Open reported Earnings recently, their revenue was just inside the guide given the previous quarter. The immediate reaction from the market was a loss of 7%, yet quickly it gained everything back and then some. The next day the stock was up +20%, despite guiding just $2.2 b to $2.6b in revenue for the third quarter. This was influenced by the news that Opendoor and Zillow will go into a multiyear partnership, where Zillow will allow homeowners to request an Opendoor offer on their platform.

Thanks for reading LongYield! Subscribe for free to receive new posts and support my work.

Performance Summary:

Revenue

Q2 2022 Revenue was $4.2b up 254% vs Q2 2021

Revenue was down 19% vs last quarter

YTD Revenue $9.3b vs $1.9b last year 383% growth YoY

Key Metrics:

10,482 Homes sold, up by 204% from Q2 2021

Homes sold in the quarter came down by 17% or 2,187 fewer homes

14,135 homes were purchased in the quarter the highest since Q3 2021, which was 15,181

The inventory at the end of the quarter was 17,013, higher than previous quarter close (13,360)

The value of the inventory at the end of the period was $6.6b

Opendoor finished the quarter with presence in 51 markets, up from 45 at the end of March 2022

These 51 markets cover 30% of the real estate market transactions

Offer requests grew 69% YoY

As of June 30, 2022, 5% of homes were listed on the market for more than 120 days, down from 7% in Q1 2022. Better than the 14% of the homes in the overall market (adjusted for Opendoor’s buy-box)

