Peloton reported earnings a couple of weeks ago, the only thing that is certain about the company so far, is that this company will definitely be remembered and mentioned as an example for many decades in the future. Either it will be because of a huge turnaround or it will be remembered as a perfect example of the “everything bubble”, a bubble that allowed a company offering a “bike with an iPad” reach a $50b valuation,, as of now, we still don’t know which way the company is taking, the only thing we know, is that the company is still restructuring and still struggling, and that the market so far is still reacting poorly every time they report earnings. This time it went from $13.48 to $11.01 after reporting earnings, a 18% loss of value. The following days it continued to drop, closing on Friday at $9.44 or a valuation of $3.19b. In this piece we will summarize and analyze their latest earnings report and try to figure out if its new management is starting to turn around the company or not

Performance Summary:

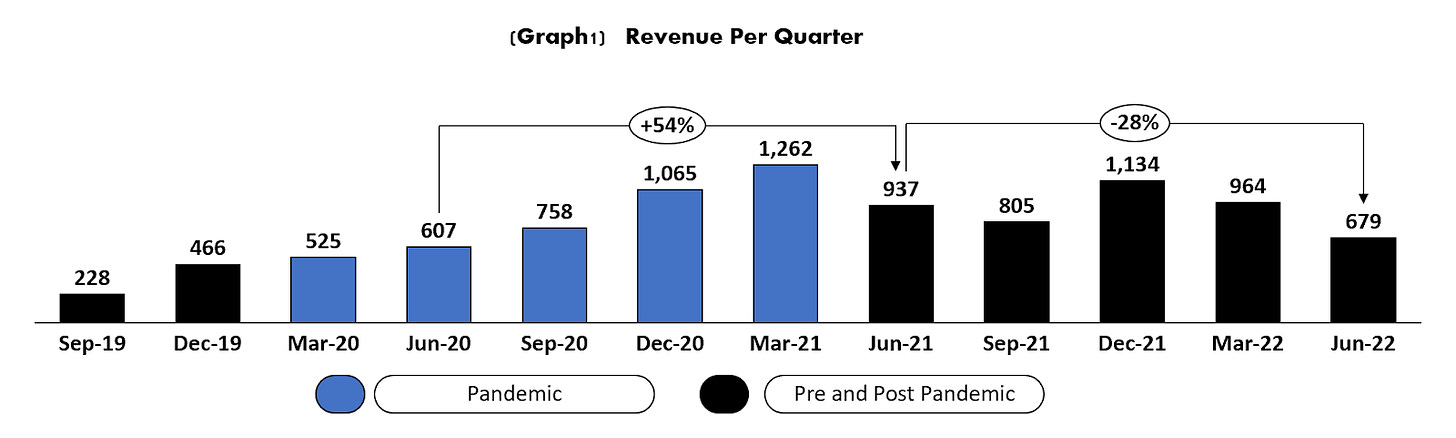

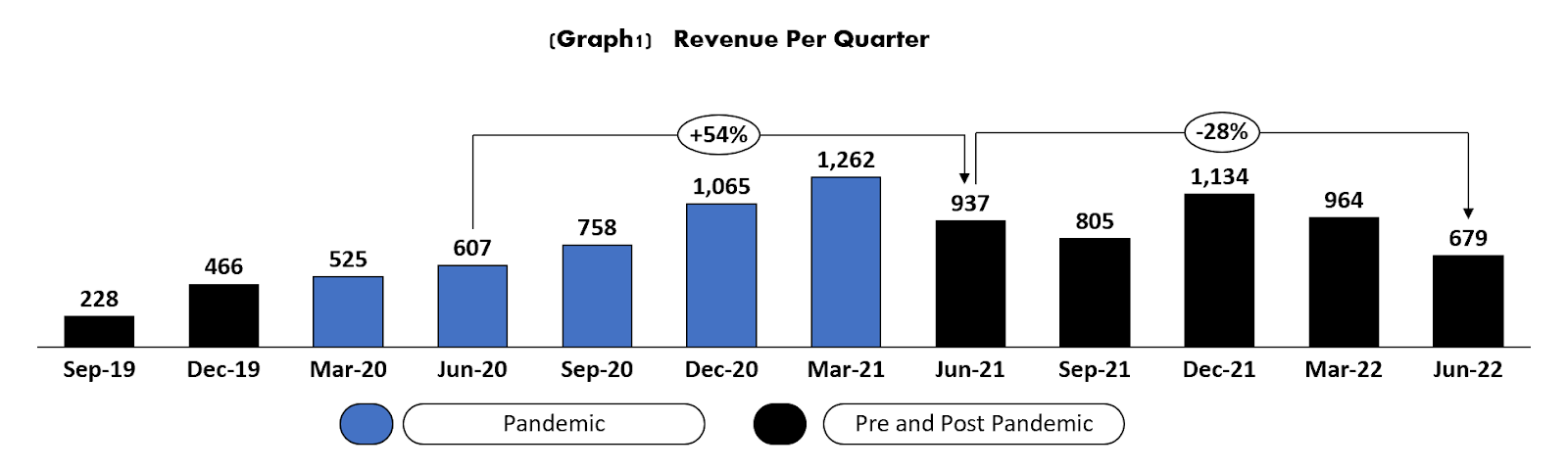

Revenue

Revenue during Q4 2022 was $679 million (Their fiscal year ends in June)

