the faster they will be tapping into debt or issuing common stock again.

The likelihood of the company going under we see it as low , the brand is strong (despite recent operational issues and bad press on how they process titles) and the business model is here to stay. Everyone will copy it, we see Carmax already becoming more Carvana like. Yet we see that the company will continue to burn through cash to grow, a possible scenario like we mentioned in our previous piece is that they are acquired by a cash rich company that can fund all of that growth. Another likely scenario is that they find their own Softbank, a heavy investor that is willing to continue to fund the company through their growth phase.

Given all of this, the fundamental valuation is still the same in our view, the company still should be valued at about $18 per share in our base case and $50 per share in our optimistic case. When you take into account the hope that they will be the market leaders and will realize everything they want they still could be valued at about $30b to $40b in the future. This if they manage to use all of their capacity efficiently. This is the key, the efficient use of their capital, they need to show improvements in scale, they need to show that the more they sell the more profitable they become, not the other way around. Once they do that for some quarters, their valuation should look a lot different, you could say by then the stock would already be way higher, and that might be true, but that becomes speculation territory and it is not the focus of this piece.

Read our Previous Pieces on:

Opendoor Peloton Carvana Rivian Roku