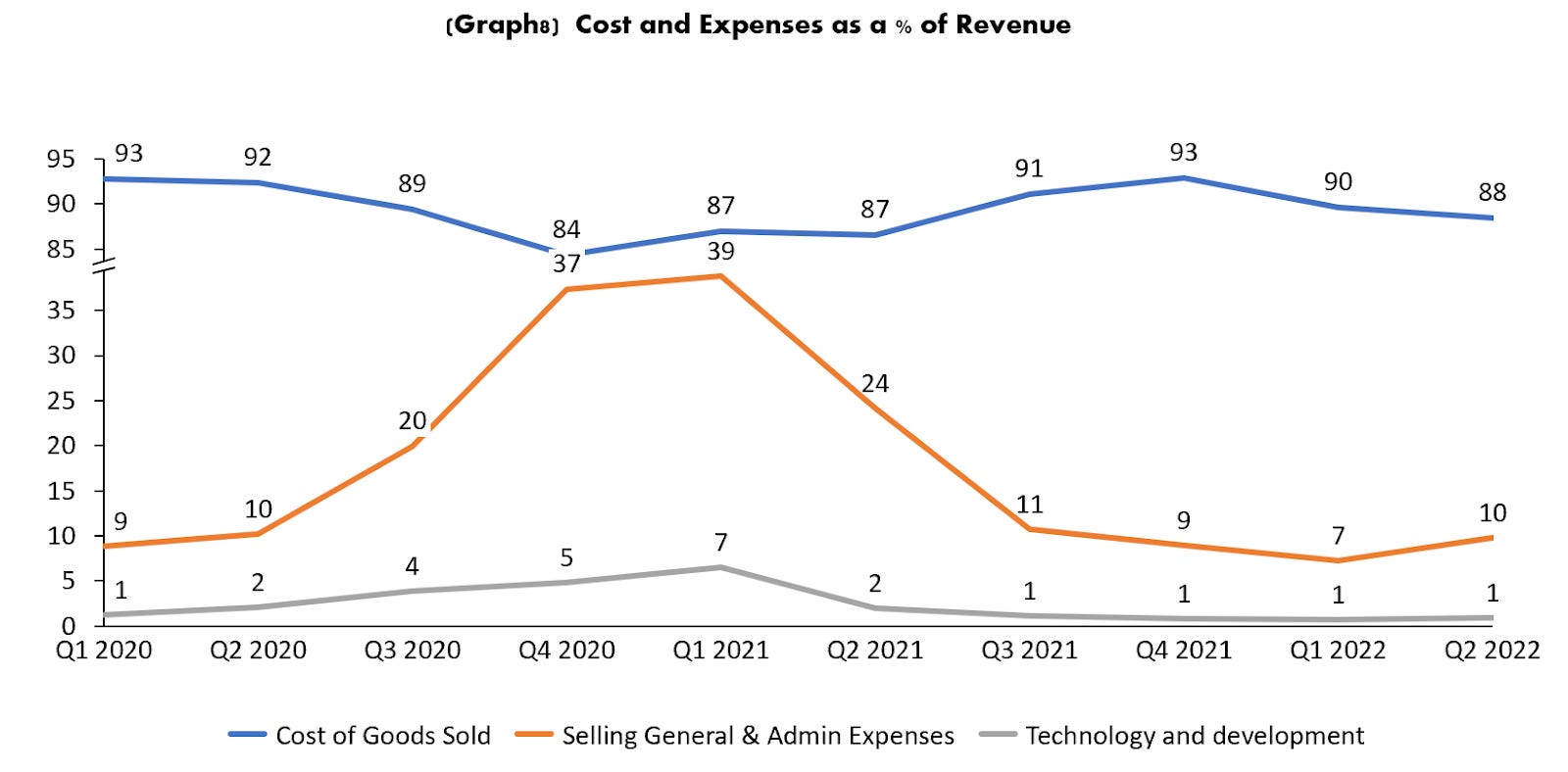

Cost and Expenses:

Cost of sales was 261% above Q2 2021. This is expected as the number of homes sold increased as well, but compared to 254% growth of revenue, cost grew faster than revenues.

Cost of sales per home was $354K up 20% YoY, increase is a result of inventory mix, home price appreciation and Buybox expansion. (Assuming all cost of sales divided by homes sold. Cost of sales includes the property purchase price, acquisition costs and direct costs to renovate or repair the home)

Sales, marketing and operations was $276m up 185% YoY

Sales, marketing and operations expense consists primarily of broker commissions, resale closing costs, holding costs and expenses associated with product marketing, promotions and brand-building

Advertising $46m up from $32m last year

Direct selling costs for the period were $100m down from $136m the previous quarter (Direct Selling Costs: Represents selling costs incurred related to homes sold in the relevant period. This primarily includes broker commissions, external title and escrow-related fees and transfer taxes. )

Direct selling cost per home was $9.5K vs $10.7K the previous quarter

Holding costs on sales for the current period were $11m, down from $16m in the previous quarter (Holding costs include mainly property taxes, insurance, utilities, homeowners association dues, cleaning and maintenance costs. Holding costs are included in Sales, marketing, and operations on the Condensed Consolidated Statements of Operations.)

General and Administrative was down 28% vs last year. This shows great scale considering the total homes sold was considerably higher this year vs last year

General and Administrative reduction was primarily attributable to a $113 million reduction in stock-based compensation due to the expense recognition of certain performance awards during the six months ended June 30, 2021

General and administrative expense consists primarily of headcount expenses, including salaries, benefits and stock-based compensation for executives, finance, human resources, legal and administrative personnel

Technology and development was $41m, T&D consists in design, development, testing, maintenance and operation of mobile applications, websites, tools and applications that support their products

Operating income from operations was $32m, second quarter in a row with positive income. ($118m in Q1 2022) Ebitda was $52m, also the second positive quarter in a row, and like many other companies Opendoor presents adjusted Ebitda. This was $218m. Like we have mentioned in other articles published, never trust an adjusted Ebitda, at least not without having a look at how they came up with the number.

There are many values that are non cash expenses but things like property financing and interest expenses are values that, even though they are not part of Ebitda, they are a core part of Opendoor business. Opendoor does asset backed financing so this is why Adjusted net income could be a better measure, this was $122m for the period. Regardless of how we look at their performance, in most of the metrics they are either profitable or close to being profitable. The Only one that is still negative is net Income, which was -$54m for the quarter.

Balance Sheet

Cash And Short Term Investments close the period at $2.47b down from $2.77

Cash And Equivalents was $2.2b, enough to hold through the coming downturn in the real estate market

Additionally Opendoor holds $615m in restricted cash

Short Term Investments were down from $464 to $233m

Total debt $7.5b, of which $4.1b is long term debt and $3.4b is short term debt.

Inventory like mentioned before was $6.6b, this number is important and it is important to compare this to total debt, since Opendoor finances its home purchases with asset backed debt, these two numbers usually move very closely together.

Thanks for reading LongYield! Subscribe for free to receive new posts and support my work.

Operational highlights

Opendoor launched Opendoor Exclusives, this is a new product where people are able to buy Opendoor properties pre market in an “e-commerce like” experience. Some of the highlights of this product are:

Exclusive prices for 14 days

Set price, not bidding wars, transparent pricing from the start.

You can back out anytime before closing, and still get 100% of your earnest money deposit back

Appraisal Price Match Guarantee, if home appraises for less they will match that price

Self tour available

Currently only available in Austin, Houston, and Dallas-Fort Worth, TX

Zillow Partnership

Opendoor announced in this quarter earnings release that they will be partnering with Zillow. Home owners will be able to request an offer from Opendoor via Zillow. Some of the details available now for this partnership are:

Opendoor offers will be available on Zillow, and customers will be able to use the service as a standalone offering

Homeowners could also package it with other Zillow home shopping services such as financing, closing and agent selection.