The revenue accelerated its drop to 27.6% YoY v. 23.6% YoY during Q3 2022

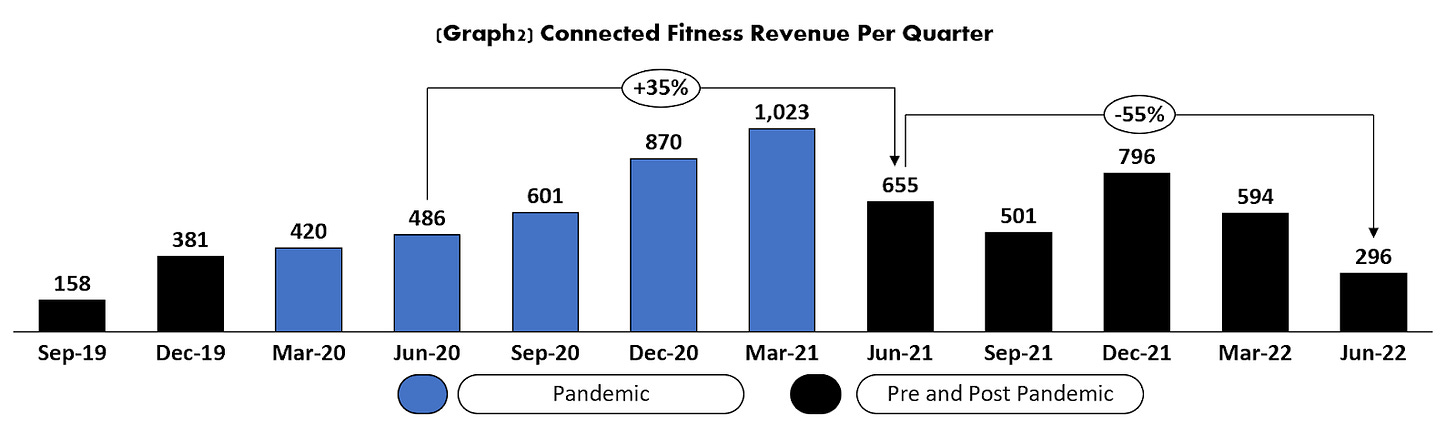

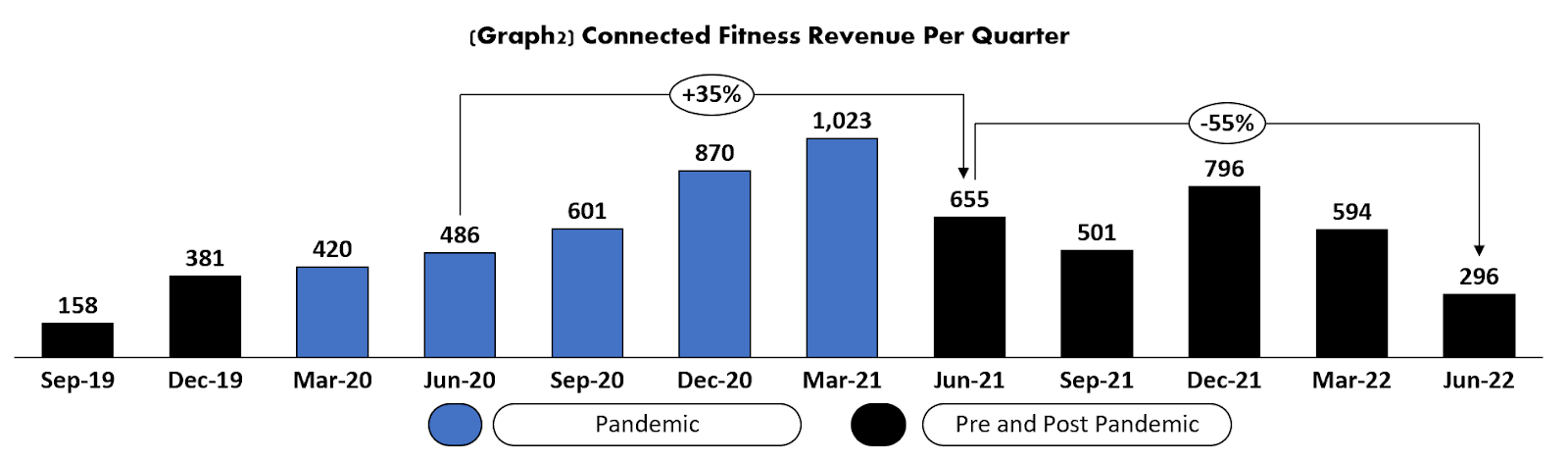

Connected fitness revenue during Q4 2022 was $296 million, down 55% from a previous year

Subscription revenue during Q4 2022 was $383 million, up 36% from previous year

Connected fitness revenue drop is accelerating to -55% YoY from -42% during Q3 2022

Subscription revenue growth was 36% YoY from 55% during Q3 2022

Revenue over the last 12 months was $3.58b down 11% from preceding 12 months

Connected fitness revenue over the last 12 months was $2.2b, down 30% over the preceding 12 months

Subscription revenue over the last 12 months was $1.4b, up 60% over the preceding 12 months.

Thanks for reading LongYield! Subscribe for free to receive new posts and support my work.

Key Metrics:

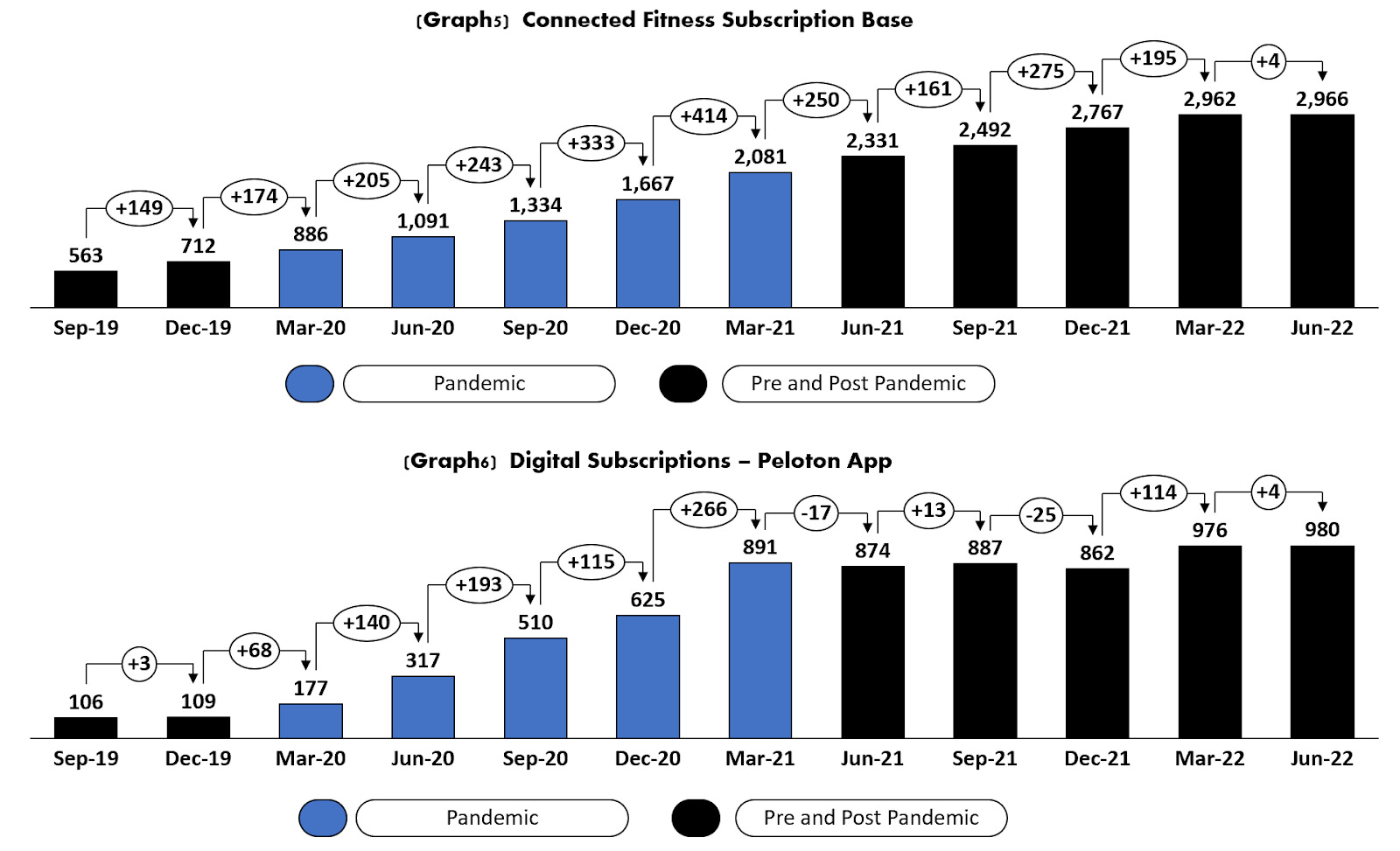

Connected subscription base ended the period at 2.96 million

Connected subscription net adds during the month was the lowest in recent quarters at only 4K

Churn went up to 1.44% from 0.75% the previous quarter. A rise was expected given the price increase of the all access membership

Churn is distorted, Peloton included Canadian customers as churned customers until they wait for Canadian Members to actively approve Connected Fitness subscription price increase. Absent this action, reported ending Connected Fitness subscriber count would be approximately 16 thousand higher

Implied gross additions were about 129K (This is calculated using the churn level and the net adds announced by the company)

Application subscription base ended the period at 980K, net adds for the period were 4k as well

14.8 Average Monthly Workouts per Connected Fitness Subscription.

Cost, Expenses and Cash Flow:

P&L

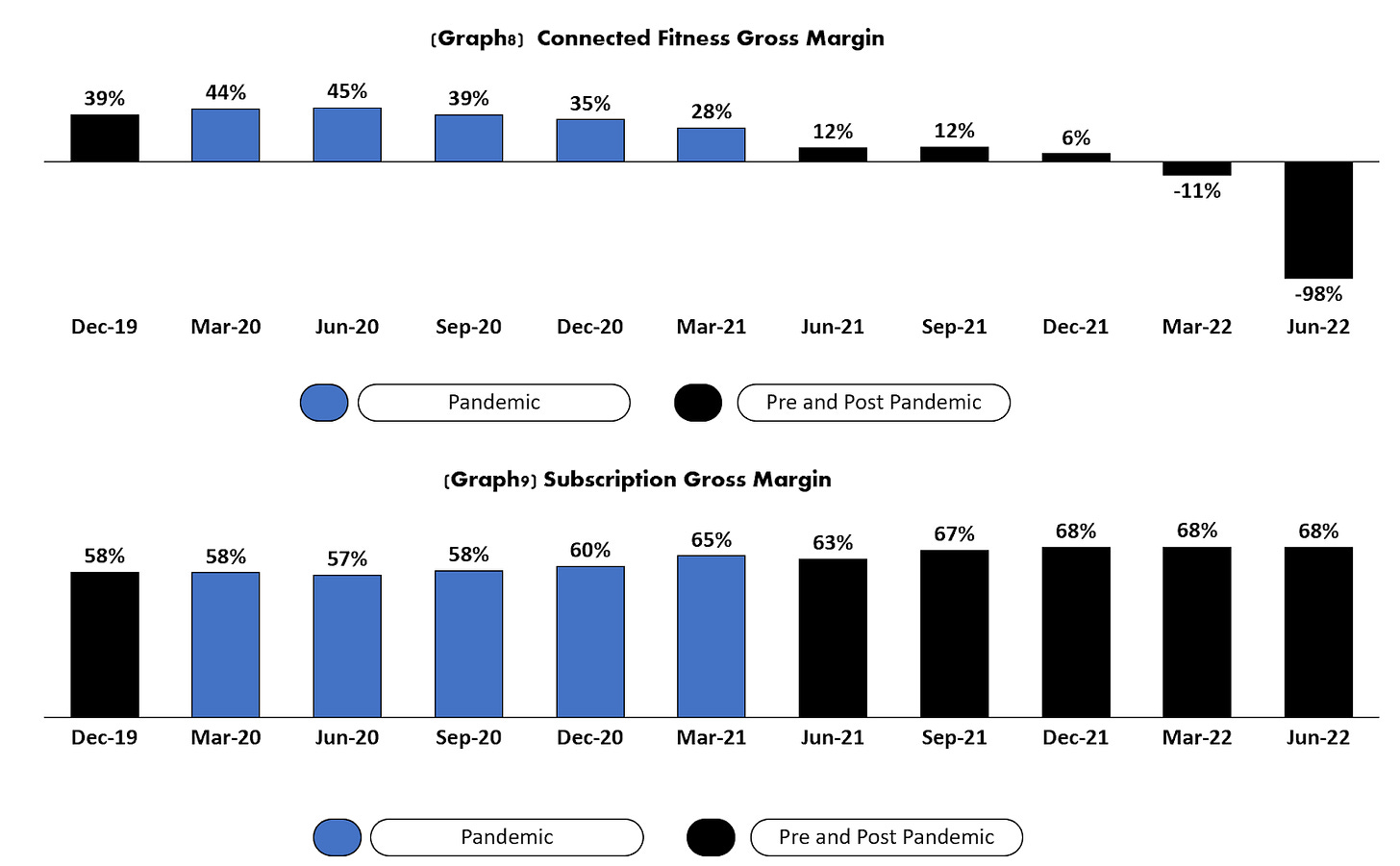

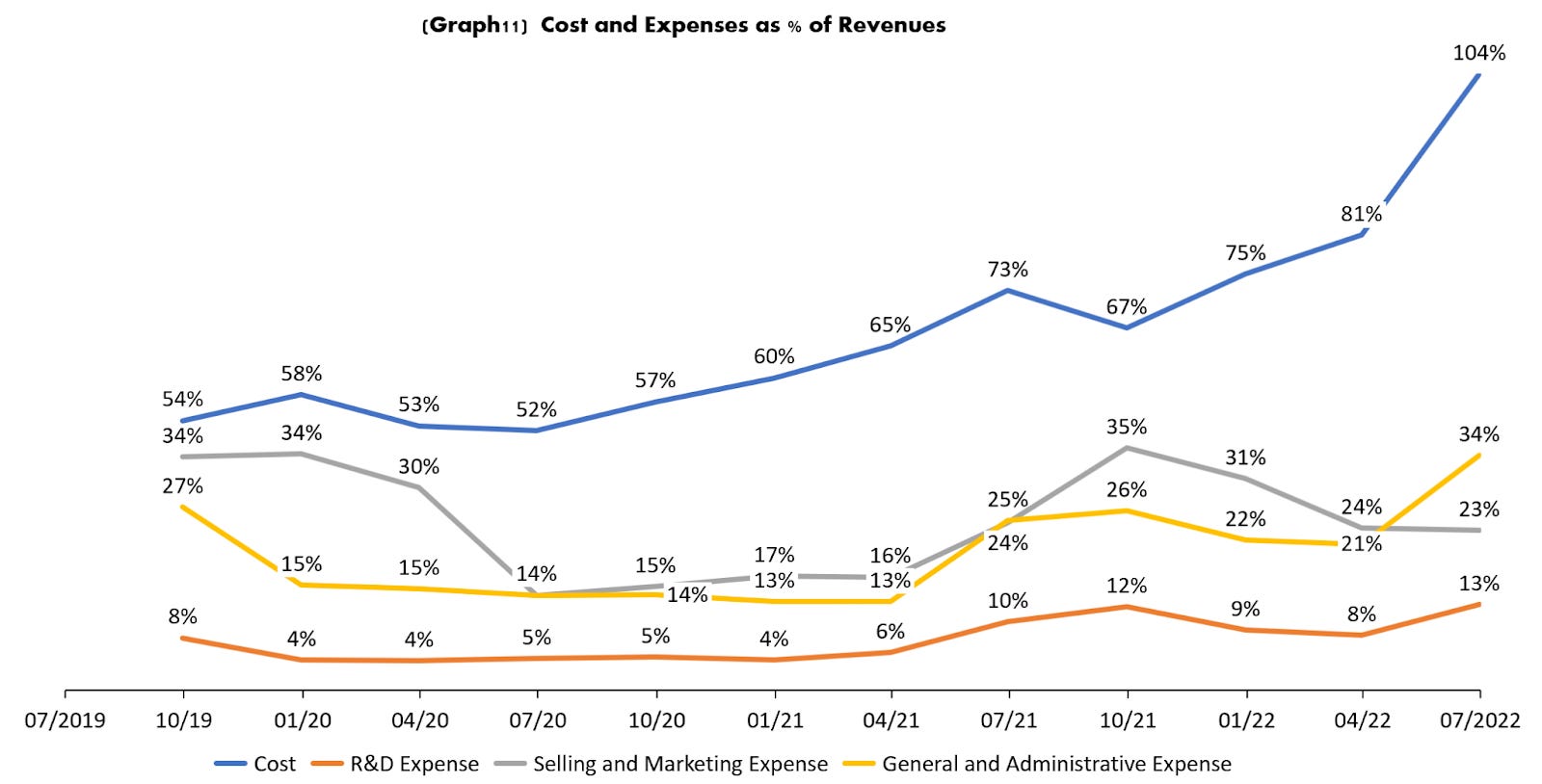

Direct cost was $709 million or 104% of revenue

Direct cost was up 4% YoY

Connected Fitness direct cost were $586 million or 198% of Connected Fitness revenue