Zillow customers will be able to work with a Zillow advisor who will serve as a guide to help understand their options if packaging with some of Zillow products.

This news came as a surprise, especially after Zillow trying and failing at the ibuyer industry just last year. Zillow exited this business saying “that further scaling up Zillow Offers is too risky, too volatile to our earnings and operations, provides too little opportunity for return on equity” . Now Zillow is back in the business as a partner of the strongest player in ibuying.

For Opendoor this is a huge opportunity to scale and grow rapidly without any huge increase in marketing expenses. Zillow is the most visited website for real estate in the US. This will make it far easier for Opendoor to penetrate new markets and accelerate their brand awareness at lightning speed. We don’t know the details on how much it will cost for them, or how much of revenue share Zillow would take, but it will be far faster and far cheaper for them to go with Zillow than by themselves.

In the future what we see is a likely merger or a likely acquisition from one of them on the other. Zillow was already trying to enter this market, and already trying to digitize the buying of homes. They failed at it, Opendoor does it a lot better. The two together are the best at what they do, in our opinion it is very likely that they would end up being only one company, and probably the one that could end up being the one acquiring could actually be Opendoor. They have a huge addressable market that, with the help of Zillow, could grow revenue and market cap very quickly making them a far bigger company soon. Today Zillow is worth $9.5b while Opendoor $4b, this could change very quickly.

Outlook

As we all know, the Real Estate market is slowing down, and slowing down fast. Existing home sales have gone from 6.49 million in February to 5.12 million in July. This is the result from the rapid rise in mortgage rates in the US. They went from 3.0% in December 2021 to 5.81% in June. They have since come down to 5.22% today. Mortgage rates mirror mostly what the 10 year yield does, and the 10 year yield went rapidly up to 3.49% at its high due to a rise in inflation and inflation expectations, that had also the Fed raising rates many times (now sitting at 2.5% on the overnight rate) The 10 yield has since come down, and it is now moving around 2.7% to 2.8%. It has come down now mainly because the market is actually starting to see a recession coming soon and inflation expectations have come down with that. Recessions usually bring a decrease in the 10 year yield, so if the recession in fact comes, we would expect the mortgage rates to actually dip below 5% and likely get close back to the 3% to 4%, but all of this with time. First we need to get closer to the recession, we need the pivot from the Fed etc. But it is actually more likely for mortgage rates to actually come down than continue to 6% or 7%. (This unless inflation actually continues up and we are actually in a stagflation environment, which is a possibility, but less likely.)

Given all of this uncertainty, Opendoor in their call gave a pretty direct plan on the reasoning why their guide for Q3 is considerably lower to what they accomplished in Q2. They summarized their approach with three main initiatives:

Increase spread levels, they have been doing this since May but this will continue through the third quarter

Adjust down inventory prices to stay in line with market prices

Lower Marketing spend

These actions will decrease acquisitions, will bring down inventory to what they call a ‘‘healthy level’’, and it will lower margins of previously purchased inventory. Profitable first half of the year gives them room to accomplish full year goals still with the coming headwinds.

Opendoor has passed through three uncommon market situations. First the start of the Covid pandemic, second, the acceleration of home price appreciation just after Covid and third the fast pivot in the market and the crazy acceleration of the mortgage rates to the upside. Opendoor has shown that it can move through these uncomfortable market situations very well. That can manage and use levers within its business to adjust to any market situation without wrecking their income statement or their balance sheet. Once we finally reach a stable market Opendoor has an amazing opportunity for further penetrating the market. Now with Zillow that would be even easier.

Opendoor is currently valued at around $4b, in all the scenarios that we have calculated in our DCF analysis we considered that Opendoor is undervalued. The differences between each scenario in terms of assumptions is mainly how fast they would reach profitability, how high the penetration would get and the difference between the cost of capital, very important for a company that constantly will need asset backed debt and that these rates will move with the market constantly.

Our base scenario gives us a valuation of $16.5 per share or about $10b, our conservative scenario would be $9.6 per share or about $6.0b and an optimistic scenario of $27 per share or about $17b. We believe that the current valuation of $3.96b is impacted by both the bear market and the fact that this company might be greatly misunderstood. Most people that just look at the company from a high level would think that the coming slowdown will wreck a company like this. But looking at it in detail this seems to be greatly exaggerated.

Thanks for reading LongYield! Subscribe for free to receive new posts and support my work.

The Content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained on our substack constitutes a solicitation, recommendation, endorsement, or offer by LongYield or any third party service provider to buy or sell any securities or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. LongYield participants may or may not hold positions or interests in stocks discussed in this website.