Subscription direct cost were $123 million or 32% of subscription revenue

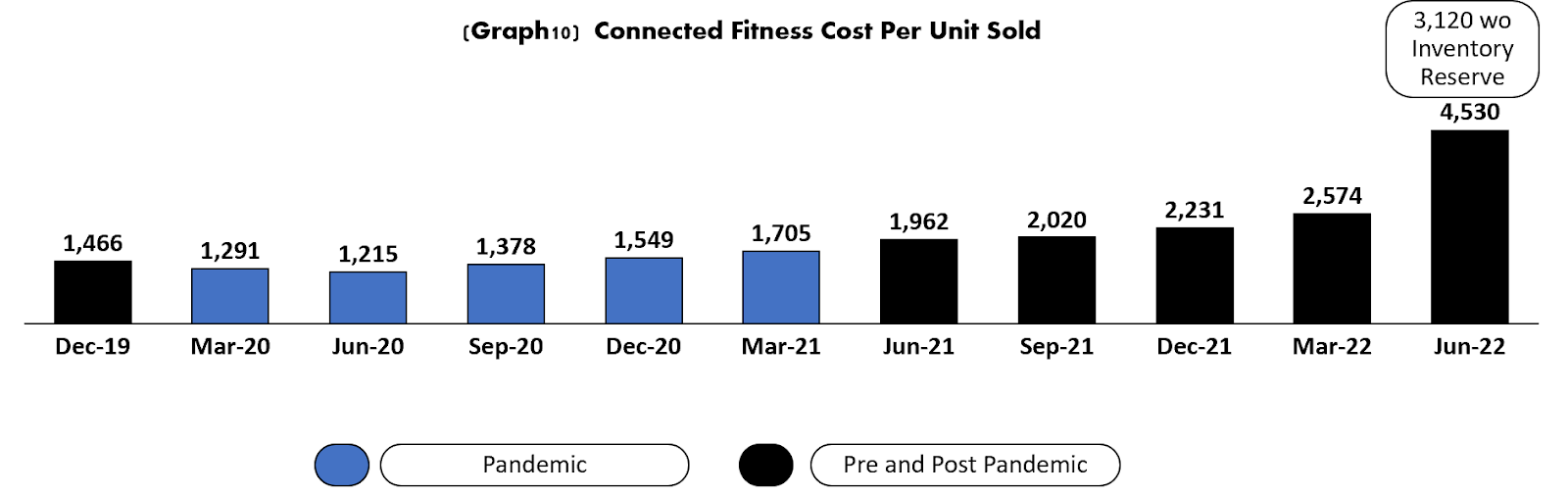

The rise in connected fitness cost was driven by a significant increase to inventory reserves of $182.3 million. The inventory reserves are primarily related to excess accessories and apparel inventory that they do not expect to sell above its current carrying value

Using our calculated gross adds, connected fitness cost per unit sold was $4.5K, when excluding the 182 million of excess reserves this goes down to $3.1K, but this number also has higher cost of delivery, storage and a few other operational issues

Sales and Marketing was down vs previous quarter at $158 million

Sales and marketing per Connected fitness subscription gross add was $1.2K, up from $0.9k during the previous quarter. (This number is not 100% accurate, we should really take also the application gross adds and the total gross over the renting product, but there is not enough information available to calculate this, so to keep the visibility of a trend we are using only connected fitness gross adds.)

General and administrative was also up during the quarter, from $205 million in Q3 to $232 million in Q4

R&D also increased to $85 million, up from $77 million a quarter ago

During this month Peloton recognized the following one-time expenses ($697 million):

$337.6 million of supplier settlements,

$337.2 million of non-cash impairment expense for write-downs and write-offs of fixed and intangible assets, primarily related to restructuring initiatives

$22.2 million of restructuring expenses.

Excluding non recurring charges on the quarter their operating expenses declined 14% YoY to $475.2 million (vs $555 million in the quarter ending June 2021)

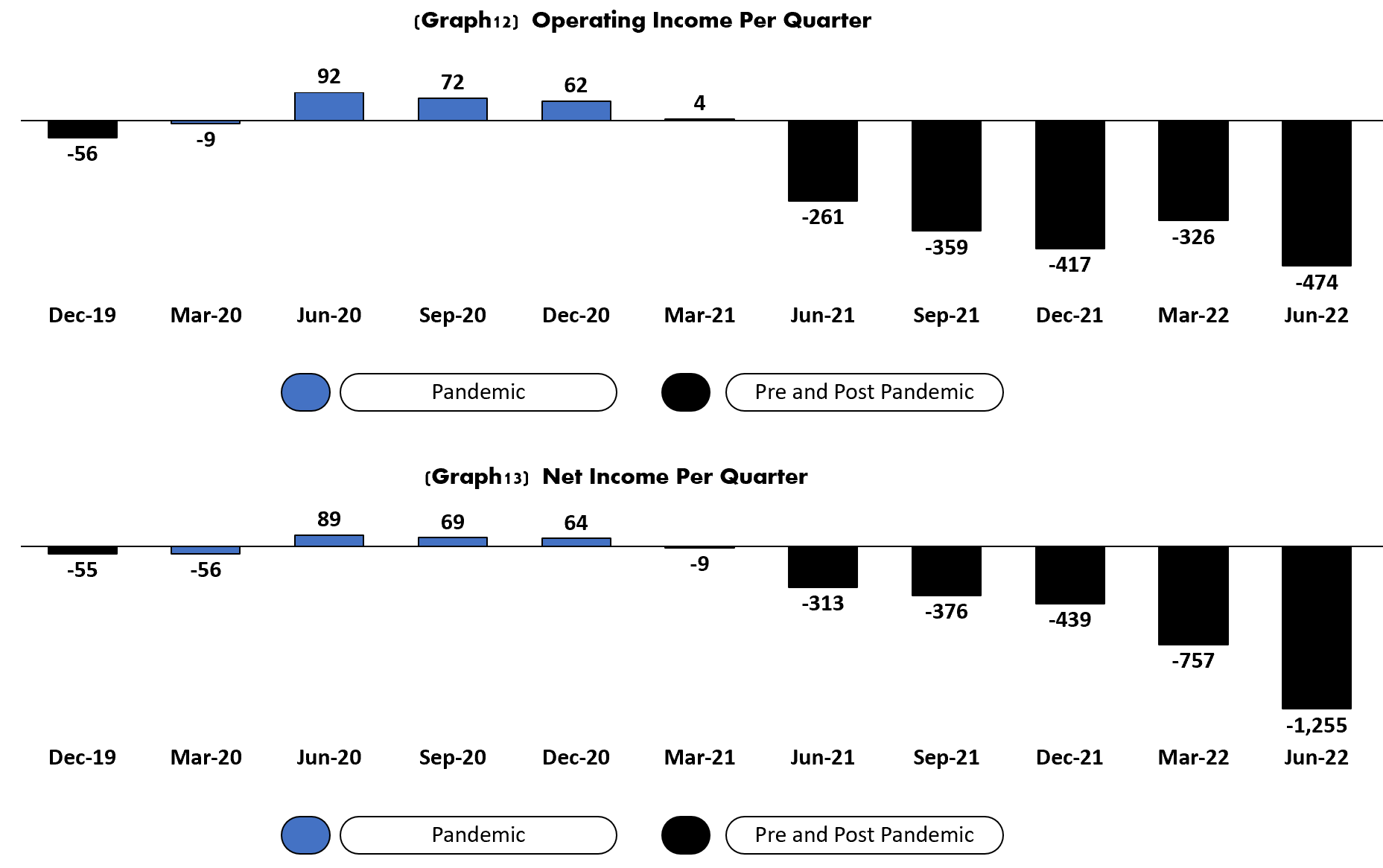

Excluding the $182.3 million inventory received and all the non recurring expenses, the quarterly loss for the period was about $322 million, $909.6 million less than the reported net loss of $1.2b

Over the last two quarters Peloton has had an accumulated net loss of $2 billion. This has been the time in which heavy restructuring of the company started. During these two quarters Peloton had $209 million in restructuring charges, $182 million of impairment of goodwill, $342 million in asset write downs, $338 million in supplier settlements and $36 million in legal settlement, all of these restructuring expenses add up to $1.1 billion, leaving an $880 million loss over the past two quarters.

Cash Flow

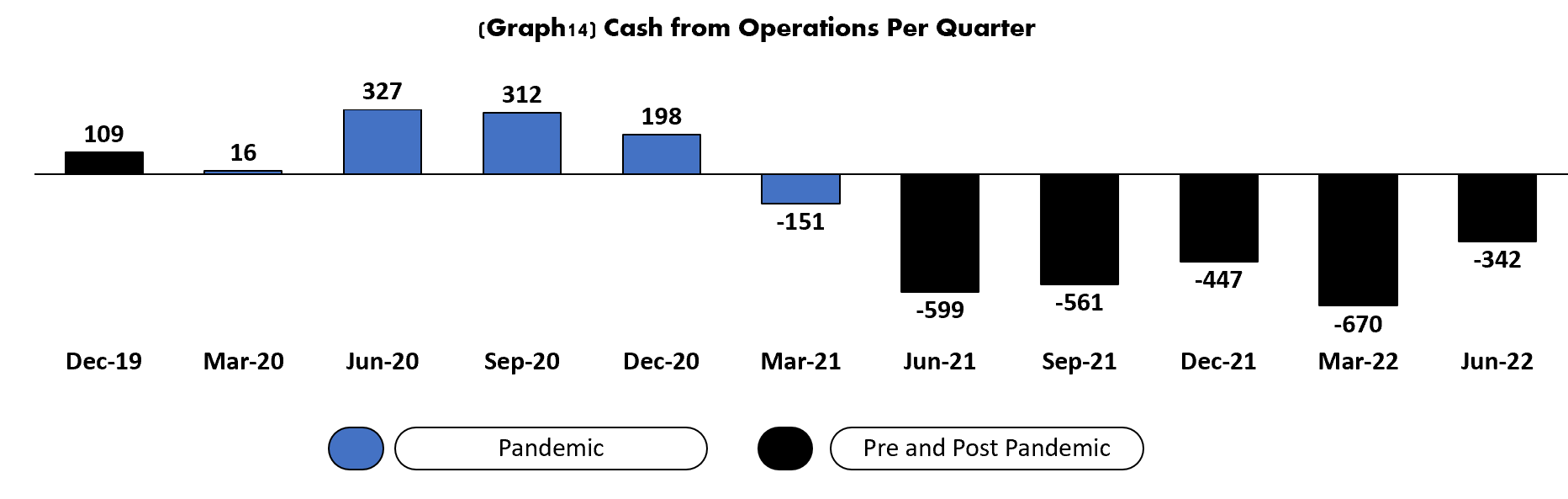

Despite having $2 billion in losses during the past two quarters Peloton has only lost $1 billion in cash from its operations. They have been helped by non cash expenses like $204 million in stock based compensation and $554 million in asset write downs

The company has gone through $2 billion from operations over fiscal year 2022, but Q4 2022 was their best quarter in terms of cash used since fiscal quarter Q3 2021

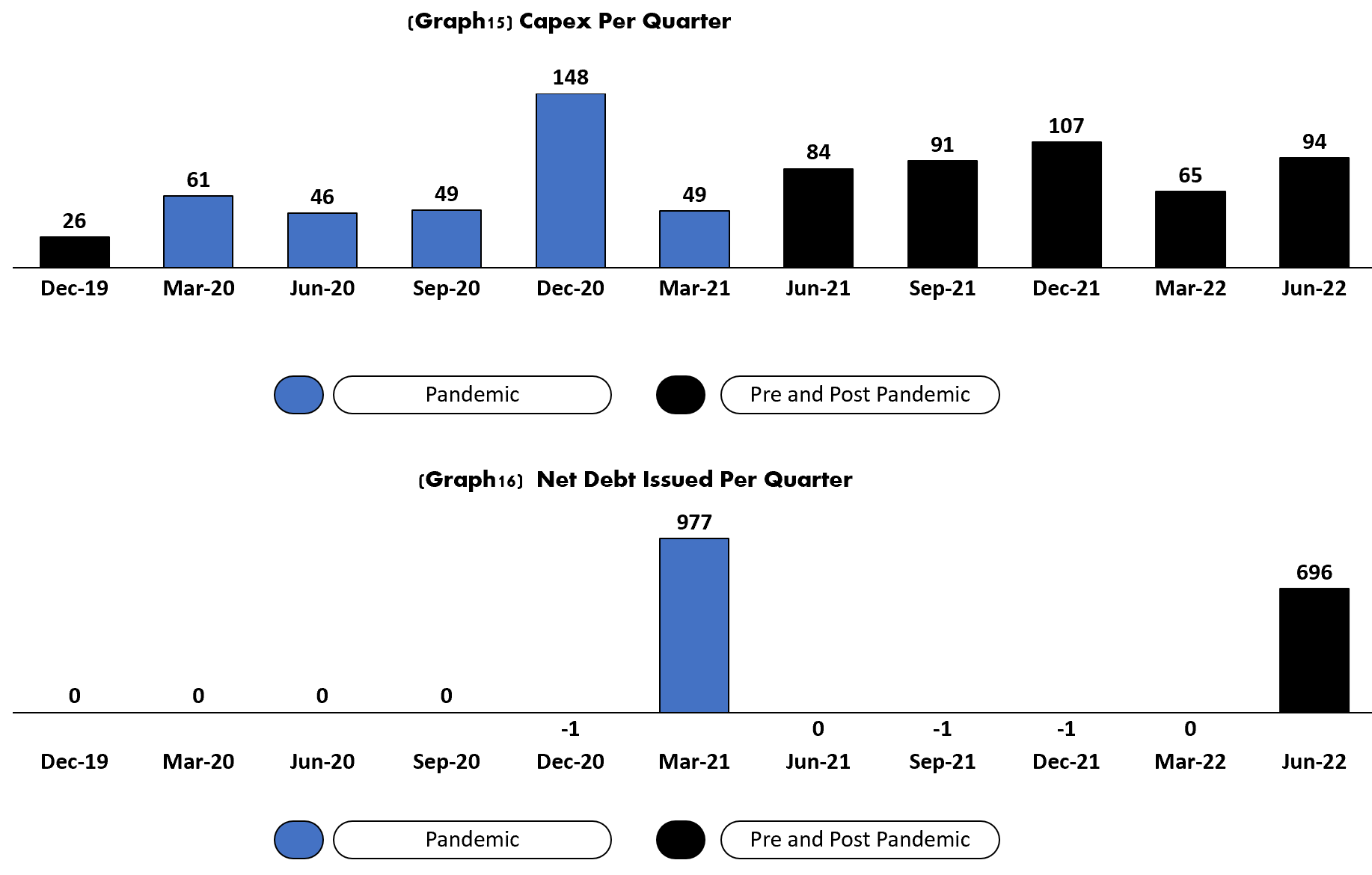

Capex invested during the quarter was $94 million, up from $65 million in Q3 2022 and $357 million over the last 12 months.

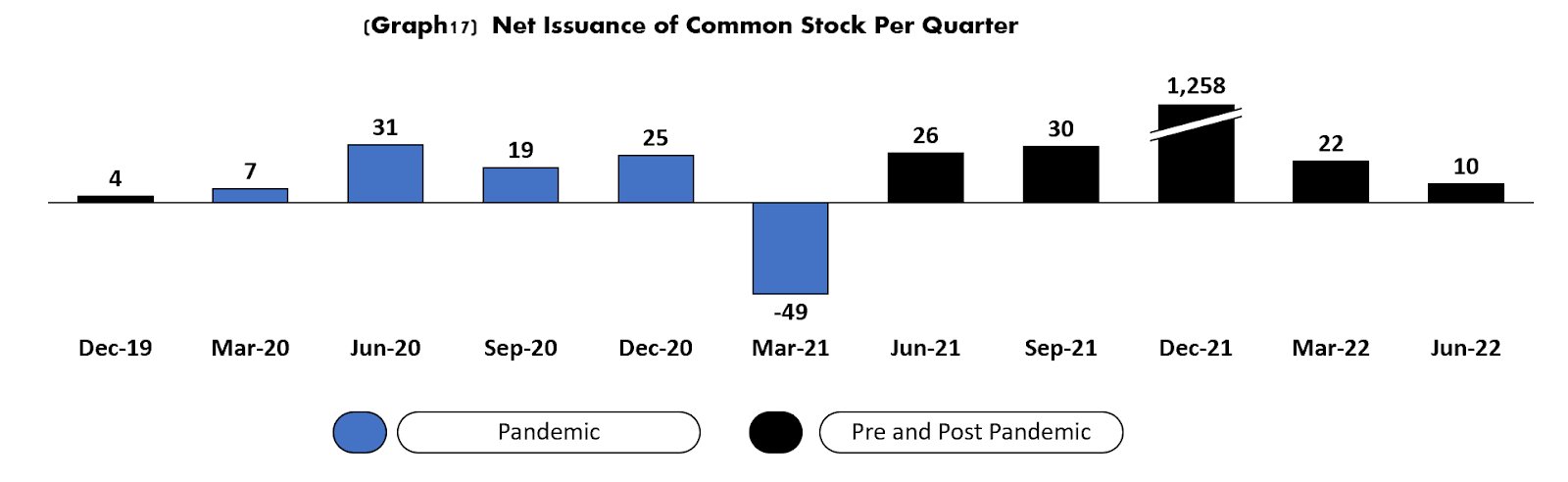

Net Debt issued during the quarter was $696 million while $10 million in common stock was issued

Balance Sheet

Cash balance at the end of the period was $1.25 billion, up from previous quarter thanks to the debt issued

Debt balance at the end of the period was $2.3 billion

Thanks for reading LongYield! Subscribe for free to receive new posts and support my work.

Redefining operating model

Peloton restructuring is going on for almost two quarters now, optics from looking at high level numbers are not great. Costs are going up, losses are growing, demand is going down, competition is growing (Apple fitness) and many other complicated operational issues (IT systems, customer care systems etc). New CEO is clearly focused on clearing the mess that he inherited, and what a mess it was, operationally the company was confused, it took the level of demand from the pandemic as the perpetual level of demand it would have if the pandemic ended. They went on to make terrible decisions like bringing manufacturing to the US, trying to fix decreasing demand with higher marketing expense, acquired a company (Precor) that will likely won’t be a part of the future strategy, etc. ( the haven’t decide yet)

So far, they have made some clear decisions that seem to be giving us an idea where the company is heading:

Took back manufacturing overseas

Cut 784 jobs in August, 570 in July

Shift last mile delivery to Third party logistics, claiming that it will reduce the cost per delivery up to 50%

Announced that will continue to reduce workforce

Prices were hike once again (after reducing them just a few quarter ago)

Bike + increases by $500

Thread increases by $800

Original bike and new guide product prices stay the same

Recruited from Amazon Liz Coddington as Chief Financial Officer

Announced that will start selling Peloton equipment and apparel on Amazon, though this might take place from 2024

Will redesigned equipment so it is easy to assemble, opening the door for DIY install and considerably cheaper delivery

Focus on pre-owned selling, rental of equipment and driving digital application penetration.

New rower products will not be rushed and it is not a priority for now.

Most of these changes make it clear that the company is trying to become more efficient and at the same time improve margins as well as trying to drive revenue with new streams or streams that have not been penetrated correctly yet.

Outlook

So far we believe that the decision and changes that the new management is making are the correct ones. In our previous piece on Peloton we highlighted the importance of the subscription business for Peloton. Peloton should be a subscription business and not a transactional business. Fitness has always been about subscription and just happens to be the part of the business that has the best margins.

Subscription is the future, and the focus is there, but in order to have a great subscription base they still need to keep a certain level of demand for connected fitness equipment. (at least until they grow the digital app and the fitness as a service product) But demand is their biggest issue for now. It has continuously come down reaching a low of about 129k units sold this past quarter. The holiday season and early 2023 will tell us a lot about the future of the company. Demand needs to pick up during that time. But an advantage that they have now is that they have 4 different type of ways they can get subscription customers:

Connected fitness equipment sales: They get the $44 per month on the subscription

Pre owned fitness equipment sales: Margin sure won’t be the focus there, but is a great tool to get to expand their TAM and have also the $44 per month on the subscription

Fitness as a service: Basically renting of the equipment, this could be a great side of the business. They get a monthly payment and if churns are low, the lifetime value of this product could be very profitable. (Even better when they have the DIY type equipment.)

Digital Application: This is the lowest ARPU but also a no brainer, and we were highly surprised on why this wasn’t pushed more before. They get great returns on content that has already been produced for the other subscriptions.

The digital app and renting, could be the two things that will help bring cash flow and also act as advertising to convert customers to buyers of the connected fitness equipment (Peloton sees renting as a 120K to 150K new renters a year). The rise of prices seems to be a decision that they took to separate the two worlds, the equipment is premium and you could still buy it, but for a premium price and the renting acts as a “lower” price, giving customers with less purchasing power the possibility to have the equipment as well.

All of this in theory are good decisions, but execution will be the key to determine if it will actually work. Everything now seems in place to bring back subscriber base, to bring customers in a cost effective way, manufacturing equipment in a cost effective way and a leaner organization that is no longer built for the demand of the Covid pandemic. So far what has happened is what we expected in our previous model. We expected that the past 6 months were going to be very bad, we also expect in our previous model that the demand will slowly adjust back to a more permanent level. What we didn’t have in our model was two things. DIY installations and Amazon deliveries. These two together, would improve cash flow dramatically from 2024. Having updated our assumptions we have the following results. Our base case is now $26 per share or about $8.8 billion, our optimistic case goes to $42 per share or about $14 billion (a lot of things have to go right for the optimistic case) and our conservative case remains at $0 or acquired.

New strategic direction makes sense for Peloton there are two big ifs, will demand for their products still exist? And if they execute well accordingly, they can’t panic again. They have a second chance, they won’t have a third.

Thanks for reading LongYield! Subscribe for free to receive new posts and support my work.

The Content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained on our substack constitutes a solicitation, recommendation, endorsement, or offer by LongYield or any third party service provider to buy or sell any securities or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. LongYield participants may or may not hold positions or interests in stocks discussed in this website.